LOVE - Ethan Allen Interiors: Q3 2023 Earnings Preview

2023-04-17 12:52:23 ET

Summary

- The management team at Ethan Allen Interiors is expected to announce financial results for the third quarter of the company's 2023 fiscal year.

- Analysts currently expect there to be weakness on both the firm's top and bottom lines and this wouldn't be surprising.

- This is in spite of continued growth in consumer furniture sales.

- Given how cheap shares are, the company does likely offer some upside from here.

Given all that's going on with the economy, I can understand why investors might be cautious to buy stock of certain companies or to buy stock in companies within certain industries. With the housing market certain to experience significant downward pressure in the coming months, one might argue that anything related to housing would be off-limits for prudent investors. This would even extend to things like furniture. Fewer homes should, in theory, translate to less of a demand for consumer furniture. And tightened budgets would likely translate to lower demand for it as well.

Even with this being the case, one company that looks fundamentally appealing at this time is interior design product company Ethan Allen Interiors ( ETD ). For those not familiar with the business, it focuses on the production and sale of home furnishings and accents, casegoods, and similar offerings. Shares have failed to keep up with the broader market over the prior few months, even though financial performance achieved by management remains largely positive. Of course, this picture can change at a moment’s notice, and what more likely time to see such a change than when earnings results are announced. It just so happens that management at the company is expected to announce financial results for the third quarter of the company's 2023 fiscal year later this month. So although I am bullish about the company in general, I would argue that there are some important things that investors should be paying attention to in order to see whether the picture is likely to worsen enough to offset the low pricing of the company's stock.

What to expect

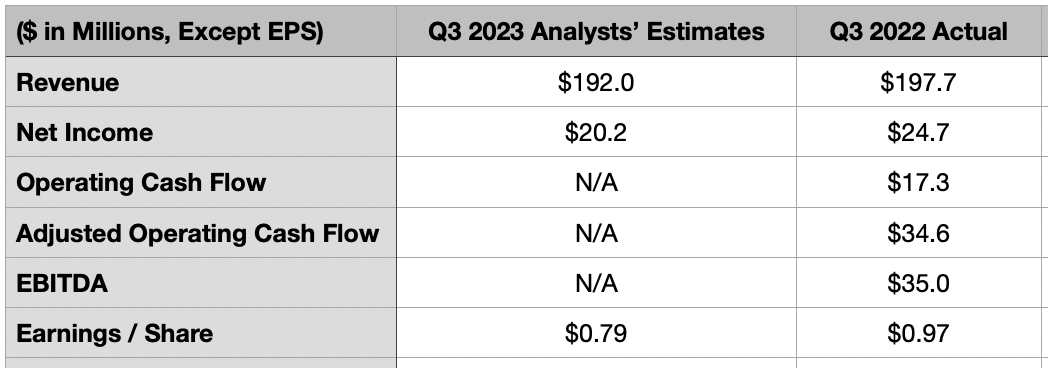

After the market closes on April 26th, the management team at Ethan Allen Interiors is expected to announce financial results covering the third quarter of the company's 2023 fiscal year. The first thing on everybody's mind would be the amount of revenue that management reports. At present, analysts are forecasting sales for that time of $192 million. If this does come to fruition, it would imply a year-over-year decline of 2.9% compared to the $197.7 million that the company reported one year earlier.

{kind=link}

Author - SEC EDGAR Data

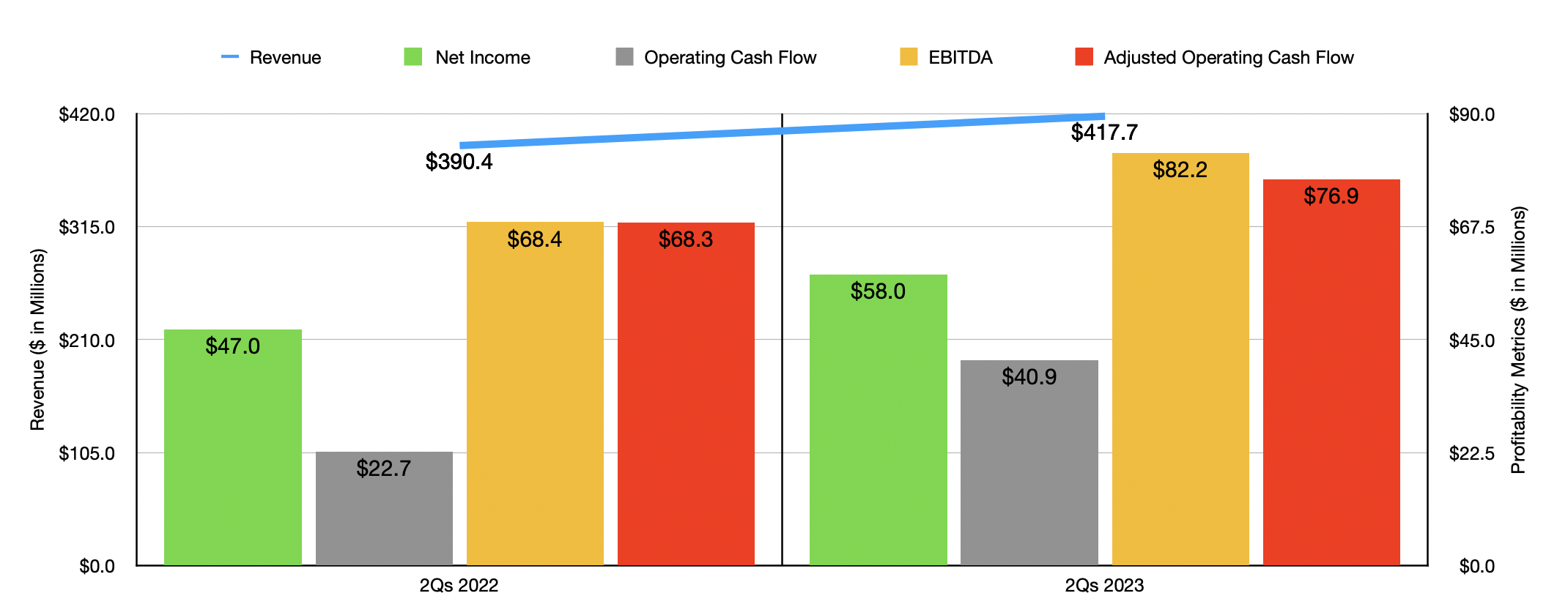

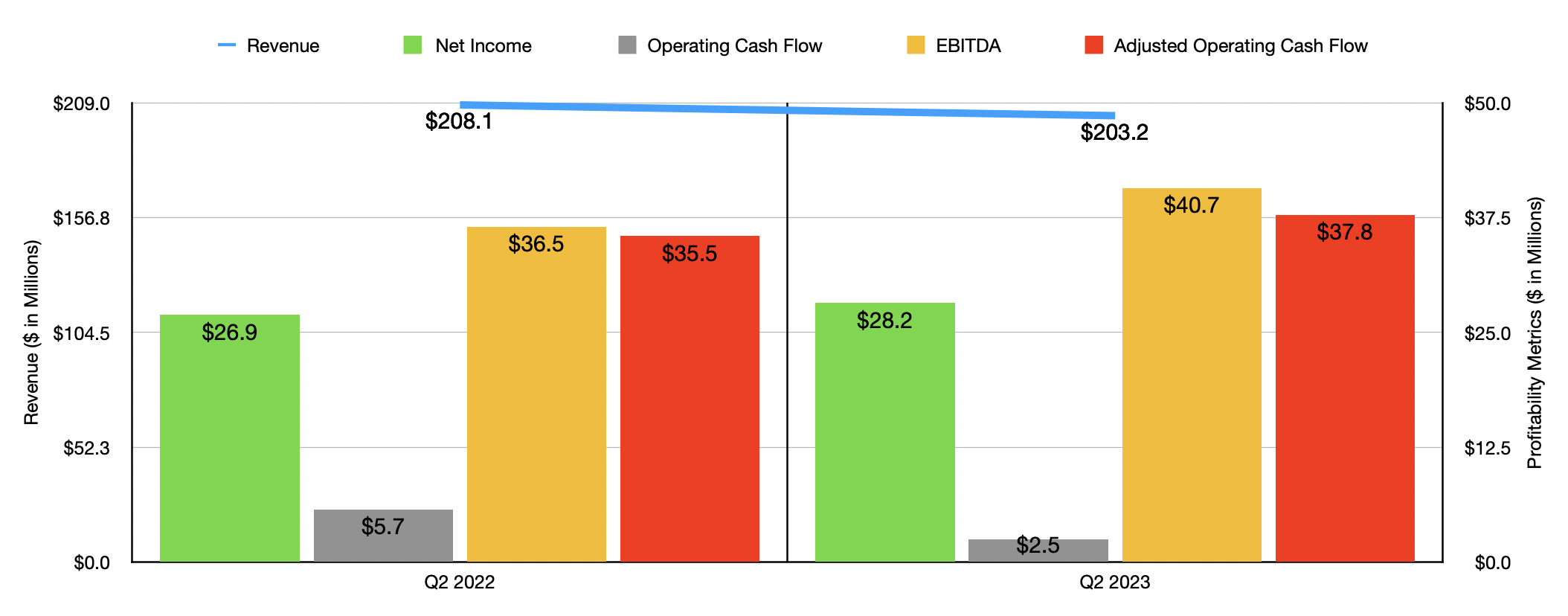

During the first two quarters of 2023 , revenue came in at $417.7 million. This was 7% above the $390.4 million reported the same time the prior year. Because of this, it may seem peculiar to expect revenue to drop. But there is recent precedent of this occurring. In the second quarter alone, sales of $203.2 million translated to a decline of 2.4% compared to the $208.1 million reported in the second quarter of 2022. That drop was driven by weakness across the board, with wholesale net revenue leading the way. Revenue there plunged 8.3%, but really all of this drop could be attributed to internal sales that go to the company's retail operations. Excluding this, revenue would have actually risen by 10.1% for that portion of the business. The weakness on the retail side was driven by economic issues causing consumers to spend less.

{kind=link}

Author - SEC EDGAR Data

On the bottom line, analysts expect weakness as well. This is hardly surprising when you consider the nature of retail. Overall earnings per share should come in at $0.79 if analysts are correct. This would be down from the $0.97 per share reported one year earlier. Based on these numbers, this would imply net income for the company of $20.2 million. To put this in perspective, earnings per share in the third quarter of last year resulted in net profits of $24.7 million. Analysts have not provided guidance when it comes to other profitability metrics. But there are a couple that investors should pay close attention to. One of these is operating cash flow. For context, in the third quarter of last year, this metric was $17.3 million. If we adjust for changes in working capital, we would get a reading substantially higher than that at $34.6 million. And finally, EBITDA totaled $35 million. Given what we know about analysts’ expectations, and assuming that they turn out to be accurate, we should expect these profitability metrics to be lower this year than last.

{kind=link}

Author - SEC EDGAR Data

There is some chance that analysts could be wrong on this front. According to Furniture Today, for instance, consumer spending on furniture this year should be around $126.3 billion. This would be 1.9% higher than the $124 billion reported one year earlier. Furniture store sales should grow slower than this, rising 1% from $72.1 billion to $72.8 billion. It's worth noting that both of these growth rates are lower than what the industry had exhibited over the past couple of years. But with housing weakness and tighter consumer budgets, it wouldn't be a surprise to see a weakening in the form of revenue. Furniture Today pointed out that excess inventory in the space could be a big problem, causing players in the market to lower prices in order to offload their offerings. I don't see this as being particularly likely when it comes to Ethan Allen. The reason why this is relates to the fact that inventory levels during the most recent quarter totaled $159.9 million. That's actually down from the $176.5 million reported at the end of the 2022 fiscal year. And it's below the $164.6 million reported during the second quarter of the 2022 fiscal year. Regardless of the cause, it looks as though management has been successful in reducing its exposure to inventory at bloated costs.

We don't really know what to expect when it comes to the 2023 fiscal year in its entirety. We do know that, for the first half of the year, revenue was higher than it was last year. I already covered this earlier in the article. Profits were also on the rise, jumping from $47 million in the first half of 2022 to $58 million the same time this year. Operating cash flow nearly doubled from $22.7 million to $40.9 million. On an adjusted basis, the increase was more modest from $68.3 million to $76.9 million. Meanwhile, EBITDA for the company grew from $68.4 million to $82.2 million. Even when you look at results covering the second quarter of the year on its own, a quarter that saw financial performance that was weaker than it was in the first quarter of the year, you can see that overall profitability has been robust even at a time when sales have fallen.

{kind=link}

Author - SEC EDGAR Data

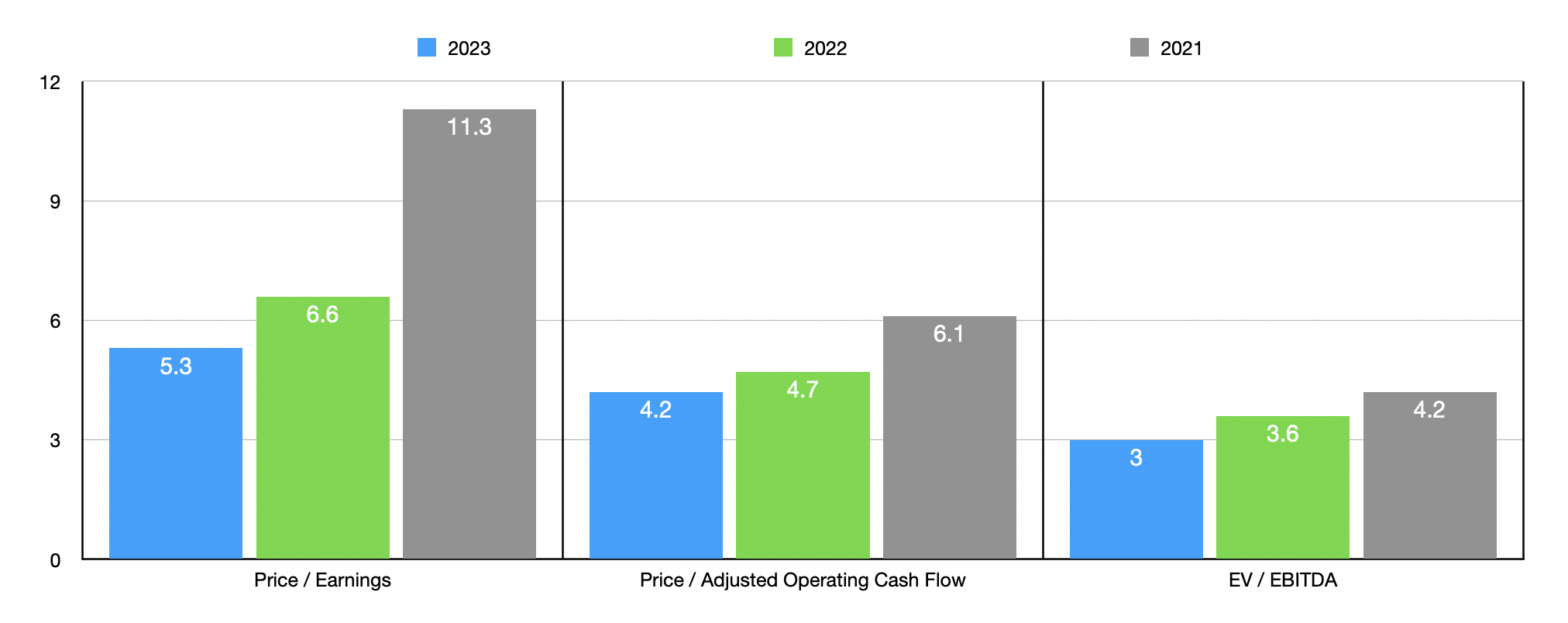

Given this performance, I have a hard time believing that financial results would be worse than they were during 2022. In the chart above, you can see house shares are priced using estimates I provided for 2023. These estimates basically annualize results experienced during the first half of the year. But the chart also shows trading multiples of the company if we assume that financial performance weakens to what it was in 2021 or 2022. To put this all in perspective, I also decided to compare Ethan Allen Interiors to five similar businesses. In the table below, you can see that, using the price-to-earnings approach, the price to operating cash flow approach, and the EV to EBITDA approach, only one of the five firms was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Ethan Allen Interiors |

| 5.3 |

| 4.2 |

| 3.0 |

| The Lovesac Company ( LOVE ) |

| 16.2 |

| 23.0 |

| 7.9 |

| Bassett Furniture Industries ( BSET ) |

| 2.4 |

| 13.1 |

| 1.7 |

| Hooker Furnishings ( HOFT ) |

| 22.6 |

| 10.5 |

| 10.1 |

| Flexsteel Industries ( FLXS ) |

| 13.6 |

| 1.4 |

| 6.2 |

| Tempur Sealy International ( TPX ) |

| 15.0 |

| 18.0 |

| 11.4 |

Takeaway

Furniture may not be the most exciting place to park your money. And during these uncertain times, I can definitely understand why investors might be cautious. Having said that, shares of the company do look incredibly cheap at this moment in time. On top of this, while sales are falling and likely will fall moving forward, it's difficult to imagine a scenario where the bottom falls out and the stock looks overvalued. Given this favorable risk-to-reward scenario, I cannot help but to keep the ‘buy’ rating I assigned the company previously.

For further details see:

Ethan Allen Interiors: Q3 2023 Earnings Preview