EPRT - Essential Properties: Don't Wait To Buy This Sweet REIT Bargain

2023-10-27 08:10:15 ET

Summary

- Essential Properties Realty Trust offers a solid value buy opportunity with an appealing yield.

- EPRT focuses on middle-market tenants and has a long weighted average lease term with focus on e-commerce resistant tenants.

- It also has a strong balance sheet and continues to achieve impressive growth, making it a good complementary holding to peers Realty Income and NNN REIT.

Dividend stocks have plenty of competition these days, not least of which comes from Treasury bonds and high yield savings accounts. However, there is no free lunch, as who knows for how long higher rates will last.

I believe that while socking money away into CDs may seem appealing today, keeping one's options open by also staying invested in dividend stocks provide a great way to hedge against reinvestment risk at potentially lower rates in the future.

This brings me to Essential Properties Realty Trust (EPRT), which I last visited here back in June, highlighting its growth potential in the middle market space. The market has baked in additional risks to the stock since my last piece, with the price declining by 13.7% mostly over the past couple of months. One of probable reasons is because of fears around a 'higher for longer' interest rate environment and its effects on perceived 'slow-growing' REITs.

In this piece, I provide an update and discuss why the recent price action on EPRT presents a solid value buy opportunity with an appealing yield, so let's get started!

Why EPRT?

Essential Properties Realty Trust is a self-managed net lease REIT that focuses on owning and leasing properties in the middle market, where opportunities are more fragmented with less competition for deals.

It's reminiscent of STORE Capital, which got acquired last year in a private market transaction, in that it gets unit-level reporting from 99% of its tenants. Its tenants are also in overall healthy shape, with average unit-level rent coverage of 4.0x. Moreover, 93% of EPR's annual base rent comes from service or experience-based tenants, making it e-commerce resistant.

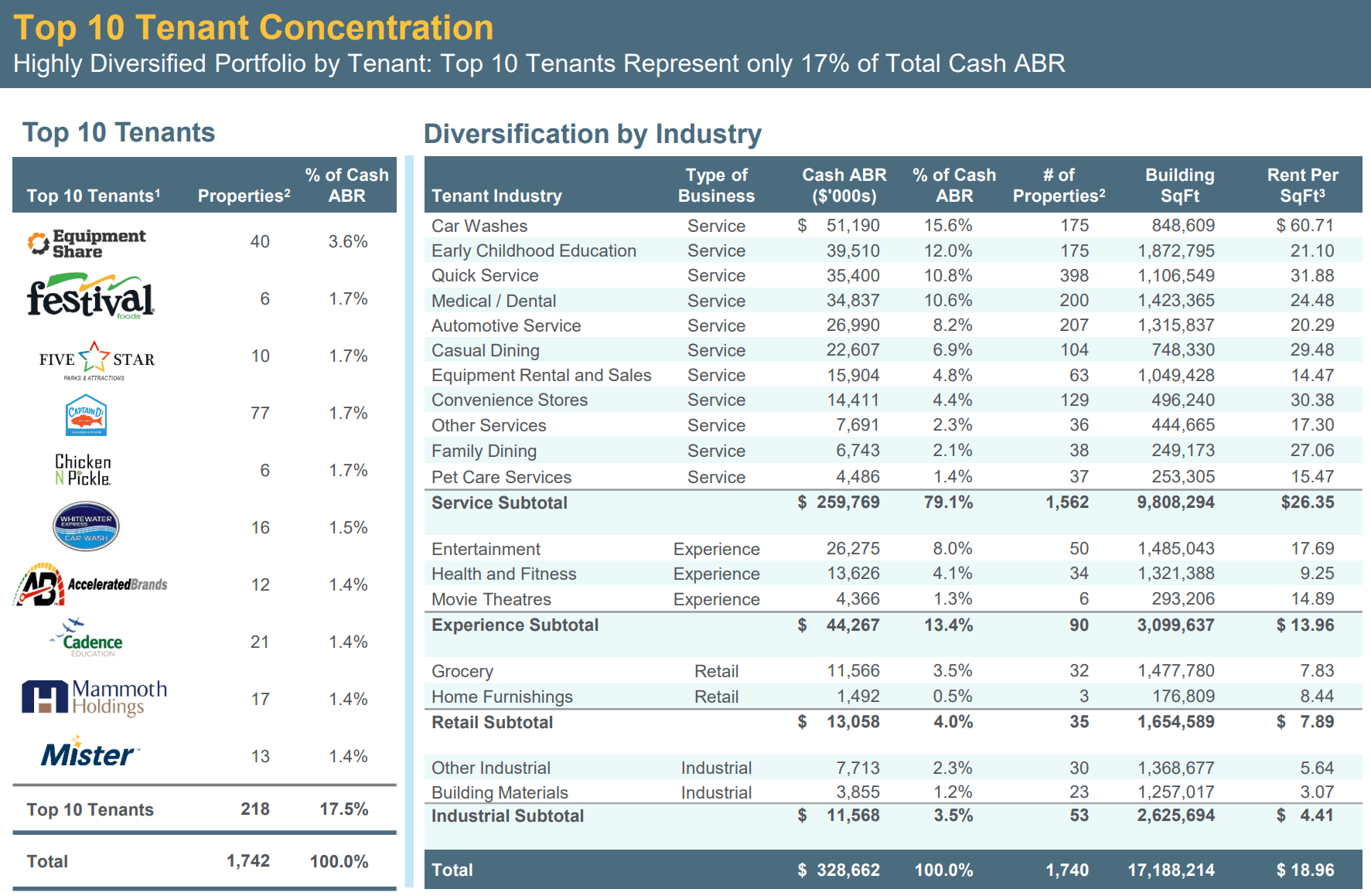

As shown below, car washes, early childhood education, quick service restaurants, medica/dental, and automotive service make up EPR's Top 5 segments comprising 57% of its annual base rent.

{kind=link}

Like most other net lease REITs, EPRT enjoys a high occupancy rate, which stands at 99.9% as of the end of September. What sets EPRT apart from peers Realty Income Corporation ( O ) and NNN REIT ( NNN ) besides its focus on middle-market tenants is its long weighted average least term of 14 years, which is meaningfully higher than the ~10 years of both aforementioned peers.

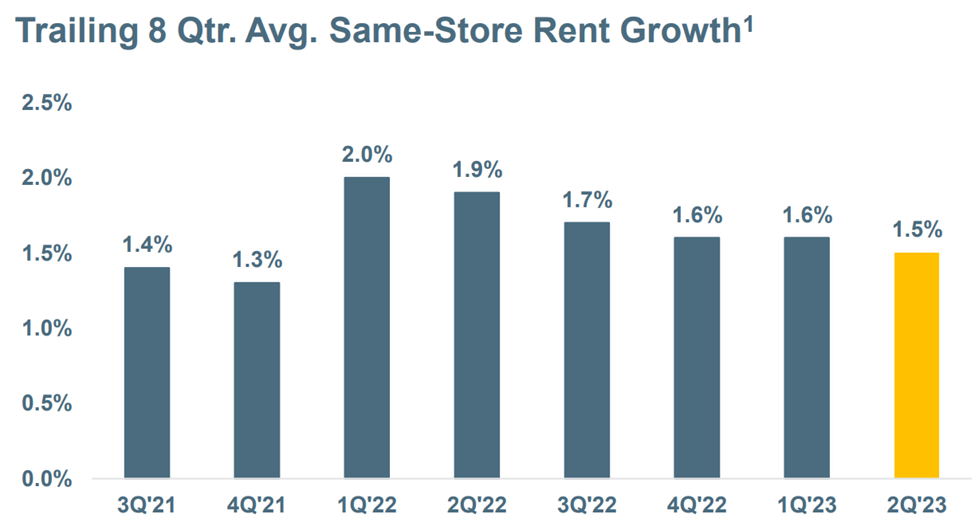

It's worth mentioning that EPRT's management carries a collective 100+ years of experience in the real estate industry, and has cultivated long-standing relationships with tenants. This is reflected by most (83%) of its transactions this year being repeat business. EPRT has also seen same-store rent growth in the past 9 quarters ranging from 1.4% to 2%.

{kind=link}

This includes the most recent third quarter results, with same-store rent growth of 1.2% compared to the prior year period. Importantly, EPRT achieved FFO and AFFO per share growth of 18% and 11% YoY, respectively. This was driven in part by the aforementioned rent growth on existing properties as well as portfolio recycling, with a weighted average cap rate of 6.5% on 10 dispositions proceeds of which were applied towards the acquisition of 65 properties at an attractive 7.6% cash cap rate.

The rest of the funding for new properties came from combined equity and debt issuances that are accretive to shareholders, considering the 7.5% cost of equity raised at just over $23 per share for $286 million and a debt issuance of $375 million at a 4.1% interest rate (cost of debt). This calculates to a WACC of 5.6%, and translates to an appealing 200 basis point investment spread based on the aforementioned 7.6% cash cap rate on new investments.

Risks to EPRT relate to higher interest rates, which would result in higher interest expense. This also raises the cost of debt. Also, EPRT's lower share price makes the cost of equity higher, which combined with higher cost of debt would compress investment spreads on new acquisitions.

Nonetheless, EPRT could still unlock value from portfolio recycling. It also has the backing of a strong balance sheet with a net debt to adjusted EBITDA ratio of 4.5x, and the leverage ratio declines to 3.7x on a proforma basis when taking into consideration stabilized rental income from newly deployed capital. The low leverage ratio, sitting below the 6.0x level generally considered to be safe for REITs by ratings agencies, also gives EPRT the capacity to rely more on debt financing should its cost of equity go higher (due to a lower share price).

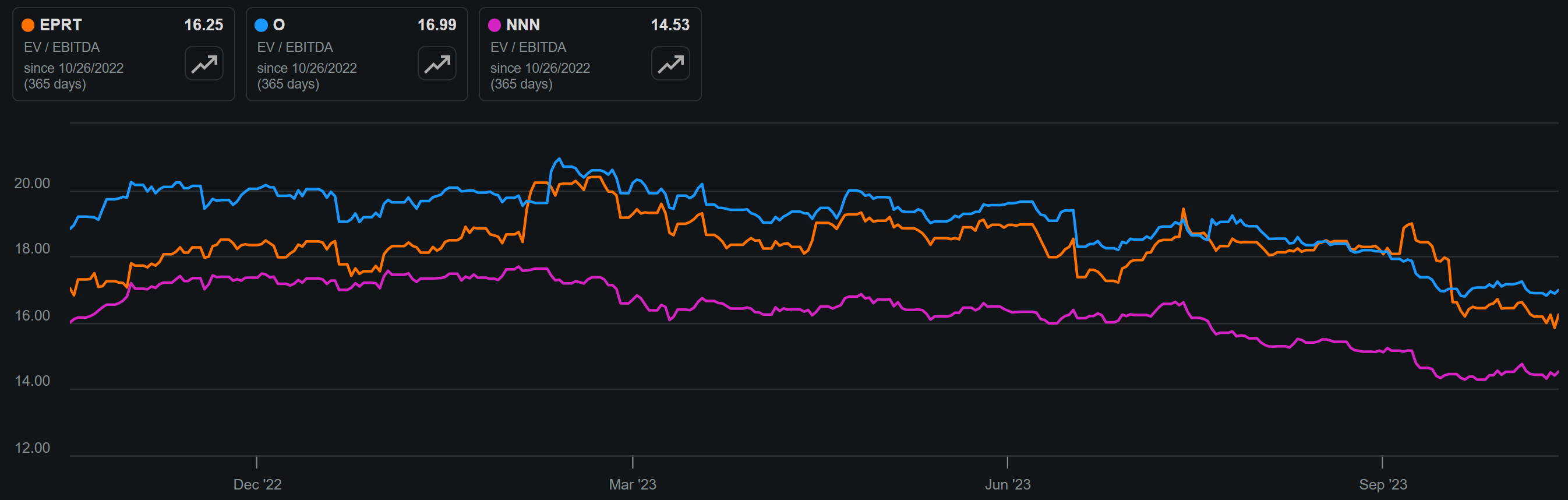

Meanwhile, EPRT currently sports an attractive 5.2% dividend yield that's well-covered by a 64% payout ratio. I also see value at the current price of $21.45 with a forward P/FFO of 12.3. While this is slightly more expensive than the 12.1x P/FFO of Realty Income and 11.1x of NNN REIT, an apples-to-apples EV/EBITDA comparison (since EV includes equity and debt) shows that EPRT's valuation fits squarely in between that of its 2 peers.

EPRT vs. Peers' EV/EBITDA (Seeking Alpha)

{kind=link}

Investor Takeaway

While investor sentiment has soured on Essential Properties Realty Trust as of late amid fears over higher interest rates, I believe that the company is well-positioned to continue its solid growth trajectory considering its large market opportunity size and low-leveraged balance sheet.

EPRT's focus on middle-market tenants and long-term leases and unit-level reporting provides a strong foundation for future success, and this was supported by continued impressive growth during the third quarter. While peers Realty Income and NNN REIT are definitely worth having in a portfolio, I view EPRT as a solid complementary holding to them considering its durable income stream and faster growth potential. Reiterate 'Buy' rating.

For further details see:

Essential Properties: Don't Wait To Buy This Sweet REIT Bargain