LRLCF - Estée Lauder: Down 11% In A Month Since Q2 FY23 Results

Summary

- EL shares fell 4.4% on the day when Q2 FY23 results were released and have now fallen by more than 11% in a month.

- Including currency, Net Sales fell 17% and EPS fell 49% year-on-year in the quarter, and further declines are expected next quarter.

- EL has been impacted by a variety of problems in China, the U.S. and Korea, some of which appear to be of its own making.

- EL expects growth to resume in Q4 and hints at a strong FY24. Market growth and EL's strong brands should carry it through.

- With shares at $244.64, EL is at 40x CY19 earnings and we expect a total return of 37% (10.2% annualized) by June 2026. Buy.

Introduction

The Estée Lauder Companies Inc. ( EL ) released Q2 FY23 results (for October-December 2022) on February 2. EL stock fell 4.4% that day and has continued falling, and is now down by more than 11% from before the results:

{kind=link}

EL continues to suffer from headwinds. Including currency, Net Sales fell 17% and EPS fell 49% year-on-year. EL has been impacted by problems in China, the U.S. and Korea, some of which appear to be of its own making. Net Income and Free Cash Flow (“FCF”) were lower in CY22 than in pre-COVID CY19. Q3 FY23 is expected to show another decline, and full-year outlook has been reduced significantly. Management now expects growth to resume in Q4 and hints at a strong FY24. We believe structural growth in Prestige Beauty and EL’s strong brands will help management eventually overcome execution issues. Relative to CY19 financials, EL shares are at a 40.2x P/E and a 1.7% FCF Yield. Our forecasts indicate a total return of 37% (10.2% annualized) by June 2026. Buy.

Estée Lauder Buy Case Recap

Our investment case on EL is based on the following:

- The Beauty market will continue its strong structural growth, as an aspirational category for consumers, helped by growing demand from APAC (especially China) and premiumization (especially in Skin Care).

- EL has strong global franchises built on leading brands, high-quality products, scale, innovation and marketing capabilities, and will therefore grow sales faster than the market

- Natural operational leverage on EL’s platform will enable it to grow earnings faster than sales

- EL's focus on the Prestige segment and its higher exposure to Skin Care will also enable it to grow faster than its main rival L'Oréal, in line with its longer-term track record

Prior to COVID-19, EL targeted Net Sales growth of 6-8% and EBIT Margin expansion of approx. 50 bps annually (in constant currency), which (with an EBIT margin of around 20%) imply an annual EBIT growth of approximately 11%:

| EL FY20-22 Outlook (Before COVID-19) Source: EL presentation at Bernstein conference (May-19). |

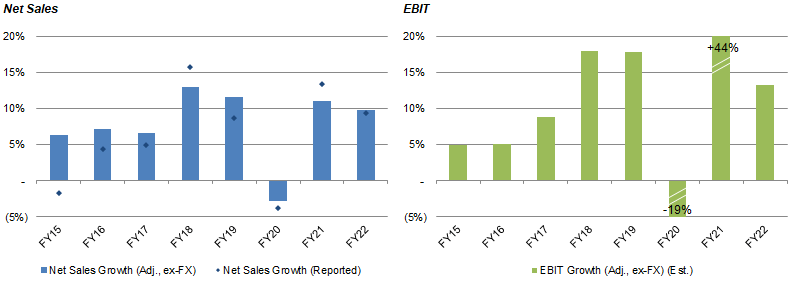

EL achieved much higher growth rates than these in FY18 and FY19, growing sales by more than 10% and EBIT by high-teens each year (excluding currency); growth fell in FY20 due to COVID-19, but more than recovered in FY21:

{kind=link}

Asia/Pacific was key behind the acceleration to double-digit growth from FY18 (excluding FY20). Asia/Pacific Travel Retail, reported as part of the EMEA region, helped accelerate EMEA ex-currency sales growth accelerate to double-digits from FY16, and Asia/Pacific ex-currency sales growth accelerated to double-digits from FY18, before both were interrupted by COVID-19. As of FY22, EL’s largest markets are China (34% of sales), the U.S. (23%) and Korea (11%).

Q2 FY23 results were poor and cast doubts on whether FY22 results were achieved with some sales pulled forward.

Estée Lauder Q2 FY23 Results Headlines

In Q2 FY23, EL Net Sales fell 11% year-on-year organically; the termination of DKNY and other fragrances licenses in June 2022 added 1 ppt to the decline, and currency headwinds added another 5 ppt, so Net Sales fell 17% as reported:

| EL Non-GAAP P&L (Q 2 FY23 vs. Prior Year) Source: EL results release (Q2 FY23). |

Gross Profit fell more than Net Sales and Gross Margin fell 432 bps year-on-year, as price increases were more than offset by inflation in EL’s supply chain, negative region and category mix shift, and higher promotional costs.

Non-GAAP EBIT fell more than Gross Profit and Non-GAAP EBIT Margin fell 928 bps, “primarily” due to lower sales.

Non-GAAP Net Income fell 49.5% and Non-GAAP EPS fell 48.8%, the latter helped by a 1.5% reduction in the number of shares after buybacks. Excluding currency, Non-GAAP EPS fell by 44% year-on-year.

Estée Lauder Q2 FY23 Results Headlines

EL has been being impacted by a variety of problems, some of which appear to be of its own making:

| EL Net Sales by Region (Q 2 FY23 vs. Prior Year) Source: EL results release (Q2 FY23). |

Americas Net Sales fell 3% organically year-on-year in Q2 FY23. U.S. Net Sales fell “single-digit organically”, while LATAM Net Sales “rose double digits”. CFO Tracey Travis attributed poor sales in the U.S. to “lower shipments of replenishment orders due to both retailer inventory tightening as we anticipated, and a later improvement in retail trends post-Christmas”, while CEO Fabrizio Freda acknowledged that EL did “continue to lose share in the quarter”, but stated that growth was improving each month.

EMEA , where nearly all of EL’s Travel Retail sales are reported (except Dr. Jart+ in Korea), saw Net Sales fell 17% organically. This was primarily due to COVID disruptions in China, which meant Global Travel Retail Net Sales “decreased double digits”. In other EMEA markets, France, Spain and Italy all “grew”, the U.K. grew mid-single-digits, and “most” Emerging Markets countries in the region grew double-digits.

Asia/Pacific Net Sales fell 7% organically, also primarily due to COVID disruptions in China, which meant Domestic China Net Sales fell by a single digit and Dr. Jart+ Travel Retail in Korea also declined. “Most” other brands in South Korea grew “double-digits”, though not enough to offset the decline at Dr. Jart+, while most other Asia-Pacific countries had “strong” growth, with Japan, Australia, Malaysia and the Philippines highlighted.

At least some of EL’s problems in Q2 FY23 were likely to be of its own making, especially in North America, where EL is still losing share and had elevated inventory levels when exiting FY22. In China, as we described in our Q4 FY22 results review, EL had a weaker distribution infrastructure that depended on locations in a single city (Shanghai).

EL’s Q2 FY23 results were also significantly worse than L’Oréal’s ( OTCPK:LRLCY ) for the same quarter, which showed a Like-for-Like sales growth of 8.1% for the group, including +9.4% for North America and +4.9% for North Asia:

| Sales Growth By Region – L’Oréal (Q 4 20 22) Source: L’Oréal results release (Q4 2022). |

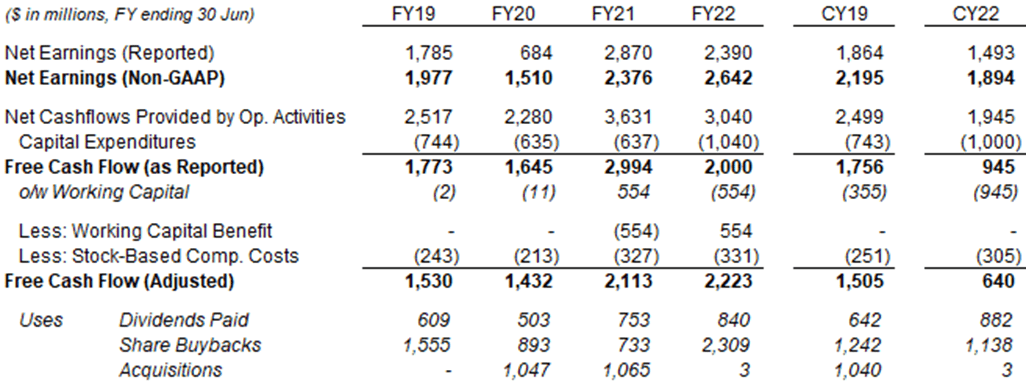

After three weak quarters, EL’s Net Income and Free Cash Flow (“FCF”) were lower in CY22 than in pre-COVID CY19.

Estée Lauder Now Smaller Than in CY19

EL’s Net Sales in U.S. dollars have basically been back at their CY19 levels for the past three quarters:

| EL Net Sales by Quarter ( CY 19-22) Source: EL company filings. |

EL’s Q2 FY23 (October-December 2022) Net Sales of $4.62bn is basically flat in U.S. dollars versus Q2 FY20 (October-December 2019), though up by about 5% excluding currency (but including acquisitions):

| EL Net Sales by Region (Q 2 FY2 3 vs. 3 Years Ago ) Source: EL results releases. |

EMEA sales remained much lower than before COVID-19, largely due to lingering disruption to Travel Retail (for Chinese travellers), while Americas sales were flattish, likely due to a poor Makeup market and competitive pressures. Asia/Pacific sales were much higher, due to structural growth in Domestic China and other countries.

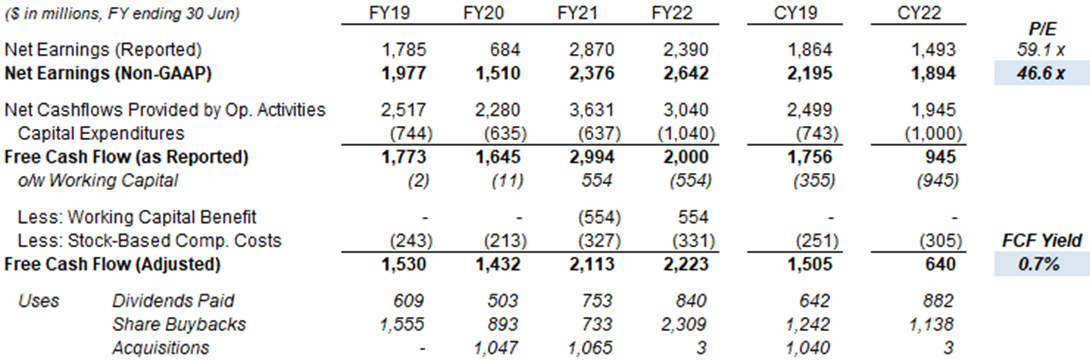

In CY22, EL had Non-GAAP Net Income of $1.89bn and FCF of $640m, both smaller than in CY19:

{kind=link}

EL appears to be suffering from some execution issues, and these are also reflected in its weak near-term outlook.

EL’s Weak Near-Term Outlook

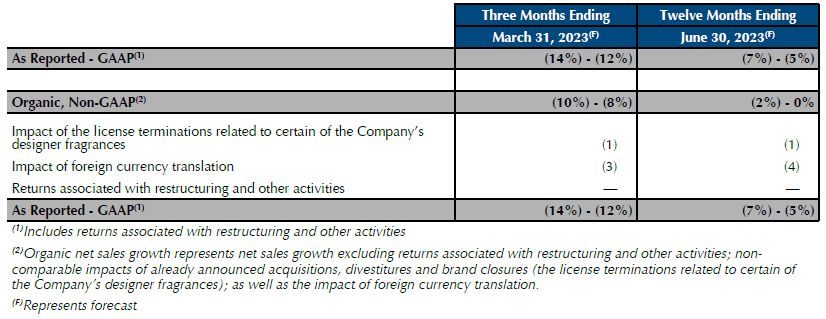

Management expects further declines in Q3 FY23 and a weak FY23 overall.

For Q3 FY23, Net Sales is expected to decline by 10-8% organically and by 14-12% in U.S. dollars; for full-year FY23, Net Sales is expected to be down 2% to flat organically, and to decline by 7-5% in U.S. dollars:

{kind=link}

China Travel Retail (in Hainan) is expected to be remain a headwind in Q3 FY23, as EL’s inventory level there “remains somewhat more elevated” at the end of Q2. Korea Travel Retail (Dr. Jart+) is expected to face a new headwind, the roll-back of COVID-related supportive measures for Duty Free. Together these are expected to more than offset the benefit of the reopening in China and Chinese travellers returning to international travel.

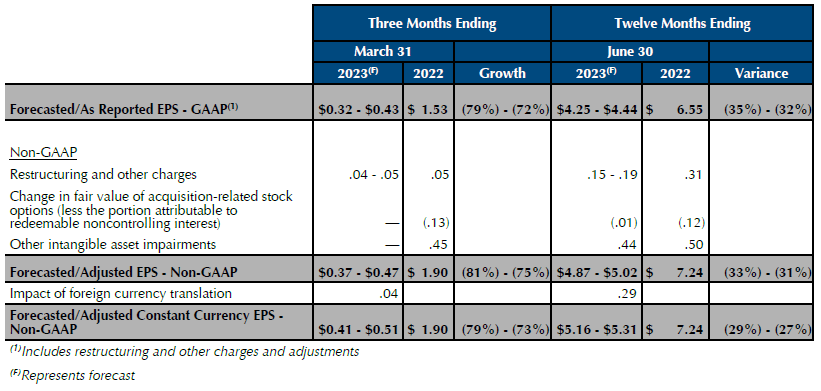

For Q3 FY23, Non-GAAP EPS is expected to decline by 81-75% excluding currency, as management intends to maintain Advertising & Promotions and other spend despite the revenue decline; full-year FY23 Non-GAAP EPS is expected to decline by 29-27% in U.S. dollars to $5.16-5.31, lower than pre-COVID FY19’s $5.34:

{kind=link}

The new FY23 Non-GAAP EPS outlook also represents an approximately 10% reduction from the one given at Q1 FY23 results ($5.69-5.84), despite a smaller currency headwind ($0.29 vs. $0.44).

The pending $2.8bn acquisition of Tom Ford Beauty is not included in the outlook. It is expected to be completed in Q4 and to result in “a slight EPS dilution” to FY23 EPS. (The original announcement referred to a $0.05-0.15 dilution.)

Management Hinting at FY24 Recovery

Management now expects growth to resume in Q4 (compared to Q3 before), and hints at a strong FY24. CFO Tracey Travis said on the earnings call :

“Given that in the fourth quarter, all markets are anticipated to be open and remain open and traveling will gradually resume and again, uncertain about the pace of that resumption, but we've certainly seen encouraging signs in many of our markets. that fiscal '24 will be a strong year for us”

Key drivers for a strong FY24 can include:

- Ongoing post-COVID recovery in China, including both the domestic market and Travel Retail

- Further improvements in EL’s distribution in North America

- Continuing innovations in EL’s product portfolio

Management provided some datapoints to support this expectation on the call. For China, CEO Fabrizio Freda believes EL has expanded its market share in Prestige Beauty during Q2 FY23, with gains in all four product categories; for the U.S., he referred to a sequential increase in growth rates through the quarter:

“The overall market in China was negative double digit (in Q2 FY23). Our net sales were and our retail was negative single digits, and we built market share in every single category …

(In the U.S.) every single month, October, November and then December, there was progress in top line sales acceleration. First of all, in retail, the quarter in the U.S. ended at plus 2%, so on the positive. But December was plus 6.5%, 7%. So in line with our goals of acceleration. So we see the U.S. progressing.”

Management indicates that sales growth and operational leverage will generate strong earnings growth in FY24, though with Non-GAAP EBIT margin likely to remain below 20% (compared to 19.7% in FY22 and 17.5% in FY19).

EL will not be providing actual FY24 guidance until FY23 results in August.

We believe structural growth in Prestige Beauty and EL’s strong brands will help management eventually overcome execution issues.

Is Estée Lauder Stock Overvalued?

At $244.64, relative to CY22 financials, EL stock is at a 46.6x Non-GAAP EPS and a 0.7% FCF Yield:

{kind=link}

FY23 Non-GAAP EPS guidance ($4.87-5.02) implies a P/E of 49.5x at mid-point.

Both CY22 and FY23 earnings are likely far below EL’s true potential, owing to COVID disruptions in China. CY22 FCF is also particularly low owing to a large working capital outflow across receivables, inventory and payables.

Relative to pre-COVID CY19 financials, EL stock is at a 40.2x Non-GAAP EPS and an 1.7% FCF Yield.

The Dividend Yield is 1.1%, with a dividend of $0.66 per quarter ($2.64 annualized), after it was raised 10% year-on-year in November 2022.

EL repurchased $257m of its stock in H1 FY23, which annualizes to the equivalent of 0.6% of its market capitalization.

Estée Lauder Stock Forecast

We reduce our FY23 EPS forecast in line with the new outlook, but continue to assume that Net Income will match to FY22 level in FY24. Our key assumptions now include:

- FY23 EPS of $4.95 (was $5.33)

- FY24 Net Income of $2.642bn (unchanged)

- From FY25, Net Income growth of 11.0% (unchanged)

- Share count to fall by 1.0% each year (unchanged)

- FY23 Dividend of $2.64 (unchanged)

- From FY24, dividend to rise by 8% annually (unchanged)

- P/E to be at 35.0x at FY26 year-end (unchanged)

Our new FY65 EPS estimate is unchanged at $9.29:

| Illustrative EL Return Forecasts Source: Librarian Capital estimates. |

With shares at $244.64, we expect an exit price of $325 and a total return of 37% (10.2% annualized) by June 2026.

Is Estée Lauder Stock A Buy? Conclusion

We reiterate our Buy rating on Estée Lauder stock.

For further details see:

Estée Lauder: Down 11% In A Month Since Q2 FY23 Results