ESE - ESCO Technologies: A Fairly Valued Stock

2023-08-25 02:33:02 ET

Summary

- ESCO Technologies reported solid Q3 FY23 results with a 13.5% increase in net sales compared to Q3 FY22.

- Strong performance in the utility solutions group and aerospace & defense segments drove the sales growth.

- Despite positive expectations for the fourth quarter, the technical chart suggests a bearish outlook, leading to a hold rating on ESE stock.

ESCO Technologies ( ESE ) produces engineered products for commercial markets worldwide. ESE recently announced solid Q3 FY23 results. I will review its Q3 FY23 result in the report. I believe ESE is a fairly valued stock; hence, I assign a hold rating on ESE.

Financial Analysis

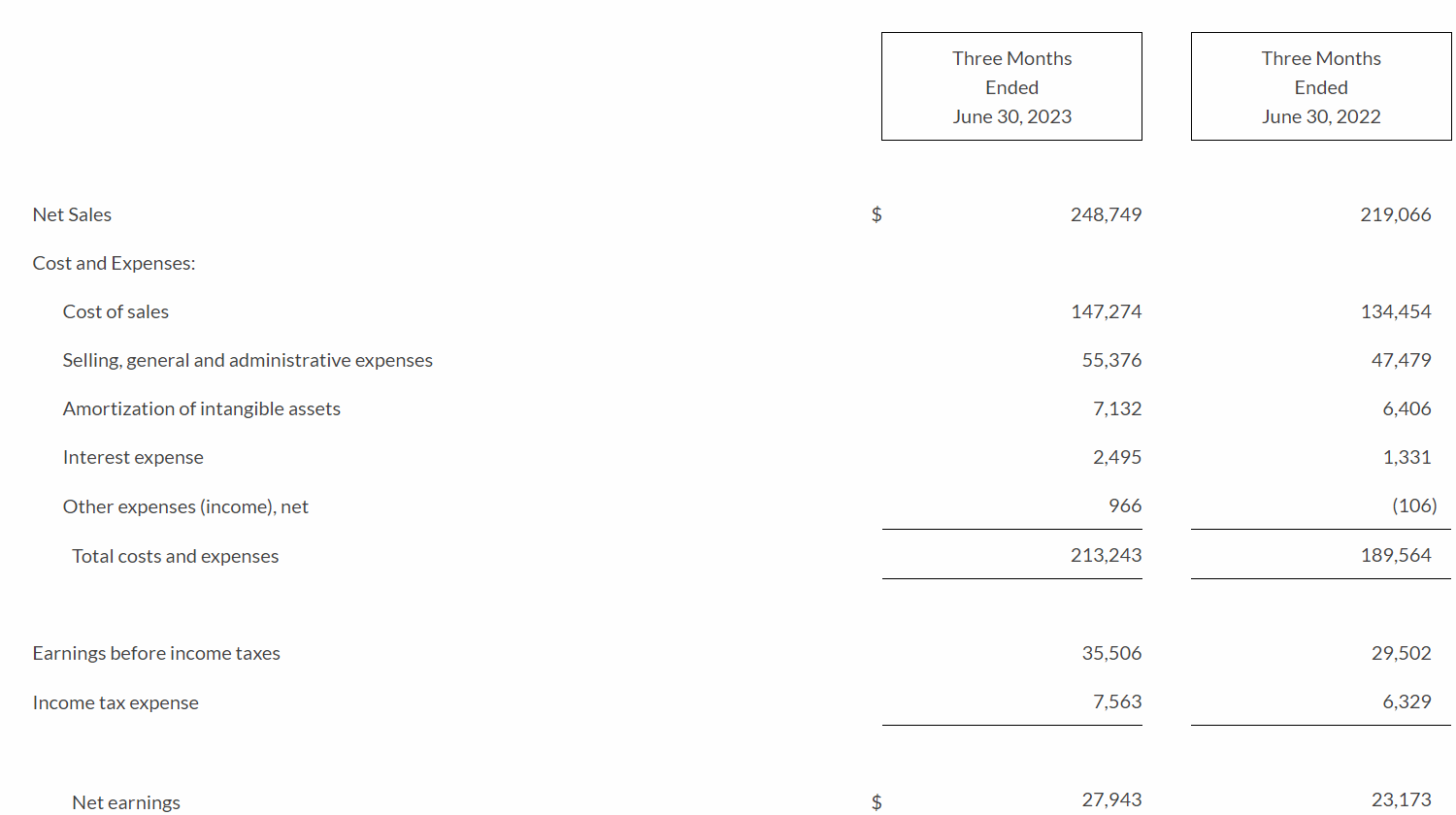

ESE recently posted its Q3 FY23 results . The net sales for Q3 FY23 were $248.7 million, an increase of 13.5% compared to Q3 FY22. I think strong performance in its utility solutions group [USG] and aerospace & defense segments was the primary reason behind the sales increase. The sales from the USG segment grew by 33.8% in Q3 FY23 compared to Q3 FY22. I believe strong demand for the company's protection testing product line and solid growth in its renewables business were the major reasons behind the outperformance in the USG segment. The adjusted EBIT margin in this segment for Q3 FY23 was 22.8%, which was 19.5% in Q3 FY22. I think higher pricing was the major reason behind the improvement. Now talking about the aerospace & defense segment, the sales grew by 11.7% in Q3 FY23 compared to Q3 FY22. The sales in the commercial aerospace business grew by 24% in Q3 FY23 compared to Q3 FY22, and sales in defense aerospace grew by 54%. Solid growth in both of these businesses resulted in revenue increase in the aerospace & defense segment.

{kind=link}

The net earnings also increased by 20.5% in Q3 FY23 compared to Q3 FY22. In my view, the financial result of ESE was fantastic because in Q3 FY23, the company had won large multiyear space orders, so comparing the two quarters was difficult. Still, the company managed to grow its sales and posted positive revenue growth in Q3 FY23, which is quite impressive. The company expects revenue growth in FY23 to be around 10%, which gives us the figure of $950 million, and with only one quarter remaining, the sales they have to achieve in order to achieve the sales target for FY23 is around $266 million which I think is quite achievable. In addition, they had a backlog of $700 million at the end of June 2023. So, I think with a healthy backlog and strong demand for their business, I see them achieving the revenue targets for FY23. However, I would like to point out a headwind that might hamper its growth in the fourth quarter. The aerospace market is facing supply chain issues, and especially the lower tier suppliers are having trouble, which has a domino effect, and replacing suppliers is not a simple task. Hence, this is a challenge that they might face in the fourth quarter, which can hamper its sales growth.

Technical Analysis

{kind=link}

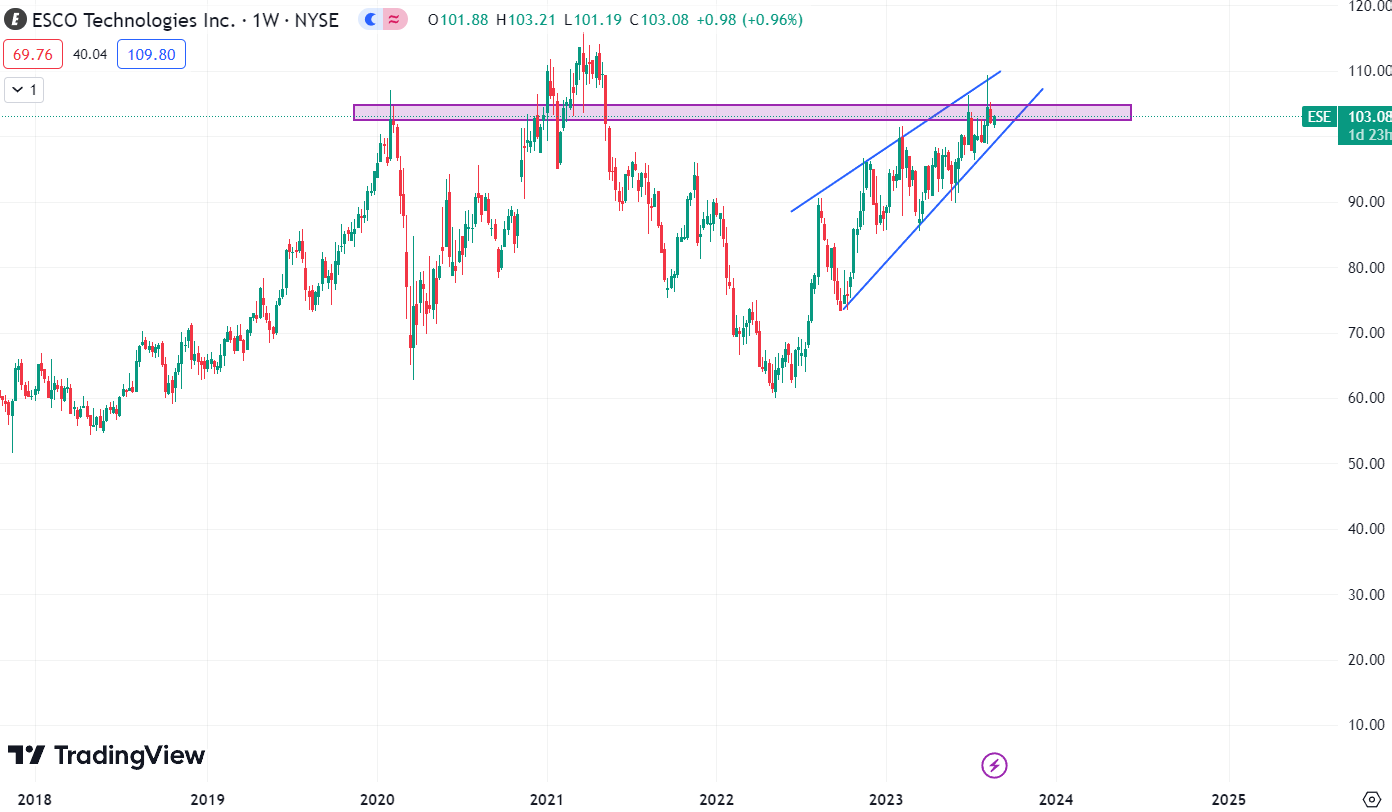

ESE is trading at $103. Based on the technical chart of ESE, I am bearish on ESE, and I expect that we might see a correction from the current level. There are two reasons I am bearish on this stock. The first reason is that if we see the price chart, the stock is at a strong resistance zone of $105. This is the same zone where the stock faced resistance in 2020 and fell more than 30% later in 2021; the stock broke out of the $105 level, but it proved to be a fake breakout, and the stock wasn't able to sustain itself above $105 for much longer, and the stock again fell down more than 30%. This is the third time the stock has tried to break the $105 level, but recently, after touching the level, the stock made a candle with a huge wick, and the candle recently made is similar to the candle of 2020, which shows weakness. Hence, I believe we might see a correction in this stock. In addition, the stock is making a rising wedge pattern, which is a bearish pattern. Hence, after looking at the price action, I will recommend avoiding it for now.

Should One Invest In ESE?

First, look at ESE's valuation. ESE has a P/E [TTM] ratio of 28.16x, which is higher than the sector ratio of 16.98x. ESE has a PEG [TTM] ratio of 1x compared to the sector ratio of 0.76x. We can see that ESE is trading at a higher premium, but I believe ESE deserves to trade at a higher premium because the growth that the company has shown has been impressive, and if we compare ESE to its peers like KAI , AIN , MWA , we can see that ESE's growth has been impressive when compared to its peers. ESE has a revenue growth [YOY] of 16.5%, KAI has a revenue growth [YOY] of 7.5%, AIN has a revenue growth [YOY] of 9.6%, and MWA has a revenue growth [YOY] of 7.7%. So, the performance of ESE explains its high valuation.

But despite posting strong results and the expectations being positive for the fourth quarter, I am not assigning a buy rating on ESE because I believe ESE is a fairly valued stock. I don't see much value currently in this stock because I think the solid performance by the company has been rewarded by the market by high valuation, and I don't see much upside from here. In addition, the technical chart of ESE is looking quite bearish. Hence, I assign a hold rating on ESE.

Risk

Sales to the U.S. Government and its prime and secondary contractors account for a sizeable amount of their overall revenue. From 26% to 28% of their revenues over the last three fiscal years have come from sales to the U.S. government or its contractors, especially in the A&D segment. These sales rely on government support for the underlying programs, which is typically determined by annual Congressional appropriations. Government funding for initiatives that pertain to the business or its clients may be reduced, terminated, or delayed. These funding effects could negatively impact their sales and profits and cause a restructuring of their business, which could negatively impact their financial situation or operational outcomes. Major American government initiatives like NASA's Space Launch System ((SLS)) and the U.S. Navy submarine fleet account for a sizeable amount of VACCO, Westland, and Globe's revenues. Government expenditure on these programs could be cut back or delayed, which could have a negative effect on their financial performance that lasts longer than a year.

Bottom Line

ESE posted impressive Q3 FY23 results, and I see them achieving revenue targets for FY23. But I believe it is a fairly valued stock, and I don't see much upside from here. In addition, the technical chart of ESE is looking quite bearish. Hence, I assign a hold rating on ESE.

For further details see:

ESCO Technologies: A Fairly Valued Stock