IAC - Eschewing 'Empty Calories' Sees IAC Margin Improvement

2023-08-10 14:22:06 ET

Summary

- IAC saw a major hit due to consolidated Angi seeing major declines as revenues plummeted.

- We take what management says at face value about changing the strategy, and like that profitability is improving.

- While Angi investors may have freaked out, for IAC which is a pretty undervalued brand portfolio anything that moves to sustainability of its businesses is good.

- We definitely don't think the declines were justified from this one earnings release, but are instead worried about macro and myriad emerging structural risks.

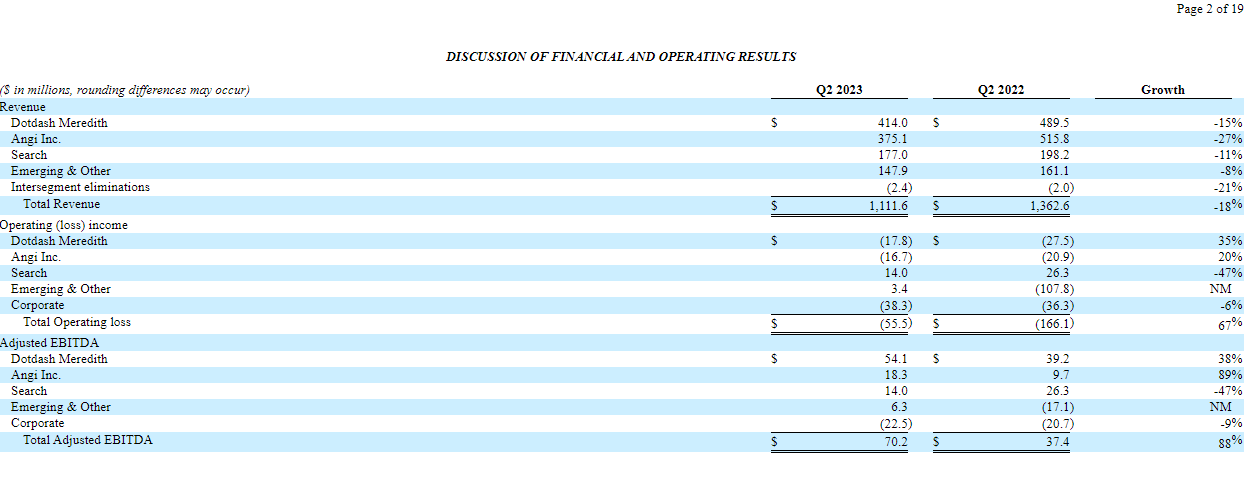

IAC ( IAC ) took a major beating as its consolidated Angi ( ANGI ) business saw declines in its own public market cap. Revenue declines across the board, mostly because of some restructuring efforts on the products in IAC's portfolio, came in exchange for higher margins. Management asserts that the products and demand channels that have been abandoned would not have produced customers with high LTVs and had too poor of a customer experience. Considering that there is a SoTP story in IAC, shareholders should come to appreciate a move to shore up profitability of its businesses so that discovery of the discount becomes tenable. Still, there is surely some pressure from general macro, and Angi is likely seeing that somewhat in the roofing business.

Q2 Discussion

Let's start with valuation, updated for after these declines.

Valuation (VTS)

They have almost 20% of MGM Resorts ( MGM ) which we've covered in the past, doing a lot in the US online gambling market thanks to BetMGM. Otherwise they have around 85% of Angi, which is publicly listed, the NCI being included in the debt side of the NFP. Then we take a proposed EV based on some comp multiples for each of the IAC properties, subtract the NFP and get our proposed equity value. We zeroed out properties that we weren't sure how to value.

The investment in MGM is a massive determinant of IAC's value. Still, the results of the operating business, which includes Angi revenues, but also revenues from IAC's digital and physical magazines and news sites, matter a lot as well. The story this quarter is that declines in revenue have been pretty meaningful across properties, especially in print and at Angi, but profits have improved. Angi has been the locus of a lot of change, the disposing of so called empty calorie businesses.

{kind=link}

Segment Revenues (SEC.gov)

Certain demand channels have been discontinued , and this was a restructuring effort started some quarters ago, because LTVs in these channels were either too small for a profit or not large enough for relevant incremental profits. These businesses were at their heights about this time last year, so comps on the revenue side are tough, even if the peaking revenues last year would have less profits to show for them. There is also the matter of roofing, which had massive declines. This was in part due to tougher comps, which are now being compared to a situation where there is a slowdown in construction and work being done on houses, partially because so much work had been frontloaded into 2022. Still, the business is moving towards profitability thanks to the end of paying lots of dollars for worthless customers. These moves also seem to have been enacted within Care.com, all these are directory businesses.

{kind=link}

EBITDA Segment (SEC.gov)

The declines in DDM were less idiosyncratic and more a signal of challenges in the spending markets for advertising. There are structural risks here too, as content becomes more short form. Also there is concern around what advertisers can accomplish in digital when we move to a cookie-less world. Things should get quite a bit harder to advertise. D/Cipher launch by DDM should help provide some value-add anyway, also reaching Apple OS consumers that have been untouchable for some years now and represent a massive part of the digital population. Still, management expects sequential growth and flat YoY performance by year's end thanks mainly to growth in Meredith, which is the print properties.

Ask is not something we are optimistic about at all as proprietary LLMs take center stage among the main search engine players. Mobile is doing OK but we don't expect anything from this segment going forward as things start to get heated while the pie in advertising has gotten smaller.

Bottom Line

We think that for any SoTP case to materialise, the businesses need to become more sustainable. IAC is making efforts to do that and they are working pretty well. It's likely that the upside is going to be a lot smaller than what is presented in the valuation, also because some of those multiples are a little bit on the stretched side, and there are difficult to map risks around AI and also the changes in digital advertising related to protecting people's privacy. Still, we think priority of profits at the expense of revenue figures makes sense for a company whose equity value is almost matched by the single holding in MGM. Nonetheless, we aren't likely to take a position in the stock considering the business lines, potential emerging risks, and the obvious and immediate potential macro risks in a rate hiking and ad budget shrinking environment.

For further details see:

Eschewing 'Empty Calories' Sees IAC Margin Improvement