EOSE - ESS Tech Levels Up

2023-09-27 09:30:00 ET

Summary

- The challenge of bringing down the cost of renewables is solved. The new challenge is managing all this cheap power with storage, software, and new transmission/distribution.

- Right now, LFP lithium batteries are tested, validated, and available in large quantities. They solve today’s problems, but not tomorrow’s, and bring a host of problems.

- What’s needed is long-duration energy storage. There are many competing technologies, and we are in the pilot program stage.

- ESS Tech checks off a lot of the new requirements.

- The new Honeywell deal provides cash, validation, and a much larger sales team.

A Long Road

Like many pandemic SPACs, ESS Tech, Inc. (GWH) is trading at a fraction of its $10 opening price. I day-traded it on SPAC Day, but have not owned it since, because they went public too early in my opinion, and the story is not ripe yet.

Over their entire existence, they have only $3.7 million in sales, all in the past 5 quarters, most of that in the last quarter. We are still at the stage of pilot projects here. The earliest we would see wide scale deployment of their batteries would be around 2030 with a ramp beginning a few years earlier.

But let's zoom in on the last week of the price chart.

What happened there is that Honeywell (HON) is making a strategic investment in ESS, one among several they are making in this space, energy storage. They have been very aggressive in partnerships in the past few years.

The reason is that energy storage solves the big problem with renewables.

The Problem With Renewables

The pace of new solar, wind and battery investment in the US is staggering, driven by three things

Thing One: In the next 10 years, the US has to add capacity for another 300 terawatt-hours of annual demand in the face of accelerating retirements of 1980s-1990s vintage coal and gas assets nearing end of life, or no longer economically feasible.

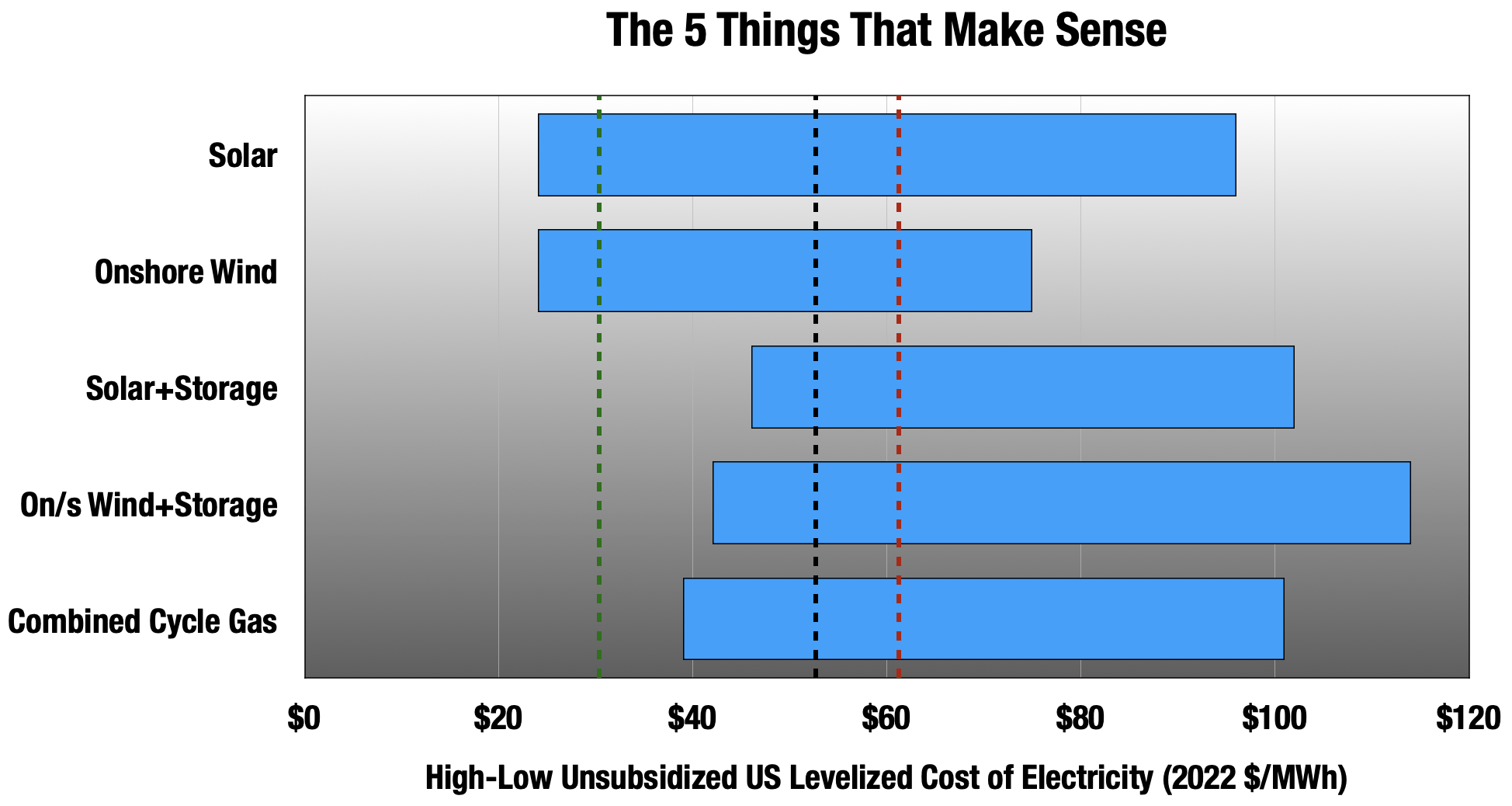

Thing Two: Absent subsidies, wind and solar are the cheapest forms of new generation, and the gulf widens every year. The only other thing in the same ballpark now is combined cycle gas.

Dashed lines are the average marginal cost from existing assets in: green = nukes; black = coal; red = combined cycle gas. The dashed lines for coal and gas reflect 2022 prices, so are a little misleading. (Lazard LCOE+)

{kind=link}

The levelized cost of electricity [LCOE] is a measure of the average cost to produce a megawatt-hour of power over the lifetime of a facility, including capital, operational and consumables costs. Those are the 5 types of new construction that make sense now in an unsubsidized world. Everything else is much more expensive. The dashed lines are the average marginal costs of existing nuclear (in green), coal (in black) and combined cycle gas (in red) in 2022. In most US geographies in 2022, new solar or wind unsubsidized costs were lower than the marginal cost of power at existing coal and gas plants, hastening their retirements.

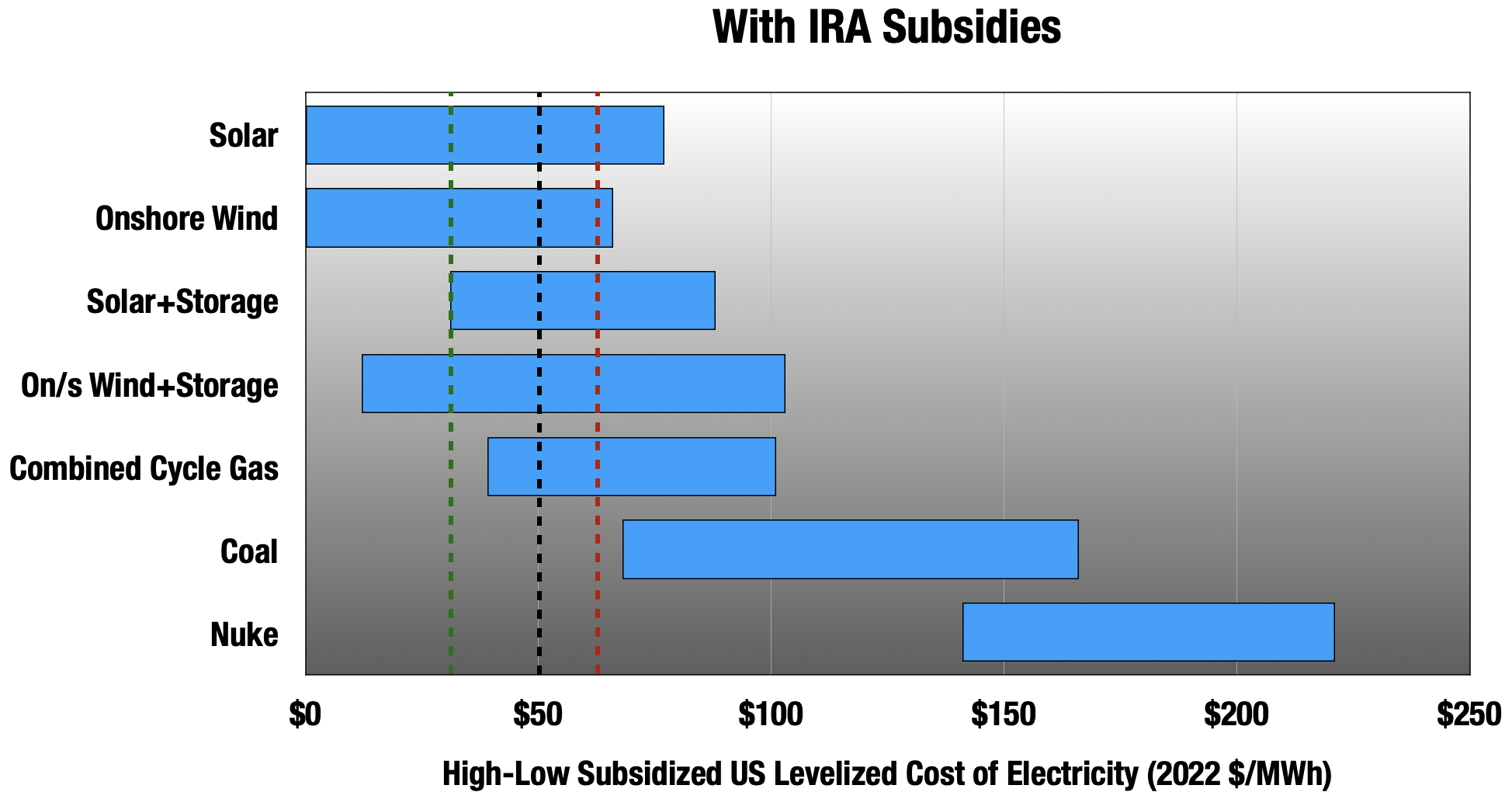

Thing Three: There are subsidies at the Federal and state levels that drive the cost even lower. Here's the subsidized analysis, only including the newest Federal subsidies in the Inflation Reduction Act [IRA]:

Dashed lines are the average marginal cost from existing assets in: green = nukes; black = coal; red = combined cycle gas. The dashed lines for coal and gas reflect 2022 prices, so are a little misleading. (Lazard LCOE+)

{kind=link}

In very limited geographies, and on projects eligible for all three major subsidies in the law, the subsidized cost of solar and wind are substantially zero. That's probably theoretical, and no one will be able to thread that needle. But even in the most expensive geographies, renewables remain a great deal in the subsidized analysis.

- The U.S. needs a lot more capacity to meet demand and replace retirements.

- Without subsidies, solar and wind are the best deals in almost every U.S. geography.

- With subsidies, it's a slam dunk.

That's what's driving everything now. The challenge of bringing down the cost of renewables is complete. The new challenges will be managing all this cheap power with cheaper and more flexible energy storage than we currently have, software, and new transmission/distribution.

The big problem with renewables is intermittency. The sun only shines during the day, and sometimes it's cloudy, even in the Arizona desert. Wind blows when it blows. There are also seasonal issues. Here are the problems that need solving:

- Diurnal mismatch. Peak demand on most days is when everyone gets home from work and school, and that's right around when the sun is setting and solar is turning off for the day.

- Fall/winter seasonal. Solar is at its low production seasonally, and more heating is starting to come from electrical sources.

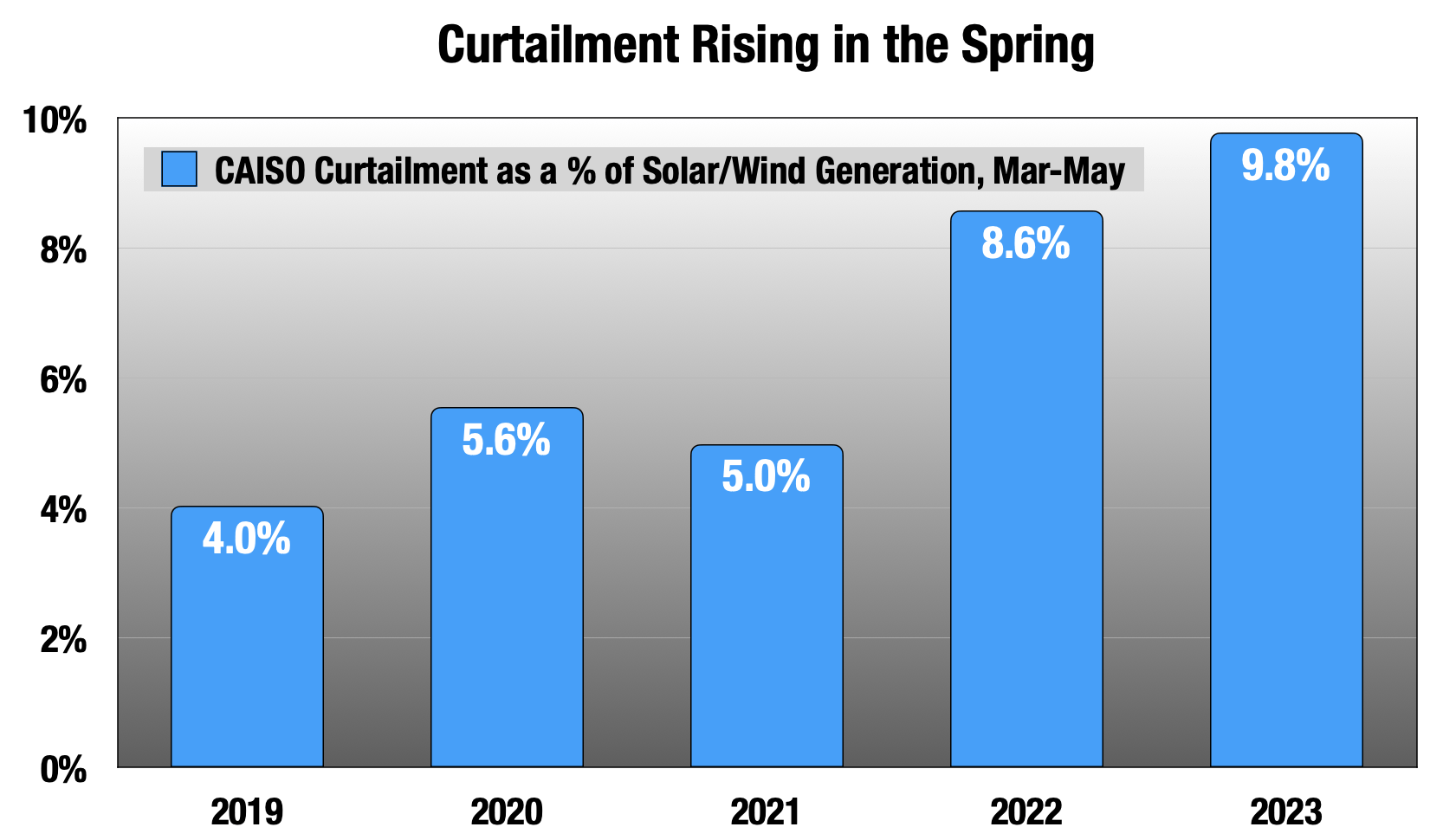

- Curtailment. Spring is curtailment season. Solar is well off its December/January low, and climbing close to the June high. But in most places, this is also a season of relatively low demand. Solar producers are forced to curtail their production, because local grids can't take all the power they are producing. The excess power is wasted. As these systems get bigger the problem grows bigger. In March-May 2023 almost 10% of CAISO (most of California) solar generation was curtailed.

- Resilience. Weather and other natural disaster events.

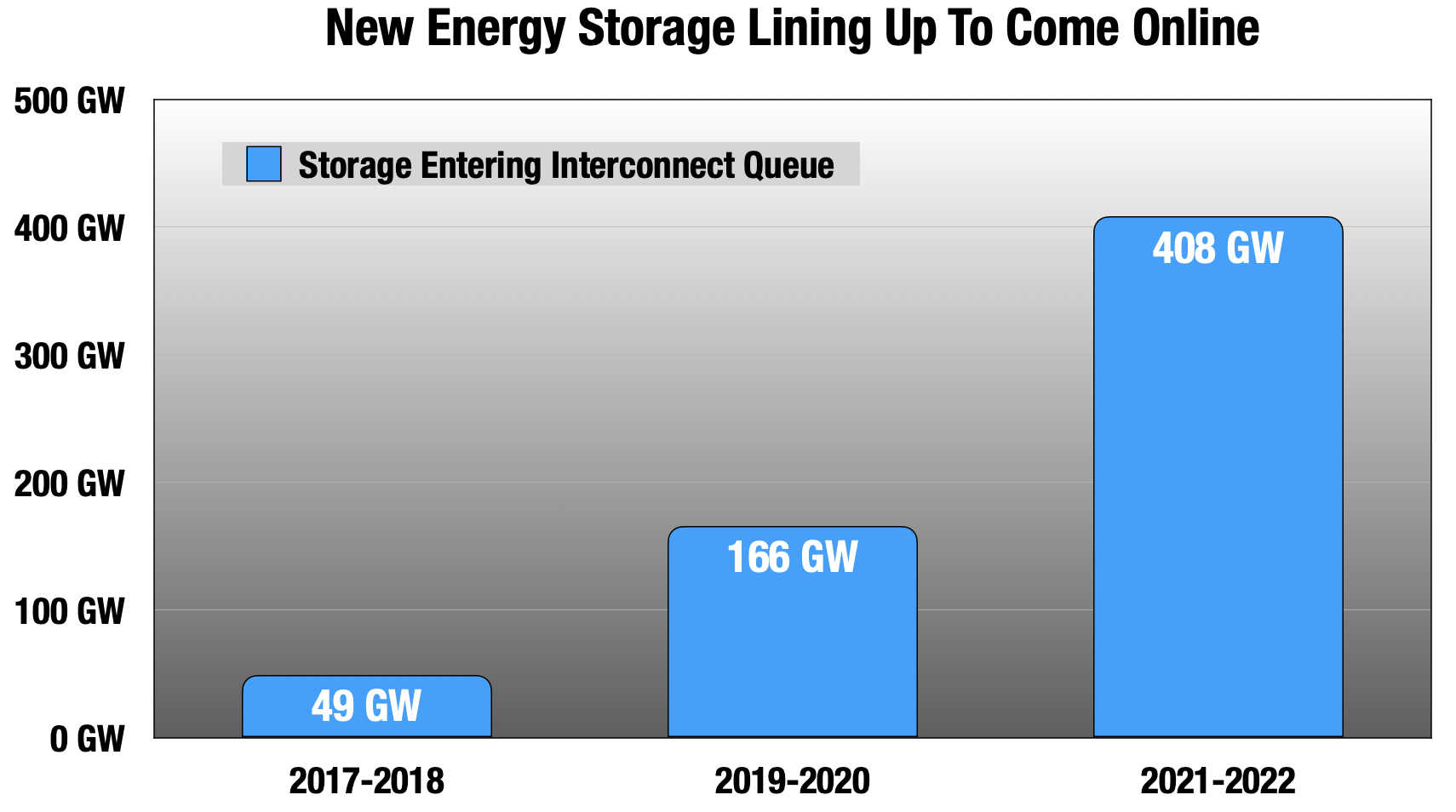

In response, we see a ton of energy storage entering the interconnect queue, the first regulatory step in getting a new asset onto the grid. Two charts tell the story here.

First, the surge in storage capacity entering the interconnect queue:

{kind=link}

408 gigawatts is about a third of all U.S. generating capacity, and almost half of peak demand. But there is a huge backlog in interconnect queues , a major hurdle right now, and a minority of that will get built. Most of it is co-located storage with new wind or solar, which makes the most sense.

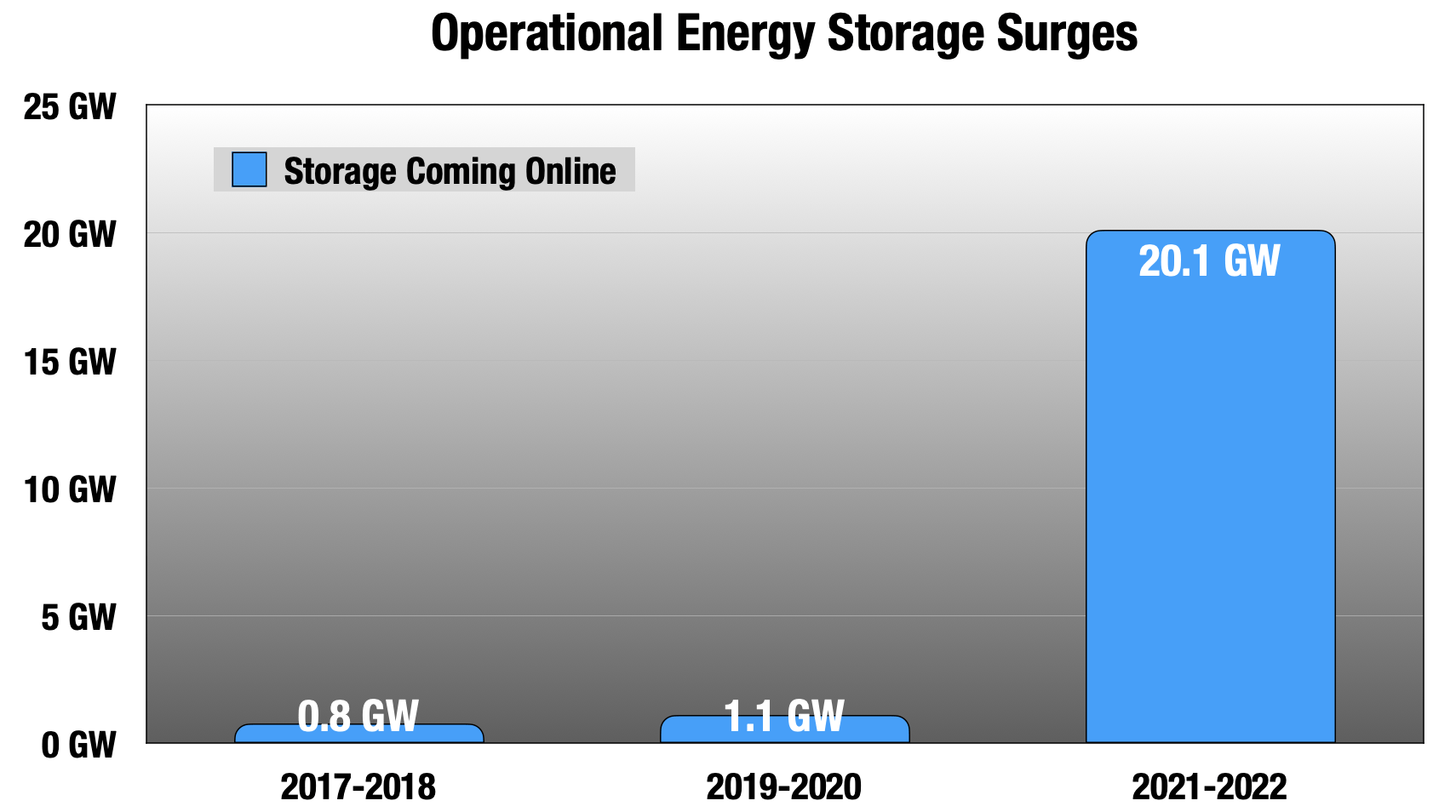

Here's what has been built so far:

{kind=link}

That's 10x as much storage in those last two years than in all previous years combined.

Right now, that's almost all lithium batteries, trending towards iron-phosphate cathodes [LFP] for their safety, reliability, and longer cycle-life than cobalt-nickel chemistries. It sacrifices some of lithium's energy density, much less of a concern for a stationary installation at a solar or wind farm than in an EV or mobile device.

But there are problems with lithium for this application.

The Problem with Lithium

Lithium is not easy. It is one of the most energy dense metals, which is why it attracted attention in the first place, but it has always been difficult to harness. The current lithium-ion chemistries, a workaround to begin with, took decades to develop, and they are still trying to perfect that.

But those decades of development and the maturity of the market are why we are seeing all that lithium-ion energy storage coming into the interconnect queue. These batteries are tested, validated, and available in large quantities.

The primary advantage of lithium batteries, the energy density, is very important if we are talking about mobile applications from smartwatches to EVs. But in the context of a stationary installation at a solar or wind farm, this is much less of an advantage. And there are also problems.

- Lithium batteries require temperature control.

- Safety issues including toxic fires.

- They can only discharge for a limited amount of time, 4-6 hours.

- They cannot hold a charge for long periods of time.

- They have a relatively short cycle life, about 10-12 years of daily cycles for LFP. Utilities are used to buying 30-year assets.

- Competing for lithium supply with EV ramp.

Lithium is ill-suited for most of what we will need energy storage for. It only really helps with diurnal mismatch and curtailment. Right now, those are the biggest issues with renewables, and since lithium batteries are ready to go in large quantities, that's what makes sense now. But this will change as more wind and solar hit the grid, and the use cases increase. Wind and solar were 15% of power generation in the US in 2022, up from 5% in 2012, and up from 10% 5 years ago. The more that gets added, the more that the problems outlined above will come to the fore, and lithium will be insufficient.

What is needed is long duration energy storage. Whereas for mobile applications energy density is the most important metric, here we are looking for:

- Long cycle life. This is key because is drives down the LCOE math.

- Long discharge times.

- Multiple charge-discharge cycles per day.

- Modular setup that can accommodate different geographies and climates.

- No major safety issues.

- Made from earth-abundant materials.

- The ability to hold a charge for months.

ESS Tech's iron flow battery checks off the first six boxes, and maybe the seventh.

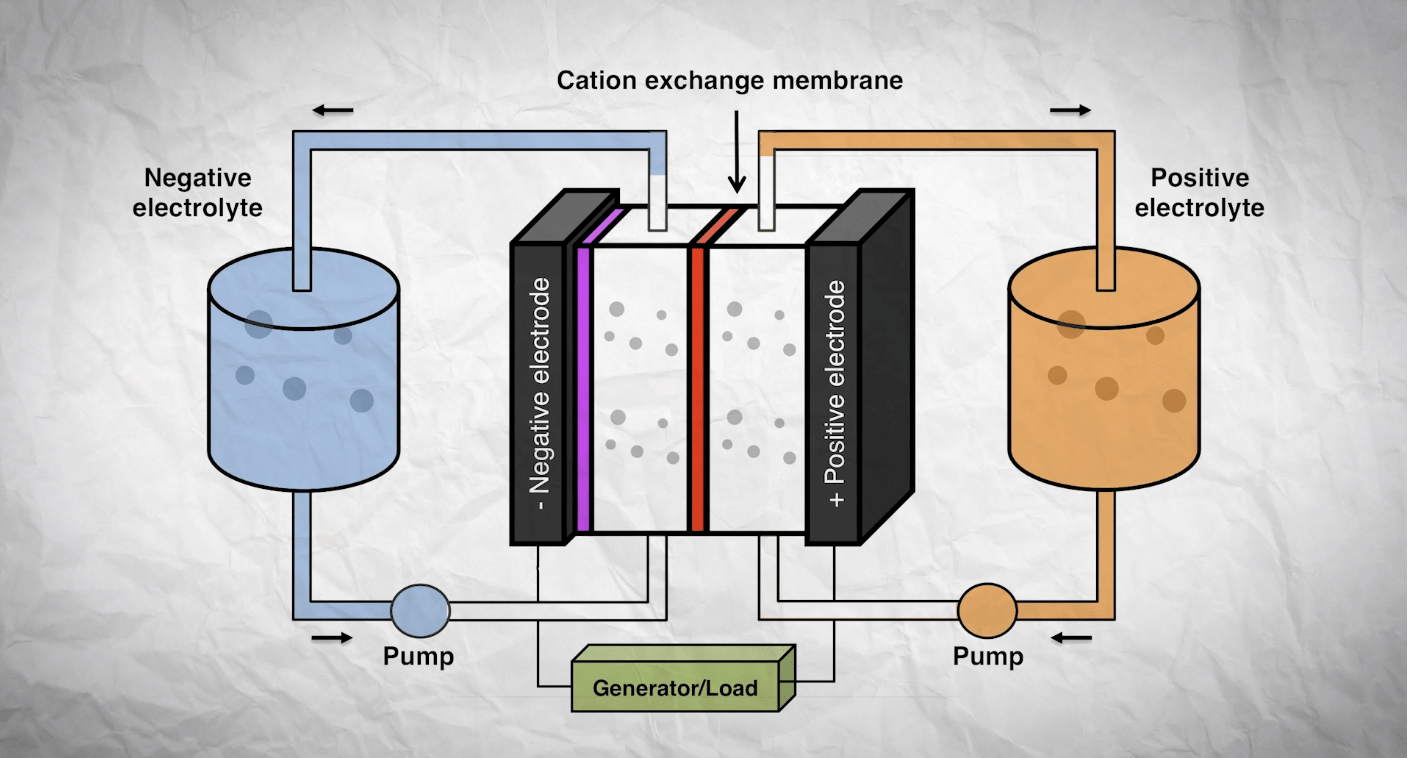

ESS Tech's Iron Flow Battery

There is a ton of private investment going into long duration energy storage, and not just batteries either. I have a spreadsheet with over 100 companies and 32 technologies or support services. There are 3 basic types:

- Electrochemical: batteries and green hydrogen

- Gravity-based: for example, pump some water to an uphill reservoir to store; let it run downhill through a turbine generator to discharge.

- Electrothermal: heat/cool/pressurize something to store energy.

The cutoff for usefulness is 80% efficiency, which is another way of saying you lose 20% of the energy in the round trip. That's about what you get from lithium-ion.

This has given new life to old battery technologies, one of these being flow batteries, where charged ions are exchanged between two large tanks of liquid electrolyte.

{kind=link}

You can see that this is wildly impractical for a phone or car. But it makes a lot more sense in the context of a stationary installation at a solar or wind farm.

Like many of the battery solutions, ESS is selling a modular containerized battery, the Energy Warehouse.

The Energy Warehouse (ESS Tech)

{kind=link}

As you saw up top, they haven't sold many. So how do they stack up to those requirements from the last section?

- Long cycle life. This is one of the primary advantages of flow batteries generally. The salt electrolytes are very stable and theoretically last forever. ESS advertises "25+" years and 20k cycles, which is 55 years of daily charge-discharge. Check.

- Long discharge times . They get half a checkmark here. They advertise up to 12 hours of discharge, which is a lot more than lithium, but also not enough to store a full day of solar for half the year. Of course additional overlapping capacity can solve that.

- Multiple charge-discharge cycles per day . Another flow battery advantage. Check.

- Modular setup that can accommodate different geographies and climates . There will have to be heating available in cold places, like most flow batteries. The iron salt electrolyte freezes below -10C (14F). The temperature ceiling is 60C (140F). Almost a full check.

- No major safety issues . None so far at least. Check.

- Made from earth-abundant materials . Iron and table salt. Check.

- The ability to hold a charge for months . The chemistry is very stable, so this should be true, but they don't advertise it, so I'm not sure. An email to Investor Relations was not immediately returned, but I imagine they're pretty busy right now. Inconclusive.

A lot of positives there, and very few negatives. So why do they have substantially no sales? The problem is that despite all the limitations, LFP batteries are ready today and solve today's problems. Long duration storage is at the pilot program stage, where utilities are doing small installations to test these things in real world environments. Announcements of these are starting to pick up in 2023.

This stage is going to take years. An optimistic timetable is mass deployment beginning around 2030, with a ramp beginning a few years earlier.

But in the energy sector, I believe this is the blue sky opportunity of the next 5-15 years. So does Honeywell.

The Honeywell Deal and Their Interest

Honeywell has been hot on energy storage since about 2018, and they like to talk about it any time they are given the opportunity. They sell containerized LFP batteries - supply deal with Freyr (FREY) - along with software and services for remote management. They were talking about launching their own flow battery in late 2021, but nothing has come of that, and maybe this investment replaces that effort. They have an investment in Electric Hydrogen, for hydrogen storage. They often work with Duke Energy (DUK) as their partner for testing things out.

The deal:

- Honeywell purchased 16.5 million shares at $1.67 for $27.5 million. This was a 24% premium to the share price when they closed the deal last Thursday. That represents a 9.6% dilution of shareholders. ESS very much needs this cash:

They said they will have about $120 million on the balance sheet at the end of the month and quarter, which gives them 6 quarters of runway at their most recent burn rate, or through the end of Q1 2025.

- Honeywell also gets warrants for another 10.6 million shares at $1.89. ESS closed on Tuesday at $1.87. So this may be another 5.8% dilution coming soon, and another $20 million to ESS. Honeywell has 5 years to convert.

- Probably even more importantly, Honeywell will be selling the Energy Warehouse alongside their current LFP offerings, and their software/services. This grafts on Honeywell sales and service teams. They are targeting $300 million in sales, with Honeywell putting $15 million down on that. Honeywell gets warrants equal to 5% of their purchases up to $15 million of shares (5% of $300 million). Shares priced at market price when purchases are made, but Honeywell cannot dip into this until 2026. They have already accrued $776k shares at $1.45.

- IP sharing, collaborative R&D, and access to Honeywell's advanced materials engineers. As part of this deal point, Honeywell gets warrants for another 6.3 million shares at $2.90. They can convert these any time in the next 5 years.

Altogether, that totals $81 million including the pre-purchase deposit, but not including the 2026 performance warrants.

Honeywell gets:

- Flow batteries to sell, after their own internal project appears to have gone nowhere. Access to ESS' IP for this stuff. Honeywell thinks flow batteries and green hydrogen will be the winners of long duration storage.

- If they grab that $1.89 tranche, they will own almost 15% of ESS. The IP warrants would take that up to almost 18%.

ESS gets:

- Much needed cash infusion, though still fairly small.

- Validation from a company that employs many engineers. This is huge, because it is a big obstacle for new technologies versus LFP.

- Grafting on Honeywell sales and support, much larger than their own. Again, that is huge. It puts them in a different category, and the deal structure incentivizes Honeywell to push their batteries.

- Access to Honeywell IP and engineers for future versions. They seem particularly interested in the advanced materials unit.

ESS shareholders got:

- Significant dilution, but a much higher price to make up for it and more.

So overall, this is a great deal for a struggling company that went public too early in the SPAC craze, but good technology may win out in the end.

Competition

This is a wide-ranging group of mostly private companies and also a few big names. Bill Gates' Breakthrough Energy Ventures is an investor in many of these companies; they were an early ESS investor, and also Electric Hydrogen. I want to mention 2 competing long duration batteries.

- The first is vanadium flow batteries, and there are a slew of companies working on this. Like lithium's energy density, vanadium has a unique property that keeps drawing in research and capital. Most metals have 1 or 2 oxidation states, but vanadium has 4, and it makes the flow battery very flexible as a result. The problem here is that vanadium is not rare, but nor is it abundant, and a whole new supply chain would have to be built for it.

- The other is the iron-oxygen (rust) battery from Form Energy , which advertises 100 hours of discharge, versus 12 for ESS' flow battery, and checks off the same boxes as ESS otherwise. Dominion (D) just announced a pilot program with Form's rust battery and Eos Energy's (EOSE) zinc battery. Form also just got in on a Department of Energy pilot program .

This remains a very wide open space in my opinion, but I think we are going to see a sorting over the next couple of years.

The Upshot

This is unequivocally good news for ESS, who were floundering a bit, and needed a shot in the arm. This is a nice shot.

But we are still at a very early stage here. LFP batteries are ready to go and solve today's problems, diurnal mismatch and curtailment. Renewables are only 15% of generation now, but growing fast. Once that hits around 20%-25%, lithium will become insufficient, and all those problems will come into sharper focus. Let's look at curtailment

{kind=link}

Almost 10% of CAISO renewables generation was wasted in March-May 2023, equivalent to about 2.5 days of average systemwide demand. As more renewables come online, and in larger scale, spring curtailment will balloon, and we will want to save some for summer heat waves, or other weather events. Lithium can't do this, nor can it power through the whole night, or a cloudy, windless day.

But all these pilot programs have to run their course. Buying a "25+" year asset is tricky business, and at 15% of generation, there is no crying need. Yet. But more and more, all the players in this world are coming to acknowledge that storage is the logical lynchpin to the whole cheap renewables buildout. It's a real blue-sky opportunity, but still not quite ripe.

For further details see:

ESS Tech Levels Up