URTH - ETO: Underperforming Recently But A Decent Fund

2023-09-20 17:09:31 ET

Summary

- Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has underperformed the market in recent months, possibly due to the impact of high interest rates on high-yielding assets.

- The fund's portfolio is decent, with a relatively low allocation to the technology sector compared to other Eaton Vance funds.

- The fund offers a sustainable 7.40% distribution yield and is trading at an attractive valuation with a 9.59% discount to net asset value.

- The fund is significantly overweighted to financials, but global financials have actually been delivering a fairly strong performance recently.

- The fund's portfolio is outperforming its share price right now, creating an opportunity for investors to purchase it.

The Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund ( ETO ) is a fairly well-known and popular fund among closed-end fund ("CEF") investors. The fact that the fund advertises itself as a globally focused fund with a respectable 7.40% distribution yield is possibly the source of its popularity. Then again, its popularity could also be linked to the fact that the fund is affiliated with Eaton Vance ("EV"), which is a fairly well-known and respected fund house. As I pointed out in my last article on this fund, its performance is quite decent, too, as the fund was outperforming the MSCI World Index ( URTH ) as of mid-July. Unfortunately, its performance since that time has left something to be desired. As we can see here, the fund's shares are down 1.97% over the past three months:

{kind=link}

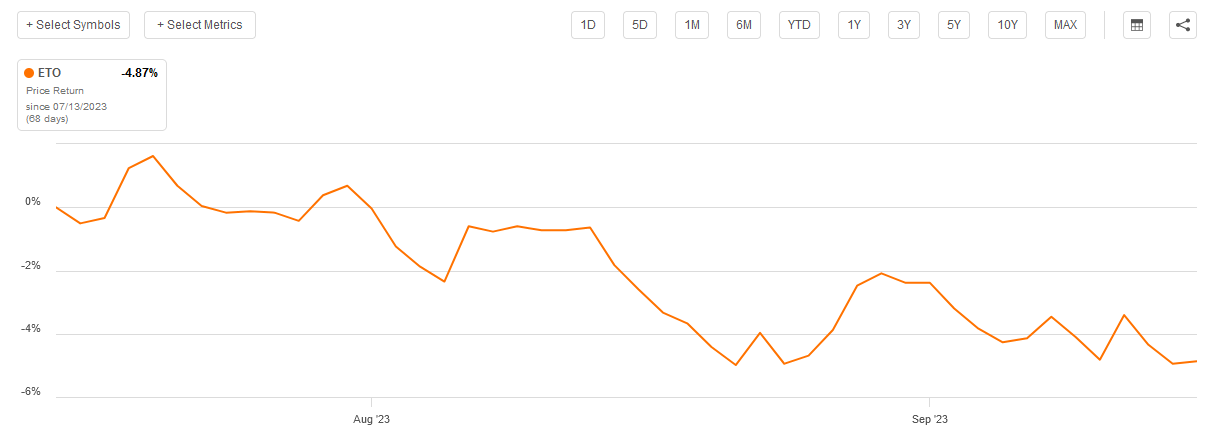

The fund's performance since my article was published has been even worse, as its shares are down 4.87%:

{kind=link}

The S&P 500 Index (SP500) is down over the same period, but not nearly to the same degree. This could have something to do with the fund's significant allocation to the major American technology companies, which I pointed out in the previous article. With the notable exception of Alphabet ( GOOG ) (GOOGL) aka Google, two of the three largest holdings in the fund as of that date are down substantially more than the S&P 500 Index.

This alone does not necessarily mean that this is a poor fund. After all, it can change its positions around as sectors go in and out of favor. This is one advantage that actively managed funds have over index funds. In addition, the fund does sport a much higher yield than just about any equity index outside of the energy sector. As such, it might still prove to be a good holding for the right type of investor. As it has been a few months since we last discussed it, let us revisit the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund and see if it could potentially make sense to pick up today.

About The Fund

According to the fund's website , the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has the stated objective of providing its investors with a high level of after-tax total return. This makes a great deal of sense considering that the fund's name suggests that it invests primarily in common equity. After all, only common and preferred equity pays dividends to investors. A look at the portfolio confirms this, as currently 83.36% of the fund's assets are invested in common stock. The fund also has reasonably large allocations to both preferred stock and bonds:

CEF Connect

As I have pointed out many times in the past, any fund that invests primarily in common stock will almost certainly have total return as its primary objective. After all, common stock is by its very nature a total return vehicle, as investors primarily purchase common stock to receive dividends as well as benefit from the capital gains that accompany a company's growth and prosperity. In contrast, both bonds and preferred stock deliver their returns primarily through the direct payments that they make to their owners. However, these direct payments are a component of total return, so the fund's objective still remains intact.

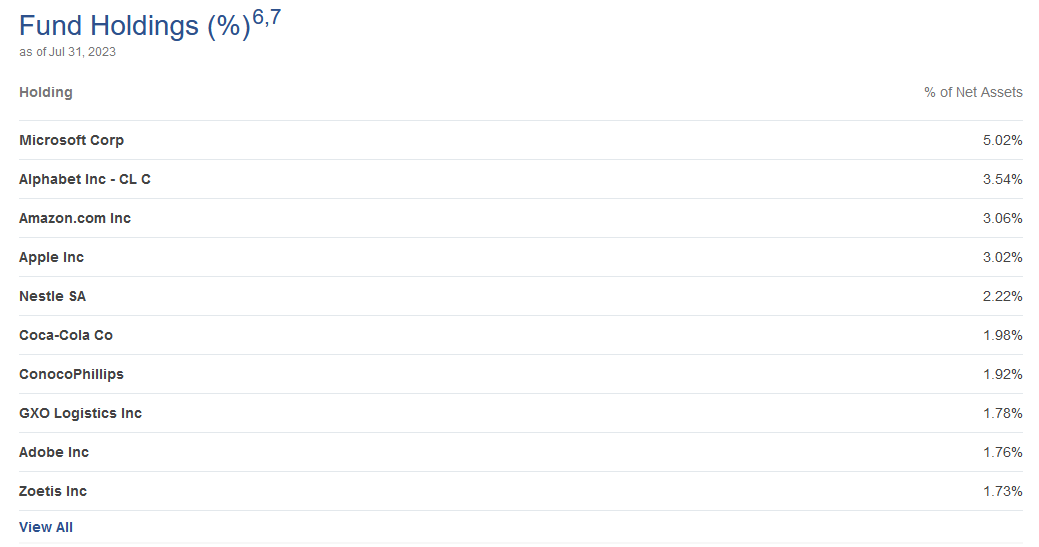

As I mentioned in my previous article on the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund, as well as numerous other Eaton Vance funds, the funds from this fund house have a tendency to include very heavy weightings to the American mega-cap technology companies. We can see that this is the case with this one today by looking at the largest positions in the fund:

{kind=link}

The combined weightings of Microsoft ( MSFT ), Alphabet, Amazon ( AMZN ), and Apple ( AAPL ) are 14.64% of the fund's total assets. This is less than the 19.13% weighting of these four companies in the S&P 500 Index, but it is still a lot for any fund, especially considering that all four companies are from the same sector.

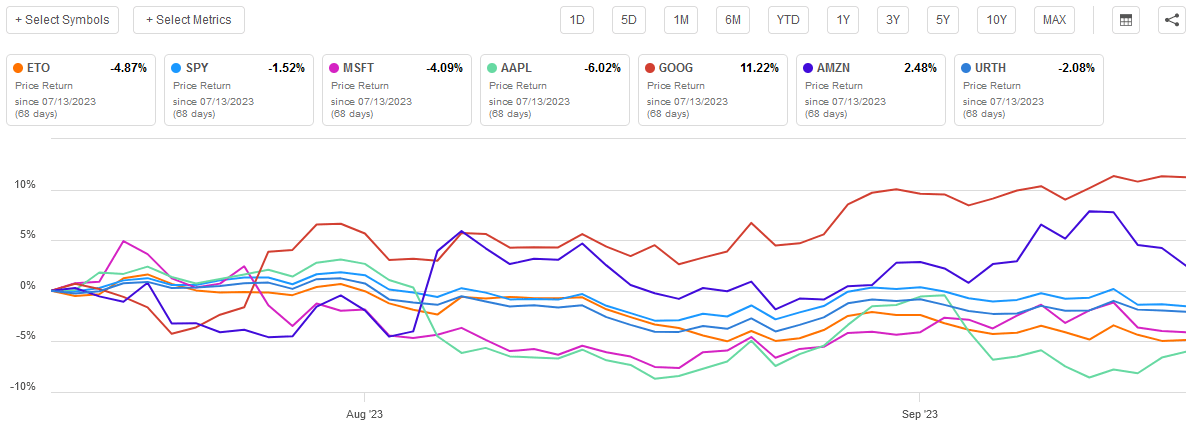

In the introduction to this article, I suggested that the heavy weighting of these companies could be one reason why the fund's share price declined more than the S&P 500 Index. This chart shows the price performance of these four companies, along with the fund, and both the S&P 500 Index and the MSCI World Index since the time that my previous article on this fund was published:

{kind=link}

We can see that both Microsoft and Apple underperformed the S&P 500 over the period by quite a lot. However, both Alphabet and Amazon outperformed both the S&P 500 Index and the MSCI World Index. When we consider that this fund is less heavily weighted to these companies than the S&P 500 Index, especially Apple (the worst performer over the period), my initial assumption was probably not correct.

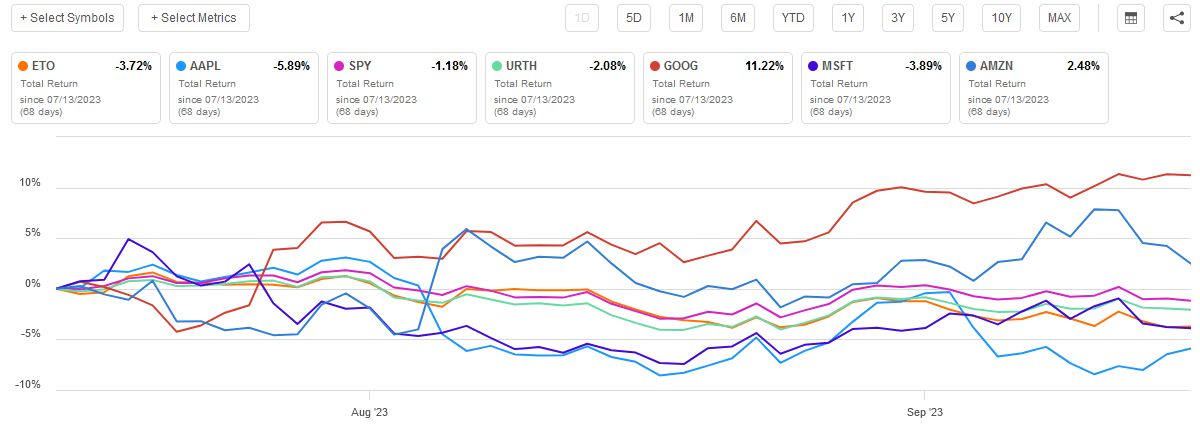

One important factor to consider is that the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund pays out a substantially higher yield than any of the above assets. This will offset some of the price declines. As such, we really should be comparing the assets on a total return basis, not solely based on their price action. Here is the same chart, using total return instead of price return:

{kind=link}

We can see here the fund does a bit better, but it still underperforms both the S&P 500 Index and the MSCI World Index. Apple and Microsoft also see a slightly improved performance, while Alphabet and Amazon still outperform. Thus, nothing really changes here, which is probably because the time period was too short for the Eaton Vance Fund's higher yield to really make a difference.

Thus, it appears that we may have to look elsewhere to find the source of the underperformance, as it was probably not solely driven by the fund's heavy allocation to those four bubble stocks. The fund's fact sheet provides some insight here. It includes some helpful information regarding the fund's sector allocation in comparison to the MSCI World Index:

Fund Fact Sheet

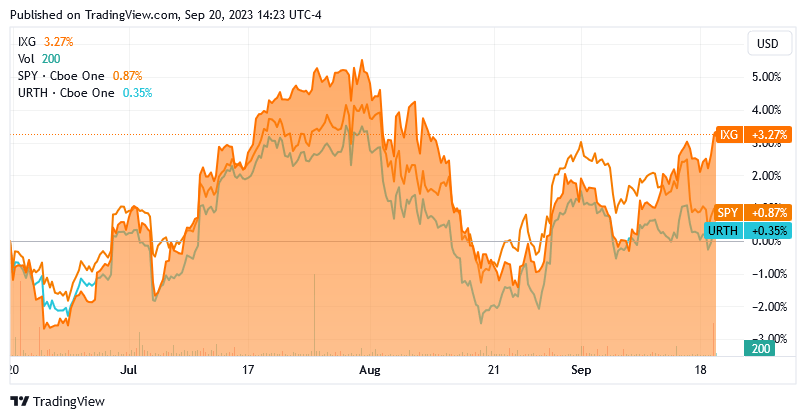

The big thing that we see here is that the fund's allocation to the financial sector is substantially above the MSCI World Index. We have been hearing a lot in the media about how the high interest rate environment has been having negative impacts on the world's financial institutions. After all, the United States is not the only nation that has increased its interest rates, although the Federal Reserve has been more aggressive than most other central banks. It seems unlikely that this high allocation to financials has been dragging on the fund's performance, however. After all, the iShares Global Financials ETF ( IXG ) has actually outperformed both the S&P 500 Index and the MSCI World Index over the past three months:

{kind=link}

We would think that the fund's outsized weightings to financials should lead to outperformance relative to the indices, not underperformance. It is possible that the outsized exposure to utilities played a role here, as the iShares Global Utilities ETF ( JXI ) has substantially underperformed both indices over the period. However, it seems unlikely that the extra 2.53% allocation to utilities would be enough to drag down the whole fund so dramatically compared to the index.

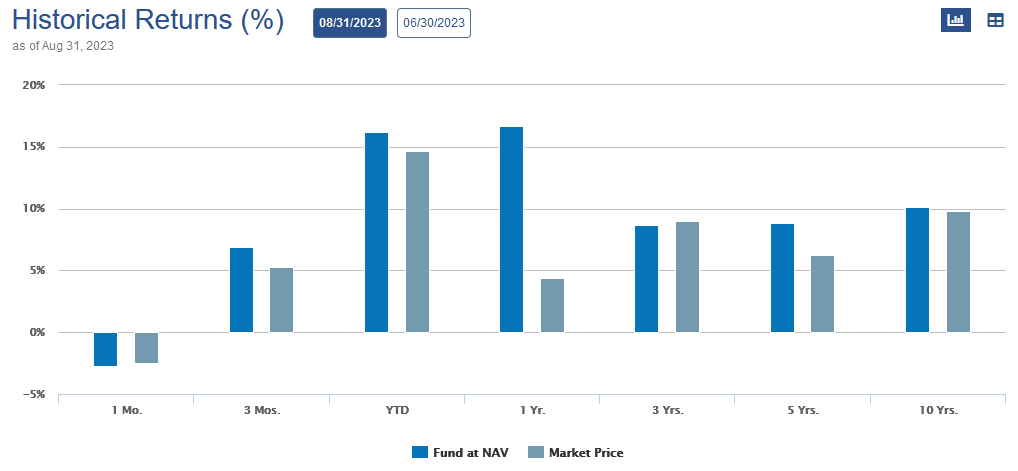

One thing that we do note though is that the fund's share price appears to be underperforming the actual underlying portfolio:

{kind=link}

As we can see here, the fund's portfolio has substantially outperformed the market price of the fund during the trailing three-month period, year-to-date period, and one-year period. While this data is only relevant to the end of August, it still gives us a good idea that at least part of the underperformance, if not most of it, can be explained by the market not valuing the shares in line with the intrinsic value of the portfolio. This is a common occurrence with closed-end funds that can sometimes allow investors to obtain shares of the fund for less than they are actually worth. We will discuss this in more detail later in this article.

Leverage

One strategy that is employed by the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund to boost its total returns is leverage. I explained how this works in a recent article :

In short, the fund borrows money and then uses that borrowed money to purchase common stocks or other assets. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective return of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has levered assets comprising 20.34% of the portfolio. This is a reasonable level of leverage that is significantly below that of most other closed-end funds, and it is of course well below the specified one-third of assets level. As such, it appears that this fund is striking a reasonable balance between risk and reward.

One thing that is worth noting is that this fund's leverage might be one factor that is contributing to its underperformance relative to the index. This is because it amplifies the fund's losses during market declines and makes it more difficult for it to catch up during the following bull market run. This is usually more of a problem over long-term horizons than it would be over a shorter timeframe, though.

Distribution Analysis

As mentioned earlier in this article, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has the primary objective of providing its investors with a high level of after-tax total return. However, as the name suggests, the fund invests in a portfolio that includes a number of dividend-paying common stocks, although it is not exclusively focused on them. The fact that the fund is overweight both financials and utilities and underweight information technology does suggest a marked preference for dividend-paying stocks, though. The fund also seeks to earn capital gains from the assets in its portfolio, which provides it with some realized profits from the non-dividend-paying stocks that are included in the portfolio.

As is the case with most closed-end funds, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund then pays out all of its investment profits, net of the fund's own expenses, to the shareholders via distributions. The goal is for the fund to keep the assets in its portfolio at about the same level over time while paying all of its profits out to the investors. This all would likely lead someone to expect that the fund has a very high yield.

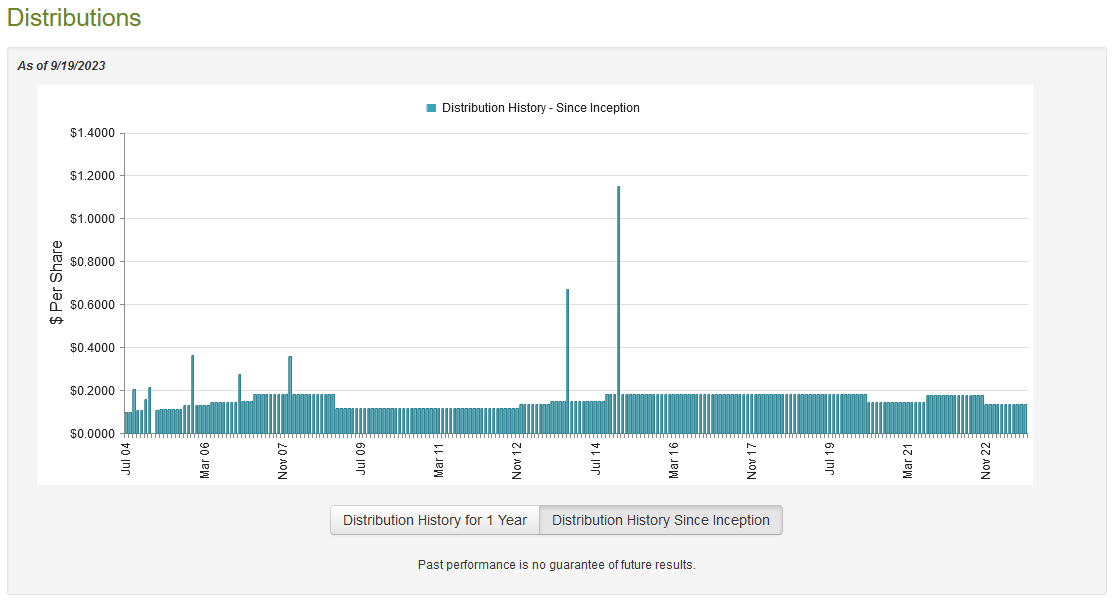

This is certainly the case. As of the time of writing, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund pays a monthly distribution of $0.1374 per share ($1.6488 per share annually), which gives it a 7.40% yield at the current share price. Unfortunately, the fund has not been especially consistent with respect to its distribution over time, but it has done a better job than many other closed-end funds. We can see that here:

{kind=link}

As we can see, the fund was able to boost its distribution in response to the market euphoria that followed the reopening of the economy following the COVID-19 pandemic. This is not exactly surprising, since that was a period of time in which governments all over the world had printed an enormous amount of money, so it was remarkably easy to make an investment profit. It had to cut the distribution back in November 2022 though, which was most likely because raising interest rates domestically and abroad drove down the value of most market assets. The fact that the fund had good reasons to cut the distribution does not necessarily mean that investors will understand though, and the recent distribution cut may still prove to be something of a turn-off for any investor that is seeking a safe and secure source of income to use to pay their bills or otherwise finance their lifestyles.

As I have pointed out numerous times though, the fund's past is not necessarily the most important thing for anyone that is buying the fund today. After all, a new buyer will receive the current distribution at the current yield and will not be especially affected by the actions that the fund has had to take in the past. Let us investigate how sustainable the fund's current distribution is likely to be.

Fortunately, we do have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. The market was generally fairly optimistic during the first few months of this year, which was a stark departure from the relatively sour sentiment that existed throughout most of 2022. As such, the market strength that we saw here could have given the fund some opportunity to make capital gains profits. This document should also provide us with some insight regarding the sustainability of the distribution at its new lower level.

During the six-month period, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund received $9,046,608 in dividends along with $2,024,448 in interest from the assets in its portfolio. This gives the fund a total investment income of $11,071,056 during the six-month period. The fund paid its expenses out of this amount, which left it with $6,087,152 available for shareholders. As might be expected, this was nowhere close to enough to cover the $13,510,381 that the fund actually paid out in distributions during the period. At first glance, this could be concerning as the fund's net investment income is nowhere close to enough to cover its distribution.

However, this fund does have other mechanisms through which it can obtain the money that it requires to cover its distribution. For example, it might be able to generate some realized capital gains that could then be paid out to the investors. Fortunately, it had a great deal of success in this endeavor during the period in question. The Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund reported net realized gains of $10,145,289 and had another $34,150,676 in net unrealized gains. This was more than sufficient to cover the distributions when combined with net investment income. Overall, the fund's net assets went up by $36,872,736 during the period after accounting for all inflows and outflows. Unless the fund has recently suffered massive losses, which seems unlikely, its distribution should be fairly sustainable for the remainder of the year at a minimum.

Valuation

As of September 19, 2023 (the most recent date for which data is currently available), the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has a net asset value of $24.61 per share but the shares only trade for $22.25 each. This gives the fund's shares a 9.59% discount on net asset value at the current price. This is a very reasonable discount that is a bit better than the 8.67% discount that the shares have had on average over the past month. Thus, the current price certainly seems to be acceptable.

Conclusion

In conclusion, the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund has been underperforming the broader market over the past few months, which is disappointing. It is difficult to figure out why this would be the case though, other than today's interest rates reducing the appeal of high-yielding risk assets.

We can see that the fund's portfolio has performed somewhat better than its shares though, so that could be a contributor to the underperformance. The fund's portfolio actually looks decent, as, despite my complaints about the high allocation that Eaton Vance funds tend to have to the technology sector, this one is actually underweighted to that sector. The fund's 7.40% distribution yield appears to be sustainable right now and it is trading at a very attractive valuation. Overall, there seems to be a lot to like here, except for the relative underperformance.

For further details see:

ETO: Underperforming Recently, But A Decent Fund