ETJ - ETJ: Modest Returns By Design But Yielding 9.1%

2023-03-23 05:03:54 ET

Summary

- The ETJ fund offers exposure to a diversified portfolio of large-cap stocks with an options overlay to reduce downside capture and portfolio volatility.

- The fund generates 40-50% of the market's returns with 50-60% of the volatility. This could be an attractive profile for some risk averse investors.

- The problem with ETJ is that with 4-6% returns on average, the fund is paying a 9%+ distribution. This setup leads to long-term NAV amortization and distribution cuts.

Recently, after I published an article on the Eaton Vance Tax-Managed Buy-Write Income Fund ( ETB ), a reader messaged me and asked for my opinion on one of his long time holdings, the Eaton Vance Risk-Managed Diversified Equity Income Fund ( ETJ ). He liked the 9% yield and conservative nature of the fund but was concerned about a distribution cut in the past few months.

The ETJ fund attempts to give investors a smoother investment experience by reducing portfolio volatility through options. It provides 40-50% of the market's returns with 50-60% of the market's volatility, which may be acceptable for risk-averse investors.

The main problem I see with ETJ is that although the fund's returns are modest by design, it continues to pay a very generous monthly distribution, currently set at an annualized 9.1%. The high distribution rate forces ETJ to liquidate NAV to sustain, which makes future distributions harder to fund. Inevitably, this leads to NAV declines and distribution cuts. I would avoid this fund.

Fund Overview

The Eaton Vance Risk-Managed Diversified Equity Income Fund (“ETJ”) is a closed-end fund ("CEF") that offers exposure to a diversified portfolio of common stocks that is hedged with a protective out of the money ("OTM") put on the S&P 500 Index while generating additional income from writing OTM calls on the S&P 500 Index and individual stocks. The ETJ fund seeks to provide less volatile returns and reduced exposure to significant losses during stock market declines.

The ETJ fund has $540 million in net assets and charges a 1.12% net expense ratio in 2022.

Portfolio Holdings Mimic The S&P 500

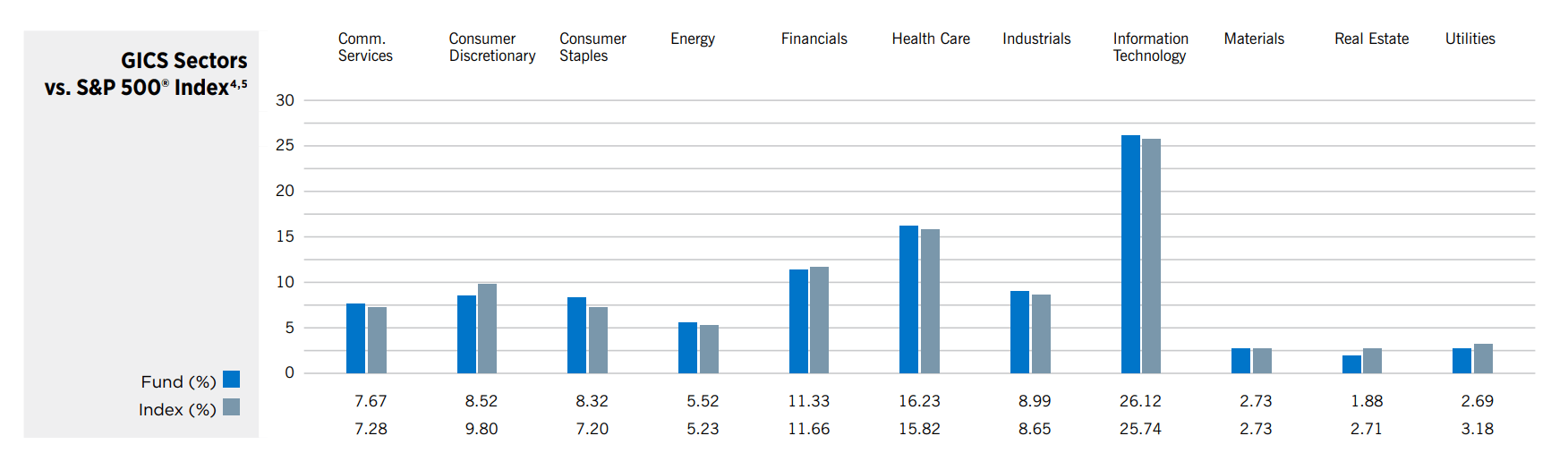

Figure 1 shows the fund's sector allocation as of December 31, 2022. In general, the ETJ fund's sector allocations are very similar to the S&P 500 Index.

Figure 1 - ETJ sector allocation is similar to S&P 500 (ETJ factsheet)

{kind=link}

In fact, the ETJ fund may hold largely the same stocks as the S&P 500 Index, with a maximum overlap of 70% to avoid tax considerations.

Modest Returns By Design

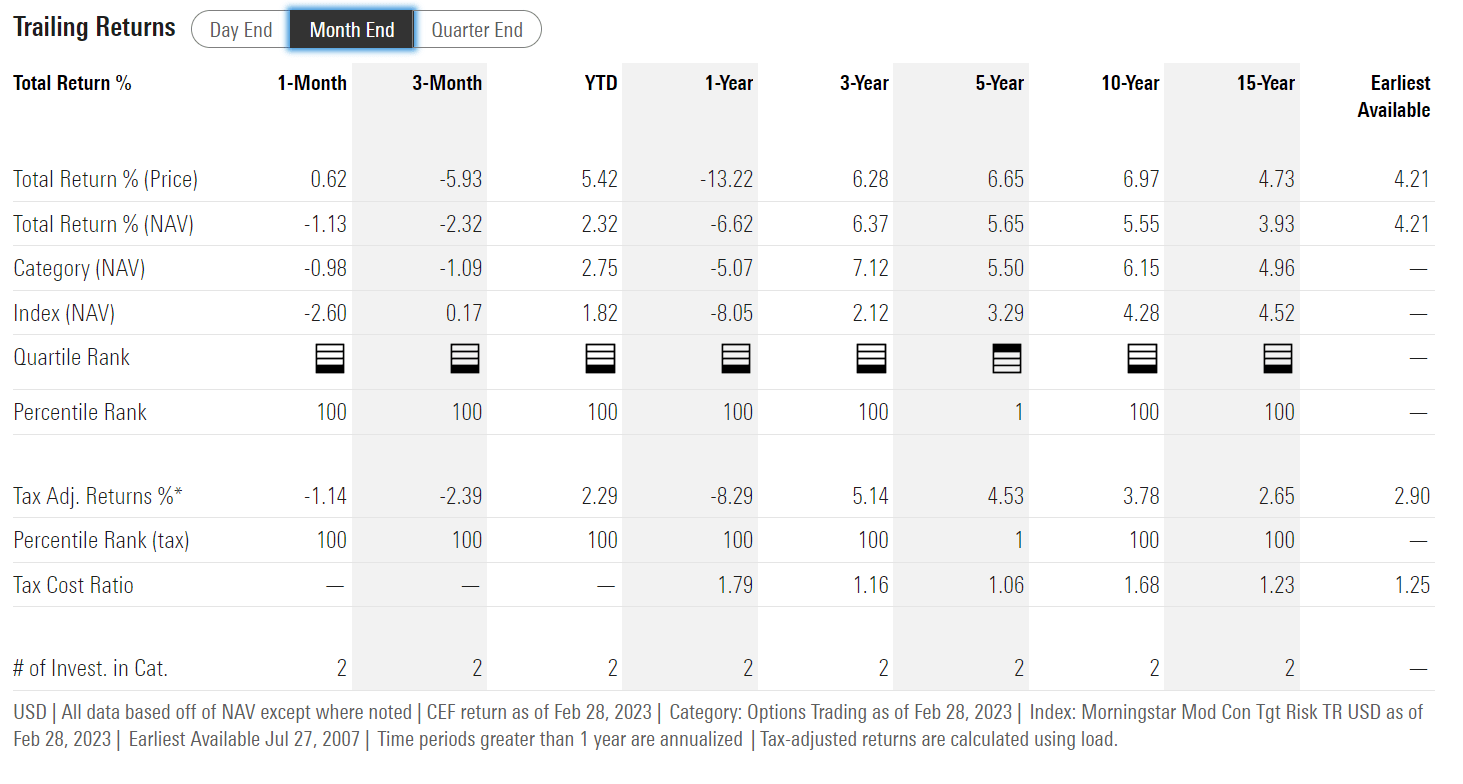

The ETJ fund's historical returns are shown in Figure 2. Overall, the fund has generated modest historical returns, with 3/5/10/15Yr average annual returns of 6.4%/5.7%/5.6%/3.9% respectively to February 28, 2023.

Figure 2 - ETJ has modest historical returns (morningstar.com)

{kind=link}

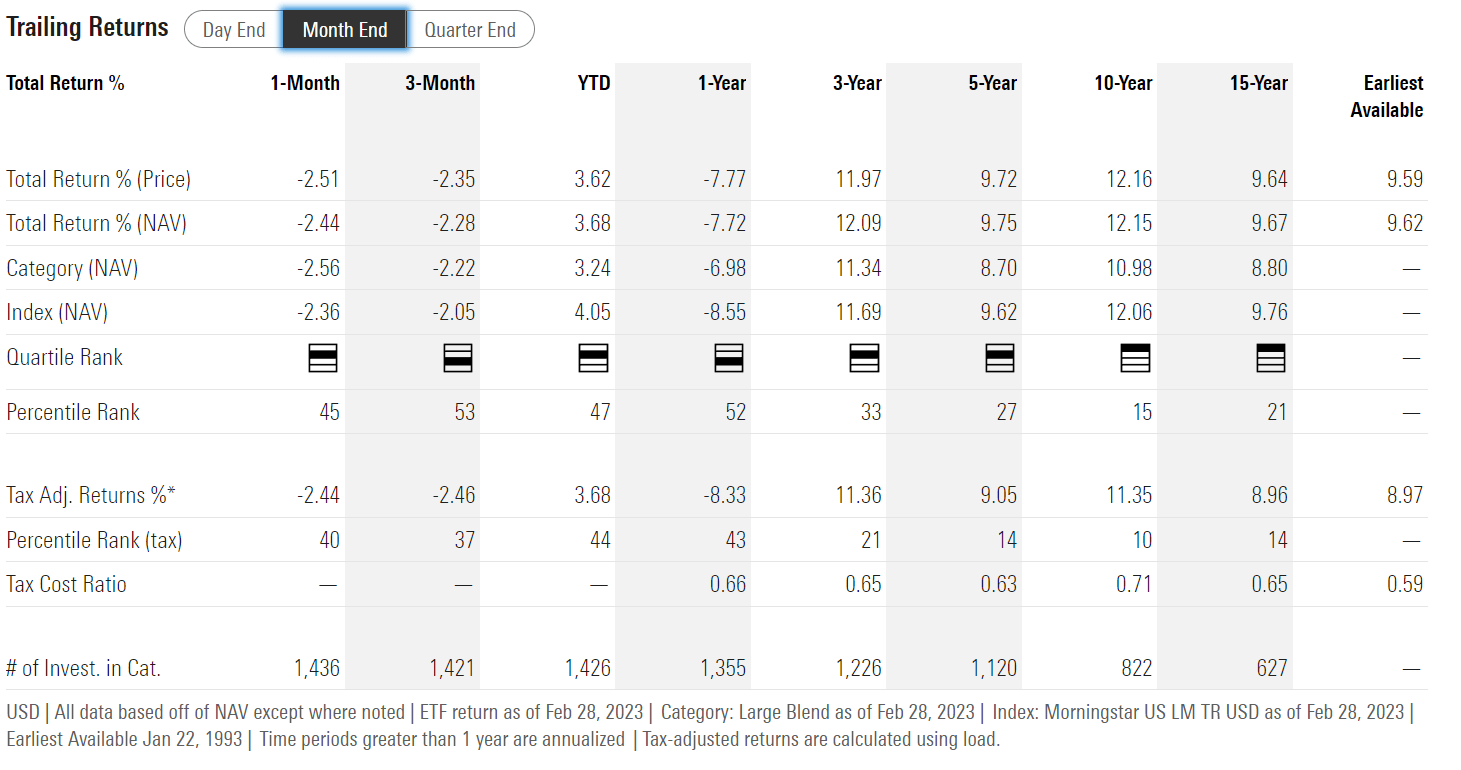

ETJ's returns lag that of the S&P 500 Index, as represented by the SPDR S&P 500 Trust ETF ( SPY ), which has delivered 12.1%/9.8%/12.2%/9.7% respectively to February 28, 2023 (Figure 3).

Figure 3 - ETJ lags the SPY in terms of returns (morningstar.com)

{kind=link}

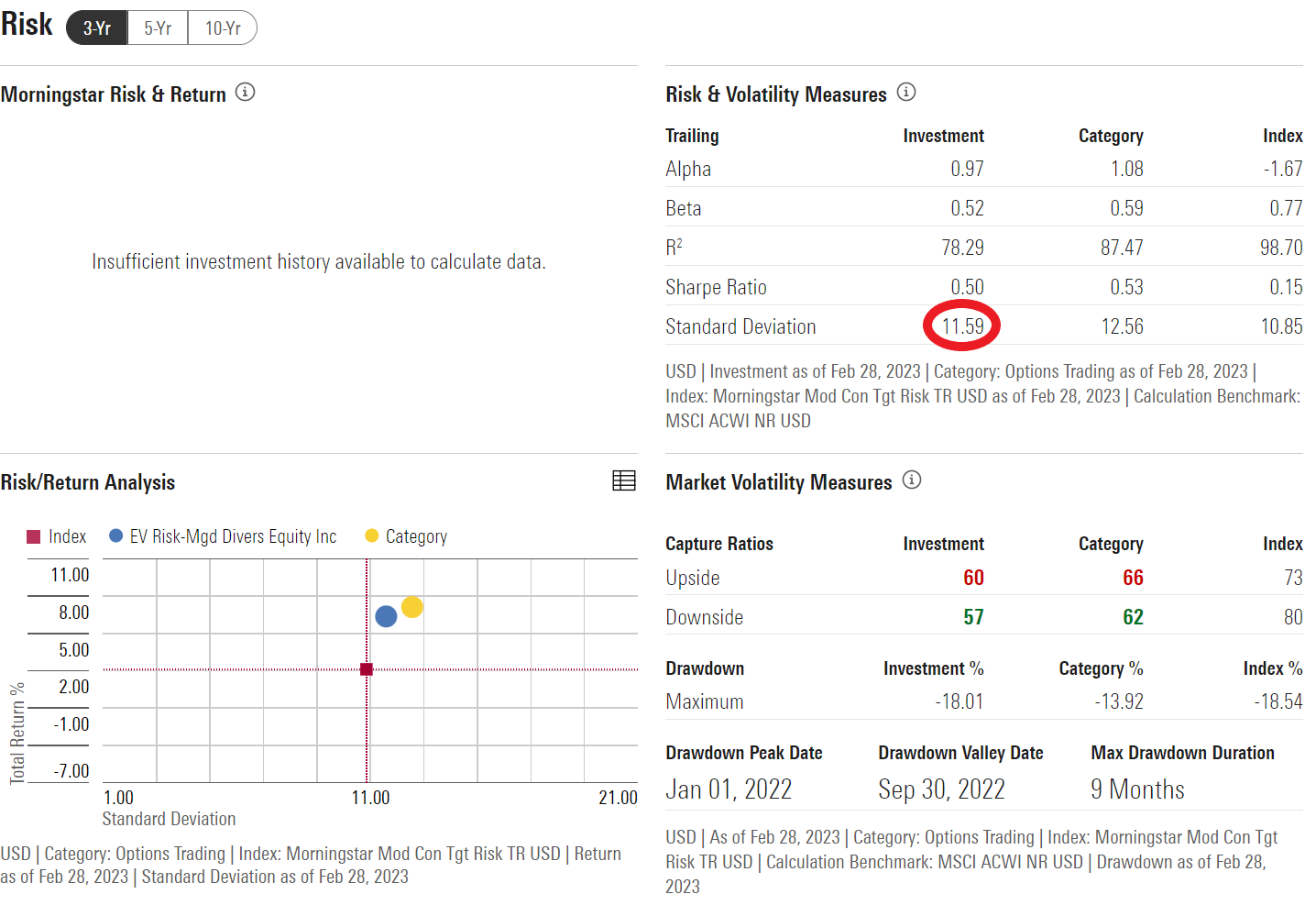

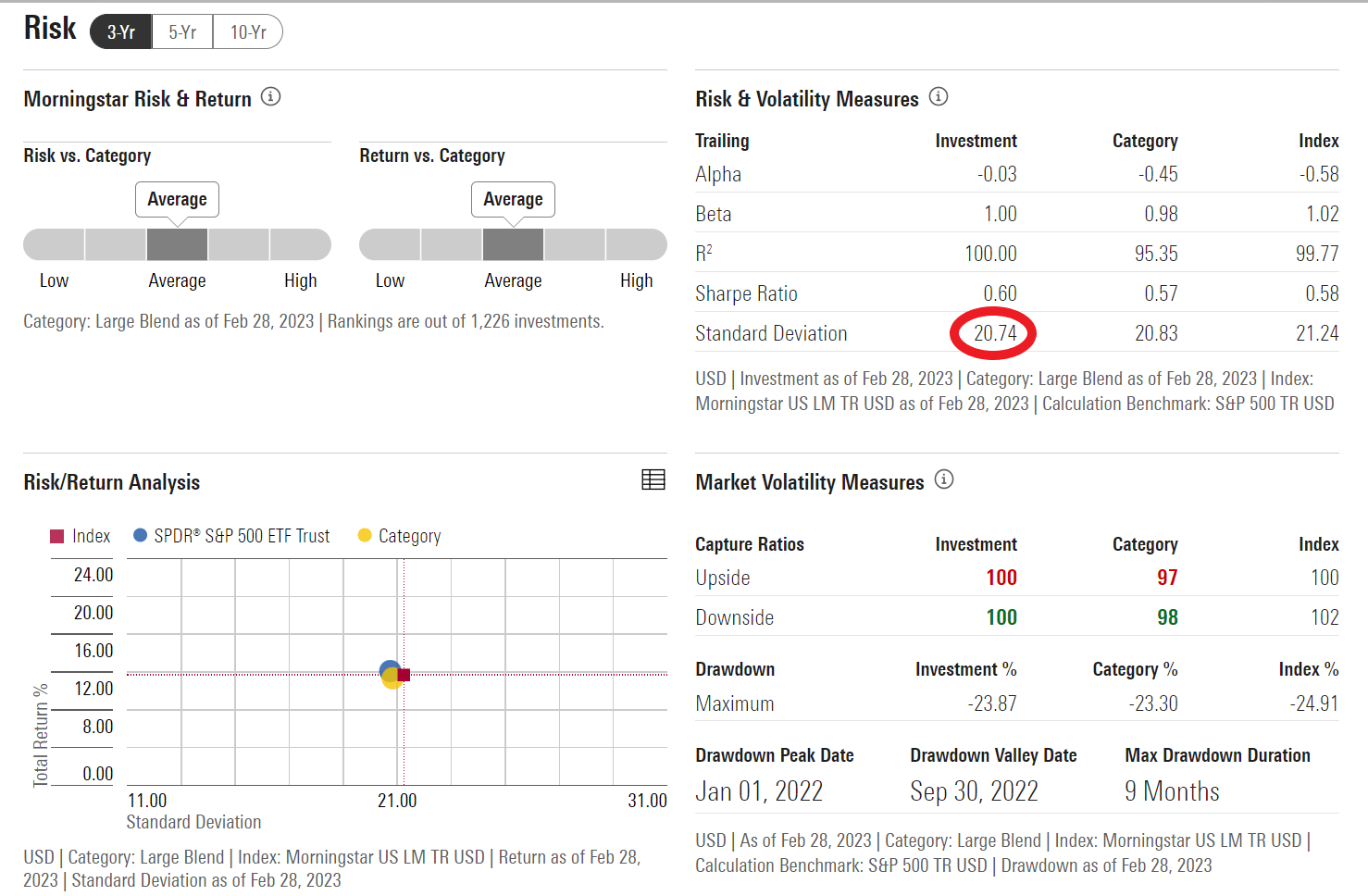

However, ETJ compensates for lower returns by having lower volatilities, with 3/5/10Yr volatilities of 11.6%/10.5%/8.6% respectively (Figure 4).

Figure 4 - As designed, ETJ has reduced volatility (morningstar.com)

{kind=link}

This is roughly 55-60% of the SPY's volatility of 20.7%/18.6%/14.8% respectively on the same time frames (Figure 5).

Figure 5 - SPY has almost double the volatility of ETJ (morningstar.com)

{kind=link}

In effect, the ETJ fund provides 40-50% of the market's returns with 50-60% of the market's volatility. For investors that want reduced exposure to market gyrations with lower commensurate returns, the ETJ fund is not a bad choice. However, one issue I see with the ETJ fund is that its distribution rate is not consistent with its returns profile.

But Distribution Rate Is Too High

The ETJ fund pays a high managed distribution, currently set at $0.0579 / month or a forward yield of 9.1%. On NAV, the ETJ fund is yielding 8.7%.

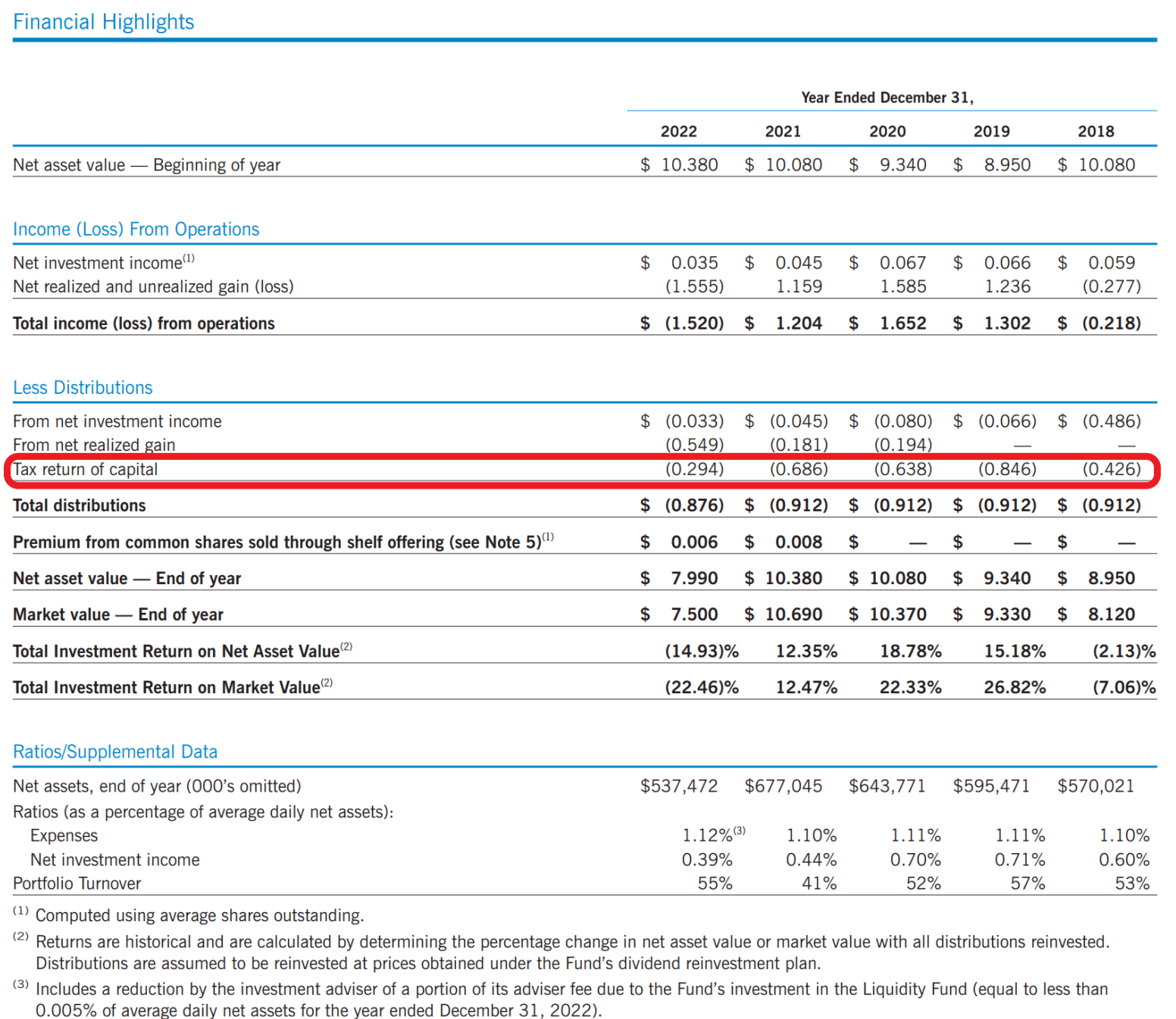

While the 9.1% forward yield is attractive, investors are cautioned that the fund only earns 4-6% in average annual total returns, so it is not 'earning' its distribution. In fact, a significant portion of historical distributions have been funded by return of capital (“ROC”) (Figure 6).

Figure 6 - ETJ has funded significant portion of distributions with ROC (ETJ annual report)

{kind=link}

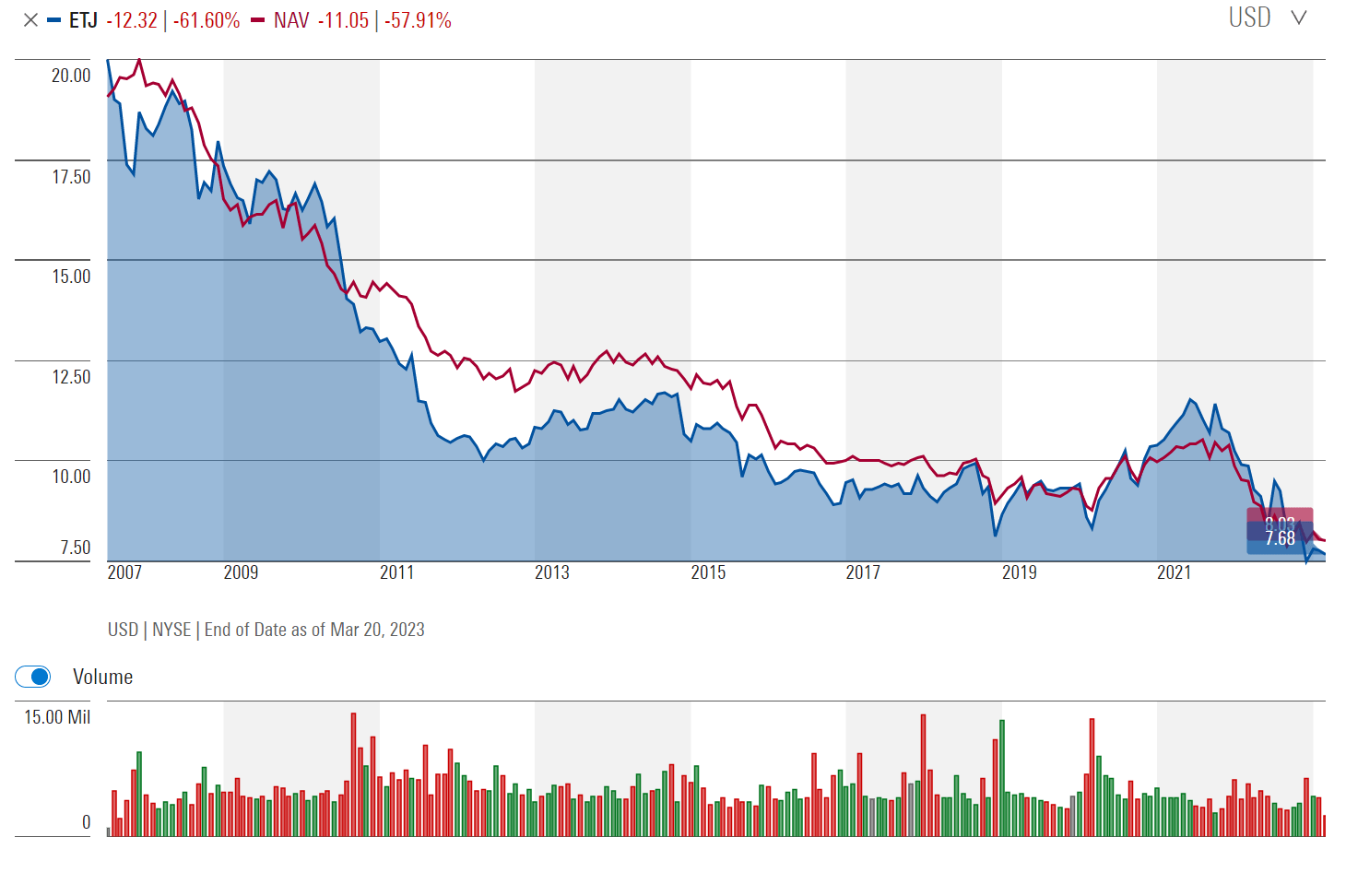

Funds that do not earn their distributions are called ‘return of principal’ funds and are characterized by a long term amortizing NAV like the ETJ (Figure 7).

Figure 7 - ETJ exhibits a long-term amortizing NAV (morningstar.com)

{kind=link}

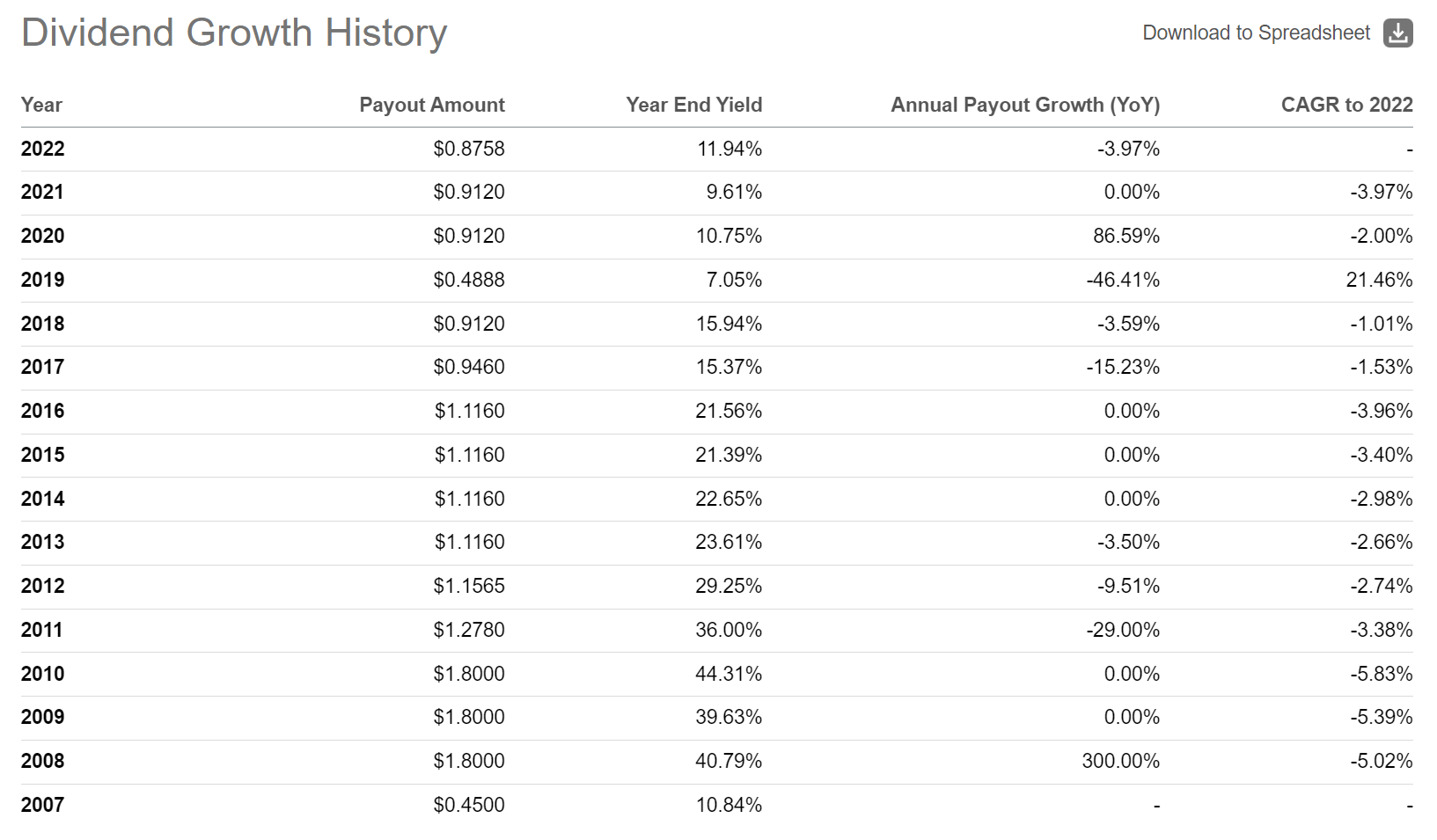

As I have written on numerous occasions, the problem with ‘return of principal’ funds is that their returns are insufficient to fund their distributions. Instead, the fund must liquidate its NAV to maintain the distribution rate that is too high relative to its returns profile. Over time, income earning assets are liquidated to fund the distribution, making future distributions even harder to maintain. Inevitably, ‘return of principal’ funds end up having to reduce their distributions, like ETJ has done on numerous times since inception (Figure 8).

Figure 8 - ETJ has cut distributions on numerous occasions in the past (Seeking Alpha)

{kind=link}

Long-term holders of 'return of principal' funds like ETJ end up having declines in their principal (as market price tend to track NAV) and income (from distribution cuts).

Conclusion

The Eaton Vance Risk-Managed Diversified Equity Income Fund attempts to give investors a smoother investment experience by reducing portfolio volatility through options. It buys index put options to reduce downside capture while selling OTM calls to generate additional income. Overall, the ETJ fund provides 40-50% of the market's returns with 50-60% of the market's volatility, which may be acceptable for risk-averse investors.

The main problem I see with ETJ is that although the fund's returns are modest by design, it continues to pay a very generous monthly distribution, currently set at an annualized 9.1%. The high distribution rate forces ETJ to liquidate NAV to sustain, which makes future distributions harder to fund. Inevitably, this leads to NAV declines and distribution cuts.

Before investing in high-yielding closed-end funds like the ETJ, investors are encouraged to weigh the prospective returns of the asset class (equities in the case of ETJ) and fund structure (buying protective downside OTM puts and selling upside OTM calls) against the distribution yield being offered. If it looks too good to be true, it probably is. I would personally avoid the ETJ CEF.

For further details see:

ETJ: Modest Returns By Design But Yielding 9.1%