ETSY - Etsy: Rocky GMS Trends Offset By Strong Profitability (Ratings Upgrade)

2023-11-29 07:42:37 ET

Summary

- Etsy's stock has declined over 30% this year due to weakened consumer spending and higher inflation.

- Despite rocky trends in gross merchandise sales (GMS), there are upside drivers such as high profit margins and new buyer additions.

- Etsy's valuation multiples suggest potential short-term upside, with a price target of $88 representing a 17% increase from current levels.

- The best move here is a short-term trade, as unclear top-line trends make a long-term investment untenable.

Once a pandemic favorite stock as consumers hoarded collectibles on the internet, Etsy (ETSY) has lost a lot of its shine this year as consumer spending weakened on the back of higher inflation. Year to date, the stock is down more than 30%, at one point slicing in half upon hitting a YTD low at $60.

I put Etsy back on my watch list in August when the stock was trading north of $80 per share, issuing a neutral opinion at the time and citing a buy point below $70. Now that the stock has dipped to the $60s and rebounded post-earnings, however, I think there is short-term upside to chase here. I'm cautiously optimistic on Etsy and am now bullish on the name.

Now, that recommendation comes with several caveats. First - I don't think Etsy has an easy path back up to the $120s, and I do think any upside is more short-term and capped in nature. That's largely because Etsy's GMS (the sum total of all sales conducted on the platform) continues to undergo rocky trends as the company battles weaker shopper behavior. That being said, however, there are a number of upside drivers to counterbalance the company's rocky GMS trends:

- Rich profit margins. Etsy regularly posts adjusted EBITDA margins nearing 30%, which is a nice concession for a company whose top-line growth has slowed to the single digits.

- New buyer trends still remain well above pre-pandemic levels. Though certainly a niche site, Etsy continues to draw a following, with ~6 million net-new active buyers added per quarter. Reactivated buyers are also high, allowing Etsy to shift the focus of its marketing spend to retention rather than new customer acquisitions.

- Seller fees are still below the competition. Though Etsy seller fee increases trigger immediate ire, it must be noted that Etsy's 7.5% fee is still less than eBay, Amazon, and Poshmark. Fees for these sites vary by category, but generally average around ~10% or more of final sales prices.

From a valuation perspective: at current share prices near $75, Etsy trades at a market cap of $8.96 billion. After we net off the $1.05 billion of cash and $2.28 billion of debt on Etsy's most recent balance sheet, the company's resulting enterprise value is $10.19 billion.

Meanwhile, for next fiscal year FY24, Wall Street analysts are expecting Etsy to post $2.61 in pro forma EPS (+8% y/y) on $2.89 billion of revenue, up 6% y/y. And if we assume Etsy holds its current ~27% adjusted EBITDA margin next year, adjusted EBITDA would be roughly $780 million. This puts Etsy's valuation multiples at:

- 3.5x EV/FY24 revenue

- 13.1x EV/FY24 adjusted EBITDA

- 29x forward P/E

The best move here: Etsy is a buy in the mid-$70s, but don't get greedy and let go of the stock when it hits a 15x FY24 adjusted EBITDA multiple - representing a price target of $88 and ~17% upside from current levels.

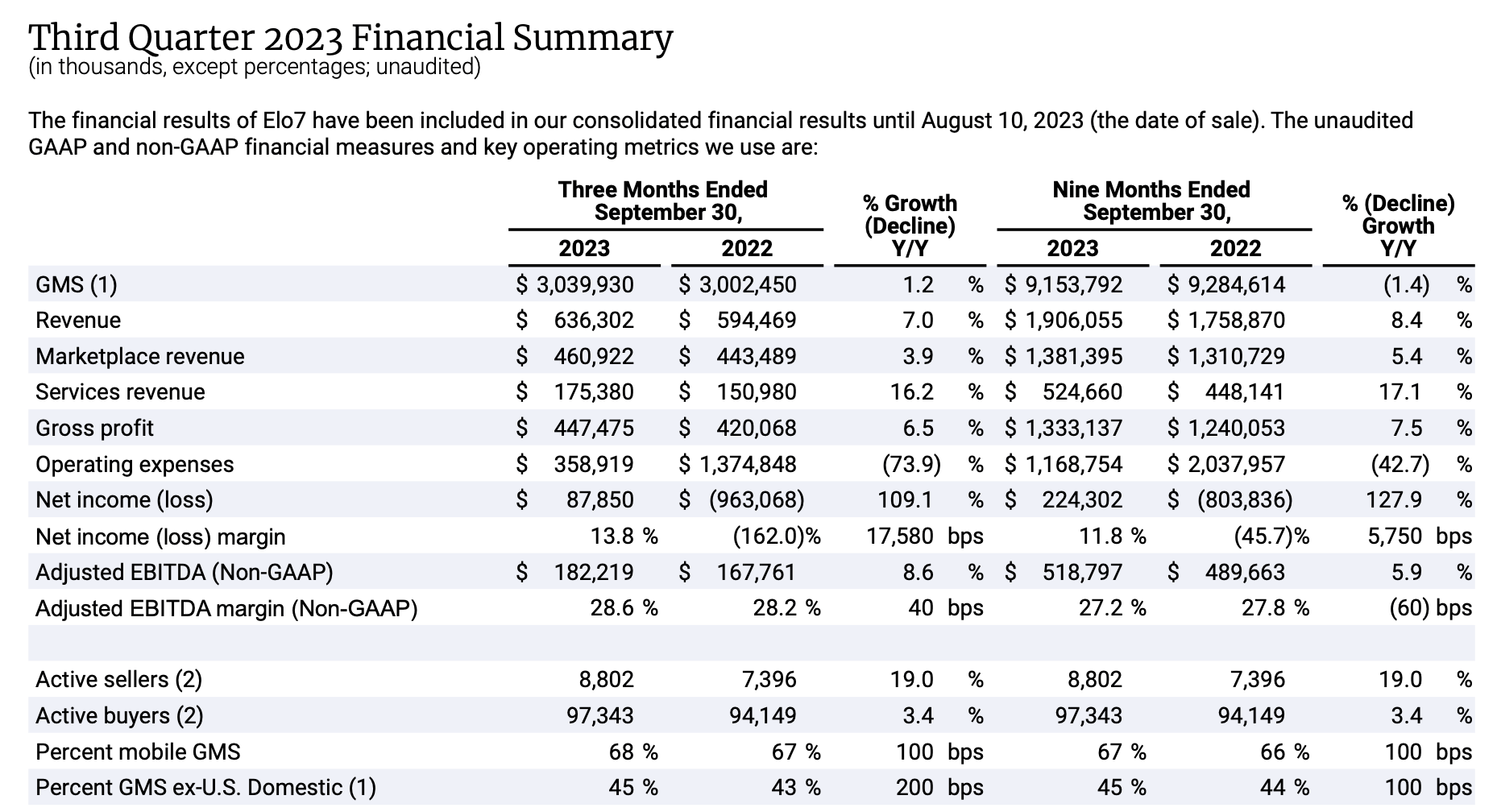

Q3 download

Let's now go through Etsy's latest Q3 results in greater detail. The Q3 earnings highlights are shown in the table below:

{kind=link}

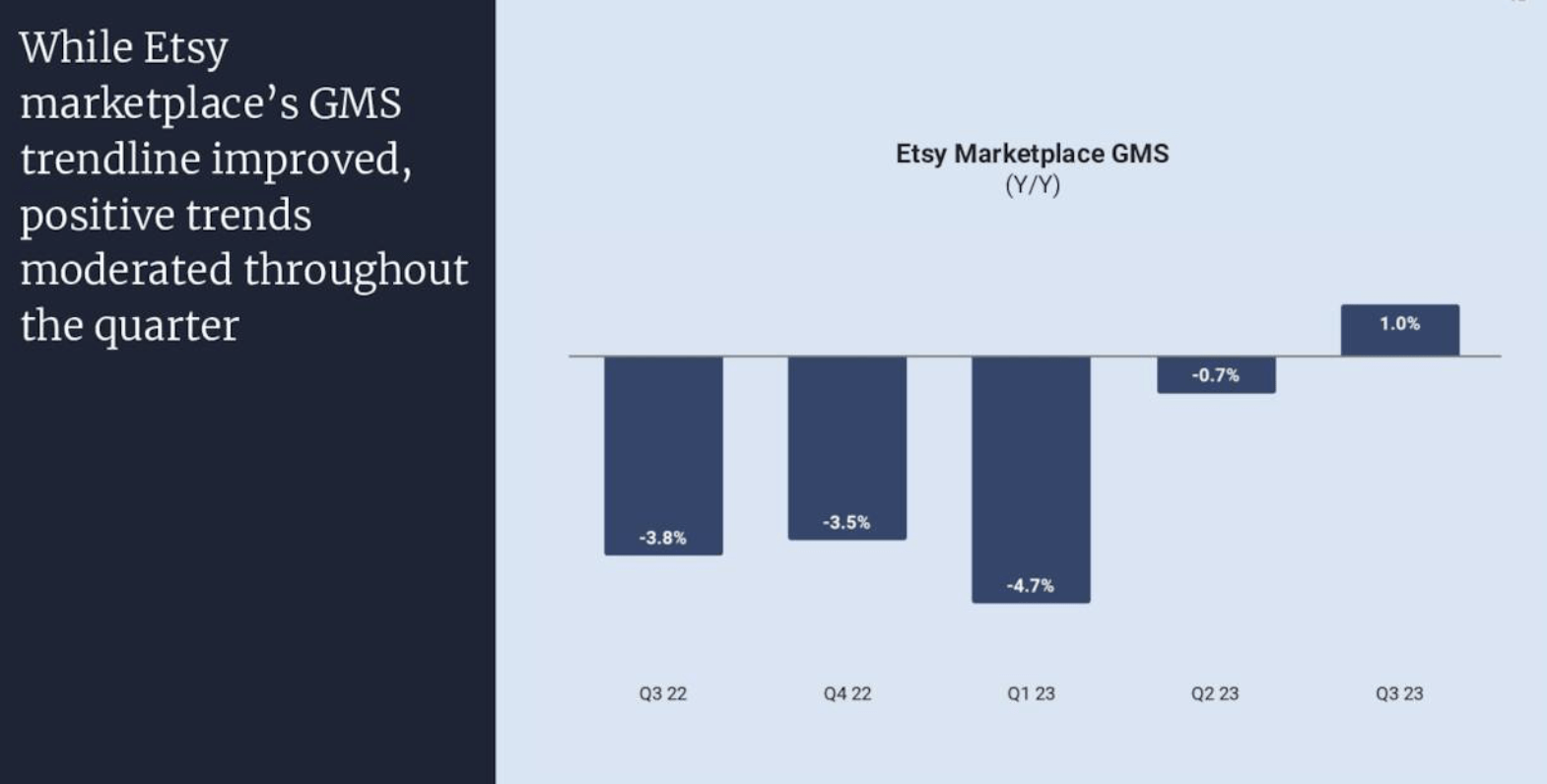

The key thing here to note: GMS re-accelerated to 1.2% y/y growth to $3.04 billion, reversing a multi-quarter declining trend. As shown in the chart below, this is 170bps better sequentially than Q2, which in turn was four points better than Q1:

{kind=link}

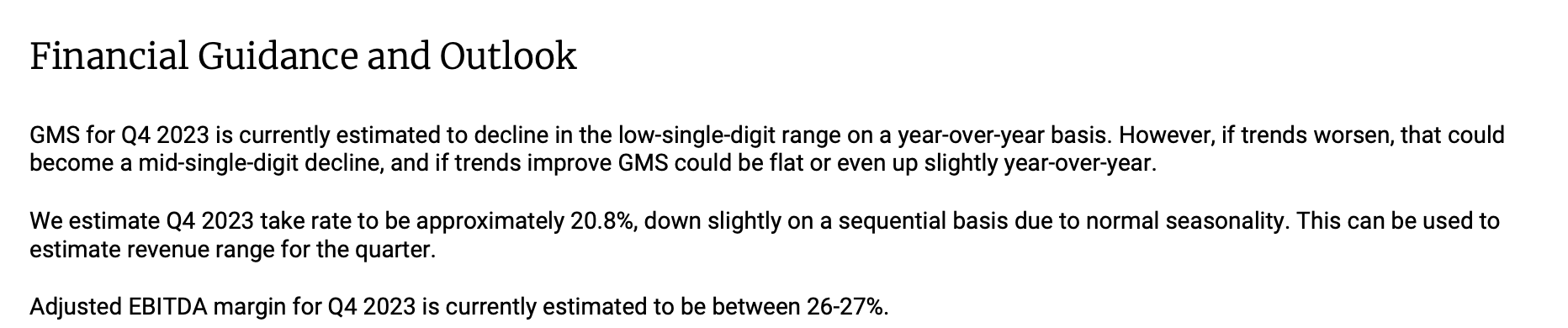

There is room for caution, however. The company noted that the strong trends that it saw within Q3 began to moderate in the back half of the quarter, which is leading to a Q4 outlook that calls for GMS to decline in the low single digits, essentially reverting back to Q4-Q1 levels (and against arguably easy comps that declined in the prior year period):

{kind=link}

Per CEO Josh Silverman's remarks on the Q3 earnings call regarding buyer trends:

As you all know, there's been significant pressure on consumer discretionary product spending, as high inflation, elevated interest in mortgage rates, splurges on experiences, and declining savings balances have meant that there's little leftover for many consumers after paying for food, gas, rent, and child care.

These issues are magnified for lower-income buyers, and we feel the impact on the Etsy marketplace. We're also experiencing an increasingly competitive retail environment with a very heavy emphasis on deep discounting and in some cases competitors investing it potentially unsustainable levels in marketing and promotions. While the headwinds we're facing at this moment in the cycle are undeniable, I'm pleased that once again performance green shoots for the Etsy marketplace were evident in the third quarter."

The company has been stepping on the promotional gas to try to lift GMS results. In September, the company kicked off an Etsy-funded "Get $5 off" promotion on any purchase greater than $25, which it noted led to a surge in reactivated buyers. The company additionally noted that seller-driven sales and coupons drove an additional $100 million of incremental GMS in the quarter.

Revenue, meanwhile, grew 7% y/y to $636.3 million, slightly ahead of Wall Street's $630.4 million (+6% y/y) expectations.

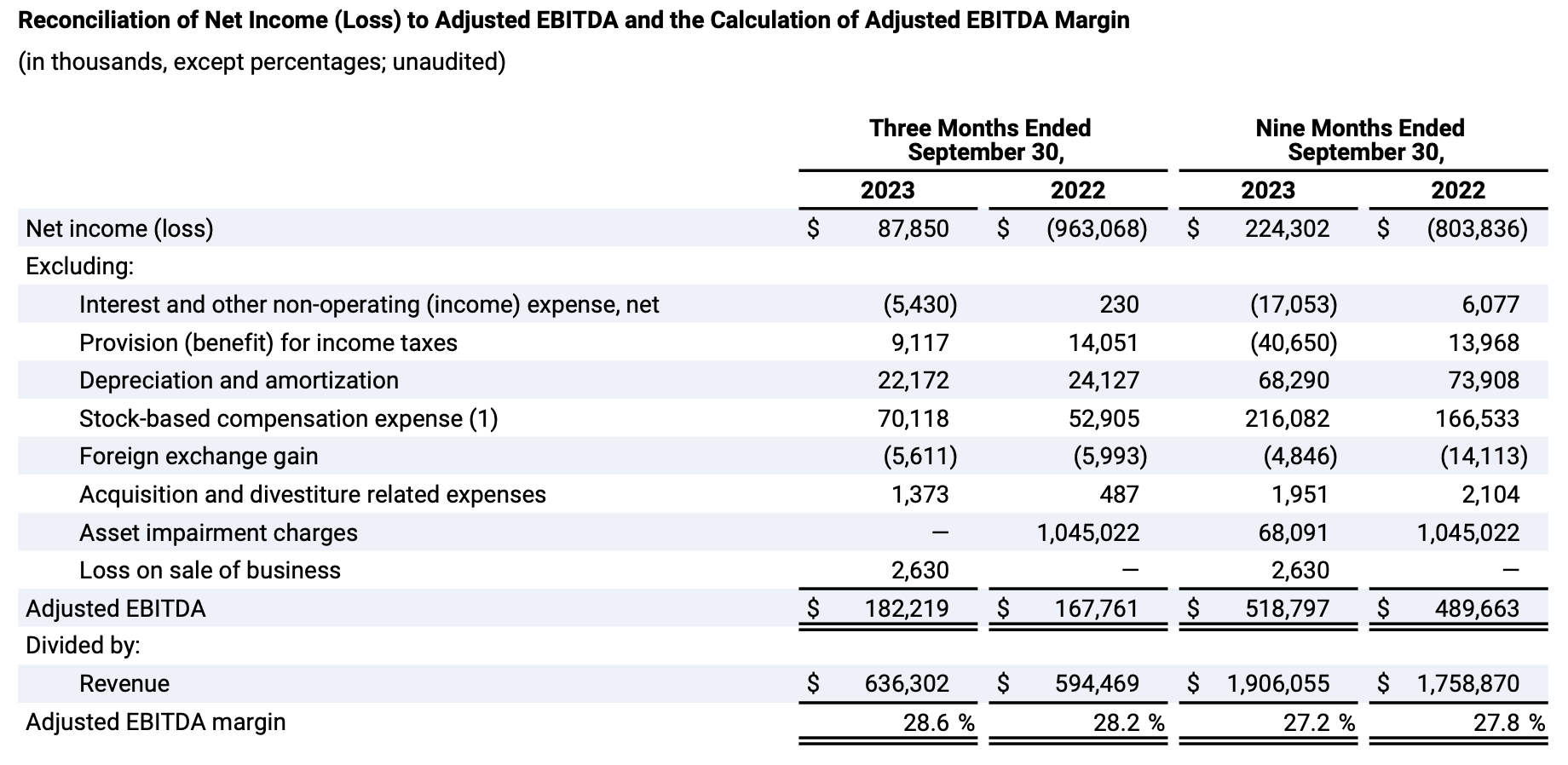

Adjusted EBITDA also rose 9% y/y to $182.2 million, reflecting a 28.6% adjusted EBITDA margin - 40bps richer than the year-ago period, and in spite of the "Get $5" promotion this quarter.

{kind=link}

Deeper attempts by the company to solve declining GMS trends through Etsy-funded promotions may start to claw away at the company's hard-earned margin gains, though I'd argue at this juncture that growth and winning over new buyers takes precedence over short-term profits.

Key takeaways

As mentioned upfront, I see a limited opportunity for a short-term trade in Etsy as the company temporarily rallies off the back of stronger Q3 GMS results (though be cautious as the company has warned trends will soften in Q4). Don't get greedy, however; and sell before $90.

For further details see:

Etsy: Rocky GMS Trends Offset By Strong Profitability (Ratings Upgrade)