WTRG - Essential Utilities Is The Cheapest It Has Been In More Than A Decade

2023-10-07 00:56:17 ET

Summary

- Essential Utilities stock has declined 30% and is currently trading at a 10-year low price-to-earnings ratio.

- The company has a wide business moat and is on a reliable growth trajectory.

- Analysts expect 7-8% growth in earnings per share, and the stock has a potential upside of 45% when interest rates normalize.

About two years ago, I advised investors to avoid Essential Utilities (WTRG) due to its rich valuation back then. I reiterated my thesis last year, as the stock had remain overvalued. Since my first article, the stock has declined 30% and thus it has dramatically underperformed the broad market, given that the S&P 500 has shed only 2% over the same period. Due to its decline, Essential Utilities is currently trading at a 10-year low price-to-earnings ratio of 17.9 . This is by far the cheapest valuation level of the stock in more than a decade. The cheap valuation has resulted from the surge of interest rates to 16-year highs. Whenever interest rates begin to normalize, Essential Utilities is likely to highly reward its shareholders.

Business overview

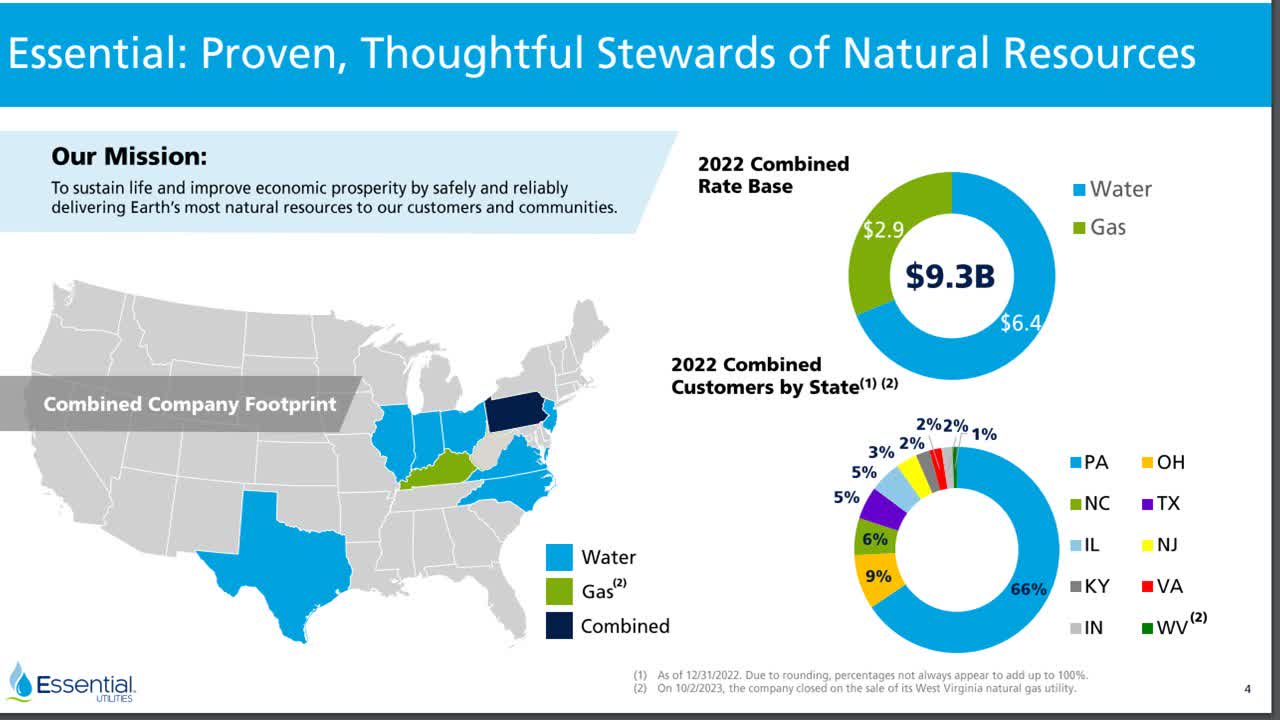

Essential Utilities is one of the largest publicly traded providers of water and natural gas in the U.S., with about 8.9 million customers across ten states. Its most important segment is its regulated water business, but the distribution of natural gas generates a significant portion of earnings as well.

{kind=link}

The water business comprises 71% of the rate base of the utility while the gas division comprises the remaining 29% of the rate base. The company has 66% of its customers in Pennsylvania and 9% of its customers in Ohio.

Just like most utilities, Essential Utilities spends excessive amounts on the expansion, improvement and maintenance of its network. These amounts somewhat burden the balance sheet of the company but they also form an almost unsurpassable barrier to entry for potential competitors. As a result, the company enjoys one of the widest business moats investors can hope for.

Moreover, Essential Utilities has proved capable of acquiring smaller companies and integrating them into its network. It has acquired nearly 200 companies over the last decade and has repeatedly provided guidance for 2%-3% average annual customer growth over the long term.

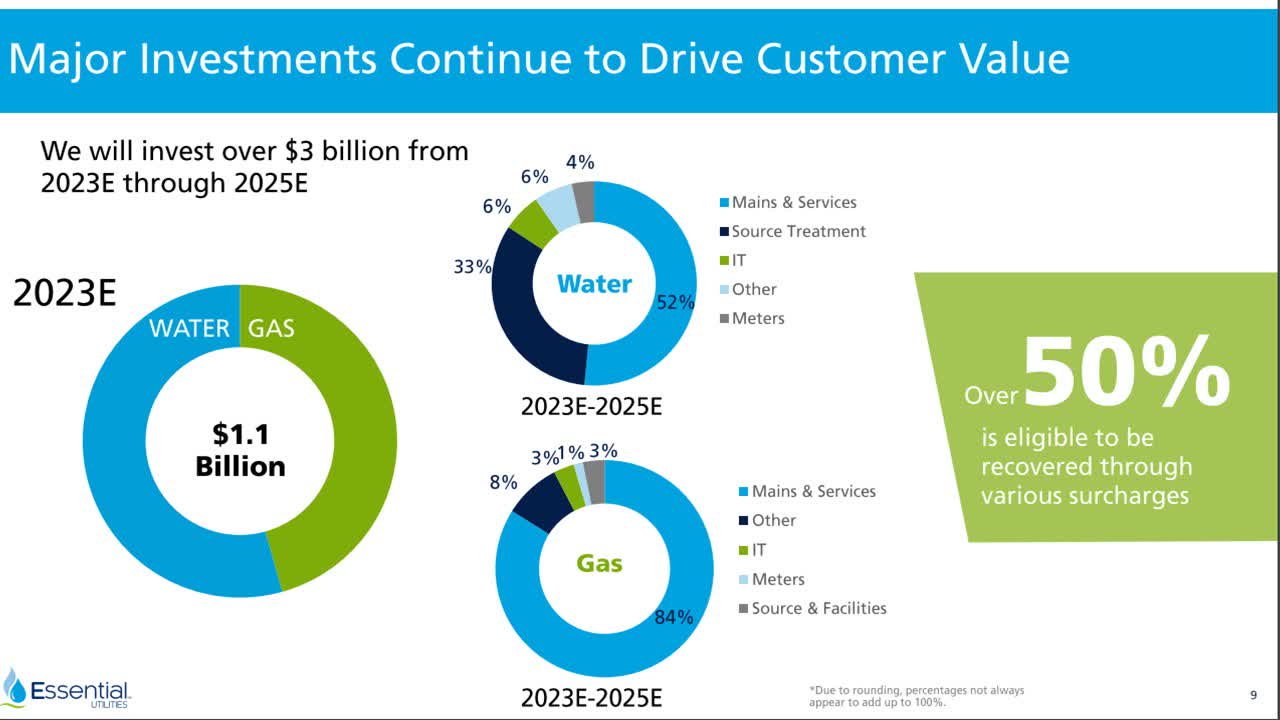

While acquisitions are likely to remain a material growth driver, the primary growth driver is the investment program of the company. Essential Utilities expects to invest more than $3 billion in the expansion and improvement of its infrastructure until the end of 2025.

Essential Utilities Growth Prospects (Investor Presentation)

{kind=link}

As this amount is 34% of the current market capitalization of the stock, it is obvious that the company is heavily investing in future growth. More than half of the invested capital is eligible to be recovered through rate hikes. Therefore, Essential Utilities has promising growth prospects ahead.

Indeed, management has repeatedly provided guidance for 5%-7% annual growth of earnings per share until at least 2025. This guidance compares favorably to the 4.8% average annual growth of earnings per share of the utility over the last decade. It is also important to note that the company enjoys reliable rate hikes year after year, as regulators have to provide incentive to the company to invest in the improvement and expansion of its infrastructure.

Analysts agree on the promising growth potential of Essential Utilities. They expect it to grow its earnings per share by 8% next year and by 7% in 2025. It is also remarkable that Essential Utilities has missed the analysts' estimates in only 4 of the last 20 quarters. Even in these four quarters, the company missed the estimates by only $0.01 or $0.02. This is a testament to the reliable and predictable growth of earnings of the utility. To cut a long story short, Essential Utilities is likely to meet or exceed the analysts' expectations for 7%-8% growth of earnings per share in the next two years.

Valuation

Essential Utilities is currently trading at a price-to-earnings ratio of 17.9 , which is far lower than the 10-year average of 25.0 of the stock. In fact, the current valuation of the stock is the cheapest it has been in more than a decade.

It is also remarkable that the stock is trading at only 15.5 times its expected earnings in 2025. The extremely cheap valuation has not resulted from poor business performance, as the company is on track for 5% growth of earnings per share this year, to a new all-time high. Instead, the cheap valuation has resulted from the surge of interest rates to a 16-year-high level. High interest rates enable investors to identify attractive yields in many securities, both bonds and stocks, and thus they render the dividends of utilities less attractive. This is why the stock of Essential Utilities is likely to remain suppressed as long as interest rates remain around their current level.

However, interest rates are not likely to remain around their 16-year high for years. Such high interest rates are likely to finally cool the economy as intended by the Fed. They are likely to reduce the total investment in the economy as well as the demand for new houses and thus they are likely to eventually drive inflation to the target zone of the Fed. The aggressive interest rate hikes have already born fruit, as inflation has cooled from a peak of 9.2% in the summer of 2022 to 3.6% now. Whenever inflation reaches the target range of 2.0%-2.5% of the central bank, the latter is likely to begin reducing interest rates. When that happens, the stock of Essential Utilities will probably enjoy a strong tailwind, i.e., the reversal of the 31% decline incurred this year. In other words, the stock has approximate upside of 45% (=100/69 - 1) off its current price.

Numerous investors would like to gain exposure to the consistent and reliable mid-single-digit growth of earnings per share of Essential Utilities, given its rock-solid business model, the absence of competition and the immunity of the company to recessions. However, thanks to these characteristics and the depressed interest rates that prevailed until 2021, the stock had remained richly valued for several years. Now that interest rates have skyrocketed, it is the ideal time to purchase this reliable and resilient stock and remain invested with a long-term perspective.

Dividend

Essential Utilities is a Dividend Aristocrat, with 32 consecutive years of dividend growth. It has achieved such a long dividend growth streak thanks to its consistent earnings growth and its resilience to recessions, as people do not reduce their water consumption even under the most adverse economic conditions.

Due to its 31% decline this year, Essential Utilities is currently offering a 10-year high dividend yield of 3.7% .

Moreover, the company has a healthy balance sheet, with an A credit rating from S&P and a Baa2 rating from Moody's. Interest expense consumes just 39% of operating income while net debt (as per Buffett, net debt = total liabilities - cash - receivables) is standing at $10.2 billion. This amount is 117% of the market capitalization of the stock but it is manageable thanks to the rock-solid business model of the company and its reliable growth trajectory. This helps explain the above strong credit ratings earned from the rating firms.

Given also its healthy payout ratio of 64% , Essential Utilities is likely to continue growing its dividend for many more years. The company has grown its dividend by 7% per year on average over the last decade and over the last 5 years. As it is expected to grow its earnings at a similar pace in the upcoming years, it is likely to keep raising its dividend by about 7% per year in the years ahead. Overall, investors are given the opportunity to lock in a 10-year high dividend yield and rest assured that the dividend will keep rising meaningfully for many more years.

The bottom line

Due to its mundane business model and its overvalued status for more than a decade, Essential Utilities has passed under the radar of most investors for years. However, due to the surge of interest rates, the stock has been beaten to the extreme this year. As a result, it has become highly attractive from a long-term point of view. Whenever interest rates normalize, the stock is likely to highly reward investors.

For further details see:

Essential Utilities Is The Cheapest It Has Been In More Than A Decade