WTRG - Essential Utilities: A Cheap Pick For Steady Dividend Growth

2023-12-08 00:57:37 ET

Summary

- Utilities have characteristics that often make them smart picks for consistent dividend growth.

- Essential Utilities' operating revenue slightly declined in Q3, but its diluted EPS surged higher.

- The water and gas utility comfortably covers interest expenses from its earnings.

- Shares of Essential Utilities appear to be trading at a 29% discount to fair value.

- Assuming mean valuation reversion and accurate growth forecasts, the stock could meaningfully outperform the S&P 500 in the next 10 years.

As a dividend growth investor, I am always seeking out new dependable dividend growers to add to my portfolio. It just so happens that nine of my 101 dividend growth stocks are regulated utilities, which isn't a coincidence.

Regulated utilities are often some of the most established dividend growers in the investment universe. Because utilities are often the only game in town within a service area, they operate as virtual monopolies. To reasonably prevent price gouging, regulatory authorities oversee the rate case activity. The necessity of the services provided by utilities is also another characteristic that I like.

A look at Dividend Kings' list of Dividend Champions (e.g., companies with 25 or more years of dividend growth) reveals that there are 134 entries. Of those, 17 are utilities. This reinforces the argument that utilities are well-represented among the highest-quality dividend growers.

One utility in my portfolio that also appears on this list is Essential Utilities ( WTRG ). For the first time since October , I will revisit its operating fundamentals and valuation to explain why I am maintaining my buy rating.

{kind=link}

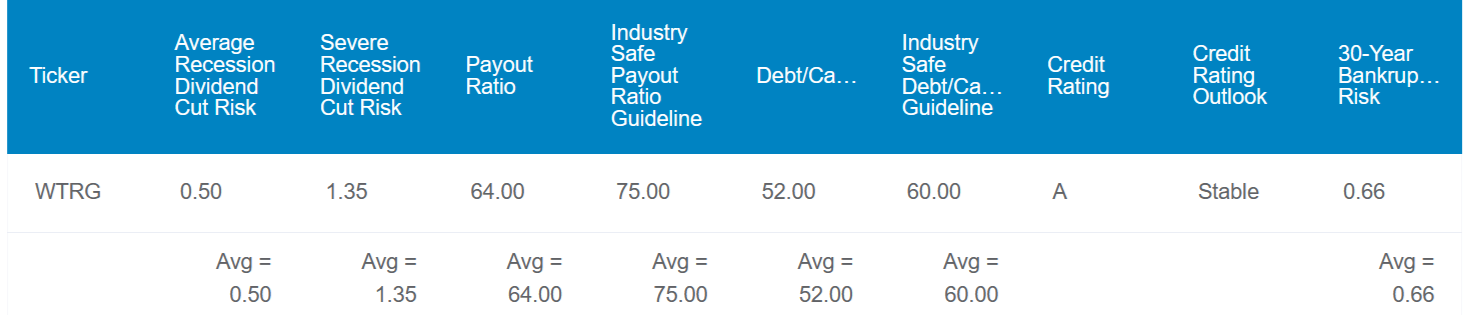

WTRG isn't a pure income play, with a 3.4% dividend yield. This is below even the current 10-year U.S. treasury of 4.1% . However, the company compensates for this lower starting yield in a multitude of ways. For one, WTRG's 64% EPS payout ratio is well under the 75% that rating agencies prefer from utilities. This gives the company plenty of room to keep growing the dividend at a high- single-digit rate annually over the long haul.

WTRG's 52% debt-to-capital ratio is also almost squarely within its targeted ratio of 50% to 55%. This itself is conservative versus the 60% debt-to-capital ratio that credit rating agencies want to see from utilities. Thanks to its manageable dividend obligation and prudent capitalization, WTRG earns an A credit rating from S&P on a stable outlook.

These reasons are precisely why Dividend Kings pegs the risk of a dividend cut from the utility in the next average recession at 0.5%. Even if the next recession were severe, that probability is still just 1.35% for WTRG.

{kind=link}

As I will confirm with a look at its recent operating results, WTRG appears to be a fundamentally wonderful business. Even better, the underlying stock is attractive here at the current $36 share price from my perspective.

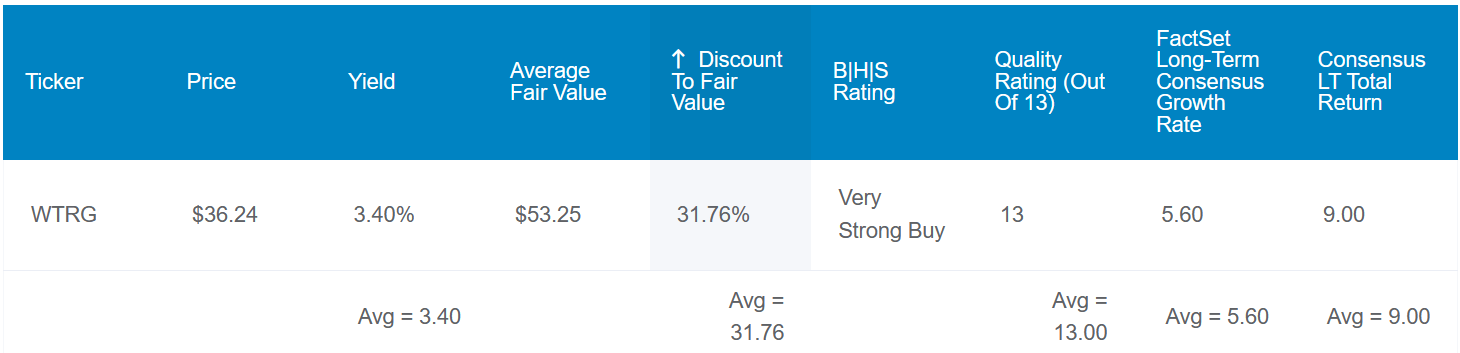

This is because according to Dividend Kings' historical dividend yield and P/E ratio valuation metrics, WTRG is worth $53 a share. I came out to a similar fair value per share of $49, which was driven by these inputs in the dividend discount model: A $1.2284 annualized dividend per share, a 10% discount rate, and a 7.5% annual dividend growth rate.

Based on an average $51 fair value, WTRG is currently priced 29% below fair value. If the company returns to that fair value and meets the growth consensus, here is its 10-year total return potential:

- 3.4% yield + 5.6% FactSet Research annual growth consensus + a 3.5% annual valuation multiple upside = 12.5% annual total return potential or a cumulative 10-year 225% total return versus the 9% annual total return potential of the S&P 500 ( SP500 ) or a 137% cumulative 10-year total return

Even With A Mixed Third Quarter, Fundamentals Are Still Solid

{kind=link}

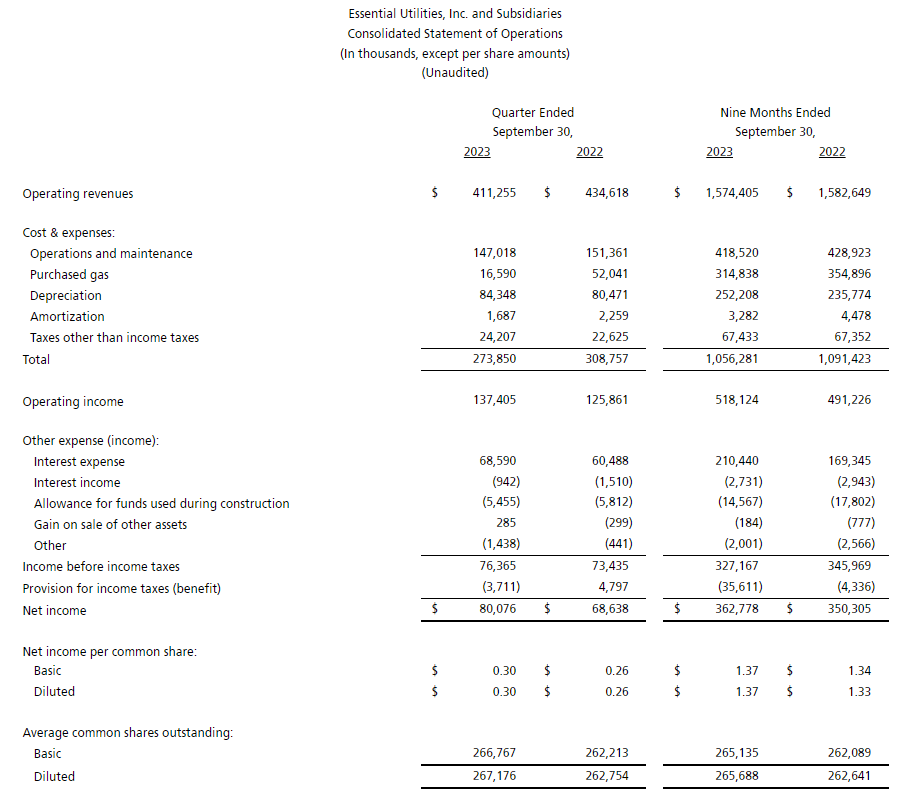

On November 6, WTRG reported its financial results for the third quarter ended September 30. The company's $411.3 million in operating revenue declined by 5.4% year-over-year, also missing the analyst consensus by $43.9 million .

A contracted topline isn't what I like to see from a utility, but I still think these results were fine. Regulatory recoveries and organic/acquisition growth in its regulated water segment contributed to respective operating revenue growth of $14.1 million and $3.2 million during the third quarter.

However, these tailwinds were offset by two headwinds that I would argue will not persist indefinitely. Mostly, the company was hurt by a drastic drop in natural gas commodity prices over the year-ago period per CFO Dan Schuller's opening remarks in the earnings call . That alone weighed on operating revenue to the tune of $35.5 million in the third quarter. Additionally, lower water consumption in northern states due to rainier weather more than offset higher consumption in the south. That resulted in a $5.7 million decrease in WTRG's operating revenue for the quarter as well.

The company's diluted EPS increased by 15.4% year-over-year to $0.30 during the third quarter. This exceeded the analyst consensus by $0.01. Less purchased gas expenses and disciplined cost management overall caused WTRG's total operating expenses to drop by 11.3% over the year-ago period. That is how profitability improved as operating revenue temporarily dipped.

As noted in my previous article, WTRG anticipates that it will invest $1.1 billion annually in capital projects through 2025. The corresponding growth in the company's rate base should lead operating revenue and earnings higher over time. That is why FactSet Research currently believes earnings will grow by 5.6% annually over the long run.

Finally, WTRG is financially vigorous. The company's interest coverage ratio through the first nine months of 2023 was 2.6. This suggests that WTRG should have minimal issues in paying dividends to its shareholders, investing in its future, and servicing its debt.

An Appealing Combo Of Starting Income And Growth Potential

As I alluded to in the opening, there are higher-yielding alternatives out there than WTRG. But it has shined at delivering respectable dividend growth to its shareholders throughout its 32-year dividend growth streak.

WTRG is forecasted to generate $1.87 in diluted EPS in 2023. Measured against the $1.1882 in dividends per share paid during this year, that works out to a 63.5% payout ratio. This should allow the company to hand out plenty more healthy dividend raises moving forward.

Risks To Consider

WTRG has arguably earned the distinction of being a flawless 13/13 ultra SWAN per Dividend Kings' quality rating. However, the company still has risks.

I would reiterate WTRG's rate base concentration in one market as being one of the more notable operational and regulatory risks. For context, approximately 75% of the company's rate base as of the end of 2022 was concentrated in Pennsylvania (slide 6 of 74 of WTRG's November 2023 Investor Presentation ). Although this is one of the more constructive regulatory environments in the country for utilities, that may not be the case indefinitely. This leaves WTRG meaningfully reliant on favorable rate case outcomes in the state to fuel growth.

Another risk to WTRG is the potential for water supply contaminants to result in additional costs that may not be recoverable, as well as a disruption to operations. If it were to occur, this could also weigh on the company's fundamentals.

Finally, WTRG stock will likely be rangebound in the near term until interest rates begin to come back down. Whenever this does happen, the stock could rally as it becomes more in demand and is again viewed as an interesting option by more investors.

Summary: A Pick For Deep Value And Dividend Growth

{kind=link}

{kind=link}

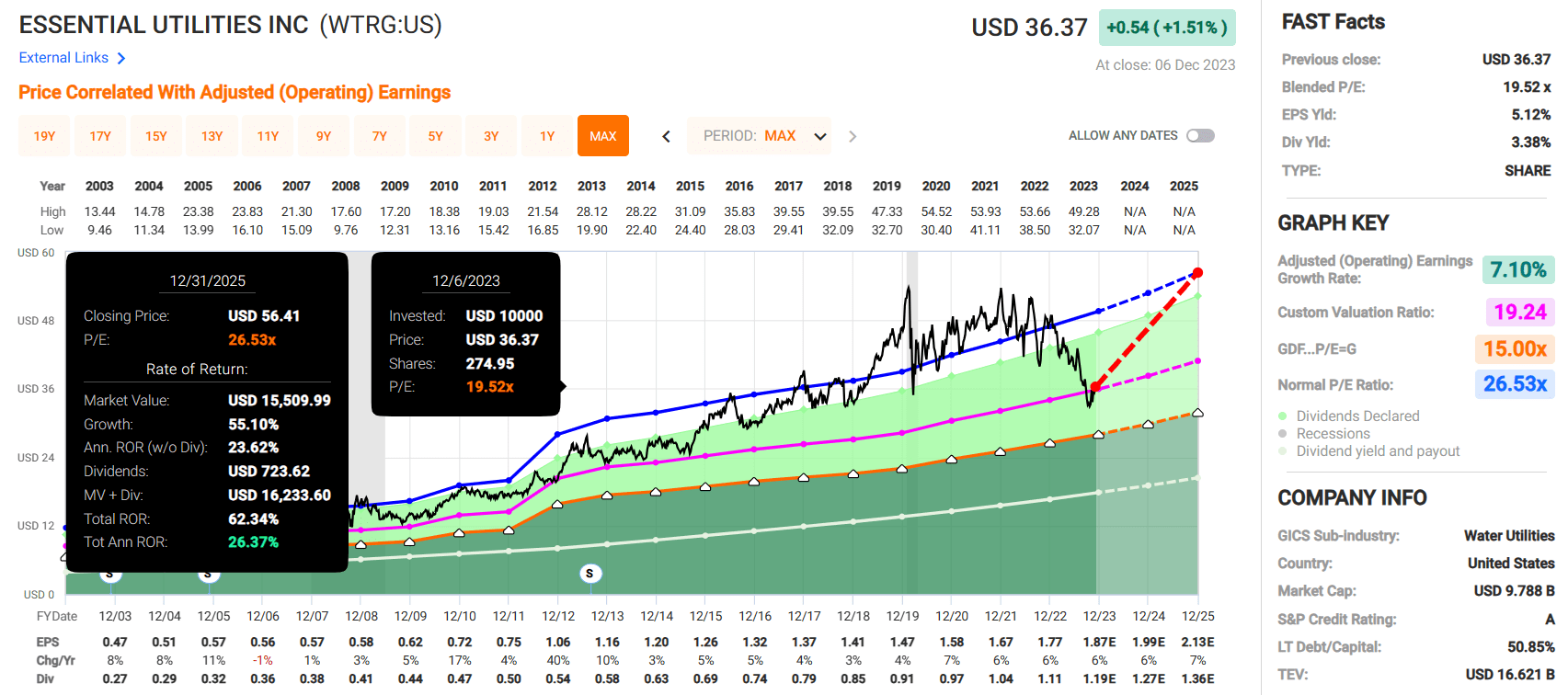

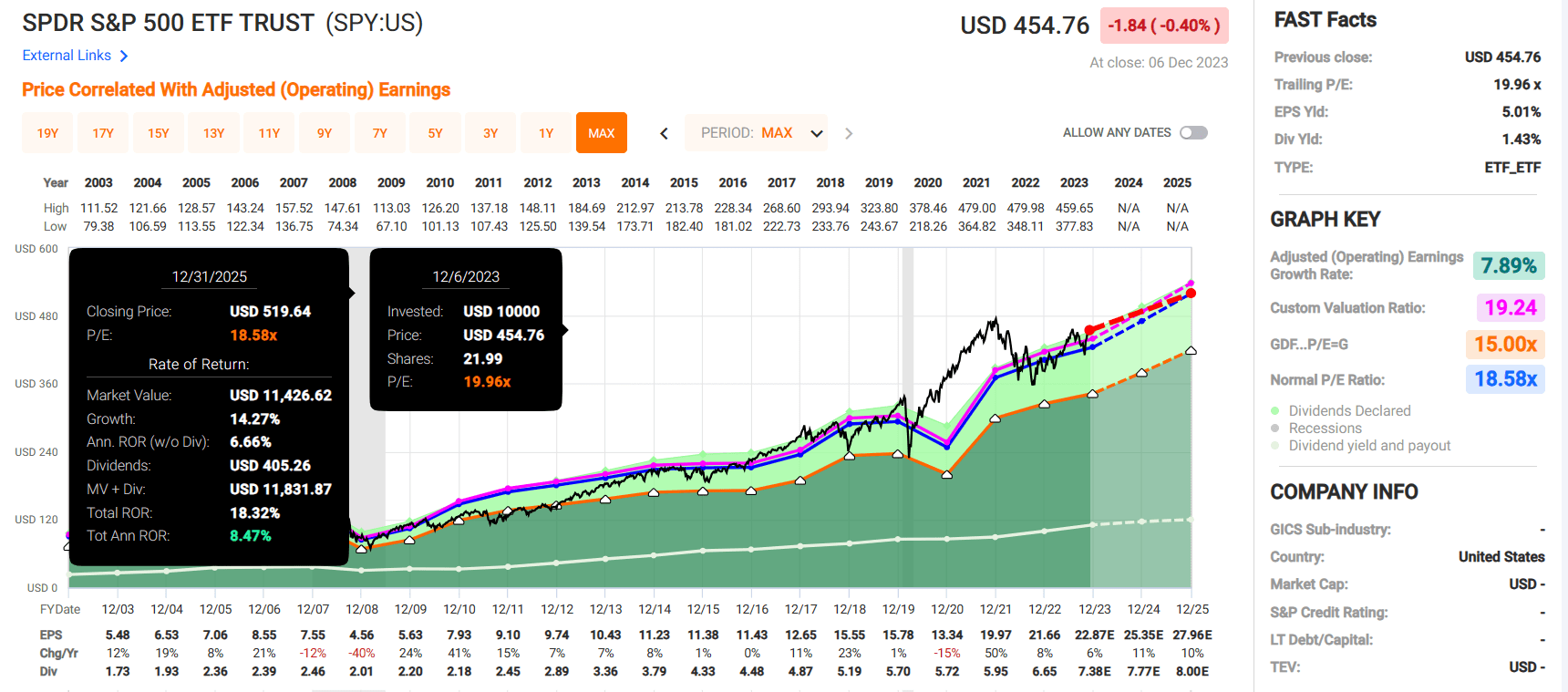

Much of the last two years have been characterized by a rising/elevated interest rate environment. Thus, it's no surprise that shares of WTRG have been beaten down to their current P/E ratio of 19.5, which is well below the historical P/E ratio of 26.5 per FAST Graphs. When interest rates inevitably begin to get cut, this could be setting the stock up for a significant recovery. If the company reverts to its historical P/E ratio and grows as forecasted, it could deliver 62% cumulative total returns through 2025.

That's much better than the 18% cumulative total returns that the SPDR S&P 500 ETF Trust ( SPY ) is expected to generate during that time. This builds an intriguing margin of safety into WTRG's stock, which is why I am reaffirming my buy rating.

For further details see:

Essential Utilities: A Cheap Pick For Steady Dividend Growth