ETD - Ethan Allen Interiors: Impressive Resilience

2023-11-29 23:27:19 ET

Summary

- Ethan Allen has faced challenges due to flooding in its manufacturing plant and a challenging demand in the furnishing industry.

- The company's long-term financial history shows poor growth, but margins have risen to a new level after the pandemic.

- ETD has a strong balance sheet to carry the company through the headwinds on top of the relatively strong earnings performance.

- The stock seems to be priced for very little, making the current risk-to-reward favorable, in my opinion.

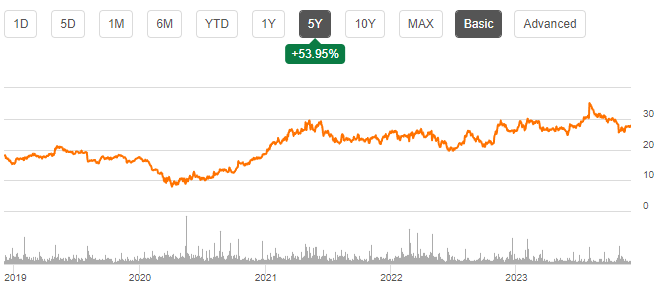

Ethan Allen Interiors ( ETD ) manufactures and sells furnishing and interior design products, with recent initiatives to improve the interior design offering and marketing through a network of design centers. The company has faced significant headwinds due to flooding in Ethan Allen's Vermont manufacturing plant, as well as an industry that's facing tough quarters due to macroeconomic pressure. The stock seems to be priced very conservatively, seemingly pricing in further struggles. Despite the challenges and a currently cheap stock, Ethan Allen's stock has performed well in the past few years - the stock has appreciated by 54% in five years, on top of which Ethan Allen pays out a great dividend with a current yield of 5.27% .

{kind=link}

Long-Term Financial History

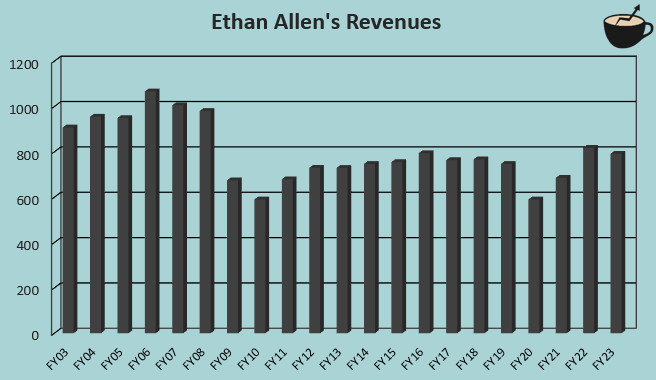

Ethan Allen's long-term financial history doesn't seem too appealing - the company's revenues decreased significantly during the great financial crisis, but haven't recovered well, making the company's growth from FY2003 to FY2023 negative. After the crisis from FY2011 to FY2023, the revenue CAGR is slightly better at 1.3%. The figure isn't very impressive, but does seem to suggest that Ethan Allen's revenue level has mostly achieved stability in real terms over a longer time period.

{kind=link}

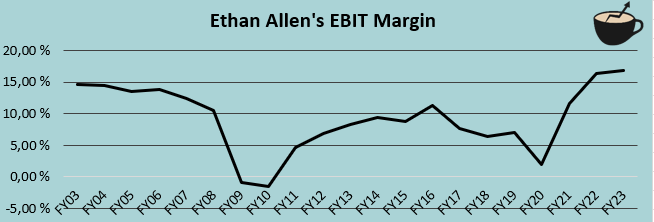

The long-term horizon doesn't seem too good for margins, either. Ethan Allen's EBIT margin has fluctuated largely, with the margin level having decreased widely after FY2008. On a more recent basis, Ethan Allen seems to have achieved a better level after the Covid pandemic - in FY2023, the EBIT margin was 16.9% compared to a FY2019 level of 7.0%. I would expect the achieved margin level to mostly be sustainable - Ethan Allen has been able to cut SG&A by $22 million between the years despite high inflation, while simultaneously pushing for higher gross margins.

{kind=link}

An Industry & Company with Current Headwinds

The furnishing industry is facing significant challenges due to macroeconomic pressure, as well as a slowdown in need for furnishing after the pandemic. Ethan Allen saw a revenue decrease of 23.6% in Q1/FY2024, with competitors seeing similar figures. For example, La-Z-Boy's revenues declined by 20.3% in the most recent quarter, Bassett's (which I recently wrote an article on) by 26.1% , and Hooker Furnishings' by 36.0% . The sales should eventually recover as the economy improves, but the industry should still see tough upcoming quarters with a very uncertain economy.

On top of a struggling industry, Ethan Allen's manufacturing plant in Vermont was disturbed during the most recent quarter in Q1/FY2024 - the plant faced flooding in July, disrupting manufacturing and damaging a part of the company's inventory and machinery, creating costs for the company. In addition, as manufacturing was paused, some of Ethan Allen's shipments had to be cancelled. The lost revenues are estimated at a size of $15 million in Q1; without the flooding, Ethan Allen's revenues would have decreased by an estimated 16.6%. In September, the manufacturing plant resumed operations.

Impressively for Ethan Allen, the company has still been able to keep a good margin level despite the lower revenue level - in Q1/FY2024, Ethan Allen managed to have an EBIT margin of 12.1% even with costs related to the flooding. The proven resilience in operating income seems very valuable in my opinion, as the mentioned competitors seem to have had much more difficulties in keeping up good profitability.

Strong Balance Sheet Provides Safety

Ethan Allen has a strong balance sheet . The company doesn't hold any interest-bearing debts intended for financing purposes. In addition, Ethan Allen has a good amount of cash and short-term investments, with a current cash balance of $57 million and $106 million in short-term investments that have been made in recent years. As the industry is going through a rough patch, the relatively strong earnings coupled with a very strong balance sheet make Ethan Allen a lower risk pick in the furnishing industry than most competitors.

Valuation - Not Much is Priced In

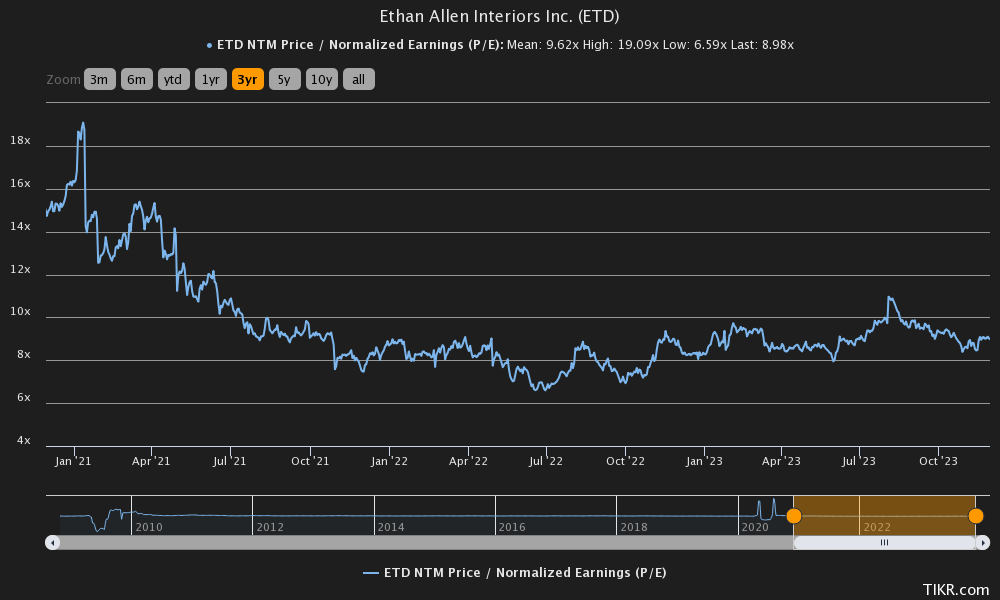

The stock currently trades at a low forward P/E of 9.0, a bit below Ethan Allen's three-year average of 9.6:

{kind=link}

The low P/E ratio coupled with a strong balance sheet and a relatively strong recent performance seems like a good buying opportunity. Still, the low valuation could be explained by Ethan Allen's mediocre long-term growth - to contextualize the valuation better, I constructed a discounted cash flow model in my usual manner.

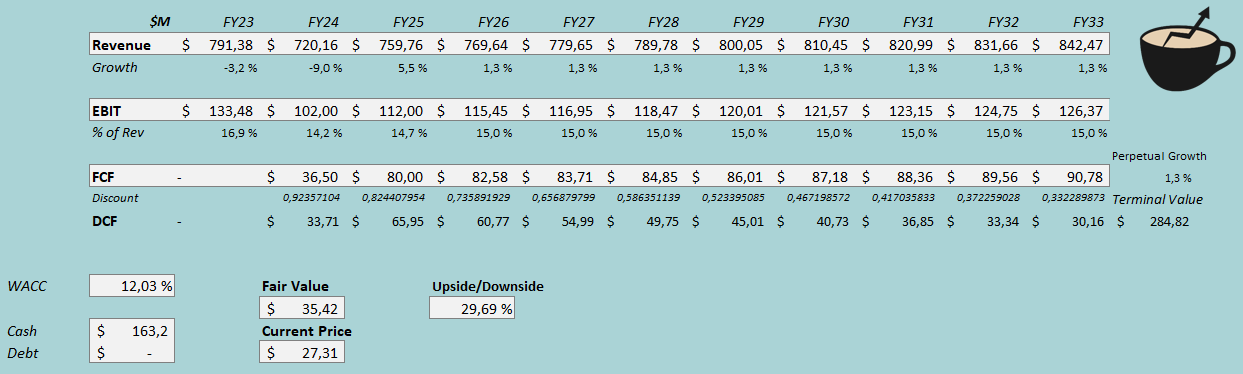

In the model, I estimate revenues to decrease by 9% in FY2024, estimating low declines in the three upcoming quarters due to the challenging demand environment. After the year in FY2025, I estimate a revenue rebound through demand recovery with a revenue growth of 5.5%. After the year, I estimate revenues to grow at the FY2011-FY2023 average rate of 1.3%, representing a reasonably mediocre future growth. For margins, I believe that Ethan Allen could recover slightly from the FY2024 estimate of 14.2%. As revenue levels normalize and Ethan Allen doesn't have costs related to the flooding in coming years, I believe that slight operating leverage is likely - I estimate an EBIT margin of 15.0% in FY2026 and forward. As the company doesn't seem to be geared for growth, I don't see increasing capex or working capital needs, making the cash flow conversion quite good.

With the mentioned estimates and a cost of capital of 12.03%, the DCF model estimates Ethan Allen's fair value at $35.42, around 30% above the stock price at the time of writing - the stock doesn't seem to be priced for much. As the upside is quite significant, Ethan Allen's risk-to-reward seems great in my opinion.

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

As has been told, Ethan Allen doesn't currently leverage debt in financing. I wouldn't expect this to change as the industry is struggling, and Ethan Allen seems to play the balance sheet safely - in the CAPM, I estimate a long-term debt-to-equity ratio of 0%, not counting debt as a form of financing. For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 4.30% . The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Ethan Allen's beta at a figure of 1.24 . Finally, I add a small liquidity premium, crafting a cost of equity and WACC of 12.03%.

A Note on Risks

The DCF model's estimated upside could deteriorate, if Ethan Allen doesn't sustain the achieved margin level - prior to the pandemic, the company achieved EBIT margins below 10% against my DCF model's estimate of a sustainable 15% EBIT margin - a fallback to single-digit margins would deteriorate the DCF model's fair value. For example, with a 10% EBIT margin from FY2025 forward, the stock would already have an estimated downside of 6% instead of the upside. I believe that the higher margin level is a good baseline scenario estimate, though, as the cost cuts and higher pricing seem to have stuck around even in a challenging sales environment.

On another note, the bullish thesis doesn't rely very much on Ethan Allen's short-term financial performance. The company could still have very challenging upcoming quarters that could very well be worse than my DCF model has as estimates for FY2024. Although I don't believe that such a scenario deteriorates the long-term thesis, the stock price could fall significantly in the short term as a result. Because of Ethan Allen's strong balance sheet, though, temporarily very bad cash flows and earnings are very unlikely to be detrimental to the company in the long run.

Takeaway

Ethan Allen's is facing significant issues with the flooding in Q1/FY2024 and a challenging sales environment. Still, the company has been able to keep up a relatively good earnings level, and the strong balance sheet provides more safety to the investment. Although Ethan Allen's long-term revenue history has been mediocre at best, the stock's risk-to-reward seems good - my DCF model estimates upside even with mediocre future growth. For the time being, I have a buy rating on the stock - the past years' stock performance seems to have room to continue.

For further details see:

Ethan Allen Interiors: Impressive Resilience