EPRT - Essential Properties: I Bought The Debt But I Didn't Buy The Equity

2023-09-14 09:00:00 ET

Summary

- Essential Properties Realty Trust has a presence in 48 out of 50 states in the US, with a focus on Sunbelt states.

- EPRT has a diverse portfolio of 1,750 commercial properties, with 99.9% occupancy and 360 renters operating 560 brands.

- We look at the valuation of this triple net REIT and tell you why Bob Marley's picture is gracing this article.

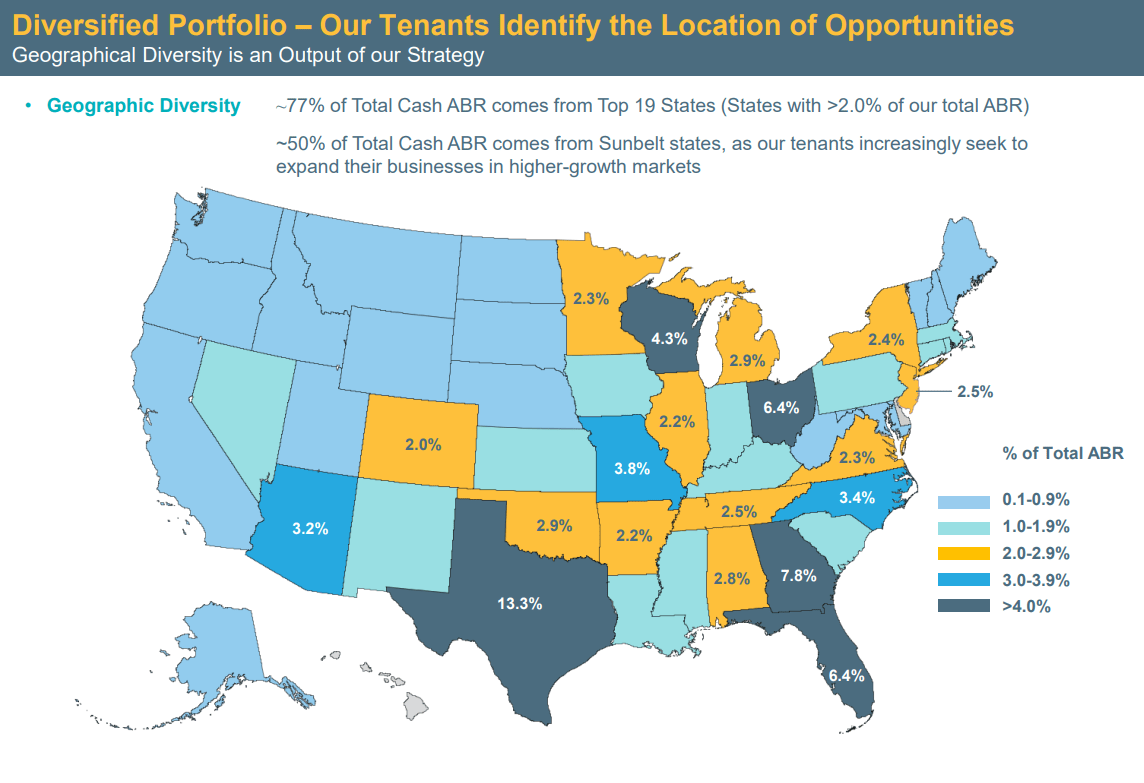

The United States has 50 states. Essential Properties Realty Trust, Inc. (EPRT), an internally managed REIT, has a presence in 48 of them. Admittedly, just like all fingers are not equal, here too the distribution is skewered towards 19 of the 48 states, with the Sunbelt states contributing around half of the annualized base rent or ABR.

{kind=link}

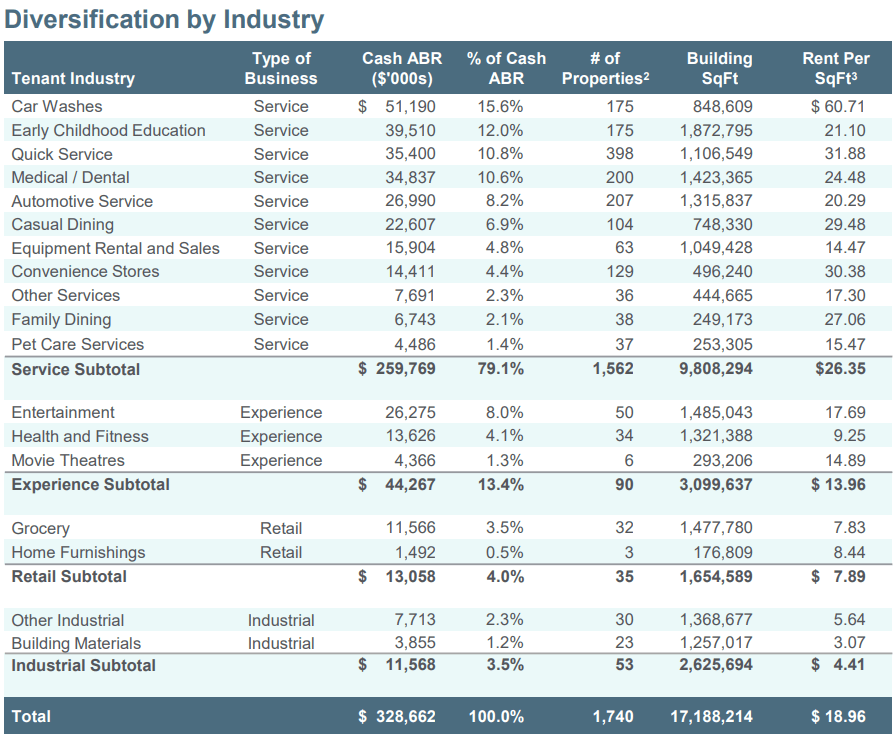

At the end of Q2, this REIT had a portfolio of close to 1,750 freestanding, single-tenant commercial properties and that was 99.9% occupied. The tenants of this REIT are primarily in the "service-oriented or experience-based" business. There is sufficient diversification within that realm, with a roster of 360 renters operating 560 brands. Given the vast number of brands, an assortment of industries is also a given.

{kind=link}

In another shining example of diversification, their top tenant occupies 40 of their properties, but contributes only 3.6% of the REIT's ABR.

Investor Presentation - Sep 2023

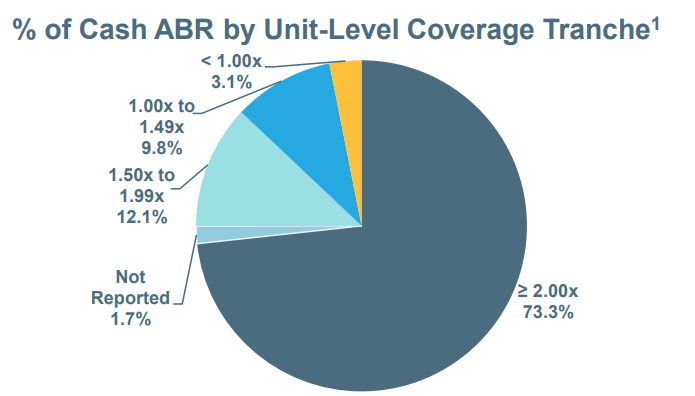

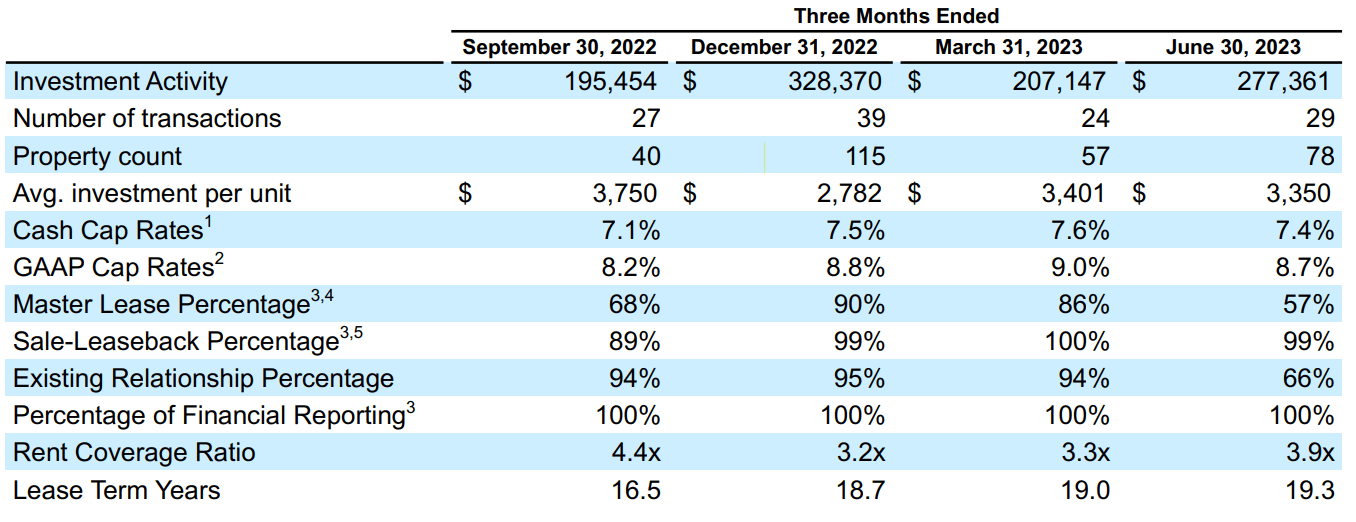

The vast majority of EPRT's leases are of the triple-net nature, that is, the tenant bears all the costs involved in the operation of the property such as repairs and maintenance, insurance, utilities, property taxes, etc. This shields our protagonist from the impact of rising costs, aka, inflation to an extent and also limits their expenses to those for structural repairs or capital improvements. To that end, EPRT keeps an eye on the financial health of its tenants, with almost all of its leases contractually obligating the tenants to provide the REIT with their unit-level financial reporting or EBITDAR. At June 30, the weighted average rent coverage ratio of the portfolio was a healthy 4.1x.

{kind=link}

EPRT's weighted average lease term or WALT is an impressive 14 years. To put this in perspective by comparing to a couple of established triple-net names, Realty Income Corporation (O) had a 9.6 years weighted average lease term at the end of Q2, and NNN REIT Inc. (NNN) while higher at 10.2 years , was still considerably lower than EPRT. We recently covered Four Corners Property Trust, Inc (FCPT) that began operations in 2015, a few years before EPRT's commencement in 2018. FCPT compares poorly in this regard to EPRT, with a WALT of just 8.1 years at June 30, 2023.

In addition to a 1.6% weighted average annual rent escalator built into 98.5% of the leases, 65.8% of EPRT's contracts are master leases. These type of leases protect the REIT from the risk of default by the tenant. Under the master lease agreement, a tenant leases multiple properties and a default on any one results in them losing all of them. EPRT coveys its predilection for these type of leases in the 10-Q .

We strongly prefer to use master lease structures, pursuant to which we lease multiple properties to a single tenant on a unitary (i.e., "all or none") basis.

This REIT started by distributing 22 cents in 2018, and after consistent increases over the years, the quarterly payout now stands at 28 cents. At the current price of $23.73, it yields around 4.7%. In contrast, O currently yields around 5.6%, NNN yields close to 6%, and FCPT comes in at around 5.5%. Irrespective, EPRT has outperformed the trio by a margin since it entered the scene.

This is the first time we are covering this popular REIT on this platform. While the price action makes us dial back our excitement, we are definitely intrigued by what appears to be an extremely lean, mean, well run machine.

Q2-2023 Results

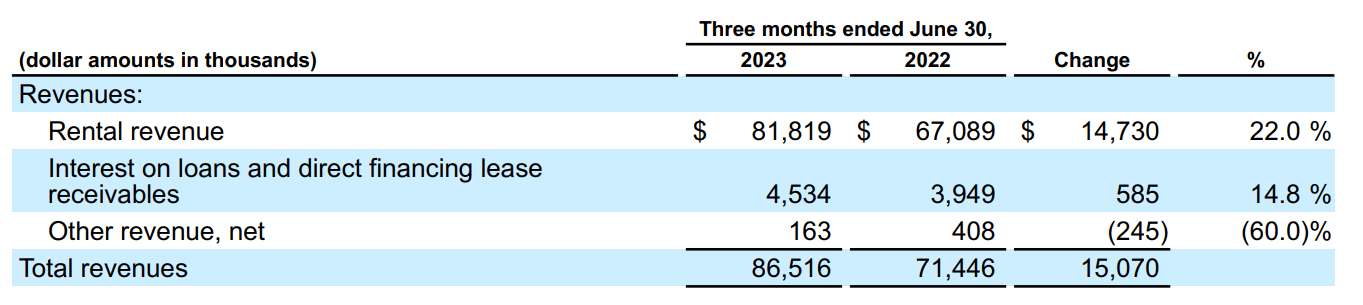

The rental portfolio grew by 15% since June 30, 2022. That, along with contractual rent escalators drove the 22% year over year increase in the rental revenues.

{kind=link}

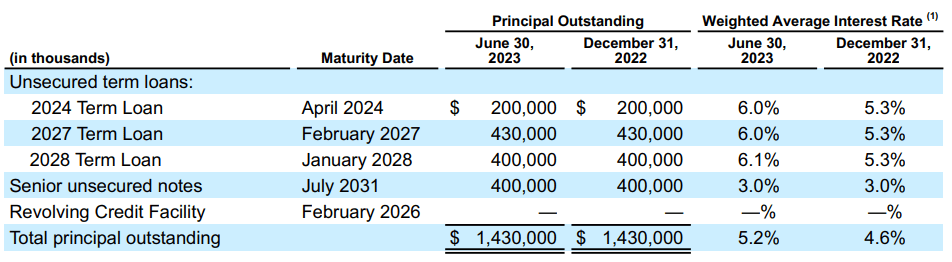

Of the 1,742 properties in this REIT's portfolio, 142 are EPRT's collateral for the mortgage loans they have extended to third parties. The average daily balance of the loans was higher in Q2-2023 versus the comparative quarter in 2022, resulting in the increase in the year over year interest income. Talking about the expenses and the elephant in the room, EPRT is no exception to the by now common theme of higher year over year interest expenses. The weighted average interest rate on its debt rose from 2.6% at June 30, 2022 to 5.2% at the end of Q2-2023, without taking into account the swaps in place.

{kind=link}

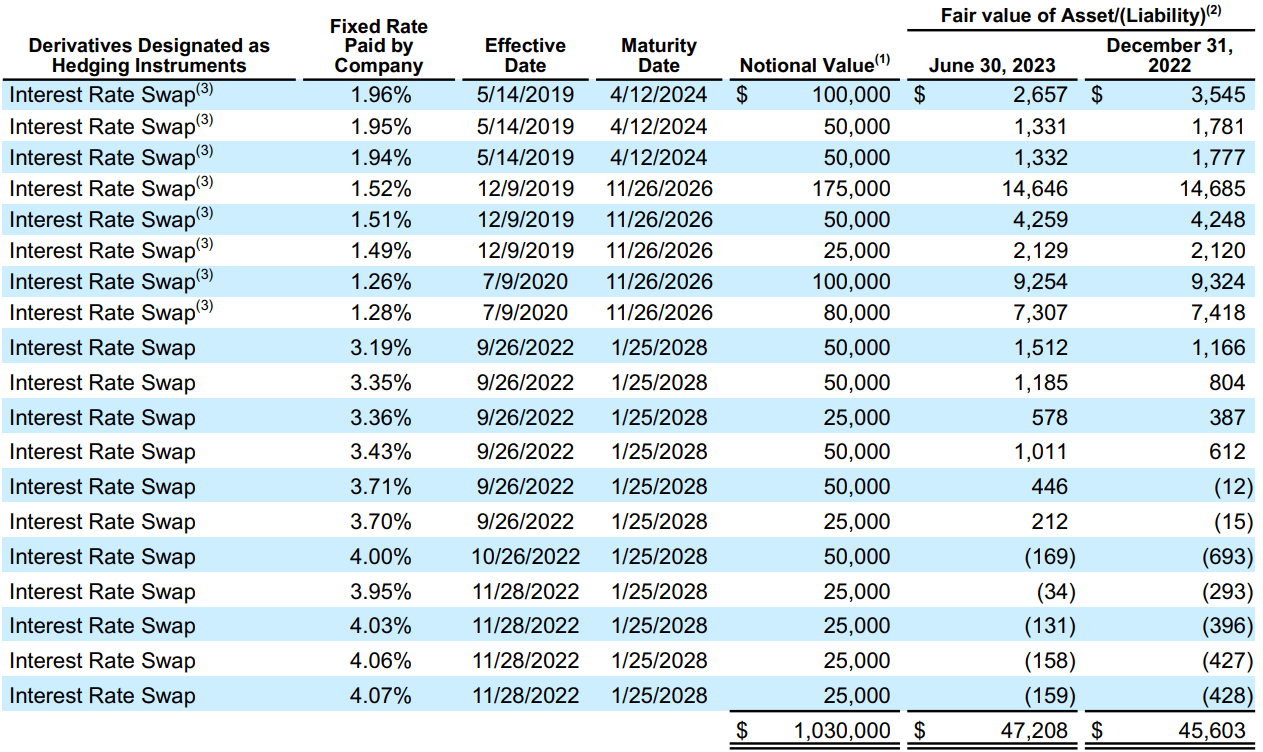

Taking the swaps into account, the weighted average interest rate increased from 2.8% at June 30, 2022 to 3.3% at June 30, 2023. About 20% of EPRT's swaps mature in 2024, replacement for which will be at higher than the rates they currently enjoy.

{kind=link}

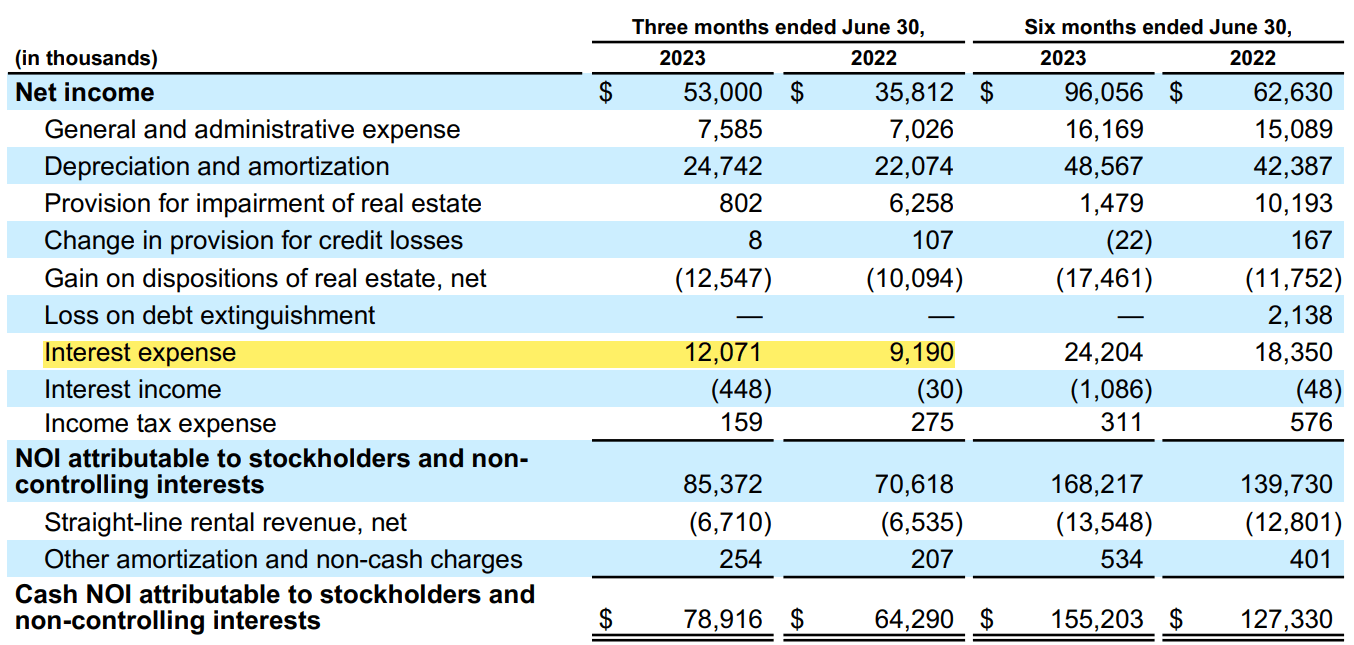

Coming back to Q2-2023, the increase in rates combined with the higher loan balance in 2023, resulted in a 32% increase in the year over year interest expense.

{kind=link}

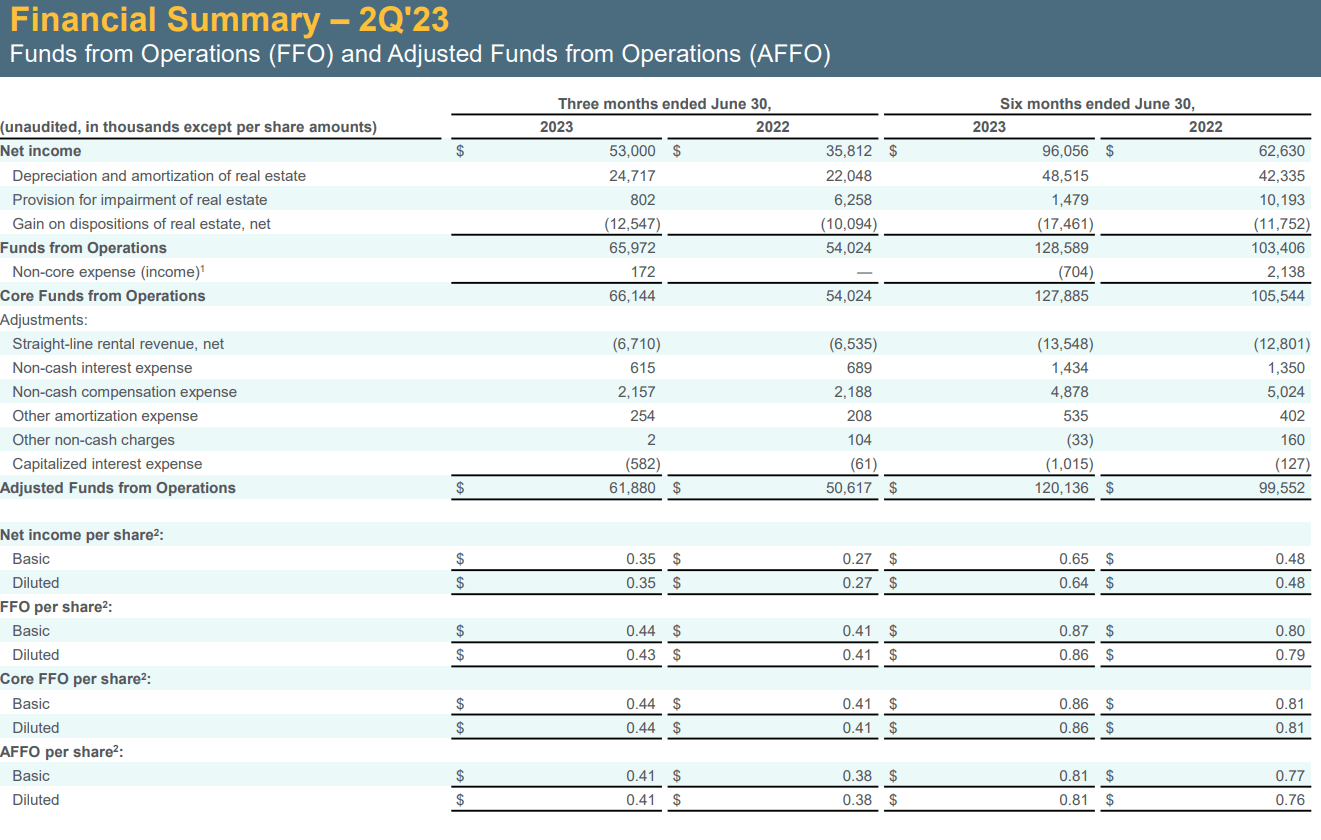

The net operating income still comfortably surpassed the 2022 number by close to 23%. The increase trickled down to the total funds from operations or FFO and adjusted funds from operations or AFFO.

{kind=link}

The per unit numbers, while higher year over year, were still more muted in comparison as a result of equity issuances.

That is par for the course for an equity REIT and EPRT is at least doing this exercise on an accretive basis. Using the simple inversion of the FFO method, we see that the cost of equity for this REIT is around 7.3%. The REIT's latest debt issuance carried an approximate rate of 5.25%. Even if we assume an equal weight between equity and debt funding, we can see that EPRT comes out ahead as its acquisitions are at a cap rate higher than that.

{kind=link}

EPRT ended the Q2-2023 results announcement on a positive note by raising its guidance for the balance of the year.

we raised our AFFO per share guidance range for the full year of 2023 to $1.62 to $1.65 per share, which reflects not only our 2Q investment performance, our visibility into our investment pipeline, and our performance expectations for the core portfolio. But importantly, the strength of our middle market tendency which experienced no material credit losses in the first half of the year. The midpoint of our increased guidance range implies a year-over-year growth rate of nearly 7%.

Source: Earnings Call Transcript

Liquidity and Debt

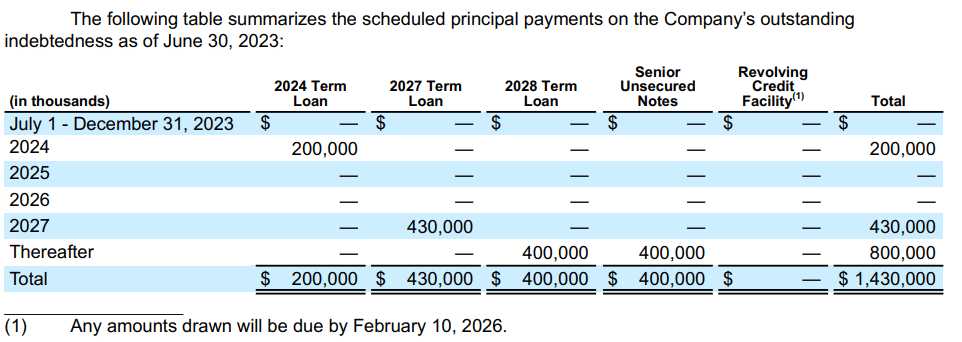

EPRT paid off the 2024 term loan with the proceeds from the 2029 term loan that it financed last month .

{kind=link}

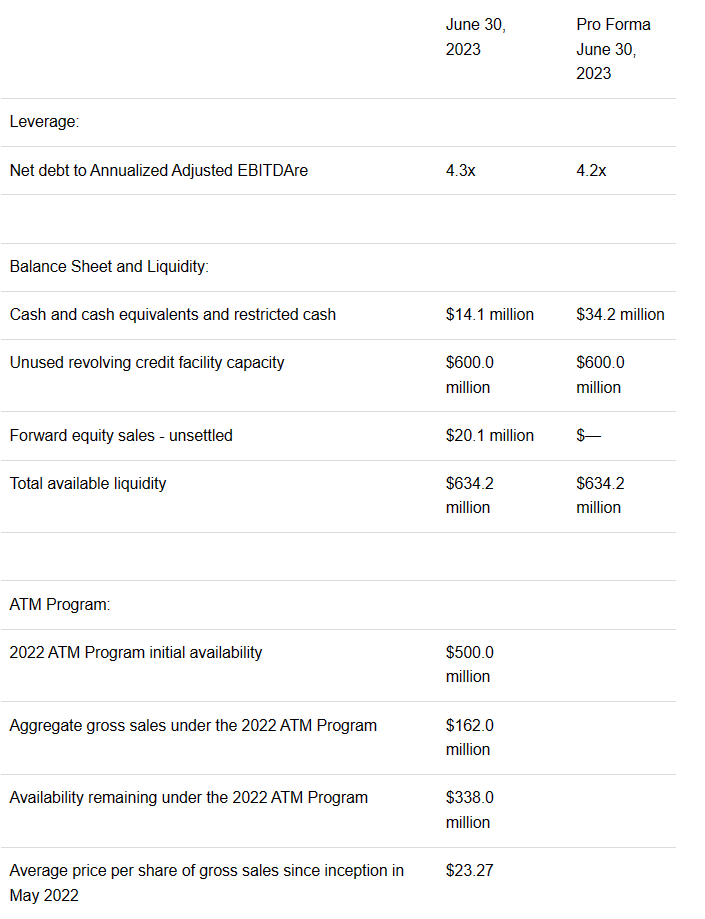

As a result of this, it has no near term maturities to deal with. Even if it drew from its $600 million revolving credit facility, the REIT has until 2026 to repay it. All in all, EPRT paints a very pretty picture in terms of its 4.3x net debt to annualized adjusted EBITDAre and liquidity.

{kind=link}

I Bought the Debt, But I Didn't Buy the Equity

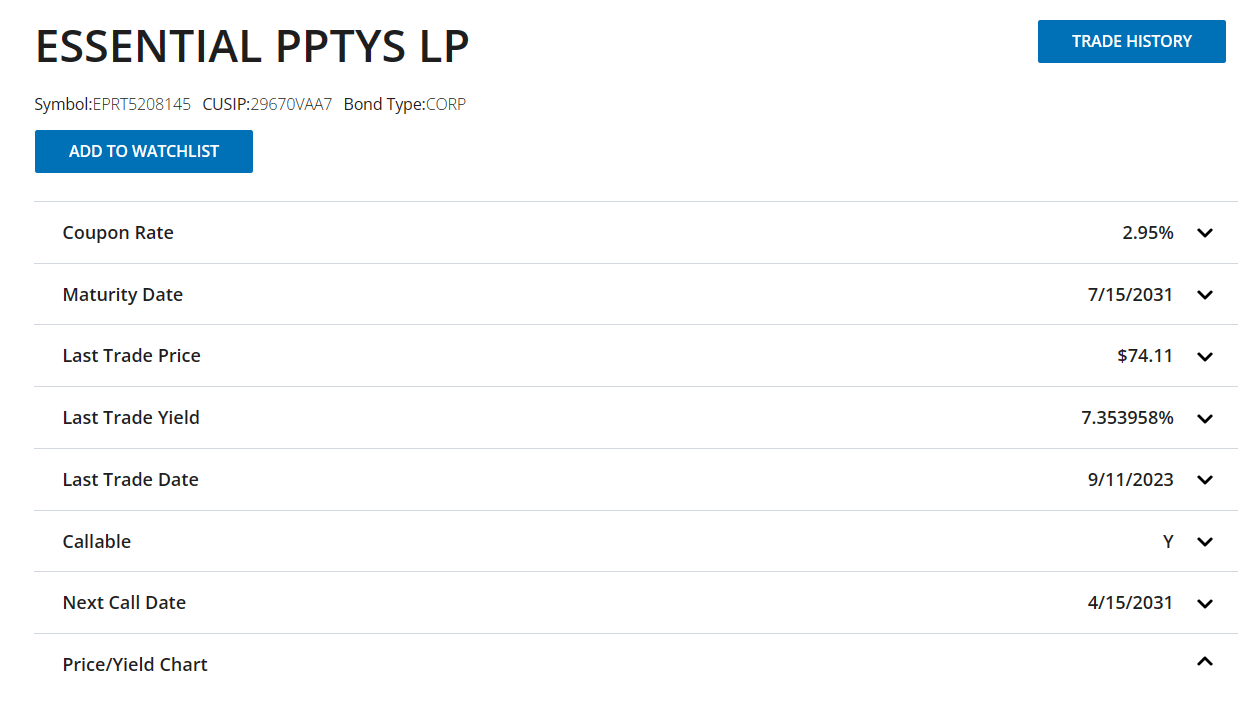

Last week, we analyzed FCPT and while it was essentially making all the right moves, the valuation was a dealbreaker for a bargain hunter like us. It traded at around 15x forward FFO, while EPRT trades at around close to 13.5x. This is around the same as O and a little higher than NNN, which trades around 12x. Another favorite of ours W. P. Carey Inc. ( WPC ) also trades at 12x. So while EPRT is not as expensive as FCPT, it is still not cheap enough for us to slap a buy on the common shares. We did however get involved with this quality REIT via its bonds, more specifically, those maturing in 2031.

{kind=link}

On our purchase price we got a 7.31% yield to maturity, which for this quality portfolio and this low debt, is pretty fantastic. The firm also carries a BBB rating from Fitch , which we think understates the quality of the bonds. So as Bob Marley would have put it , we aimed at just one tranche of the capital structure. We are happy with our purchase from earlier this year and will hold off on the common equity until it trades a multiple or two lower.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Essential Properties: I Bought The Debt, But I Didn't Buy The Equity