URTH - ETO: Limited International Diversification But The Fund Is Not That Bad

2023-12-01 11:46:26 ET

Summary

- Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund offers a 7.27% yield, which is better than many common equities but not impressive compared to fixed-income or blended closed-end funds.

- The fund's performance has been reasonable, with a 2.25% gain since September, but it has underperformed the S&P 500 Index and the MSCI World Index.

- The fund's portfolio is not well-diversified globally, with a majority of its assets invested in American issuers, and its largest positions do not consist of high-yielding dividend stocks.

- The U.S. has substantially outperformed most foreign indices over the past decade, causing most American investors to have a substantial amount of home country risk.

- The fund is fully covering its distribution and trades at a reasonably attractive valuation.

The Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund ( ETO ) is a closed-end fund, or CEF, that specializes in providing its investors with a very high level of current income while still retaining exposure to the upside potential of global equity markets. The fund does boast a 7.27% yield at the current level, which is better than many common equities, but this is not especially impressive compared to the double-digit yields of fixed-income or blended closed-end funds. It is also not really that impressive considering that it is not that difficult to find common equities with yields pretty close to that level in European or Asian markets. After all, many foreign markets have far lower valuations and higher yields than what we find in the United States currently. As this fund's name explicitly states that it invests in dividend-paying stocks from around the world, its yield is not especially impressive.

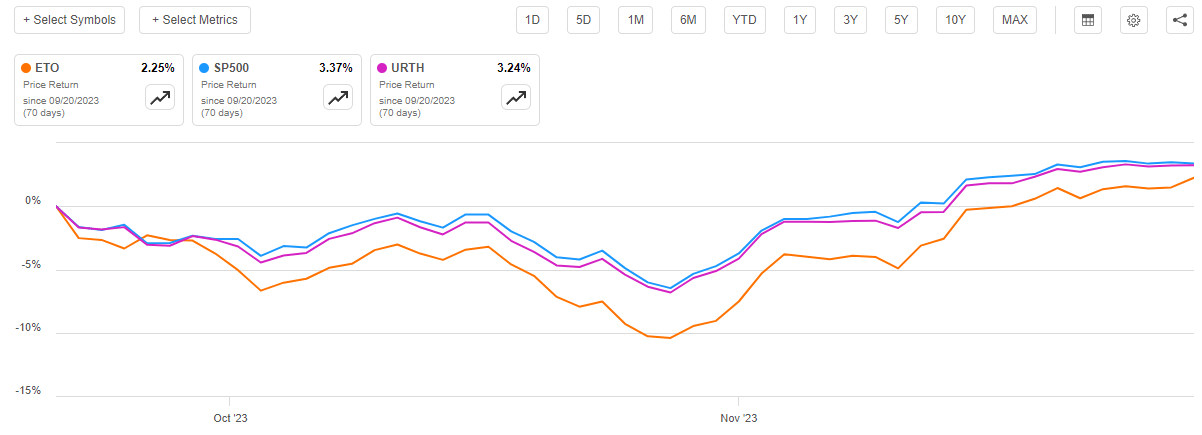

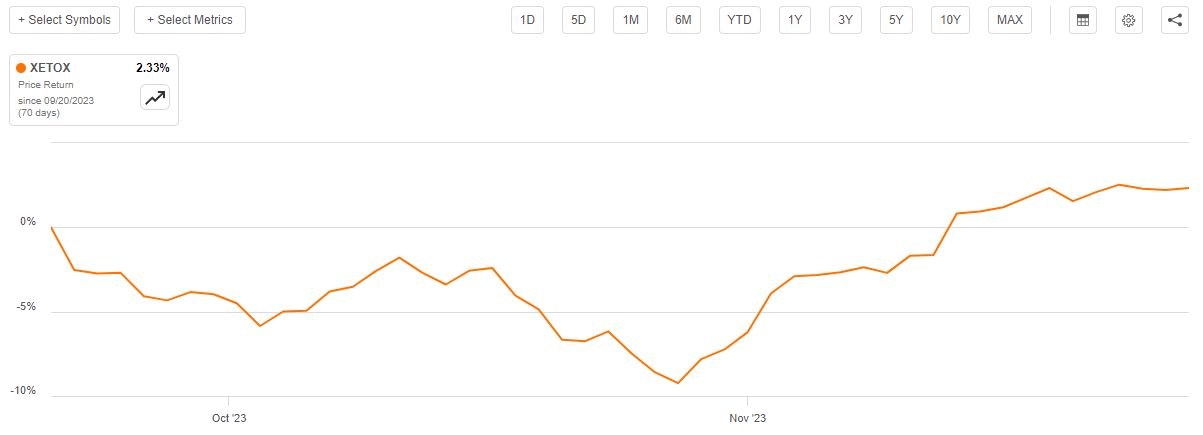

As regular readers may recall, we last discussed the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund back in the middle of September. The conditions in the market have obviously changed a great deal since then, since the overall mood throughout the environment seems to have shifted in late October and asset prices have generally been bid up since that time. As might be expected, the share price performance of this fund has been reasonable since that time, although its 2.25% gain has still been worse than the performance of either the S&P 500 Index ( SP500 ) or the MSCI World Index ( URTH ):

{kind=link}

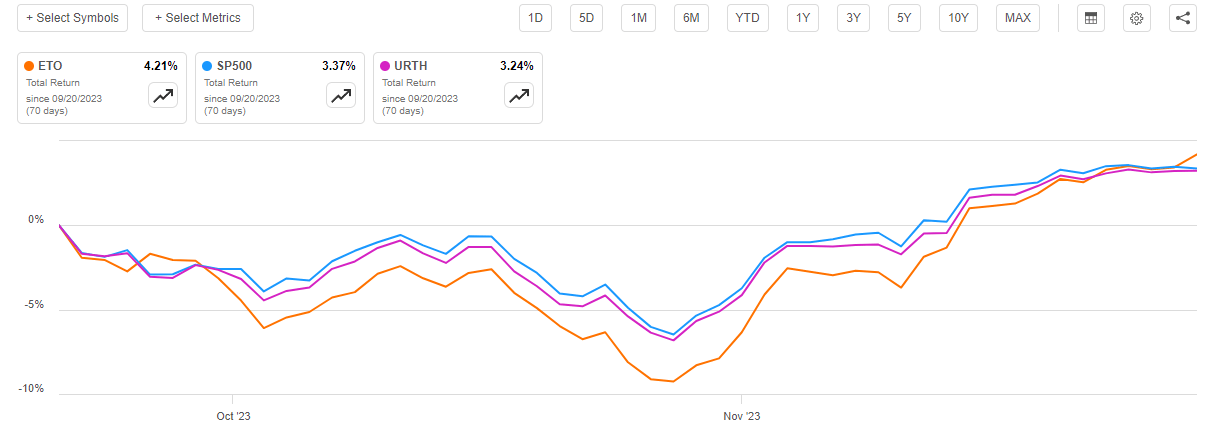

This is still certainly better than the losses that the shares of numerous other funds have been handing us since that time, however. As I have pointed out before, it is sometimes misleading just looking at the price performance of a closed-end fund's shares. After all, the modus operandi of most of these funds is to pay out essentially all of their investment profits to the shareholders and simply attempt to keep the fund's net asset value per share relatively stable. As such, we can get a better idea of how investors in this fund have actually done by adding in the distributions that it paid out. When we do that, we see that investors in this fund have seen their money appreciate by 4.21% since the date that my prior article on this fund was published. That is much better than the return of either the S&P 500 Index or the MSCI World Index over the same period:

{kind=link}

Thus, for the most part, investors in this fund have been suitably pleased with its overall performance over the past two months. However, this alone does not mean that the fund is a good investment today as there have been recent cases of funds getting bid up beyond that justified by their performance.

Let us investigate and attempt to determine whether or not purchasing this fund makes sense today following its recent gains.

About The Fund

According to the fund's webpage , the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has the primary objective of providing its investors with a very high level of after-tax total return. This makes a great deal of sense, as this fund invests primarily in common equities. As we can see here, 80.64% of the fund's assets are invested in common equities, alongside much smaller allocations to preferred stock, bonds, and various other things:

CEF Connect

Common equities are by their very nature a total return vehicle. After all, investors typically purchase common equities because they are seeking to receive income in the form of dividends as well as capital gains that accompany the growth and prosperity of the issuing company. The same cannot be said of preferred stocks and bonds. As I have pointed out in numerous previous articles, these assets are intended primarily as income vehicles. However, their inclusion in a fund like this is usually an attempt by the fund's managers to generate a higher level of income than could ordinarily be obtained by simply investing in common equities. As income is a component of total return, their inclusion still works with that objective.

The fund's fact sheet provides a description of the fund's strategy, as Eaton Vance does not include such information on the fund's website for some reason. Here is how the fact sheet describes the fund's strategy:

The fund invests primarily in global dividend-paying common and preferred stocks and seeks to distribute a high level of dividend income that qualifies for favorable federal income tax treatment.

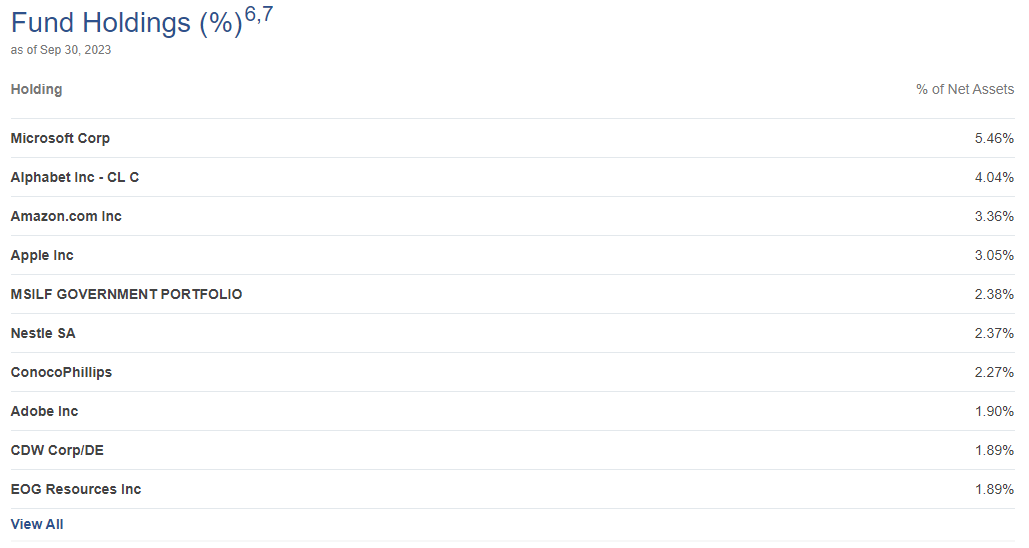

This is pretty much what we would expect from a fund whose name basically states that it invests in dividend-paying common equities. However, the fund's portfolio is certainly a bit strange if that is its strategy. The fund's largest positions include a number of companies that either do not pay a dividend or pay such a small one that it is basically immaterial. Here are the largest positions in this fund's portfolio:

{kind=link}

Here are the current yields of these stocks:

| Company |

| Current Yield |

| Microsoft ( MSFT ) |

| 0.79% |

| Alphabet ( GOOG ) |

| N/A |

| Amazon.com ( AMZN ) |

| N/A |

| Apple ( AAPL ) |

| 0.51% |

| Nestle S.A. ( NSRGY ) |

| 2.92% |

| ConocoPhillips ( COP ) |

| 2.04% |

| Adobe Inc. ( ADBE ) |

| N/A |

| CDW Corp. ( CDW ) |

| 1.17% |

| EOG Resources ( EOG ) |

| 2.95% |

As of the time of writing, the S&P 500 Index yields 1.55%, and the MSCI World Index yields 1.57%. As we can see, the only stocks on this list that have a higher yield than either of the indices are the two energy companies and the Swiss food company. There are three companies on this list that pay no dividends at all. Furthermore, both Microsoft and Apple might as well be non-dividend-paying stocks with how low those yields are. Overall, this certainly looks like a very strange portfolio for any fund that claims to be specifically targeting its investments towards "dividend-paying stocks."

Another thing that we notice here is that only one of the companies on this list is not an American company. That is another very strange thing to see from a global fund, although now that the United States accounts for 69.80% of the MSCI World Index, it probably should not be that surprising. The United States accounts for less than a quarter of global economic output so just about any fund that invests in both American and foreign companies will be substantially overweighted to the United States relative to its actual representation in the global economy. We do see that in this fund too, as 63.40% of the fund's assets are invested in American issuers:

Fund Fact Sheet

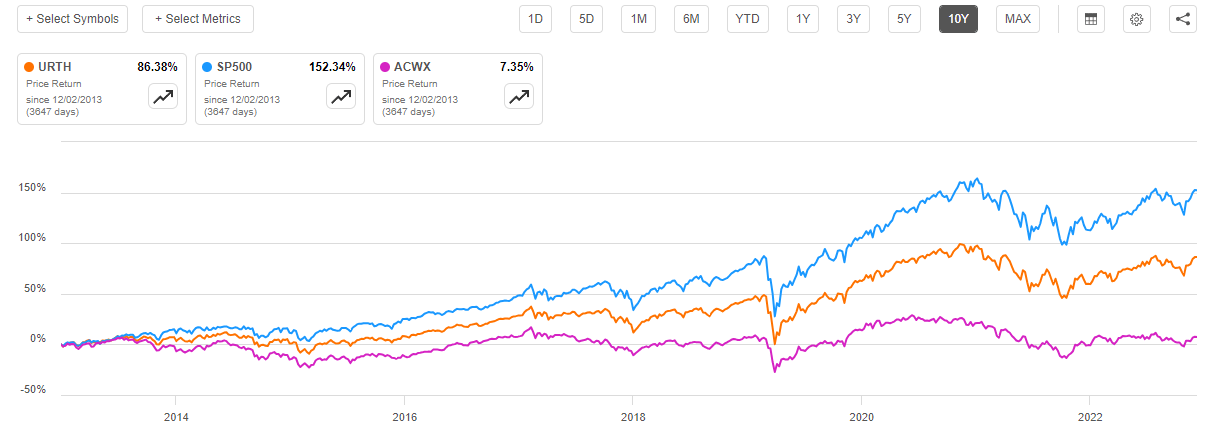

Fortunately, this is not nearly as bad as what we see in the MSCI World Index. That is a good thing, as one of the biggest problems facing the average American right now is that they are overweighted to their home nation. This is not surprising, considering that the United States has substantially outperformed other global markets over the past decade. We can see this quite clearly by comparing the MSCI World ex-US Index ( ACWX ) to the MSCI World Index and the S&P 500 Index over the past decade. Here is the chart:

{kind=link}

As we can see, the S&P 500 Index has more than doubled over the past decade and the MSCI World ex-US Index has been basically flat. Apart from the United States, the entire planet's markets only went up 7.35% over the course of ten years. That is less than 1% per year. There can be little wonder then that foreign stocks frequently have much higher yields than American ones. The MSCI World ex-US Index has a 2.39% yield right now and there are several countries whose securities comprise that index with higher yields than that figure. We can see this simply by looking at some of the single-country index exchange-traded funds:

| Index Fund |

| TTM Yield |

| iShares MSCI Germany ETF ( EWG ) |

| 2.69% |

| iShares MSCI United Kingdom ETF ( EWU ) |

| 3.38% |

| iShares MSCI France ETF ( EWQ ) |

| 2.50% |

| iShares MSCI Italy ETF ( EWI ) |

| 3.48% |

| iShares MSCI Singapore ETF ( EWS ) |

| 4.89% |

These high yields relative to the United States come from the fact that the market has not been rewarding the growth of the companies in these nations. After all, a company that increases its dividend every year but sees minimal share price appreciation will end up with higher yields after a few years have passed. In addition, a company that is unable to reward its shareholders with capital gains will simply start paying out a larger dividend to provide some sort of investment return. We can see then that yield-seeking investors might be better served by purchasing equities in foreign countries as opposed to within the United States. This could also provide another benefit as it provides exposure to foreign currency, and some of these nations have far better national fiscal outlooks than the United States.

As a result of the general outperformance of the United States relative to foreign countries over the past ten years, any investor who was not actively rebalancing and reducing their American exposure over time is now undoubtedly highly exposed to this country. That is a particularly big risk for American investors since their income is also earned in the United States. As such, an event such as a severe recession in the United States could result in both the loss of income (due to a job loss) as well as a market decline that inflicts damage to their investment portfolio. The only realistic way to reduce this risk is to increase foreign market exposure at the expense of American market exposure. Unfortunately, as we can see, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund is not doing that particularly well. After all, the fund still has more than half of its assets invested in American issuers. As such, we cannot rely on this fund as a way to achieve global diversification.

A look at the largest positions in the fund may lead one to believe that this fund has outsized exposure to the American technology industry. However, that is surprisingly not the case. The Information Technology sector constitutes 21.72% of the MSCI World Index, but this fund only has 19.12% of its assets invested in that sector.

Fund Fact Sheet

As we can see, the only sector to which this fund is significantly overweight relative to the index is financials. That is something that could concern some readers. After all, American banks suffered $126 billion in unrealized losses during the third quarter of this year and are now sitting on $684 billion in total unrealized losses overall:

Schiff Gold/Data from FDIC

However, it does make some sense for an equity income fund to be overweight financials. Other than perhaps energy, the financial sector has some of the highest yields available in the market today. This is partly because investors have been very worried about the impact of rising rates on the value of the fixed-income securities and loans held by the banking system. We can certainly see above that these fears are not altogether unjustified. However, as I have pointed out before, at the moment these are only paper losses and do not translate into real losses unless the bank is forced to sell the security prior to maturity. In addition, the Federal Reserve set up a program in the aftermath of the Silicon Valley Bank collapse that was intended to prevent banks from being forced to sell their securities at a loss. While the same cannot be said for banks in foreign countries, it seems very unlikely that regulators and central banks in any developed country will allow any bank's losses to get too great for it to bear. As such, we probably do not need to worry too much about the fact that this fund is heavily invested in the banking sector.

Leverage

As is usually the case with closed-end funds, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund employs leverage as a means of boosting the effective total return of its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase common stocks or other assets. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective return of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has leveraged assets comprising 20.07% of its portfolio. This is a bit less than the 20.34% leverage that the fund had the last time that we discussed it, which makes a certain amount of sense. After all, we have already seen that the fund's share price has increased since our last discussion about this fund. The fund's net asset value per share has increased by 2.33% over the period as well:

{kind=link}

Thus, the fund simply maintaining static leverage would result in the ratio going down because the portfolio's net assets went up. This was pretty much exactly what happened over the past two months.

The fund's leverage appears to be very reasonable at the current level, and it represents a nice balance between risk and reward. We should not need to worry about it too much.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund is to provide its investors with a very high level of after-tax total return. In order to accomplish this objective, it invests in a portfolio that consists primarily of dividend-paying stocks. As we have already seen, there are certainly several assets in the portfolio that are not dividend-paying common equities, but the majority of its holdings are, even if their yields leave something to be desired. The fund collects the money that it receives from these securities into a pool and adds any capital gains that it realizes to this pool of money. It seems likely that the capital gains could be a greater source of investment return than the dividends, considering the low yields of many of the securities here. When we consider that common equities on average appreciate by around 10% per year though, realized capital gains can give a portfolio a reasonable total return. The fund pays out all of the money that it manages to collect via these business operations to its shareholders, net of its own expenses. We can assume that this would result in the fund having a reasonably attractive yield.

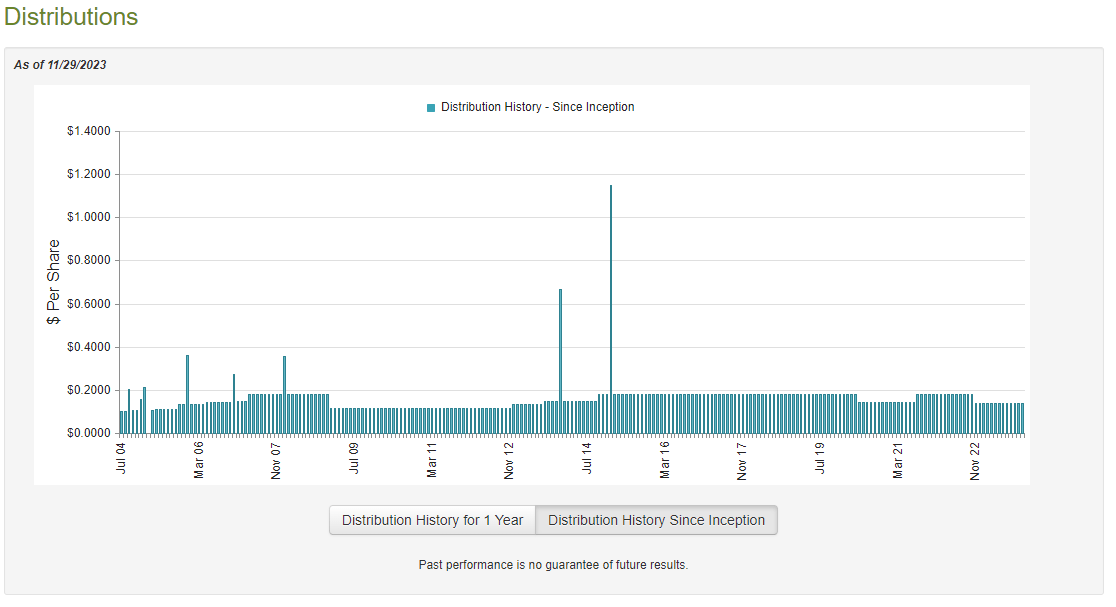

This is certainly the case, as the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund pays a monthly distribution of $0.1374 per share ($1.6488 per share annually), which gives it a 7.27% yield at the current price. That is certainly not an incredibly attractive yield compared to many other closed-end funds, but it is certainly not horrible compared to the yield of most common stocks. Unfortunately, this fund has not been especially consistent with respect to its distribution over the years. As we can see here, the fund has varied its payout by quite a lot over its history:

{kind=link}

The fact that the distribution has tended to vary over time may prove to be something of a turn-off for those investors who are seeking to generate a safe and consistent income from the assets in their portfolios. The distribution cut last year certainly will not improve the fund's perception in the eyes of income-focused investors as it came at a time when inflation was very high and caused the purchasing power of the fund's distributions to decline. During such an environment, investors need rising income to maintain their lifestyles, not static or declining ones.

However, as I have pointed out in the past, the fund's history is not necessarily the most important thing for anyone who is considering purchasing the fund today. After all, today's buyer will receive the current distribution and the current yield. This hypothetical buyer will be completely unaffected by actions that the fund had to take in the past. As such, we should investigate the fund's finances in order to determine how well it can sustain its current distribution.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, it will not include any information about the fund's performance over the past seven months. That is quite disappointing as a great many things occurred over that period. For example, the market was generally characterized by euphoria during the first three months of that period as investors bid up the price of various technology stocks that had a relationship to artificial intelligence. There was also a return of the bear market that lasted throughout much of the summer. These events almost certainly had an impact on the value of the fund's assets and its ability to generate sufficient returns to cover the distribution, but at the present time, there is no official information available from the fund sponsor detailing its performance over that period.

During the six-month period reflected in the report, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund received $9,046,608 in dividends along with $2,024,448 in interest from the assets in its portfolio. This gives the fund a total investment income of $11,071,056 over the period. The fund paid its expenses out of this amount, which left it with $6,087,152 available for shareholders. Obviously, that was nowhere near enough to cover the distribution that the fund actually paid out. The fund paid total distributions of $13,510,381 to its investors over the period. At first glance, this is something that could be concerning, as the fund did not have nearly enough net investment income to cover the distributions that it paid out.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distributions. For example, the fund might be able to realize some capital gains that can be paid out to the investors. Realized gains are not included in net investment income, but they obviously reflect money that comes into the fund. Fortunately, the fund enjoyed a great deal of success in this task during the period. It reported net realized gains of $10,145,289 and had another $34,150,676 in net unrealized gains. Overall, the fund's net asset value increased by $36,872,736 after accounting for all inflows and outflows during the period. Thus, the fund did manage to cover its distributions during the period.

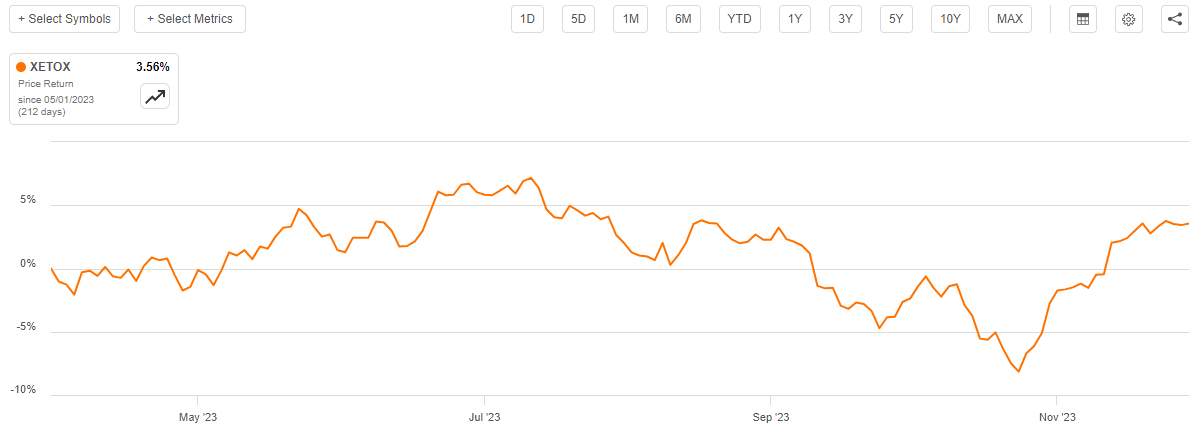

It remains to be seen whether or not the fund can sustain its distribution going forward, but its net asset value per share is up 3.56% since May 1, 2023:

{kind=link}

This strongly suggests that the fund has managed to cover its distributions since the end date of the most recent financial report, which is a good sign. Overall, we probably do not need to worry about a near-term distribution cut.

Valuation

As of November 29, 2023 (the most recent date for which data is available as of the time of writing), the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has a net asset value of $25.03 per share but the shares only trade for $22.70 each. This gives the shares a 9.31% discount on net asset value at the current price. That is a fairly large discount, although it is not as good as the 11.11% discount that the fund's shares have had on average over the past month. As such, it might be possible for investors to obtain a better yield by waiting for a better entry point, although the current price is not horrible if you wish to obtain the fund's shares today.

Conclusion

In conclusion, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund is a closed-end fund that has proven to be relatively popular among investors who are seeking to earn a high level of income from the assets in their portfolios. However, the fund does not have nearly as much international diversification as might be expected from a global fund, although this may not be entirely the fault of the fund managers. After all, the United States is substantially overweighted in many global indices right now, so if the fund were not overweighted to this index, there could be some investors who would be complaining about underperformance. Other than this complaint though, the fund looks decent as it is fully covering its distribution and it is currently trading at a discount on net asset value.

For further details see:

ETO: Limited International Diversification, But The Fund Is Not That Bad