GWH - ESS Tech: Without More Transparency Investors Left In A Lurch

2023-07-10 08:38:16 ET

Summary

- Despite 11 years of R&D pre-SPAC merger and access to hundreds of millions of dollars of cash post-SPAC merger, ESS has only reported ~$1 million in revenue.

- This amounts to revenue recognition on only about 5 Energy Warehouse units of about 46 announced.

- If management offers better transparency on the announced book of business, they should regain some credibility and the stock should do well vis-a-vis its peer group.

Background

ESS Tech Inc. (GWH) went public via a SPAC merger in late 2021. The company produces a grid scale battery with 4-12 hour duration that can stabilize power generation and be more accommodating for intermittent renewables. Unlike other grid battery offerings, those from ESS rely on iron and salt. Its chemistry avoids toxic electrolytes, flammable lithium, and expensive rare metals that are incorporated in competing offerings. The battery is made in the USA, and this may be very important in qualifying for the domestic content in the Inflation Reduction Act of 2022 . The company has an all-star cast of investors including Softbank and Bill Gates' Breakthrough Energy Ventures. Joint venture and sales announcements have been tremendous but this hasn't translated to GAAP recognized revenue for reasons that aren't entirely clear.

A spreadsheet detailing ESS's announced wins

The abbreviated spreadsheet below ( full sheet and footnotes available ) details ESS Technologies Inc ("GWH") public announcements on sales wins to date, since the company's SPAC merger. Very few company updates have been provided on previously announced wins and shipments.

| ESS Customer Announcements |

| Max |

| # of |

| Project |

| Customer |

| Location |

| Product |

| units |

| Size MWH |

| Softbank |

| Davis, CA |

| EW |

| 1 |

| Applied Medical |

| EW |

| 2 |

| Terrasol/Sycamore |

| West Grove, PA |

| EW |

| 1 |

| Terrasol/Sycamore |

| West Grove, PA |

| EW |

| 1 |

| Turlock |

| California |

| EW |

| 2 |

| 3000 |

| Schipol |

| Amsterdam |

| EW 75kw/500kwh |

| 1 |

| Coldwell Solar |

| Mendicino, CA |

| EW |

| 3 |

| QUT |

| Australia |

| EW 75kw/400kwh |

| 1 |

| Stanwell? |

| Tarong? |

| EW 75kw/500kwh |

| 10 |

| Stanwell? |

| Rockhampton? |

| EW 75kw/500kwh |

| 9 |

| Stanwell? |

| EW 75kw/500kwh |

| 35 |

| SMUD |

| Sacramento |

| EW |

| 6 |

| 2000 |

| LEAG |

| Boxberg |

| 50 MW/500 MWh |

| 3000 |

| Consumers Energy |

| Michigan |

| EW |

| 1 |

| 4000 |

| Burbank Water |

| Eco Campus |

| EW 75kw/500kwh |

| 1 |

| Portland General |

| adj to ESS |

| EC 3MWH |

| 1 |

| 3 |

| SDG&E |

| Cameron Corners |

| EW 400kwh |

| 6 |

| 2.4 |

| 46 |

| 12040.4 |

This spreadsheet was put together by extracting data from company announcements in 2022 and 2023. The 2022 start date is only a bit after the SPAC merger. But data from 2021, while a different corporate era, provides further alarming data on units that have been announced but never updated. For instance 2GWH to the company's largest shareholder: ESS and SB Energy Sign Agreement to Deploy Two Gigawatt-hours of Long-Duration Storage , 17 EW or 8.5MWH to Enel Green Power Espana , and 4 EW to Patagonia .

What sort of information could ESS provide on each announced install?

Here's an overhead shot of one of the earliest installs in the spreadsheet above, Cameron Corners:

{kind=link}

Cameron Corners Microgrid (google maps)

The six EW units are pictured at the right hand side of the shot above. A call to one of the establishments, connected to this microgrid, confirmed that they do have power when the grid is down so the EW's must be working. Some update from SDG&E or ESS on the number of outages where the unit has served as backup and the number of kwh supplied would be helpful. Particularly since this project was done by ESS chairman Michael Niggli's alma mater Sempra Energy/SDG&E, it ought to be reasonable for shareholders and analysts to request an update and for Mr. Niggli to facilitate SDG&E providing one that wouldn't give away any proprietary information.

Regarding all the other ESS installations, I invite SA readers to dig out and post any similar shots and testimonials/refutations in the comments below.

The company's offer to "look at the spreadsheet"

This offer was made after my description of the spreadsheet derived from publicly available information in ESS press releases and the missing items. I've explained that "looking at the spreadsheet" is not an undertaking to fill in the blanks. In any event we're beyond "looking" and "blank filling". Here is a verbatim list of items I called out that are among those that need discussion:

"On a social media posting about the QUT battery, one of your employees said he was looking forward to working with Stanwell on its installation. Can't find a press release that ever mentioned Stanwell was the ultimate customer for all these Australia units in limbo. Should your shareholders believe company press releases or social media posts by your employees? Or, quite possibly and the need for a conversation on these type of issues, did I miss something?

on a social media posting one of your employees posted he was looking forward to working with SMUD again. Was your employee pulled off of SMUD and put back on? Or was this a corporate hiatus of some sort, and if so why and when? Why is this all being unrolled on social media and not in company releases for your many shareholders who don't comb through social media posts?

Where's an update on Patagonia, Enel Espana, or Softbank or did I miss these as well. An update on Softbank would be particularly helpful since they are your largest shareholder, are represented on your board and you have apparently reserved production capacity for them. If that deal is dead you, and they, should disclose it. Reserved capacity for an outfit that's bought 1 Energy Warehouse is likely a deterrent to the Consumers, SMUD's and LEAG's that might want to have your whole 800MWH of annual capacity, or whatever you are willing to give them. Is there a regular board review that company information Softbank Energy has received from the company is not being misused? Is there the reverse: that information ESS may have received from Softbank is properly used and partitioned ?

The release on an Energy Center to be built by Portland General Electric has never been updated, that I have seen on your website or theirs. The release stated it was going to be built on land adjacent to ESS. I now have the tax plot owners of the only two vacant parcels adjacent to you and PGE is not one of those owners. I don't see either of the two vacant parcel owners leasing to PGE for this function.

Even though you aren't concerned with filling in these blanks I will continue to do so and write about them as I receive FOIA responses, drone pictures, zoning board responses, and other responses to inquiries. This information shouldn’t flow to shareholders from me, or other blog writers, or from competitors, or from Wall St analysts, or from customers, or from trade journals. It should be coming from you."

[Author's note: the reference to "Stanwell" in the first paragraph above refers to Queensland, Australia's government owned power generator. "Patagonia, Enel Espana, or Softbank Energy in the second paragraph are all customers or prospective customers where releases have been put out by the company. For a full list of releases referred to here, click on the link to the full spreadsheet that appears right above the spreadsheet.]

And here is ESS's response to the items raised above

"I’m sorry you feel that this is a lack of transparency on our part, but please know that we’ve tried to share what we can, where we can, in keeping with the customer’s desires. Some of these folks change plans/locations/timing/etc. and simply don’t chose to share that until they are ready.

A few things that I can say about your points below, either because they are already out there, or because they are not material.

- The SBE agreement is still in place – certainly any cancellation would have been a disclosure. That said, as previously disclosed, there is no ‘loss’ of capacity due to that agreement. With SBE and all customers, our promise of reserved capacity is subject to their timely orders – effectively all we promise is that if they place the orders per the agreement, we will build their product on that schedule. SBE’s agreement has zero impact on LEAG or any other customer until such time as orders are placed and we accept them. Side note, with planning cycles so extended these days, we’d be able to build more capacity within the timeframes of most larger orders.

- Appreciate your telling me that Stanwell was ‘leaked’ by someone on our side. I’ll look into that, as it is a clear violation of confidentiality. I know ESI has posted about Stanwell, but that’s kind of the point, this is Stanwell and ESI’s announcement to make (or disclosure to give, if you prefer), not ESS’s. We have no contractual relationship with ESI’s customers.

- As to SMUD, this is a great example of looking for something that isn’t there. We have a number of people on our team, including our head of delivery, who have worked with SMUD in the past, for different companies. That includes me. “Looking forward to working with you again’ means exactly that – but there is no previous ESS relationship – this is the first agreement we’ve ever done with them.

As to the others where you mention ‘no update’, all I can say is that when there is an update, we’ll update. If we haven’t updated, you can assume that there is no update to give."

And here are some further comments on that exchange.

- Management is at least trying to engage in a dialog on my transparency concerns. I thank them for thoughtful and timely responses. We appear to disagree on whether the transparency issue has been solved.

- There was no update on the 2021 announcements for a sale to Patagonia or ENEL Espana.

- Management didn't reply to my questions on Portland General Electric. I just received this response from PG&E on the state of the project, "Hi Fred, Yes, the update is that this project is further delayed. Construction of the units has not yet started, and the planned energize date has been moved out to summer of 2024." Since ESS press released this project on 12/20/21, I'd like to know when the project was delayed, and what caused the delay. Since PG&E is willing to respond to an email inquiry it must be public information. Ask yourself whether its reasonable that the company should have updated this project with the delay information.

- Finally on the "reserved capacity" for Softbank Energy, is it reasonable to expect the customer or prospective ESS investor to parse this language on a reserve that isn't a reserve unless orders are place? I know where to look and can't find a detailed 8K reference to this very material 2GWH contract.

What do competitors disclose on key metrics? Is it reasonable to expect more transparency given what company peers are disclosing? What would ESS's disclosure look like in that format?

Below find a slide from the first quarter presentation from peer Energy Vault:

{kind=link}

Energy Vault Metrics (Energy Vault )

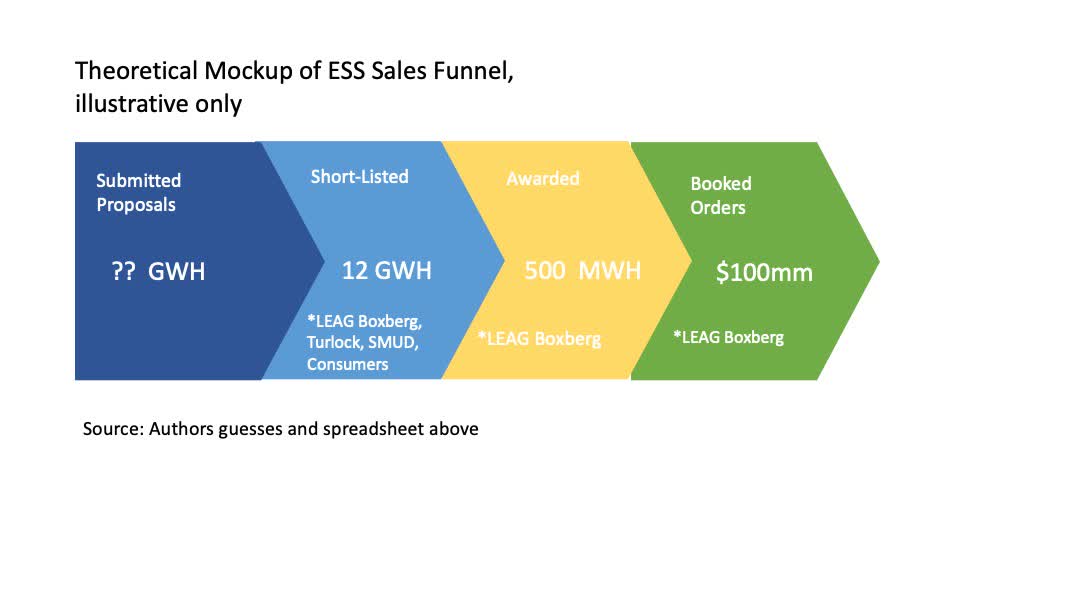

And here's what the ESS information might look like even with just the paucity of information that's been given to shareholders:

{kind=link}

Source: Author

Selling to the right type of customer

ESS needs to prioritize its sales and realize that markets that look great now may not look so good over the 20-25 year life of their batteries. I believe a great many of the announced wins don't fall in these categories listed below. I believe there are three market types on which ESS should be concentrating now that should stand the test of time with this long lived technology:

- Balancing resources and meeting carbon reduction goals for base load generators. Examples from ESS's spreadsheet of announced projects include LEAG, Stanwell, Consumers Energy and Portland General

- Diurnal storage. This is a fancy term for saving power generated in the afternoon sun from Photovoltaics to be used in the evening demand peak. Closest example from ESS's spreadsheet of announced projects is the Cameron Corners microgrid of SDG&E.

- Curtailment for wind and solar producers. Wikipedia defines curtailment as follows: "In electric grid power generators, curtailment is the deliberate reduction in output below what could have been produced in order to balance energy supply and demand or due to transmission constraints." There are no pure examples of this in ESS's spreadsheet of announced projects.

Of course each of these concentration areas blend together in certain instances.

Base Load Operators

Aside from just trying to operate profitably, base load operators in the US are now facing an array of recommendations and legislation on battery storage and carbon reduction. Flow batteries make great sense in this application: it saves an operator from spinning up its most expensive resource-- peaking gas turbines-- to meet a demand spike which can't be handled by the base load facility. As opposed to turbines, battery storage can be dispatched instantaneously and emits no carbon. The best example from the spreadsheet, on which ESS has not provided any updates, is Consumers Energy. Based on the link above, utilities in Michigan "...need to deploy 2,500 MW of energy storage by 2030 and 4,000 MW by 2040 to ensure grid reliability as fossil fuel generation retires."

Diurnal storage

Unfortunately peak solar production doesn't occur during the morning or evening demand peaks. Longer duration flow batteries like those from ESS are a key tool to solve this. There are some excellent papers on the topic , including great pronouncements: "..diurnal storage can likely be sufficient to meet the integration needs of high renewable energy penetrations up to at least 80%." That paper included modeling results on their 2050 storage forecast: "...deployment for energy storage exceeds 125 GW by 2050, more than a five-fold increase from the current installed storage capacity ... . For battery storage, there is at least 3,000 times more battery capacity in 2050 than exists today"

The curtailment opportunity for flow battery storage is huge

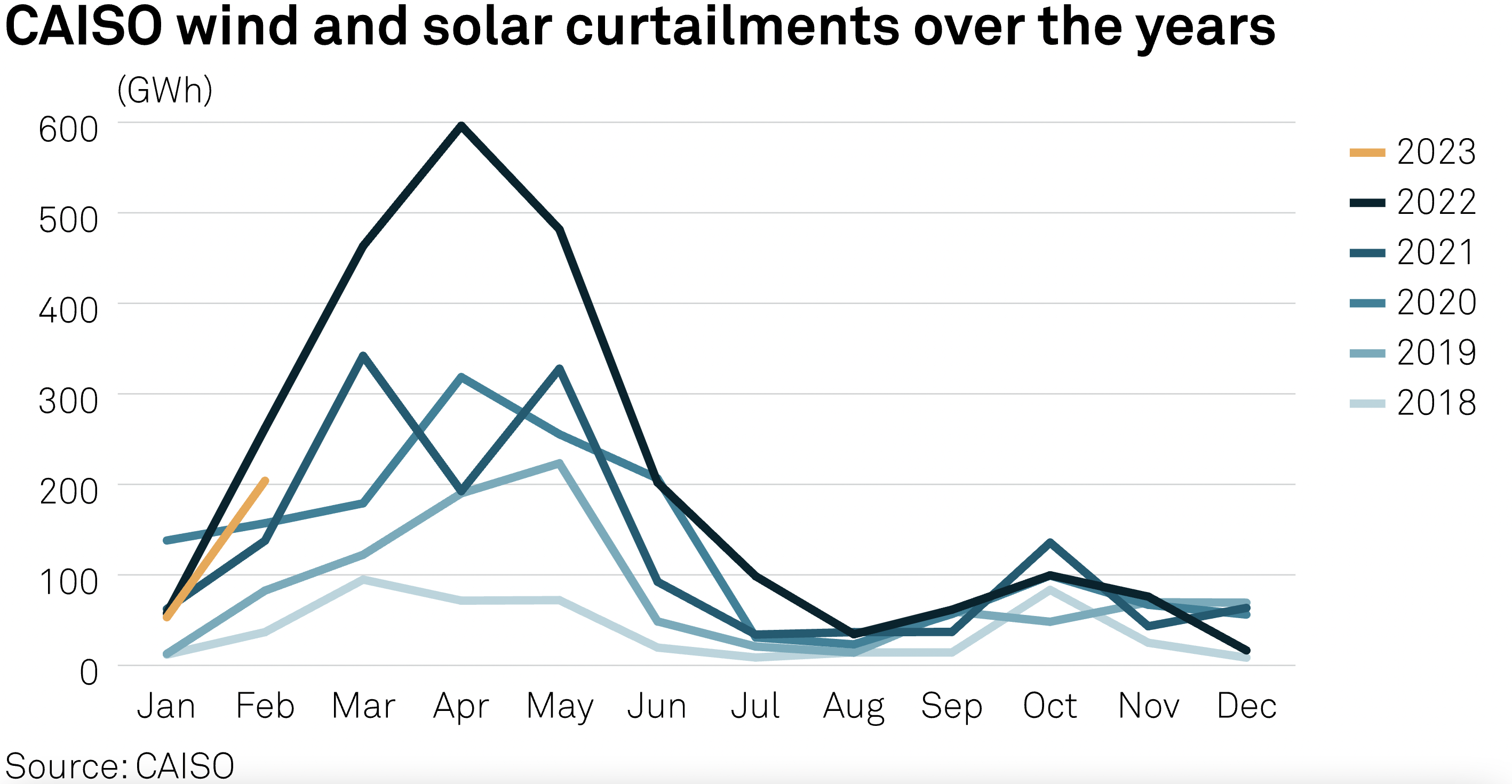

With growing installations of wind and solar the amount of curtailments will continue to climb. Here are some recent numbers for California:

According to the California Independent System Operator (CAISO), approximately 1,400 GWh of utility-scale solar and nearly 80 GWh of wind were curtailed in California in 2021. This is enough to power nearly 220,000 homes for a year.

The amount of solar curtailment in California has been increasing in recent years, as the state has added more solar capacity to its grid. In 2019, only 600 GWh of solar were curtailed. [Source: Google Bard]

{kind=link}

California Curtailments over time (CAISO via S&P Global)

And here's some information on curtailment in the Texas market:

-The amount of wind and solar generation that is curtailed in Texas varies from year to year, but it is typically around 4% of total generation. In 2021, for example, ERCOT curtailed 109,924 GWh of wind generation, which represents 4.2% of total wind generation in the state.

One way to mitigate the cost of curtailment is with longer duration batteries such as ESS's 12 hour iron flow offering. Of course this won't alleviate the effects of over production of wind in a week long storm, but it may allow storing production and turning it into revenue in periods where the sun is down or the wind is diminished.

“The most important decisions you make are not the things you do, but the things you decide not to do.” This quote is attributed to Steve Jobs. I have been a fan of foreign sales since some of those markets are enormous and moving quickly. The Boxberg, Germany order is the biggest the company has booked. Australia and East Germany look like great markets but sales and service there involve 2 days of plane travel vs. the amazing opportunities a car ride away from Wilsonville, OR. Those foreign operations will require selection of partners, where the company has not performed well, and understanding and lobbying on legislation that's difficult to stay on top of without deep local knowledge and connections. Given the company's demonstrably poor record of selecting partners and executing in Australia, I am cooling on foreign sales.

I have also been a fan of selling batteries into the Time Of Use arbitrage which often exists in states like Hawaii and California with enormous spreads between peak and off peak power costs. I received a great fable on pursuing the fickle arbitrage market, which, along with a compression of the available arbitrage due to a narrowing of spreads between peak and off-peak rates, has cooled my enthusiasm for this segment:

The Arbitrary Arbitrage Fairy . Let’s say you’re approached and offered a $1M wall safe. The idea being pitched is that every single day you can put $1,000 into the wall safe in the morning, go about your day, and when you return, you can withdraw $1,500 from the wall safe. A magic Arbitrage Fairy has turned your $1,000 into $1,500. But there are caveats. The Arbitrage Fairy isn’t included in the purchase price, it isn’t even part of the safe, it exists and acts independently of the safe and the safe’s manufacturer. The manufacturer has no contact with, or control over the actions and whims of, the Arbitrage Fairy. Whether the currently favorable economics of this wall safe will continue to be favorable is unknown.

It’s entirely possible that in the foreseeable future you may deposit $1,000 into the wall safe and withdraw $1,300, or $1,200, or $1,100 instead of $1,500. Worst case scenario is that if the Arbitrage Fairy simply stops showing up and performing its daily magic, every time you deposit $1,000 in the morning, it will become $600 by the afternoon. After all, this is an Arbitrary Arbitrage Fairy. Would you still like to buy a $1M wall safe?

I believe several of the announced wins in the spreadsheet above are pursuing this Time of Use arbitrage market, which may look good now but may not prove a reliable enough factor for customers to afford the ESS battery in the future. My ardor has also cooled on the arbitrage market due to the astonishing admission that ESS's roundtrip efficiency is only 60% (see question from Colin Rusch) This is an enormous disadvantage to lithium at 70%+ and pumped hydro at ~80%. This means that, for every 1MWH hour put into the ESS battery, it is generating 400kwh of heat. Imagine your little toe warmer 1000watt heater under your desk plugged in for 400 hours! That's a lot of heat and calls into question the company's assertion that no cooling is needed. Or in the parlance of the fairy and the wall safe, $400 of every $1000 you put into the safe is immediately burned up. Perhaps still an interesting proposition as long as the fairy stays healthy and visits the safe regularly; a big "if". While PG&E's TOU rates once allowed the $1000-in and $1500-out economics in the first paragraph of the wall safe fable, now the diminished fairy is only delivering about $1200 in peak rate revenue for every $1000 off peak battery charge cost (and this is before cranking in the 60% round trip efficiency which eliminates the desirability of the safe and the beautiful fairy, at this spread.)

Why am I still at a buy on GWH with all these cautions?

I moved to a very speculative "Buy" based on the news of the 50MW/500MWH order ESS received from LEAG for its Boxberg, Germany plant. If ESS is beginning to book grid scale batteries like this, which will pull in $100 million of revenue, then its stock could recover quickly beyond post-SPAC heights.

But I will move quickly back to a "hold" or even a "sell" if the following things don't happen either before or on the next earnings call, expected in mid August:

- I'd like to see management explain, in detail, this recurring revenue recognition problem. They should fill in the blank cells in the spreadsheet above. Shareholders and perspective customers likely have the same questions on these announced projects: are they commissioned? are they generating MWH of storage? are they operating on spec?

- Some specificity on the LEAG contract would be great; it is due to be signed in the third quarter. Oddly this was announced before it has been completely inked. Ideally it will include a cash deposit and progress payments.

- I believe management should regularly update shareholders on the performance and adequacy of the inevitable foreign partners they will need to support foreign sales. ESI Asia does not appear to be performing in Australia. As of the last earnings call they had 10 Energy Warehouse units in country but stuck in the port; no revenue has been recognized on these units. ESI Asia has promised a $70 million facility in Queensland where it will assemble ESS batteries. ESI Asia has passed along the news of their ground breaking on two separate occasions, odd for a single capital project. Alas, the pictured ground breakings were not on land that they own or propose to buy. Not a twig has been disturbed , or a spoonful of dirt moved on that land. As partners are selected to support the LEAG battery we need to know who they are, what their deliverables and dates are, and how they are performing.

Conclusion

Please ask yourself whether the revenue recognition problem has been properly addressed. I used to think the problems were related only to our old accounting firm and being stuck in R&D accounting, which apparently has different requirements for revenue recognition. And perhaps our problems had to do with legacy sales contracts which required ESS to wait on revenue for project deliverables out our its control. The longer the lack of revenue recognition continues-- more than two years in the case of some announced sales-- the more I feat there is a specification over-promise or some difficult flaw in these batteries. Other investors may have more success sourcing this type of information from management or elsewhere; perhaps delay your own stock purchases until you have answers. A truly depressing hand waving discussion is CFO Tony Rabb's remarks in the most recent earnings call. This isn't rocket science. The gaps in the spreadsheet should be filled in by the company, its customers, analysts or even Seeking Alpha writers and commenters. Tell us whether each unit is hooked up and how many MWH are being stored, daily, in ESS flow batteries.

A transparent ESS, that is not only announcing wins, but regularly updating them can be an extremely well valued entity. Customers want to see results in order to make a purchase decision and so do shareholders.

For further details see:

ESS Tech: Without More Transparency, Investors Left In A Lurch