LRLCF - Estee Lauder: Recovery Is Expected But High Growth Is Not

2023-09-18 09:40:57 ET

Summary

- Estee Lauder's top-line growth has been higher than its closest competitor, L'Oréal, while potentially displaying a significant competitive advantage over its peers.

- Short-term headwinds, including the pandemic and crackdown on "Daigou" reselling, are unlikely to permanently impact the company's fundamentals.

- The stock price is currently at fair value, and investors should wait for a higher margin of safety before investing.

Investment Thesis

Estee Lauder ( EL ) runs a highly successful global cosmetic business together with its closest competitor, L'Oréal ( LRLCF ). While both companies are great investment choices for high-end cosmetic businesses, in my opinion, EL is a better investment from a long-term perspective.

The company's business was hit by a list of pandemic-related short-term headwinds that are unlikely to permanently impact the company's fundamentals in the long run.

EL is also affected by the Chinese government's efforts to clamp down on the widespread practice of "Daigou", which is essentially a reselling practice where EL goods are purchased cheaper from the duty-free market only to be resold at a higher price to consumers in China. These clampdown activities might affect the revenue of EL in the short-term but in the long term, I believe EL's margins will improve since consumers are forced to pay for the full retail price in the long run.

Historically, the company does have a track record of growing its revenue which trickles down to its free cash flow ("FCF") consistently in the long run. However, its growth is consistently low.

The stock price is now at fair value. Investors should hold and wait for a higher margin of safety to present itself before investing in EL.

Overview Of The Company

Estee Lauder, a leading global beauty manufacturer with over $17.7 billion in revenue in 2022, is considered one of the largest cosmetics companies worldwide, together with L'Oréal. The company’s product portfolio includes skincare, makeup, fragrance, and hair care products.

The company gets a significant amount of sales from the Retail Travel segment. According to BeautyMatter :

Of Lauder’s $16.2 billion revenue in fiscal 2021 (ending last June), the channel accounted for just under 30%, making it bigger than the entire Americas business.

Competitors

L’Oréal, the world’s largest cosmetics company, can be considered its closest competitor. L’Oréal has developed activities in various beauty sectors such as hair color, skincare, sun protection, make-up, perfume, and hair care. The company's portfolio of beauty products includes Maybelline, Garnier, NYX Professional Makeup, Redken, and CeraVe.

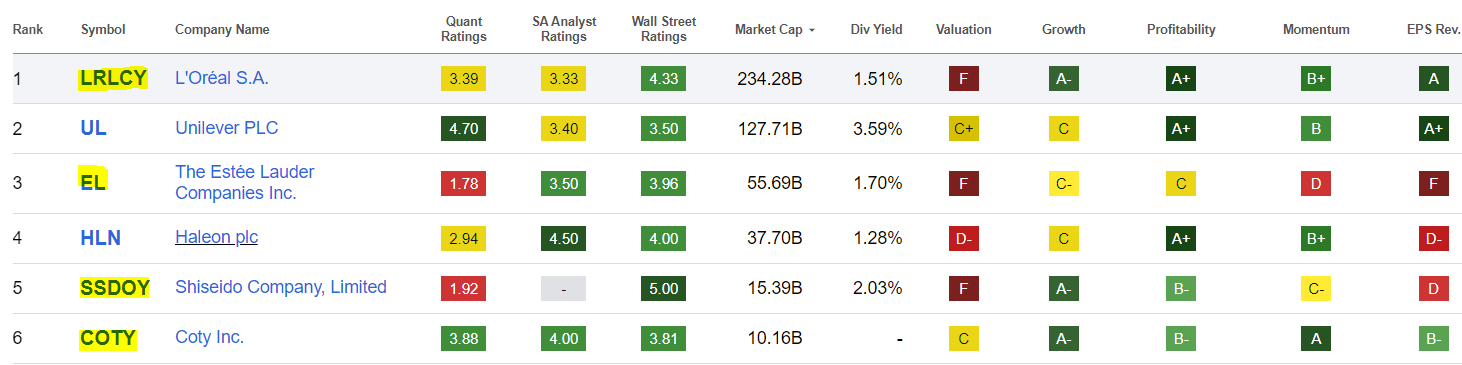

Based on the list of " Top-Personal-Products-Stocks " published by Seeking Alpha, we can observe that EL and LRLCF are ranked near the top of the list when sorted by Market Capitalization:

{kind=link}

In my opinion, Unilever ( UL ) and Haleon ( HLN ) are not direct competitors of EL. While both are in the same market category of "Personal Products", they are not widely known to be selling "high-end", or "luxurious" make-up brands, which I considered EL to be competing in.

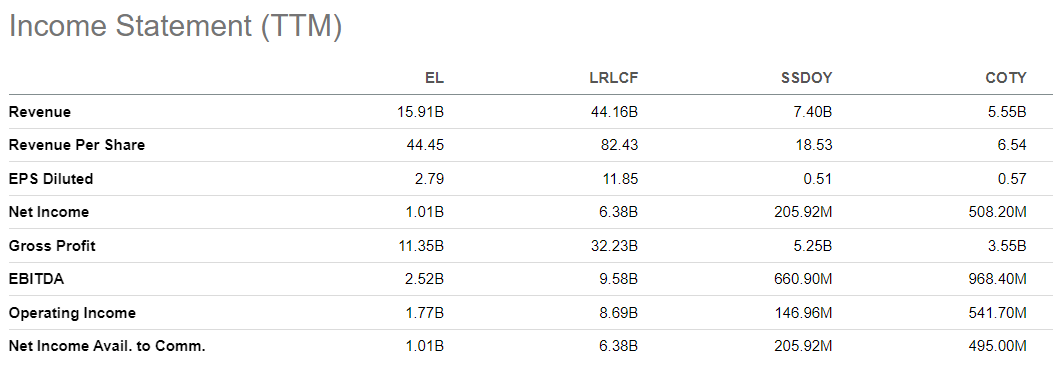

From the financials , it is easy to see EL and LRLCF having a clear lead over other competitors in both the top and bottom lines. Most of the financial figures shown for these 2 companies are in the "billions" while its smaller companies are in the "millions".

{kind=link}

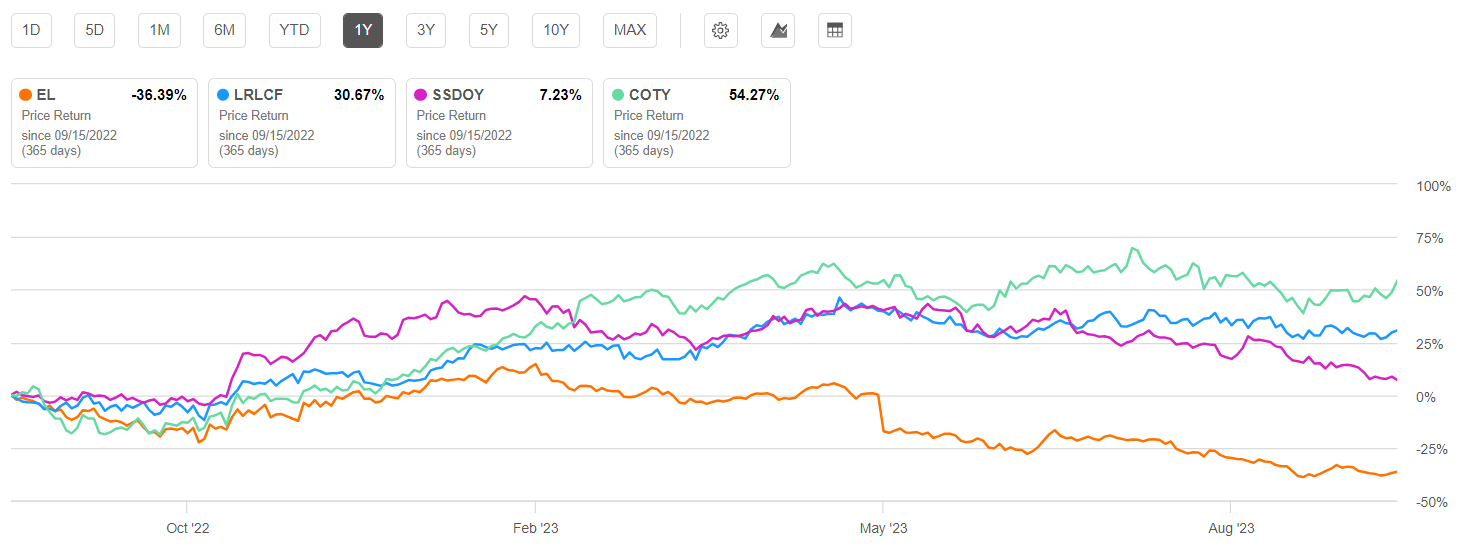

In terms of price performance, EL clearly underperforms its competitors (even the smaller ones) in the short term of the last 1 year. In this time frame, LRLCF might have performed better than EL, but it is mostly on par with its other smaller competitors.

{kind=link}

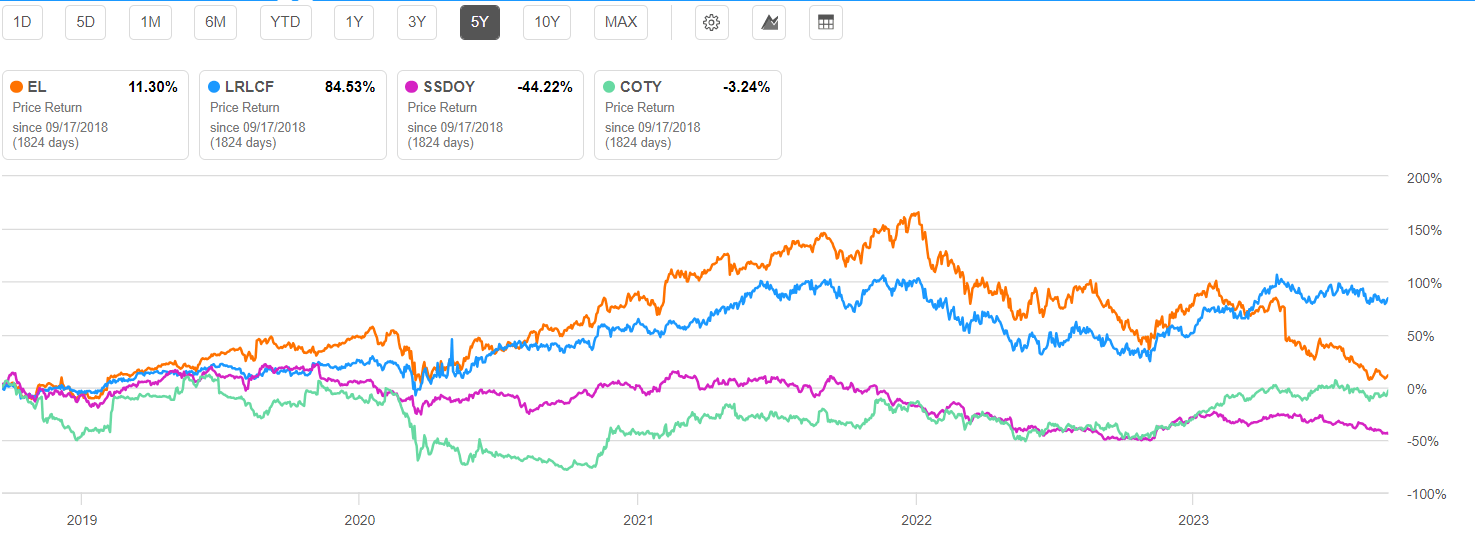

But if we look at the medium-term time frame of 5 years, EL and LRLCF both consistently outperform their competitors towards the end of 2019. EL outperformed LRLCF in most years except since the start of this year (2023).

{kind=link}

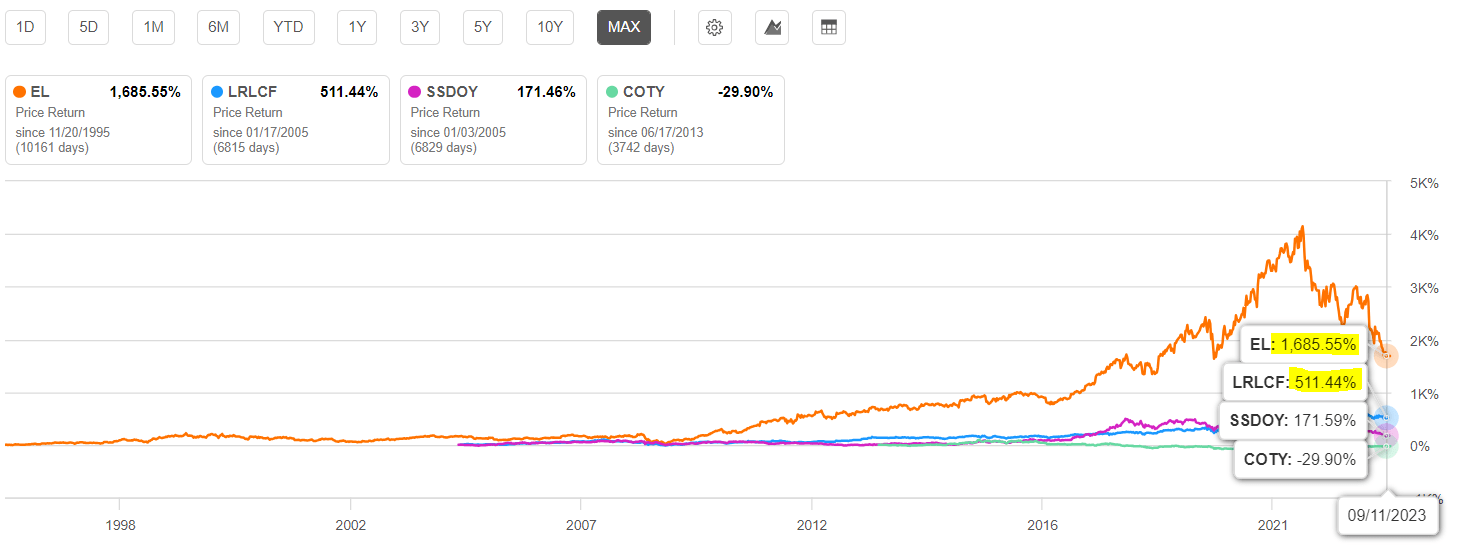

Now, if we look at the very long-term time frame of more than 20 years, EL clearly outperformed all its competitors by a wide margin since 1996.

{kind=link}

The key takeaway from this analysis is that for long term investors who are looking for high-end cosmetic businesses to invest in, both EL and LRLCF are clear choices, depending on the time frame of the investment. However, for EL, investors should be prepared to hold the investment for a very long time to see significant returns on these investments.

Short-Term Issues (Pandemic-induced woes )

Travel restrictions have a negative impact on Estee Lauder's travel retail sector. The easing of COVID-19 restrictions around the world had raised expectations for a rebound in travel retail, but the slow recovery of Asia's travel retail, particularly in China, has led to a larger forecasted decline in full-year sales and profit for Estee Lauder. This is a stark contrast to European peers LVMH and L'Oreal which saw a rise in first-quarter sales

Shipping Products to fulfill online orders had also been a challenge for EL. The weeks-long shutdowns in China prevented the company from shipping its products to the country.

Retailers and other brick-and-mortar stores are forced to practice strict inventory management to reduce wastage as a result of drastically reduced sales.

In my opinion, these are short-term setbacks for EL. According to McKinsey , the Chinese governing is already removing travel restrictions rapidly:

While the sudden opening may lead to uncertainty and hesitancy to travel in the short term, Chinese tourists still express a strong desire to travel. And the recent removal of quarantine requirements in January 2023 could usher in a renewed demand for trips abroad.

As one of the top brands in the cosmetics industry, recovery from these headwinds should be probable although it might still take longer for the recovery to be reflected on the company's financial bottom line.

Short-Term Issues (Crackdown on "Daigou")

One of EL's short-term issues is its sales in China. According to this article , this has been a concern observed by Goldman Sachs since July this year:

“Results from China Tourism Group Duty Free and takeaways from an expert call held by one of our colleagues both suggest that beauty sales in Hainan are falling short of our prior expectations,” Goldman Sachs analysts led by Jason English wrote in a note. “The weakness is being attributed to tighter restrictions on Daigou resellers by the government.”

According to the Cambridge online dictionary, this is the definition of " Daigou ":

someone who is outside China who buys goods for someone who lives in China:

For many years, Chinese consumers have benefitted from buying luxury goods from Daigou sellers at a price lower than the original retail price. During the pandemic , these re-sellers flocked to Hainan’s duty-free shops to buy luxury items in bulk at a much lower price when they were barred from international travel shopping. In recent years, a crackdown on these reselling activities has negatively hurt global luxury sales, including EL.

According to Retail in Asia , the crackdown on Daigou started on 28 September 2018 and stirred up uncertainty in the global luxury industry. The launch of China's new e-commerce law and the "928 Daigou crackdown" have raised concerns about a slowdown in Chinese spending.

In the short term, the sales volume for luxury companies like EL will dip due to the loss of these Daigou buyers. But in the long run, as consumers are used to buying products from legal channels at the original higher prices, EL's bottom-line margins are expected to improve. The established brand of EL should also allow the company to effectively assert its pricing power to further improve its long-term profits.

Projection Of Recovery

During the latest earnings call , management projected recovery to happen "beyond fiscal 2024":

beyond fiscal 2024, we expect to recapture lost operating margin at an accelerated pace by delivering annual margin expansion that is faster than our pre-pandemic historical average. This acceleration is expected to become more evident after the first quarter of fiscal 2024.

In my opinion, as an established global brand, the recovery and growth of EL are assured , but it is unclear whether the company is able to deliver a growth rate that is as optimistic as what the management has described (faster than the pre-pandemic historical average).

Financials

Let's look at some key financial figures extracted from Seeking Alpha .

{kind=link}

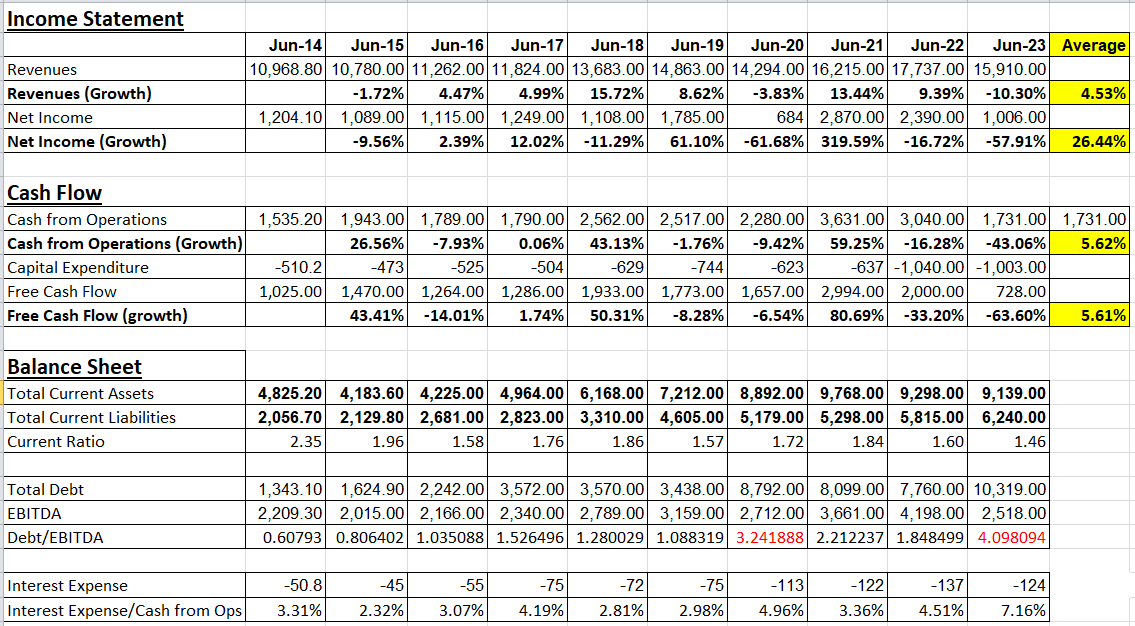

While EL's top line has been growing for most years since 2014, the growth appears to be modest at just about 5% on average. This revenue growth trickled down to its cash-related growth rates. The FCF of the company can be observed to grow at an average rate of 5.61% . We will use this growth rate when valuing the company.

The bottom line net income appears much higher, above 26%. In my opinion, this is due to the unusual dip and recovery between 2020 and 2021, recording a growth of almost 320%. If we exclude the unusual growth between 2020 and 2021, the average growth in the bottom line is almost 0.

EL has always maintained an asset level significantly higher than its liabilities since 2014, which is good for the company's long-term growth.

However, its debt profile does not look so rosy. EL's debt has been rising in recent years. Currently, the total debt is 4 times its EBITDA. In my opinion, a debt/EBITDA ratio of more than 3 is considered unhealthy.

Fortunately, EL is still able to comfortably service its debt. The interest expense of the company is just 7.16%. In my opinion, an interest expense that is less than 30% of cash flow from operations is considered healthy.

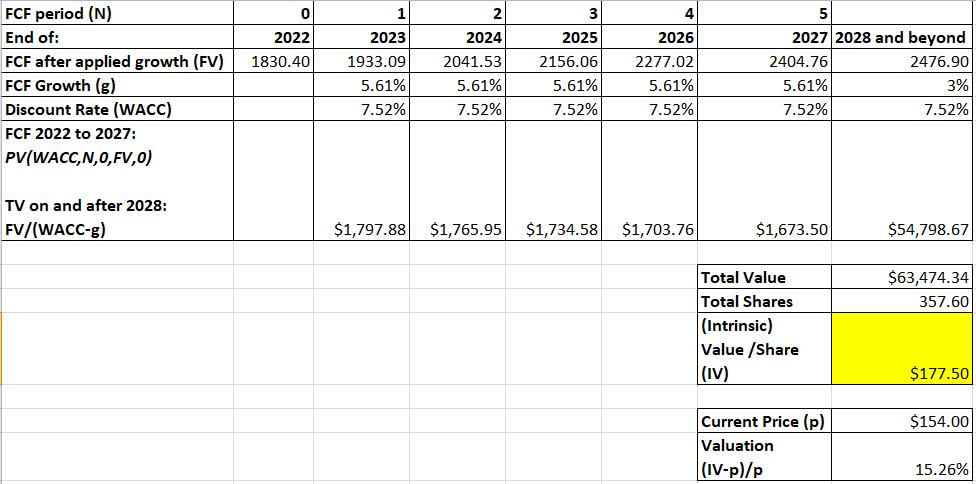

Valuation (Base Case)

We will make the following assumptions/inputs into the calculation of EL's intrinsic value using the DCF model:

We will use the average FCF from 2019 to 2023 (the last 5 years) to represent the starting FCF from 2022. This will smoothen out the irregularities due to the pandemic.

Free Cash Flow (Seeking Alpha)

{kind=link}

We will assume the average growth since 2014 of 5.61% in FCF will be maintained from 2023 to 2027 before the growth matures and tapers off to 3% from 2028 and beyond.

From GuruFocus, the company's WACC ranges from 5.86 to 10.73% over the last 5 years. We will use an average of 7.52% in our calculation

{kind=link}

We assumed the company's " shares outstanding " would stay the same at 357.6M indefinitely.

{kind=link}

Using the above-assumed figures, the intrinsic value is $177.5 .

Assuming a current market price of $154, the stock is 15.26% undervalued .

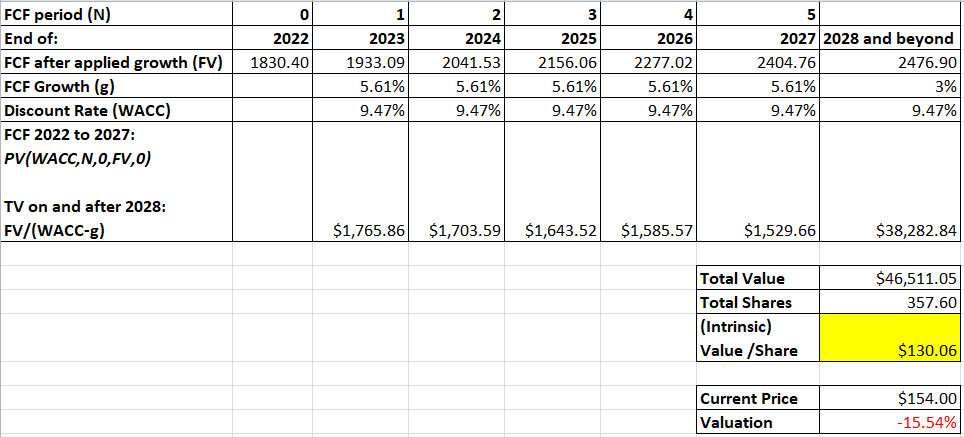

Valuation (Worst case)

In our base case valuation, we have used a WACC that is the average of the last 5 years. We will use the highest WACC of 9.47% to calculate the intrinsic value for the worst-case scenario.

{kind=link}

Using the above-assumed figures, the intrinsic value is $130.06 .

Assuming a current market price of $154, the stock is 15.54% overvalued .

Overall, at the current price, there is almost as much upside compared to the downside:

- 15.26% undervalued based on the base-case scenario

- 15.54% overvalued based on the worst-case scenario

Hence, investors should consider the stock price at the current value to be just fairly valued.

Investment Risk

In my opinion, EL runs a successful business in the cosmetic industry that is unlikely to be fundamentally affected by the recent short-term headwinds in the long run.

Still, the company's long-term growth in FCF is low and the business in the cosmetic industry is discretionary in nature. This means if a global recession occurs due to the previous rate hikes, EL will be impacted more than companies in other industries.

Conclusion

Overall, EL is a leading global cosmetics company with a good track record of growth, albeit at a significantly slow rate. The company's business was temporarily disrupted by the pandemic, but its fundamentals remain strong.

The company is also facing headwinds from the Chinese government's crackdown on 'daigou', but this is likely to be a short-term headwind. In the long run, EL's margins should improve as consumers are forced to pay the full retail price for its products.

The stock price is now at fair value. For a company like EL which is generally large and successful but not expected to grow at a high rate based on pre-pandemic historical trends, investors should hold and wait for a higher margin of safety before investing in the stock.

For further details see:

Estee Lauder: Recovery Is Expected But High Growth Is Not