ESS - Essex Property Trust: I Expect The West Coast To Outperform Next

2023-12-11 11:35:58 ET

Summary

- The housing market in California is expected to remain robust, with Essex Property Trust likely to benefit.

- The West Coast, including California, could outperform other regions due to low supply and the potential for job growth in the tech industry.

- Recent improvements in delinquencies and the ability to increase rents make ESS an attractive investment option.

Dear readers,

I last wrote an article on Essex Property Trust ( ESS ) back in June, highlighting three key reasons why the housing market in California is likely to remain robust and issuing a buy rating at $233 per share.

ESS represents my largest US apartment REIT holding, so I follow the stock quite closely. I'd argue that, since my last article, the outlook for ESS has improved materially, despite the price barely moving with a total RoR of -3%.

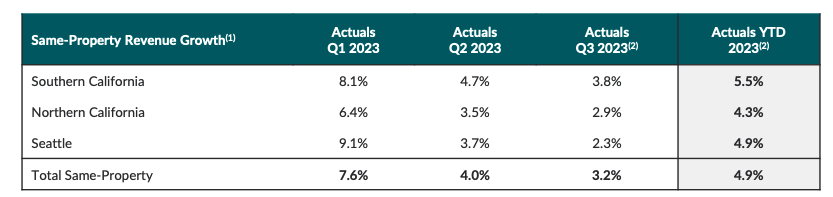

Recall that ESS owns units in three regions - Southern California (42%), Northern California (41%), and Seattle (17%).

All three regions have been seeing relatively low revenue growth, especially when compared to the East Coast. Over the past 9 months, ESS has seen its revenues rise by 4.9% YoY, which is less than half of AvalonBay's ( AVB ) East Coast portfolio which has averaged 10.4% growth over the same period.

{kind=link}

Why West Coast Could Outperform Next

But I expect that the West Coast will eventually catch up.

We actually saw similar dynamics last year between the Sunbelt and East Coast. The Sunbelt had, by far, the highest rent growth in the country in 2022, while the East Coast was seeing barely any growth. This year, however, the East Coast, and especially the NYC area has made a comeback and surpassed growth in the Sunbelt substantially. I have reason to believe that the West Coast could be next.

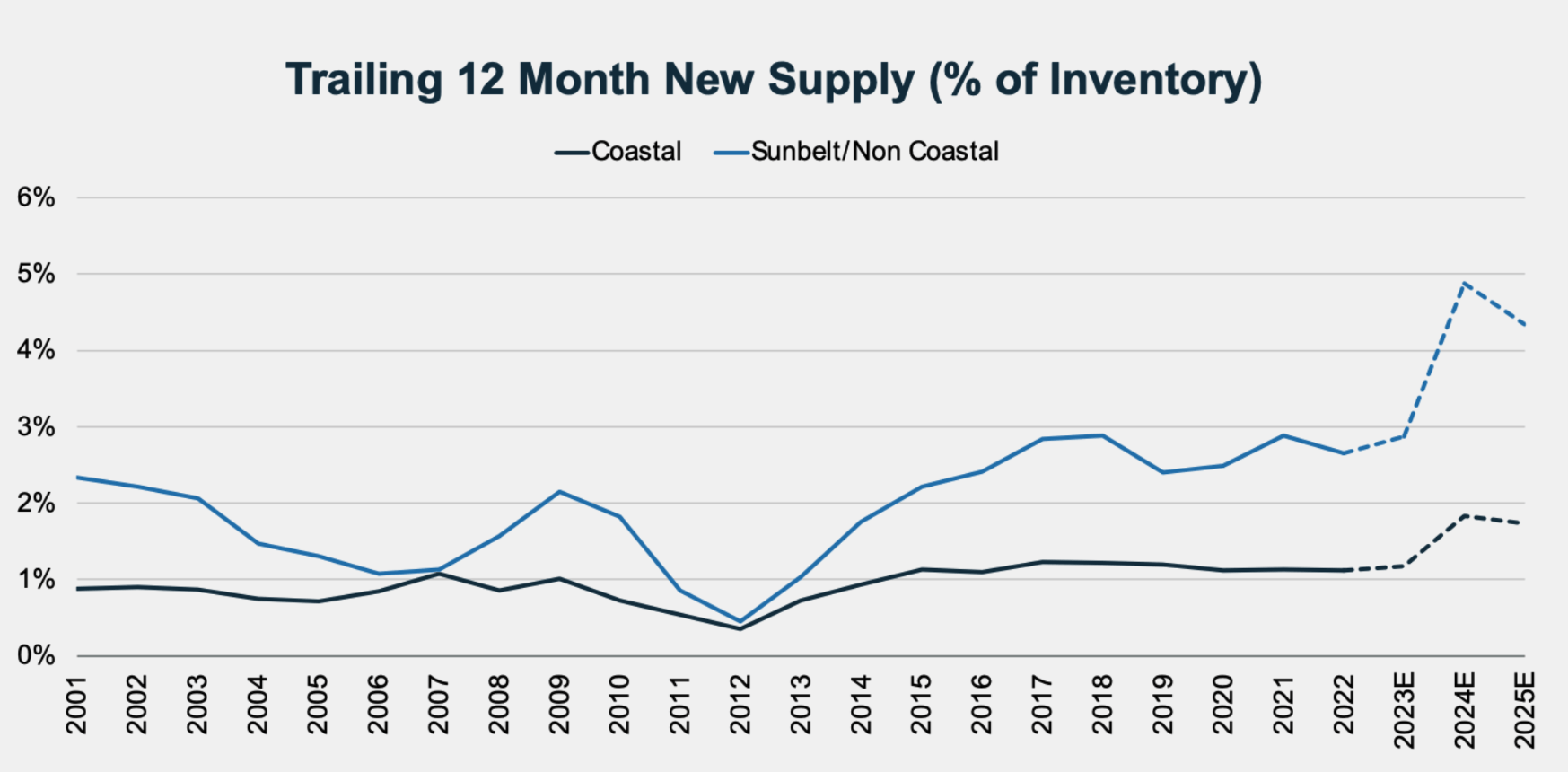

One of the main reasons is that the supply of new space remains extremely low. While in the Sunbelt total stock increases by 3-4% per year, construction activity in the West Coast remains very muted with completions expected at only 0.5% of total stock in 2023 and between 0.5-0.7% beyond (as evident from already issued building permits which make a great proxy for future supply).

{kind=link}

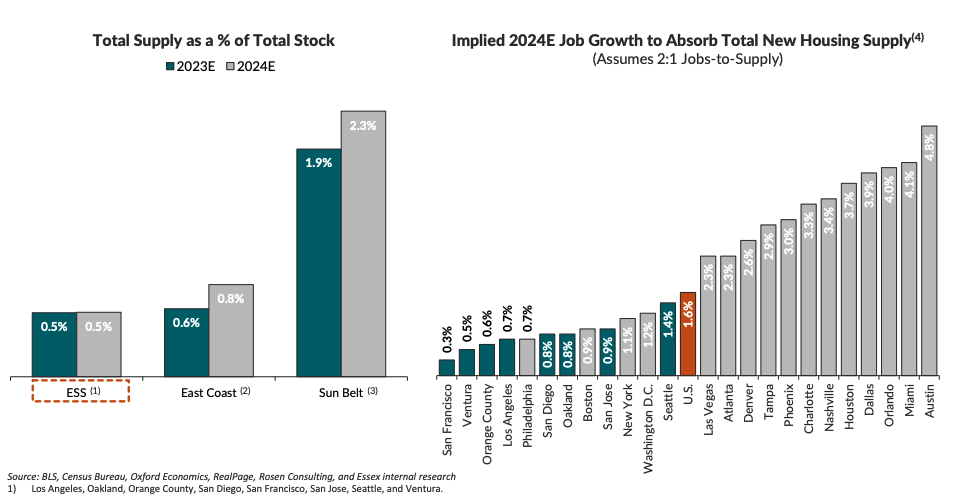

Low supply puts the market at a major advantage, because only minimal job growth is needed to absorb the supply. While nationally, job growth of 1.6% is needed to offset newly constructed stock, most of ESS's markets average under 0.7% annual jobs growth. This is much lower than most Sunbelt markets, with required job growth of 3-4%.

{kind=link}

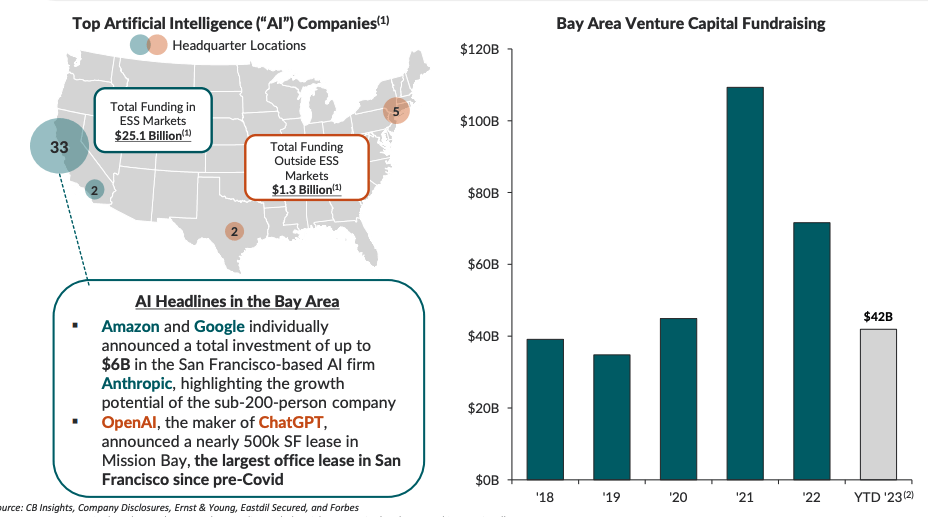

And the good thing is that despite what the headlines would have you believe, California is very likely to remain the #1 tech hub of the country and as a result, many new jobs will likely be created in the state in the future.

Texas has been attracting a lot of investment (and attention) lately, but I want to point out that AI-related funding in California remains substantially higher than elsewhere ($25 Billion vs $1.3 Billion).

{kind=link}

Moreover, demand for space will likely continue to be strengthened by the unaffordability of housing, which is amongst the worst in the country in Essex's markets. With owning 2.6x more expensive than renting, it's very likely that young people will postpone their decision to buy, simply out of necessity.

Recent Results

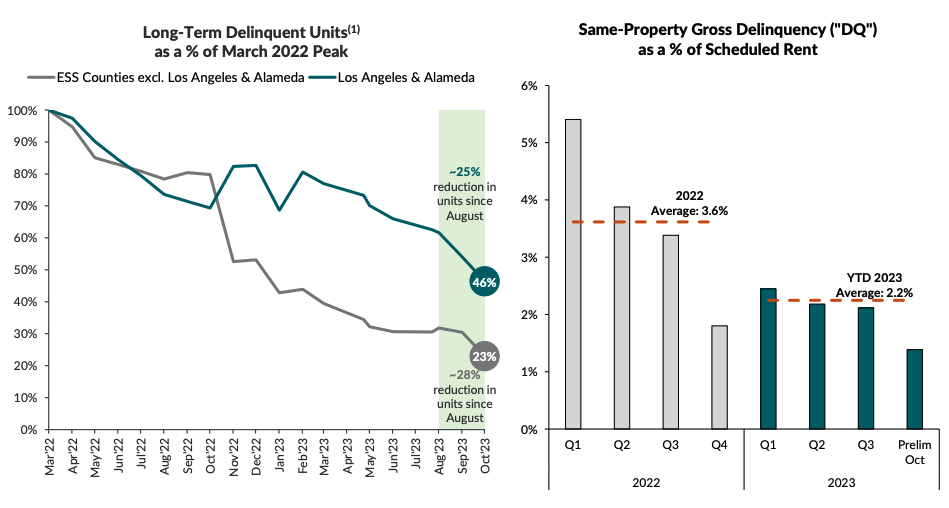

Apart from decent rent growth, recent results have shown very promising improvements in delinquencies, which Essex has been struggling with ever since Covid due to extremely stringent eviction protection measures in California.

Last year, delinquencies had a cumulative 3.6% negative effect on rental income, but as most eviction moratoria have been lifted, the REIT has been able to bring delinquencies down to just 1.3% of rent in October.

Evicting tenants has a short-term negative impact on occupancy and rent growth, but as units get re-leased the longer-term effect should be quite positive, and as a result, I expect rent growth to accelerate next year.

I also want to point out that apartment REITs are in a much better position than net lease REITs when it comes to their ability to increase rents in an inflationary environment. This is because tenant turnover is generally quite high for apartment REITs, with an average tenant staying for just 2-3 years. Consequently, the REIT is not fixed into long lease contracts with predetermined rent increases and can more easily react to changes in market rents.

{kind=link}

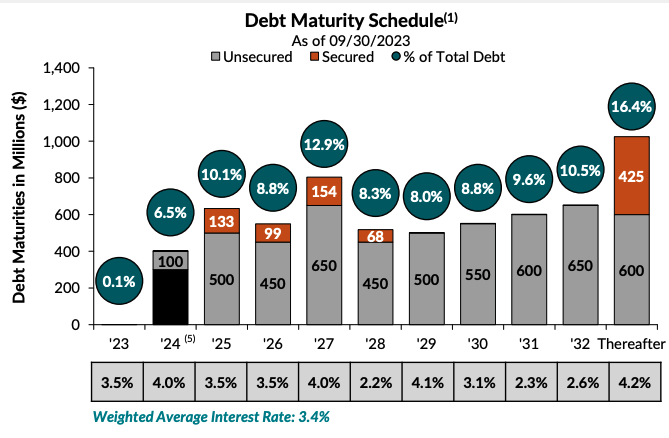

Essex maintains a BBB+ rated balance sheet with a reasonable net debt to EBITDA of 5.5x, down from 5.8x last year. The vast majority of debt (97%) is fixed-rate, the REIT enjoys a low weighted average interest rate of 3.4% and near-term maturities are manageable.

There is a $400 Million debt maturity next year, but $300 of this has already been refinanced by a 10-year secured loan, closed in July at a fixed rate of 5.08%. As a result, I expect a minimal cash flow impact from high interest rates next year.

And even if interest rates stay elevated until 2025, refinancing the debt due that year is likely to only have a 1% negative effect on total FFO, which can easily be offset by rent growth.

{kind=link}

Valuation

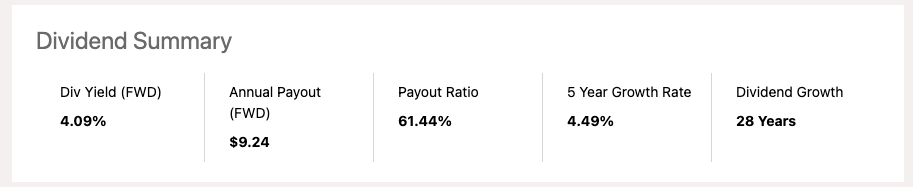

ESS has a long history of paying and increasing its dividend, which has made it a dividend Aristocrat. A low payout ratio and growing FFO make future dividend increases very visible.

{kind=link}

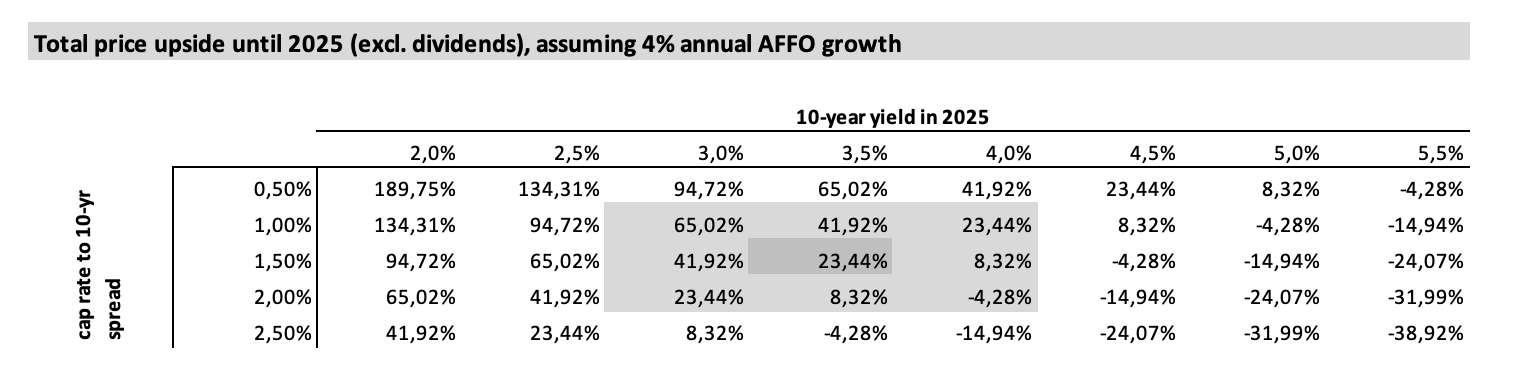

On top of the 4% dividend, I expect further upside when long-term yields decline. In my base case, I assume that FFO will grow by 4% per year until 2025, which is more or less in line with consensus.

ESS currently trades at an implied cap rate of 5.4% which is 120 bps above the 10-year treasury yield. My base case assumed a slightly more conservative spread of 150 bps, which seems appropriate for ESS's assets, and a drop in long-term yields to 3.5%. These assumptions yield a potential upside of 23%, realized over two years.

{kind=link}

4% divided + 11.5% annualized upside = 15%+ total return potential

While this sort of upside is unlikely to get realized before interest rates and yields drop, I believe that ESS deserves a spot in a conservative income portfolio, especially after recent improvement in delinquencies.

I reiterate my buy rating here.

For further details see:

Essex Property Trust: I Expect The West Coast To Outperform Next