ESCA - Escalade: A Sporting Goods Powerhouse With Strong Growth Potential

Summary

- FY22 results are nothing to write home about but could have been worse.

- Inventory levels and debt are still elevated, drawing some concern, however, management is prioritizing these.

- The financials of the company look solid for a long-term investment.

- DCF valuation that takes into account 3 years of declines in revenues still finds value.

Investment Thesis

With not the worst FY2022 results out, I wanted to see if there is an opportunity for a long-term investment in Escalade Inc ( ESCA ). With the reduction in inventory levels at the forefront over the next couple of years, the company can manage to achieve better free cash flow coupled with prioritizing the debt reduction also shows the management in good light, which in itself warrants a further look into the company. I decided to model a DCF model with improving free cash flow over time and with revenues going down for the next couple of years due to a supposedly upcoming recession. With all of the revenue growth assumptions and other factors taken into account, the company is a buy at these current levels, however, caution is warranted due to the unknown global macro environment.

Financial Year 2022

Revenues came in flat, operating, and net income declined over the year, mainly due to the softening consumer demand and excess inventories in the retail channel. The company also faced supply chain disruptions and higher freight costs that impacted its margins. However, the company was able to offset some of these challenges by acquiring new brands and expanding its e-commerce presence.

Due to supply chain issues, the company has been buying up extra inventory to account for that, however, the company is not happy with the amount of inventory still left to sell, which affected operating results in 2022 and might continue in the future if they are not able to bring it down. The management has reduced inventory by 13m in Q4 which is a good sign. Revenues are coming back down from pandemic-related consumer demand to more normalized levels. Does that mean the company is going to see a decline in revenues over the next few years? Time will tell, but in my model, I have accounted for some sort of reduction. Naturally, the EBITDA number also came in lower compared to last year, sitting at $32.5m in 2022 compared to $36.9m in 2021.

Revenue and Income figures (Escalade Inc IR website)

{kind=link}

Growth Catalysts

The management is eager to grow its e-commerce platform so it can become more efficient at selling directly to consumers. I like this idea because it means that they want to be less dependent on third-party merchants. I had a small gripe with how over 35% of total revenues came from two clients for quite a while now. The company did not mention who they are, however, if we go back to FY21 results, they state that the two largest contributors of revenue with similar percentages were Amazon Inc ( AMZN ) and DICK'S Sporting Goods ( DKS ). I would venture a guess that this has not changed year to year. I'm not saying that Amazon or DKS will go out of business anytime soon, however, it is better not to rely on one client for such a large percentage of total revenue. The E-commerce revenue segment has been flat y-o-y, while mass merchants saw a decline in revenue.

Escalade Inc said it expects to benefit from the continued consumer demand for health and wellness products, especially in the fitness, archery, and basketball categories. The company also plans to invest in product innovation, digital marketing, e-commerce capabilities, and operational efficiency to enhance its competitive position and profitability.

It seems to me that the company might be able to continue the shift to direct-to-consumer e-commerce and if they can sell their goods through Amazon and other affiliates on top of that, it can only mean better margins and more cash for the company.

The company is also open to more acquisitions in the future to bolster revenues. Most recently they added Brunswick Billiards to their wide portfolio of goods.

Pickleball

One very interesting metric I found while researching was the explosive popularity of pickleball in the US. The number of players in 2021 was 4.8m, and as of August 2022, that number reached 36m people! That is a massive increase and could bring an extra boost to the company's revenues in the future as they offer one of the leading pickleball paddles currently- the Onix paddle which has received great reviews and has gained popularity.

The pickleball market size in 2021 was around $153m and is expected to grow at around 7.7% CAGR through 2028 which will be $287m if my math is right.

The above market size numbers are only in the US. The global pickleball market size is estimated to be $1.3B and is expected to grow at 10.19% CAGR through 2028, giving a $2.37B market valuation. Since Escalade is one of the leading suppliers of the paddles, they have a good chance of grabbing a good chunk of that market's growth. Just a quick amazon search for top-rated paddles shows Onix paddle to be one of the best rated with 2nd most reviews behind Niupipo paddle.

I'm not sure how much of that market can Escalade capture, but even 1% of the 2028 number translates to $23.7m. The company unfortunately does not release specifics on how much revenue they are getting from this segment, maybe in the future.

Financials

The elephant in the room, the large chunk of debt on the books has analysts worried that a high leverage ratio and interest expenses might limit the company's profitability and financial flexibility in the future. I don't like debt also, however, I do believe that the debt the company has taken on to fund the acquisitions of Rave Sports, Victory Tailgate, and Brunswick Billiards in the last few years was a smart decision. We will have to wait for those results to show up in the future. The management also said that they are going to prioritize reducing its debt levels further. During the last quarter of 2022, the company managed to sell $13m of its inventory and managed to reduce its debt by $12m at the same time. So, I don't believe that debt is going to be a major deterrent for investors. The company is aiming to achieve a net leverage ratio of 1.5x to 2.5x EBITDA, it currently is at 2.7x.

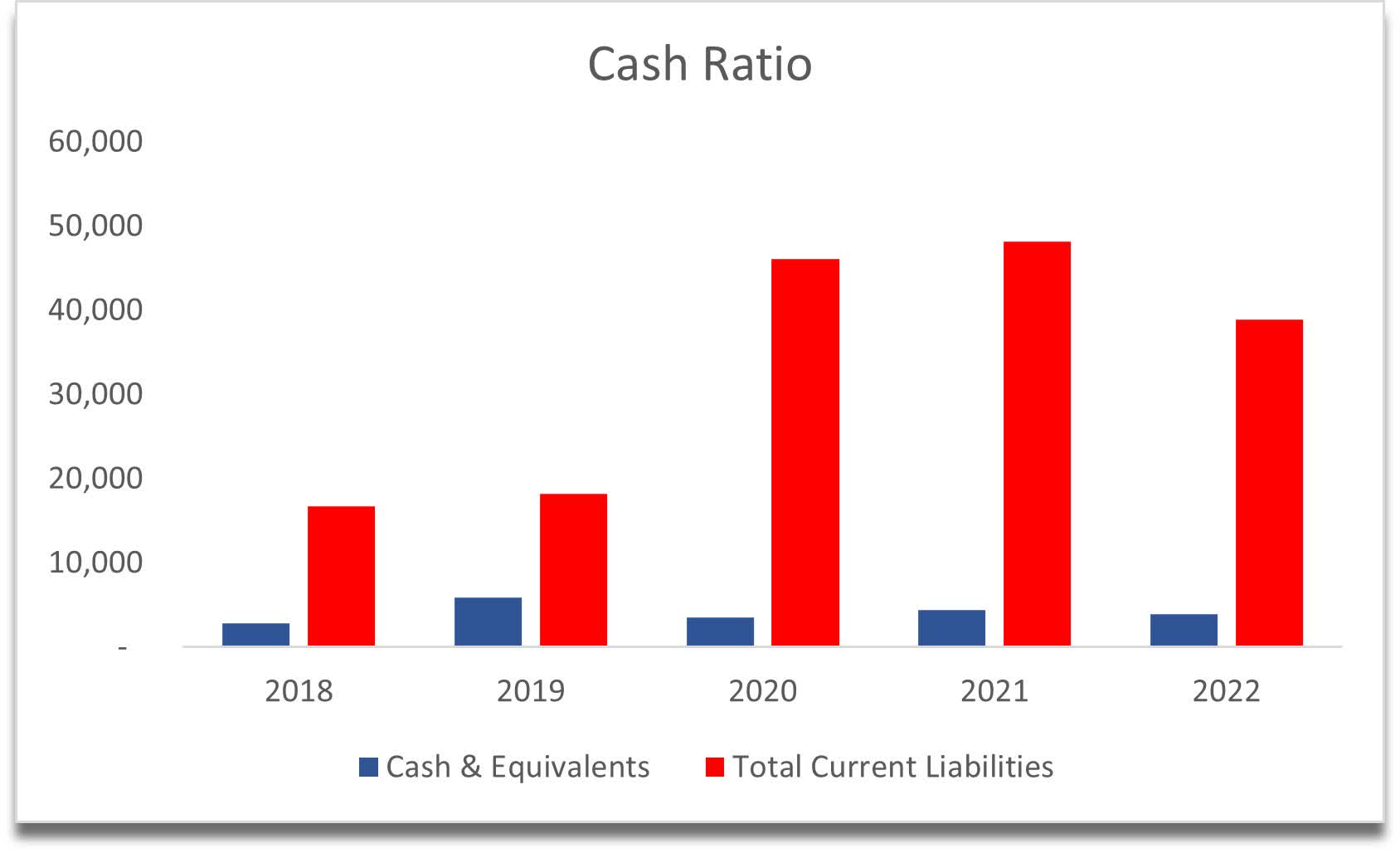

Cash ratio which is a much stricter metric that a lot of investors like to use, measures how well the company can cover its short-term obligations with cash on hand. The company would not pass this metric, however, just by looking at some of the company's competitors, Escalade is not an outlier here either.

{kind=link}

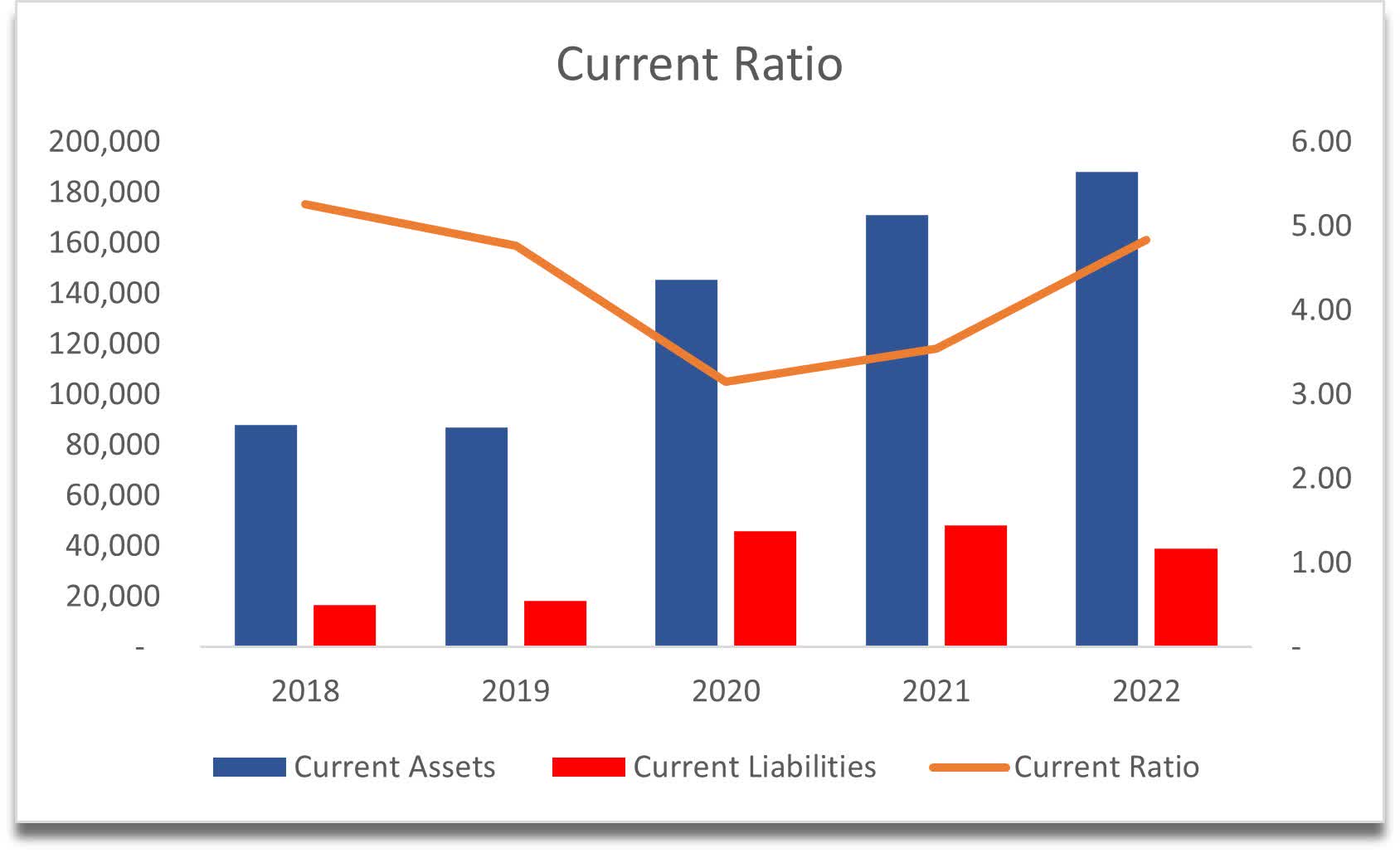

If we are going to be less strict on the liquidity ratios, the company has a very good current ratio and it looks like it had bounced back from a low of 3.16 in 2020, which was still very good, to 4.8 at the end of 2022. The company is liquid and I do not see anything that would tell me otherwise.

Current Ratio (Own Calculations)

{kind=link}

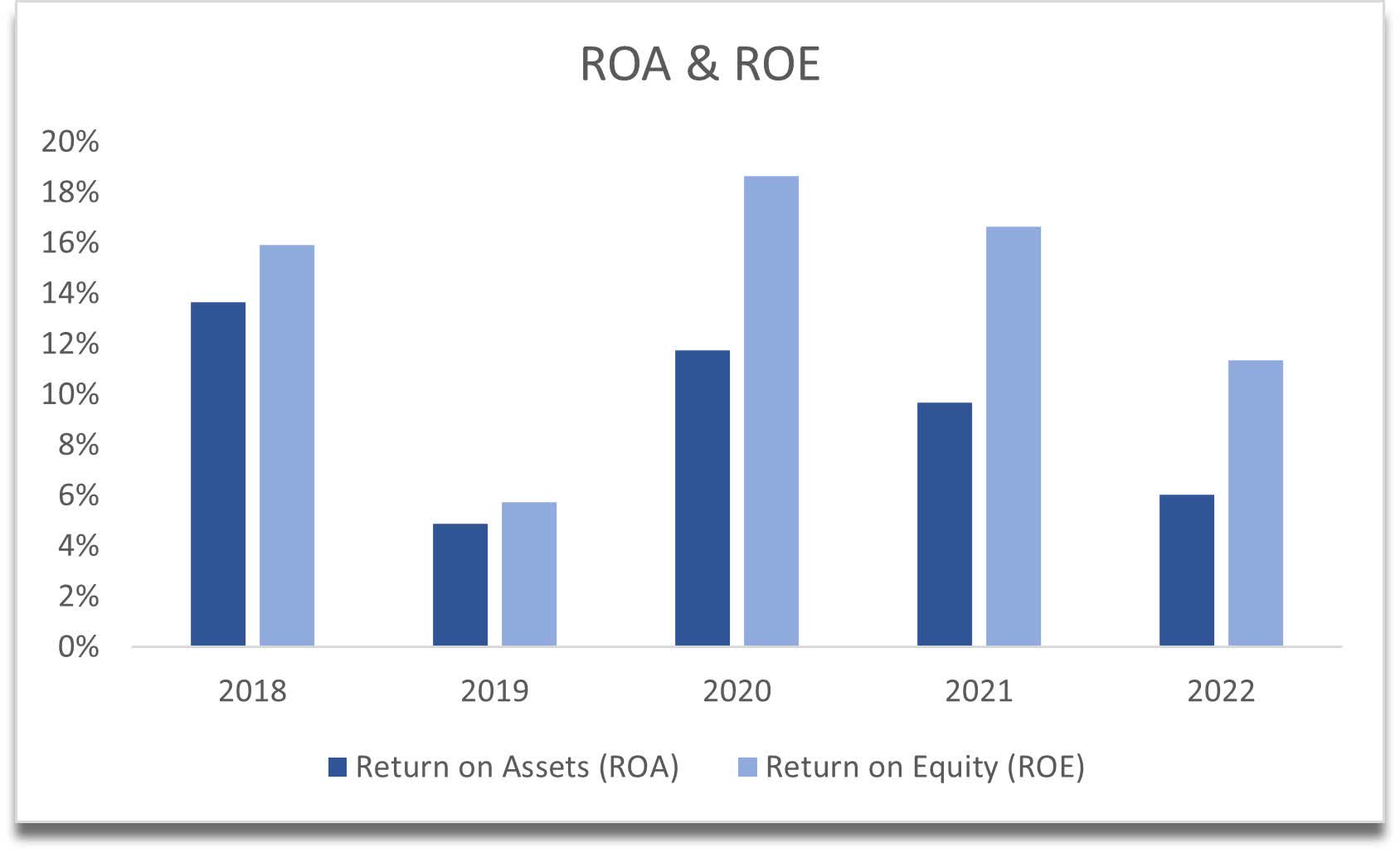

Return on assets and equity are also respectable however, these metrics have been trending down for the last 3 years. I would like to see them stabilizing in the near future or increasing. This trend down can be explained by the demand boom during the pandemic and the metric is just coming back to its normal levels.

ROA and ROE (Own Calculations)

{kind=link}

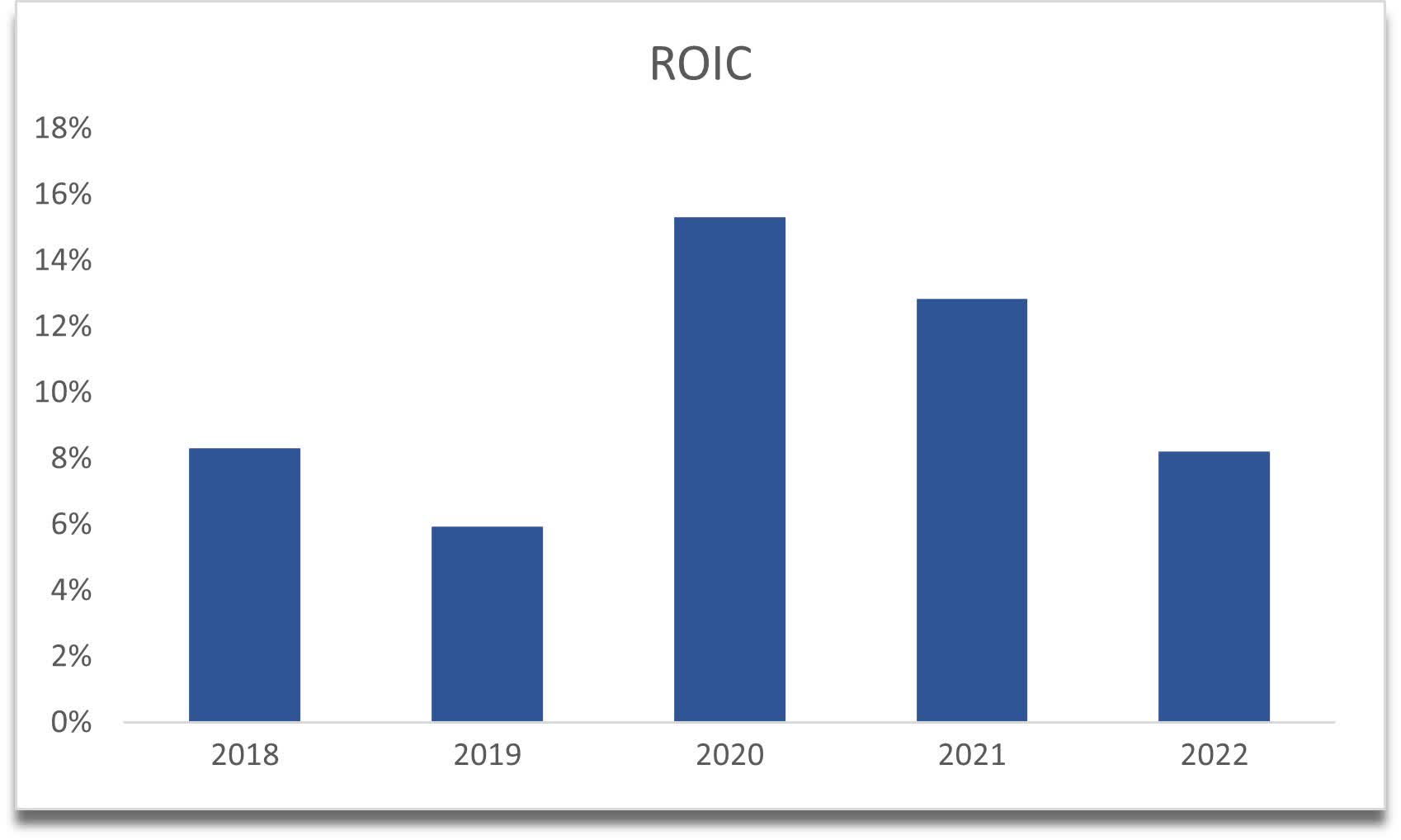

Return on invested capital is seeing a similar trend down to normalized levels of pre-pandemic. The return is still good, but I would like it to get back to an uptrend in the future.

{kind=link}

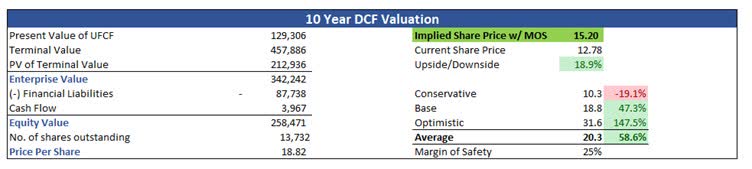

DCF Valuation

For my model, I decided to have a look at how the company's performance would be affected by taking into account a recession in the next 12-24 months. For the worst-case scenario, the revenue for 2023 and 2024 will go down by 10% and by 7% in 2025, then return to 10% growth for the next 2 years, 8 for the next 2, 6%, 5%, and 2% for the remainder of the years. I took these numbers because in the last 10 years, it only had 1 down year revenues and it was barely 1%, however, if we go back to the financial crisis, the company did see a 20% decrease in revenues per year for two consecutive years only to go back up again, so -10% for the next 2 and -7% for the third year, seems like a good proxy for some sort of a recession, which may not be as bad as 2008 one from what the Fed is saying right now. These estimates give me a 2% average growth per year.

For my base case scenario, I went with a 2% decrease in revenue in 2023 and 2024 and subsequently pick back up and normalize, which gives me 4% average growth a year. For the optimistic case, I went with a 6% average growth a year for the next 10. I kept the margins somewhat the same as the company has currently, with the optimistic case having an increase in profitability margins by 1% and the worst case having a decrease of 1%. Margins are very tight so there isn't much wiggle room to play around.

On top of what I believe are quite conservative assumptions, I also added a 25% margin of safety to the final implied share price of the company, to give me a fair value of $15.20 per share, meaning the company is trading at a discount if you do believe the assumptions I've laid out.

10-year DCF (Own Calculations)

{kind=link}

Conclusion

The company is in a good position overall to reward its shareholders in the long run in my opinion. Solid acquisitions will add value to the shareholders, and if they can reduce their inventory levels, pay off debt and produce good cashflows, the company is a long-term buy in my book. There are some factors to take into account before starting any new position or adding on to the current one. One of the big factors to consider is a recession. Will we see a major downturn in the economy very soon? Will it be not as bad, or will it be as bad or even worse than the 2008 one? If that happens, then my model did not consider a massive drop in demand for sports goods and may become invalid. Patience might be the theme here, but I wouldn't be opposed to opening a small position and seeing where the economy will go in the next year or two.

For further details see:

Escalade: A Sporting Goods Powerhouse With Strong Growth Potential