ETSY - Etsy At 15x Forward Earnings Entry: The Bull And Bear Cases

2023-11-28 15:12:04 ET

Summary

- Etsy's Q3 results have both positive and negative aspects, but the time to be bearish on the stock has passed.

- The company faces challenges in a competitive e-commerce market and needs to address consumer perceptions about its products.

- Etsy's increasing take rate and declining gross merchandise sales raise concerns about its appeal to sellers, but its profitability justifies its valuation.

Investment Thesis

Etsy, Inc. ( ETSY ) delivered Q3 results that have a lot of nuance. There's plenty for bears to latch onto, as we'll soon discuss. But my argument when it comes to Etsy is that the time to be bearish on this stock has come and gone.

Ultimately, I declare that paying 15x forward earnings is not a stretched valuation whatsoever. Yes, there are some pesky detractions to the bull case, such as its lackluster growth rates. But even considering those detractions to the bull case, I still believe there's a positive risk-reward to this name.

Rapid Recap

In my previous analysis back in September , I said:

[Here] you'll see ample reason to ascertain that including some pesky detractions to the bull case, there are a lot more positives than its share price performance would lead you to believe is warranted.

Then, I went on to highlight the following:

Yes, there was a time in the recent past when it made sense to be bearish on Etsy. I fully recognize that aspect, as I too was bearish, see here .

ETSY Michael Wiggins De Oliveira

But I believe that since then, Etsy has made some progress in improving its prospects, and the stock has started to gain some footing. Here's the performance since my previous analysis.

ETSY Michael Wiggins De Oliveira

To be honest, my timing wasn't perfect, as I first turned bullish on Etsy in June at $91 per share . However, I was clearly right to remove my sell rating on the stock.

To sum it up, I believe that this is a good time to average into Etsy. Even if I'm upfront in stating that this isn't a blemish-free thesis, investors should brace themselves for a potentially bumpy road ahead.

Etsy's Near-Term Prospects

Etsy is an e-commerce platform that focuses on handmade, vintage, and unique goods. It provides a marketplace where independent sellers, often artisans and crafters, can showcase and sell their items.

Buyers can browse a wide range of products that are not typically mass-produced, fostering a marketplace for distinctive and personalized items.

As you know, Etsy doesn't have a large moat, and it is not immune to the macroeconomic environment. This challenging economic backdrop is likely to influence consumer spending behavior, particularly in the realm of non-durable discretionary goods, where Etsy primarily operates.

Moreover, competitive pressures in the e-commerce advertising space pose a notable challenge. The rapid growth of new entrants, such as Temu of PDD Holdings ( PDD ), has led to increased advertising costs. The aggressive spending by these competitors, coupled with uncertainties about their adherence to ROI thresholds, contributes to an elevated cost of advertising. As a result, Etsy must navigate this dynamic landscape strategically to ensure its marketing investments are both effective and efficient.

Additionally, the competitive environment is marked by evolving consumer perceptions. Despite Etsy's efforts to disrupt misconceptions about its offerings, there remains a need to address the prevalent notion that its products might be more expensive. This points to a challenge in terms of altering consumer perceptions and broadening the understanding of Etsy's value proposition, particularly in a market saturated with diverse e-commerce options.

Moving on, back in Q4 2022 Etsy's take rate was 20.0%. While for Q4 of this year, its take rate is guided to reach 20.8%. Even though this figure is down marginally from the 20.9% reported in Q3 2023, down 10 basis points sequentially, the fact remains that there's an 80 basis point increase in the take rate y/y, which clearly indicates an increase in squeezing merchants.

And this is where I believe the bull case finds a crucial blemish. Etsy is increasing its take rate even as its gross merchandise sales (''GMS'') are expected to trickle lower y/y by mid-single digit.

To put this more concretely, Etsy is squeezing its sellers even as the dollar volume of merchandise through its platform is expected to be slightly down in the all-important Q4 quarter.

I find it difficult to imagine that this is a winning proposition and an attractive force for merchants to double down their efforts and grow their business on Etsy when the platform is not aligned with the sellers. So, this is something to keep an eye on.

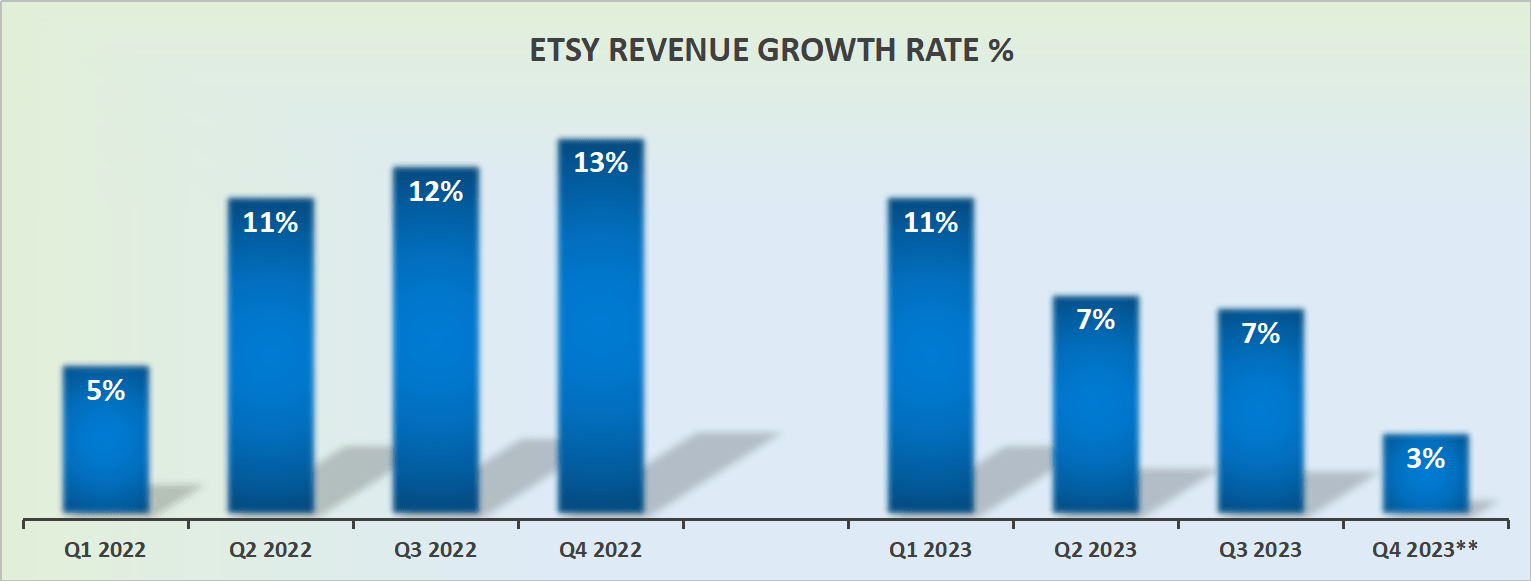

Revenue Growth Rates Don't Inspire Much Hope, But...

{kind=link}

Here's my critical contention: Investing is all about expectations. Expectations of the company's future prospects. When investors appraise Etsy, there's really very little to be enthused over.

After all, who is going to be willing and eager to pay a large multiple for a company that is struggling to grow its revenues at double digits y/y? Few investors will.

And as a consequence, its valuation has already factored this in. We'll soon turn to discuss its valuation, but before that, allow me to make this observation.

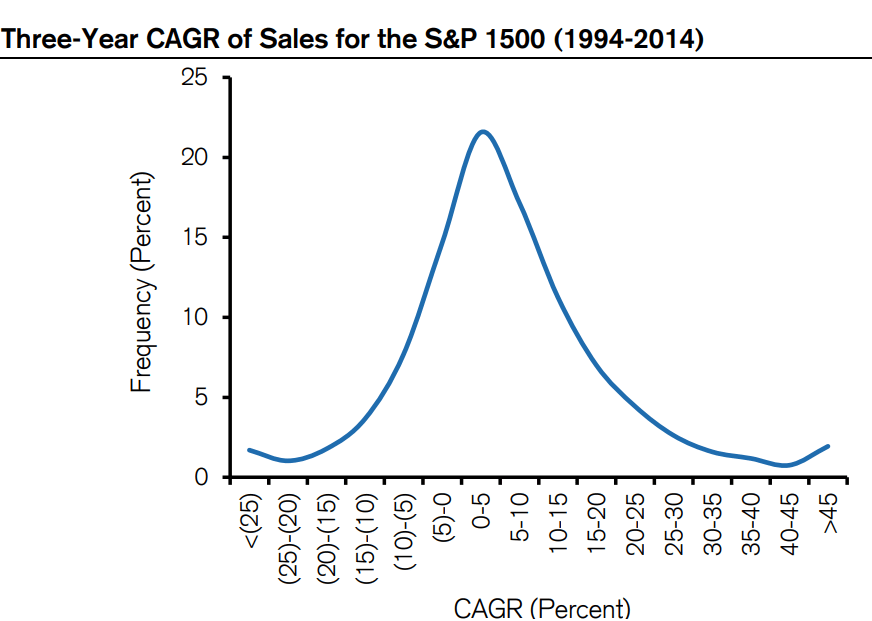

A company can grow at single-digit growth rates for a really long time. In fact, it's really easy for a company to grow in the single digits for a long period of time, rather than sustaining high growth rates for more than 5 years.

{kind=link}

Michael Mauboussin's Base Rate book is slightly outdated, but it nevertheless spans an important 20-year period that includes 2008. The results show that delivering low rates of return happens frequently, but delivering what investors truly covet, namely high growth rates for prolonged periods, happens infrequently.

Simply put, our odds of investing are much better if we understand what investors are pricing in , relative to what the underlying potential for the company could be.

ETSY Stock Valuation -15x Forward P/E

As you can see above, investors have already significantly reduced their expectations for ETSY. Could this multiple compress further? Yes, it absolutely could. How much?

Of course, that depends on a lot of factors, such as an unexpected increase in interest rates or a deterioration of its underlying prospects.

But at the same time, it's difficult to imagine a business that's growing its profitability by around 5% y/y, seeing its multiple compress towards less than 10x its EPS.

{kind=link}

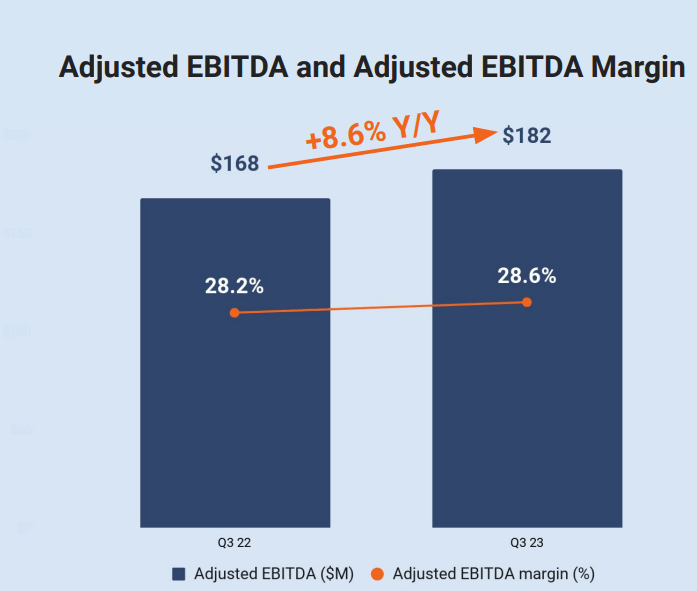

As you can see here, the business is not only highly profitable, with 2023 expected to see about $700 million of EBITDA, but there's the potential for 2024 to deliver some profitable growth on top of that.

On the other hand, Etsy does carry a significant amount of debt. More concretely, Etsy carries roughly $1.5 billion of net debt. So, although Etsy is highly profitable, it also has a restrictive balance sheet that needs to be addressed and will inhibit full flexibility in further capital allocation decisions.

The Bottom Line

In conclusion, my take on Etsy's investment thesis presents a nuanced picture.

Despite facing challenges such as modest growth rates and intensified competition, I find the proposition of paying 15x forward earnings justified.

Recognizing Etsy's strides, I'm mindful of near-term concerns, notably influenced by the economic climate and ample competition.

A crucial observation is Etsy's rising take rate amid a dip in gross merchandise sales, potentially impacting its appeal to sellers.

While noting its uninspiring revenue growth rates, the 15x forward P/E seems fair given the company's profitability. I advocate caution due to significant net debt, yet I believe that entering at this valuation offers a positive risk-reward balance.

For further details see:

Etsy At 15x Forward Earnings Entry: The Bull And Bear Cases