ETSY - Etsy: Revenue Growth Seems To Slow Down Too Much To Support The Valuation

2024-01-07 23:40:42 ET

Summary

- Etsy's financials show uncertain revenue growth and potential margin issues, leading to a hold rating.

- The company has manageable debt levels but needs to improve solvency metrics.

- Revenues have been growing but analysts predict slower growth in the future, raising concerns about the company's outlook.

Investment Thesis

At the end of February, Etsy ( ETSY ) is going to report its FY23 results. I wanted to take a look at the company´s financials to see if it’s a good time to start a small position. With uncertain revenue growth and not enough information to be certain that margins have recovered, I assign the company a hold rating as the fair value is much lower than where the company is trading at currently.

Financials

As of Q3 ´23 , the company had around $977m in cash and equivalents against $2.3B in long-term debt. Investors tend to avoid companies with excessive leverage on the books, which limits their potential to find a company that may outperform. Debt is not bad as long as it is handled correctly and is manageable. I look at a few metrics to determine whether the management is being smart by complementing their day-to-day operations with debt.

Firstly, ETSY´s debt-to-assets ratio has been in the acceptable range for most of the time, however, with the recent bad performance in FY22, that has worsened but is still decent. Anything under 0.6 I consider to be not too heavily leveraged. In FY22, this has crossed that threshold and as of 9 months ended September ´23, it´s gotten to .93, so it is pushing what I believe to be acceptable. The company´s debt-equity ratio has experienced a similar demise as D/A. Shareholder equity turned negative in FY22 due to the massive losses and an increase in AOCI, which was due to adjustments in foreign currency and unrealized gains/losses on long-term corporate bonds and U.S. government securities. Due to all this, the D/E ratio turned negative for FY22 and is even more negative as of Q3 ´23.

Lastly, I like to see if the company can manage to meet its annual debt obligations, which is the annual interest expense on debt. This metric has been great over the years and continues to be great as of Q3 ´23. Many analysts consider a ratio of 2x to be healthy, while I prefer to see at least a 5x, which allows for bad years of performance as we saw in FY22, where the company´s EBIT was still decent and easily covered interest expense, especially when accounting for interest income that the company received. So, one out of the three solvency metrics passes with flying colors while the rest are a bit shaky, therefore, I will have to add more margin of safety when looking at the company´s intrinsic value.

{kind=link}

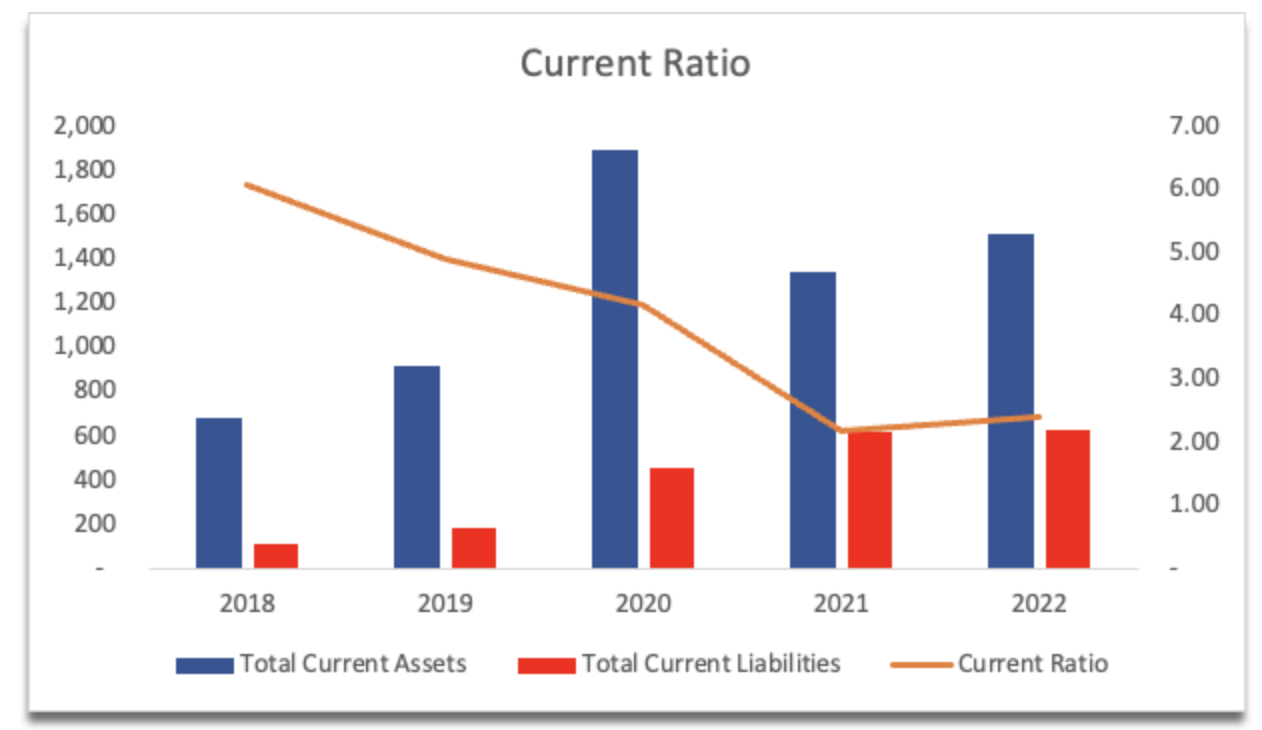

The company´s current ratio has been outstanding all these years, and the only gripe I would have with it is that it may be a bit too high, which makes it a little inefficient. However, it has been coming down, which means the company is being a lot more efficient with its assets than previously. As of the latest quarter, the ratio stood at around 2.4, which is slightly above what I consider to be an efficient ratio range of 1.5-2.0. It is better to have a high current ratio than under 1, as that way at least the company can cover its short-term obligations with ease, while still having enough capital to further the growth of the company. It´s safe to say the company has no liquidity problems or is at risk of insolvency.

{kind=link}

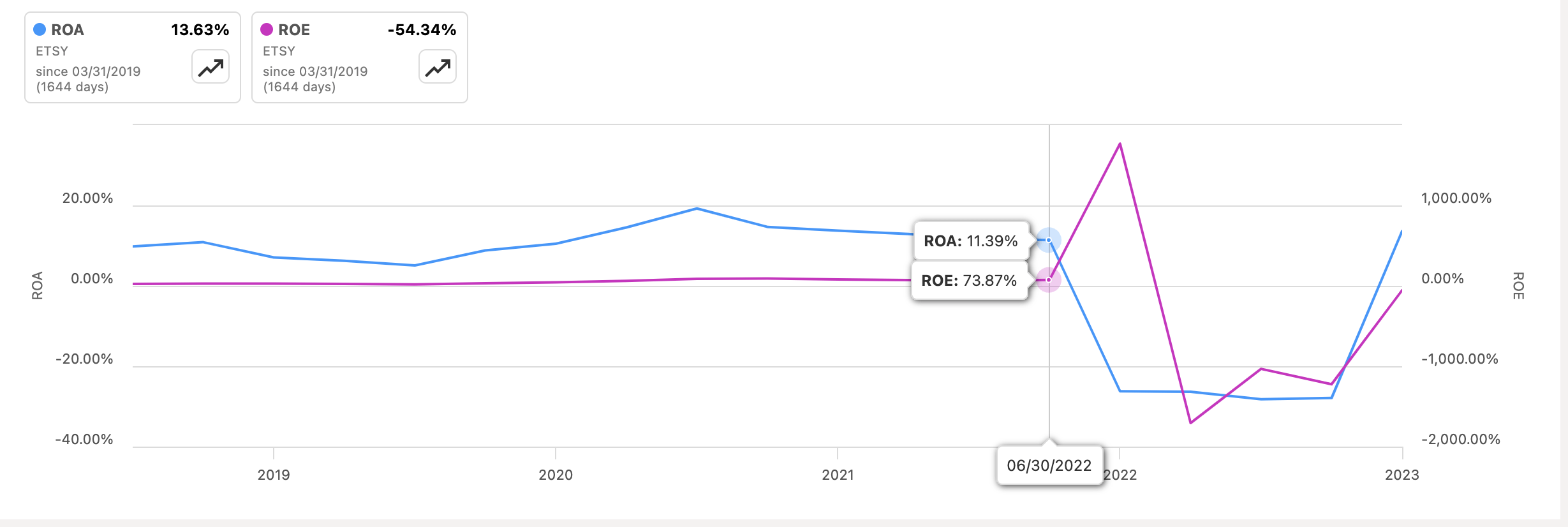

In terms of efficiency and profitability, we know that FY22 was a bad year due to the company taking an impairment charge of around $1B for the acquisitions of Depop and Elo7. We can see that this was reflected in the company´s ROA and ROE metrics. Before that year, the company´s efficiency and profitability were climbing and seemed to be bouncing off the lows recently. Can this be sustained, it is hard to tell, but so far, I don’t think the company will recover until 2025.

{kind=link}

The company´s ROTC has been fluctuating a lot over the years, which is not ideal, however, it has been quite steady over the last few years and is over my minimum of 10%, which tells me the company does have some sort of a decent moat and a competitive advantage. Compared to the competition, there are quite a few of them, however, not many are public companies, and some bigger ones are not very close competitors due to their market size and other business segments. Below are the closest I found in my opinion.

{kind=link}

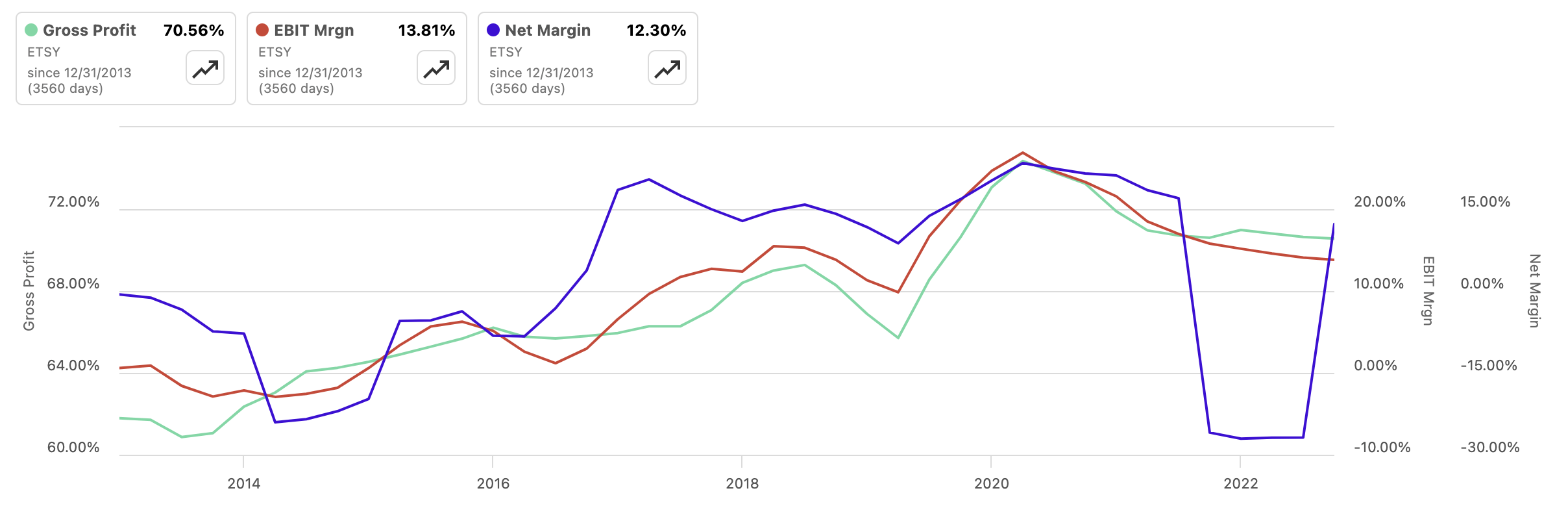

In terms of margins, before the disastrous performance of FY22, these have been steadily increasing and seem to have bottomed out so far and are positive yet again. A better macroeconomic environment has made the company profitable yet again. The question is if it is going to be sustained going forward, as the environment is anything but predictable or certain.}

{kind=link}

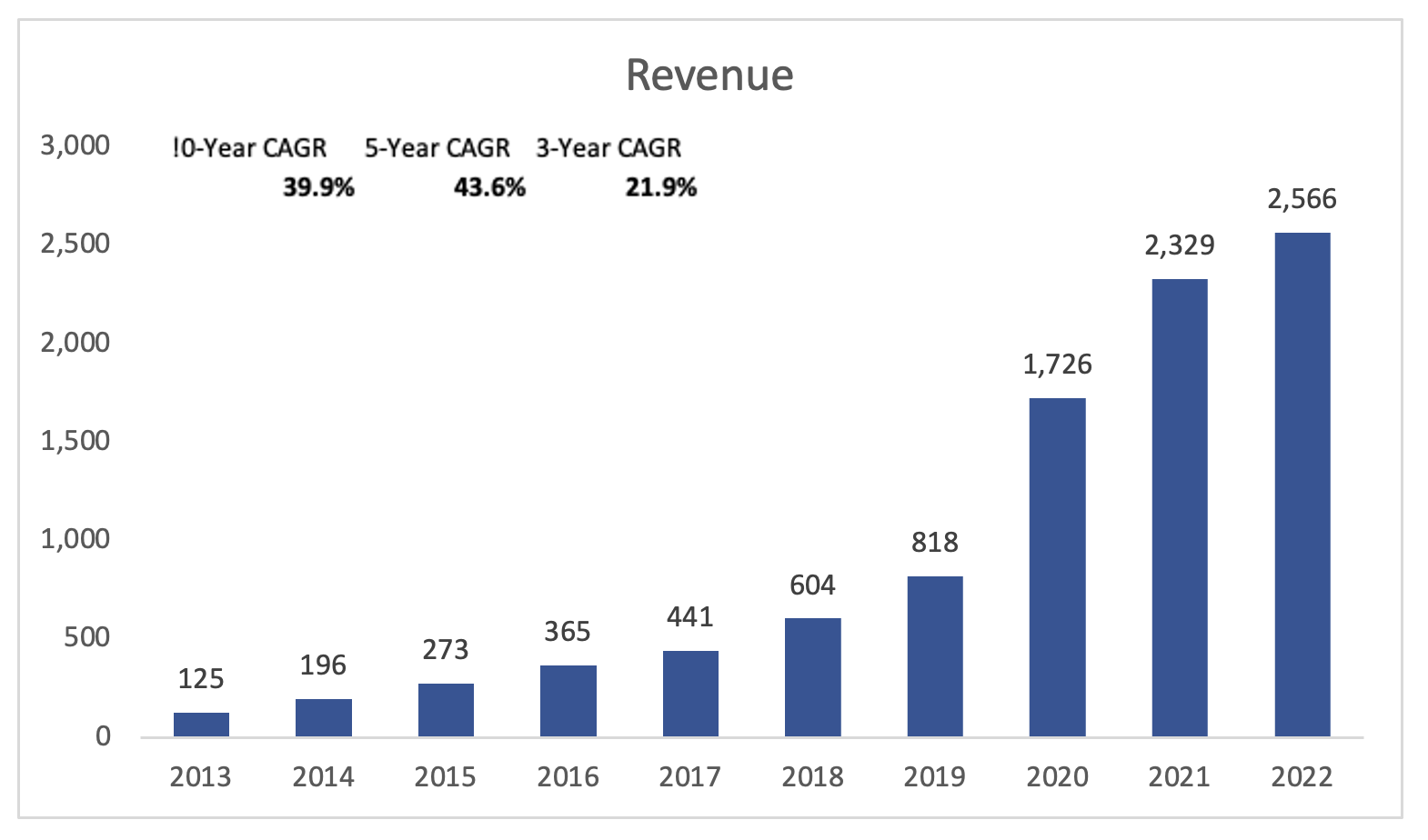

Revenues have been growing at an extraordinary pace over the last decade, so I was very surprised to see how low the analysts’ estimates are for the upcoming years. The company managed to grow at decent CAGRs over the last decade, but analysts are not even predicting the company will be able to grow at low-double-digits, which is worrying. To be honest, I take analysts' estimates for the past one year with a grain of salt, since it is all educated guesses at best, which is what I will be doing in the later section of the article.

{kind=link}

Overall, I see a company that was doing rather well and will continue to do well as I don’t expect another goodwill impairment of around $1B as it happened in FY22. Unless the company decides to write off some more impairment charges in the future, which are not easy to predict.

Comments on the Outlook

I would like to see massive improvements in the company´s gross merchandise sales, which reflects the total value of goods transacted on the platform. The latest figures showed a decrease of 1.4% y/y, which is not what I would like to see from a company that used to grow at impressive rates.

The overall macroeconomic situation is not going to be particularly favorable for Etsy or many other companies too. The sticky inflation and high interest rates for longer will weigh on the consumer for much longer than anticipated. A couple of weeks back people thought that the FED would be cutting rates as early as March, but after a couple of news that showed that the US economy is still hot, those hopes have dwindled. I would like to see the management taking care of the margins. I would like to see how these develop over the next couple of quarters, and how the management is going to navigate the rest of the uncertainty and volatility.

Valuation

I like to approach my valuation models with a conservative mindset. I usually lowball revenue assumptions to give myself an extra margin of safety, and I will not be changing my approach for ETSY either, even though the company grew at an outstanding rate in the previous years. It´s just the FY23 numbers are not up to par with the past, and I cannot speculate if the growth is going to return in the future without seeing the results already. To cover my basis, I also included a conservative and an optimistic case. Below are those assumptions and their respective CAGRs.

{kind=link}

In terms of margins and EPS, I went with the company´s adjusted metrics, as that one the company deems the "true value". I also went with these numbers to give the company a fighting chance when it comes to intrinsic value calculation to be anywhere near the company´s share price, as you´ll see later on. Below are those assumptions. You´ll see that in FY26 the numbers get worse, it's because my model includes the company starting to pay taxes, which it had not done so in a while, if ever.

{kind=link}

For the DCF model, I also went with a slightly adjusted company´s WACC. The company´s beta exploded in 2022, to around 2, but if we look at the past decade, it averaged around 1, so I reduced it to around 1.5 as I don't think a beta of 2 is going to be sustainable for long. The volatility has to come down, which will drive down the company´s beta too. Additionally, I went with a 2.5% terminal growth rate, as I would like the company to grow at least as much as the inflation target in the U.S.

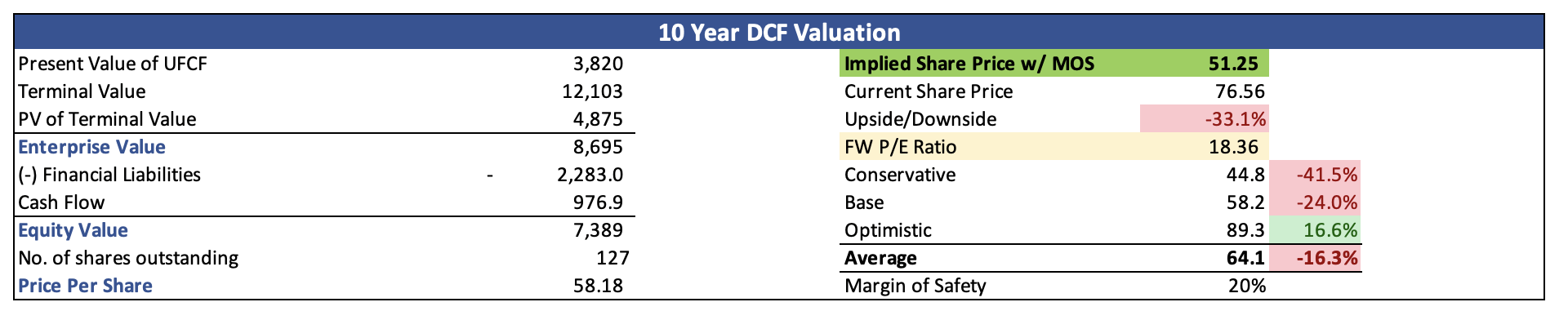

Furthermore, I also added a 20% margin of safety to the intrinsic value calculation, just to give myself even more room for error. With that said, the company´s intrinsic value, and what I would be willing to pay to take on the company´s risks, is around $51 a share, which means the company is trading at a high premium to its fair price.

{kind=link}

Closing Comments

I would like to see the share price coming down much more before I consider the company a safe investment with very little downside. Currently, it is not a good time to start a position as the risks are too high, the company is very volatile, and the revenue growth is not there. I would like to see top-line growth returning and margins continue to improve as it has in the past, however, this will take time and I don't think we have seen the bottom yet, and I wouldn't be surprised if the company comes down to around $50 a share in the next year or so. The company was just at $60 a share just in November, and with such a shaky macroenvironment where good news is bad news, I wouldn't be surprised if my price alert is going to hit within the next year or so. When and if it does hit, I will revisit my thesis and see if nothing changed for the worse, and if it is just broad market noise and the company´s financials are solid, I would be looking at opening a small position.

For further details see:

Etsy: Revenue Growth Seems To Slow Down Too Much To Support The Valuation