EXD - ETV: Attractive Fund For The Long-Term

2023-04-17 14:55:39 ET

Summary

- ETV's premium had collapsed after they cut their distribution last year, the first time in nearly a decade.

- Given the depressed prices in tech in 2022, it seemed fitting to adjust the distribution as this is a tech-heavy fund.

- The distribution yield remains attractive, and if we see some stabilization, it should be sustainable.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 2nd, 2023.

Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ) continues to be penalized for the distribution cut they put into place last year. After a sharp decline in the premium, there was a bit of a bounce back into premium territory before the latest volatility seems to have pressured it back lower. That said, one of the big beneficiaries of the latest volatility is growth and primarily the mega-cap tech stocks.

This is because if interest rates aren't expected to go as high anymore after the bank collapses, these become more attractive investments. In fact, if the Fed cuts rates sooner than anticipated due to cracks starting to show and a continuation of the trend of lower inflation, that could be seen as even better for tech stocks.

Since our last update, the fund's merger with Eaton Vance Tax-Managed Buy-Write Strategy Fund ( EXD ) was approved, and that will close on April 14th, 2023. Stanford Chemist wrote up more about the merger. Overall the implication of this move isn't overly noteworthy for ETV as EXD is such a small fund. The total managed assets won't move too much, and since these are identical funds, nothing will be moved over that is out of the ordinary for ETV to hold.

Additionally, since our last update , ETV's performance has been basically flat. On a total return basis, we see some returns by factoring in the distributions paid during this time. That was after we started to see gains early on in 2023, before the latest bank collapses brought about more volatility once again.

ETV Performance Since Prior Update (Seeking Alpha)

While I believe the fund remains attractive for a long-term investor, and the premium isn't too excessive, I would continue to believe this position is more of a hold than a buy at this time. I think that if we can get a discount on this fund, it would be a much more appealing position to consider adding more aggressively. A discount has been incredibly rare for this fund in the last decade, but with the distribution cut, investors are likely more hesitant to jump back in.

The Basics

- 1-Year Z-score: -1.49

- Premium: 0.56%

- Distribution Yield: 9.04%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $1.3 billion

- Structure: Perpetual

ETV's investment objective is to "provide current income and gains, with a secondary objective of capital appreciation." To achieve this, the fund will invest "in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to seek to generate current earnings from the option premium."

The fund is roughly $1.3 billion in managed assets, and that will climb to around $90 million more when EXD is merged into the fund. That gives us a sense of the immense size difference between these funds and why EXD going into ETV isn't likely going to change much.

Call-Writing Strategy And Tax Implications

ETV utilizes a call-writing strategy where they write calls against indexes rather than underlying holdings. That can have the impact of producing losses if the indexes are rallying because these are cash-settled contracts. One can't own an underlying index directly. However, due to holding positions that align with the underlying indexes, the theoretically infinite loss should be contained due to this offset.

Where it can benefit the fund is the fund's tax classifications. I've discussed this before, but I'll briefly touch on it again. It's part of why this fund is "tax-advantaged," so it is an integral part of the fund and why investors choose to invest in this fund.

When you have losses you are generating, that can lead to return of capital distributions since the losses offset the gains or, if they don't realize any gains, only shows losses. That's when ROC distributions can show up. For ETV, this is a fairly regular occurrence too. They've succeeded at this strategy of generating losses for the ROC classifications while not seeing massive losses in their NAV. Some of their sister funds, primarily the global-focused funds, have struggled more with this. That's mostly to be expected, though, as most of the last decade saw U.S. stocks outperforming their international counterparts.

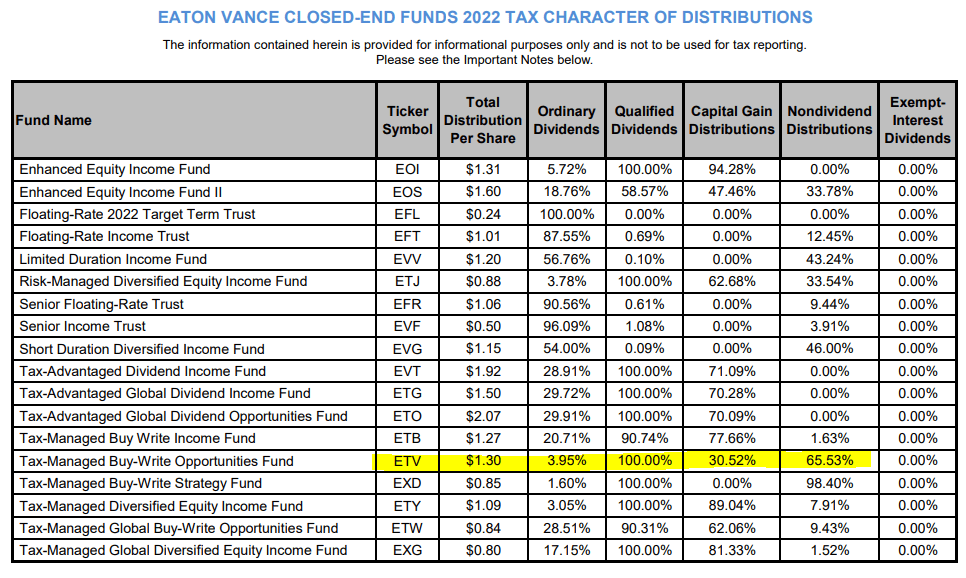

Here's the breakdown of the 2022 tax classifications for the distributions.

{kind=link}

Performance - Premium Coming Down Once Again

Of course, this last year, everything took a hit. Primarily the tech-heavy Nasdaq took a hit where ETV's portfolio is heavily tilted towards. In the last decade, the fund's NAV per share declined by around 11.5%. However, when factoring in the distributions, the fund also delivered appealing total NAV returns.

Ycharts

With a call-writing strategy and generating those losses, that does cap upside. So if you are looking for a strong bull market to come up again in the next decade, then investing in a more straightforward equity fund would probably be a better choice. However, they are likely to distribute a much lower distribution rate due to not having an income focus. With that in mind, here's a look at the performance compared to several benchmarks. Data was as of the end of December 2022.

{kind=link}

We see that ETV's downside was protected relative to the Nasdaq 100 Index in the last year. Thanks to portfolio positioning and their options strategy. However, over the longer term, it significantly underperformed on a total return basis. On the other hand, against its buy/write index counterparts, the fund has done quite well - beating their more appropriate benchmarks.

The premium remains persistent but has come down significantly from where it was a year ago. Additionally, it did appear to start making a recovery before this latest volatility sent it lower once again. That being said, we can also see that we are only a bit below the longer-term decade-long average level.

Ycharts

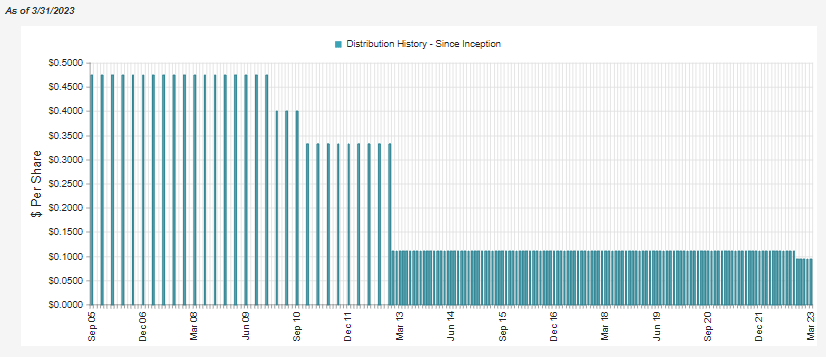

Distribution - Market Hit

ETV had been generating a fairly stable distribution to investors for years before this latest cut. It could have been that sort of stability that investors flocked to, pushing it up to last year's wild premium in the first place in such a weak year.

{kind=link}

For better or worse, Eaton Vance has never been a fund sponsor to focus on steady distributions unless it was warranted. They aren't concerned with keeping a level distribution while it is eroding a fund as other fund sponsors do. They are often the first funds to start cutting their payouts.

To generate coverage of their distribution, they rely on capital gains to a significant degree. Net investment income only covers a very small portion of the distribution to shareholders.

{kind=link}

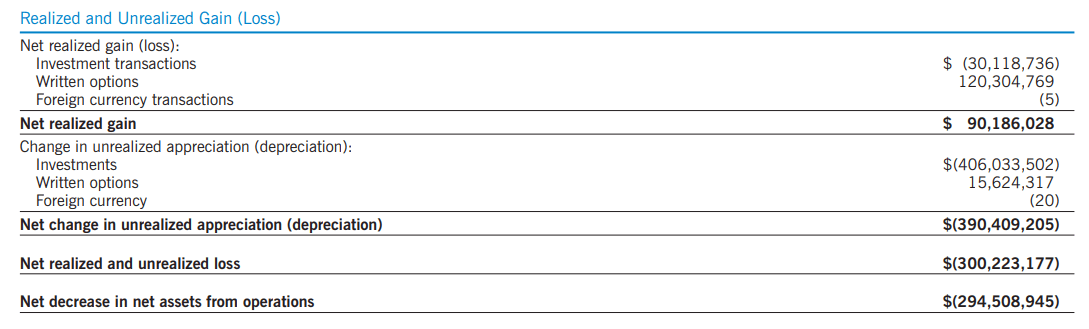

This isn't that unusual for equity funds, especially one with so much tech exposure that ETV carries. However, where ETV realized most of its capital gains in the last year was primarily from the written options strategy in the fund. That was good for over $102.3 million being generated in realized gains.

{kind=link}

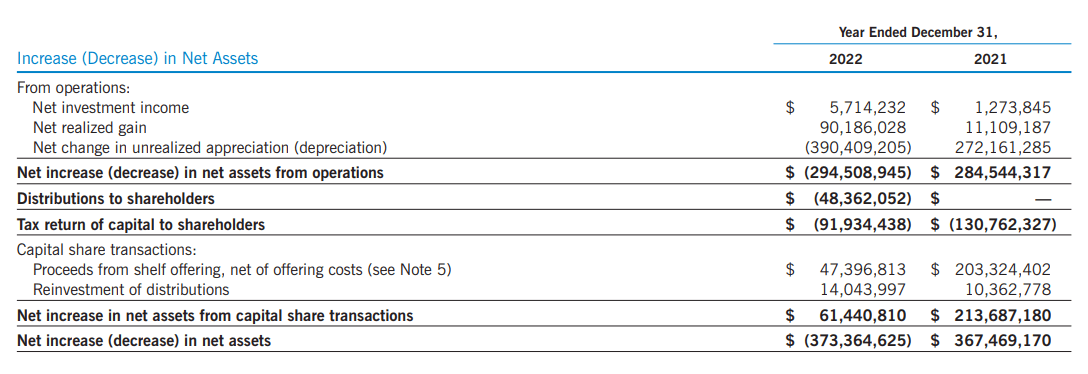

Of course, the unrealized losses and realized losses were enough to offset the realized gain side of the equation, thus, why the NAV declined in the prior year.

In total, the fund paid out ~$140.3 million in distributions to shareholders in the prior year. That includes some of the months with a cut. It's hard to pin down exactly the amount that should be distributed going forward because the fund is still flirting with a premium. That's seen the fund be able to issue shares through an at-the-market offering and generate a substantial amount of assets over the years.

I guess they didn't factor that into their equation when determining when they were going to cut their distribution. So as I said before, for better or worse. The collapsing premium for the fund sponsor is actually one of the "worse" parts for the sponsor and even shareholders, as selling shares at a premium is accretive to earnings and NAV.

In the end, it's fairly simple for ETV, though, if we experience further losses in the broader indexes, then expect losses. If you think we can rebound some from here or even stay flat, then the distribution is likely to be maintained.

ETV's Portfolio

It doesn't take a lot usually to talk about ETV's portfolio because there aren't usually a lot of changes. In the last year, they reported a 19% turnover rate on their fund, and that was over double any of the prior four years, where we saw 9% turnover in each of the years 2021, 2020 and 2018. In 2019, it was an even lower turnover at only 6%. The portfolio isn't the active part of this portfolio; it is the options strategy that is.

They overwrite their fund at nearly 100%, with the last fact sheet showing they are overwritten by 95%. They also listed that the average days to expiration were 16 days, and they were out of money by 5%. So they write fairly close-to-the-money contracts in short periods of time.

ETV Fact Sheet (Eaton Vance)

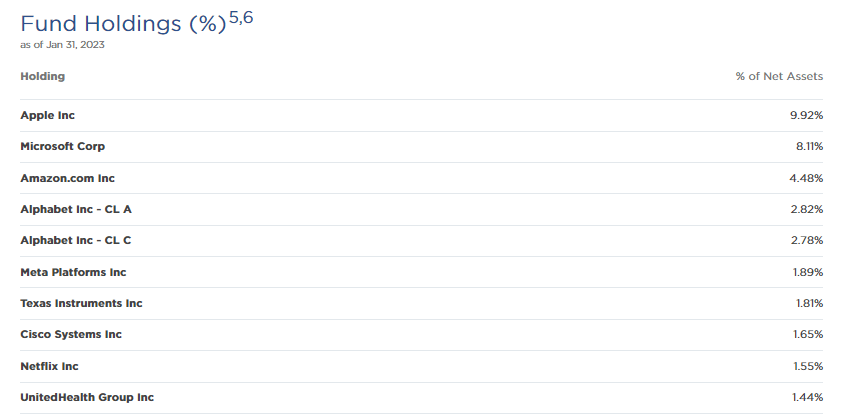

We also can see that they list 188 positions overall. That's more than the Nasdaq 100, but this fund also puts some exposure into S&P 500 names, giving us a more broad portfolio. Although, broad might be a bit of an overstatement when we take a look at their top ten holdings. The top ten make up nearly 36.5% of their portfolio.

{kind=link}

Perhaps more noteworthy is that the top few names make up a majority of that 35.5%, weighting themselves at 22.51% being allocated to Apple ( AAPL ), Microsoft ( MSFT ) and Amazon ( AMZN ). These are also significant positions in the broader indexes, as these three names make up nearly 14% of the S&P 500 index . For the Nasdaq 100, these three names command a 31.13% weighting as represented by the Invesco QQQ ETF ( QQQ )

Suffice it to say, ETV's 188 holdings near the bottom have very little meaning on the fund. As we can see, by the time we get down to UnitedHealth Group ( UNH ) exposure in ETV, we are already down to a 1.44% weighting. Similarly, the bottom positions in the S&P 500 Index also contribute very little to the overall index with its ~500 holdings.

The bottom line is that with ETV, you are getting mostly what you are getting with the broader indexes. They then apply a call-writing strategy on top of this to differentiate, which leads to its tax-advantaged and more 'income' focus with a significantly higher distribution rate. Of course, the vast majority of these distributions are funded with capital gains - either from the underlying portfolio or the premium from selling call options.

Conclusion

ETV is a tech-heavy fund that also puts a call-writing strategy overlay on the fund. That can provide for significantly higher distributions; this strategy can also contribute to its tax-advantaged focus. In a flat or slightly down market, this type of strategy can outperform. In a bull market, it can and has historically underperformed. Much like most things in investing, there are pros and cons to each investment strategy one might choose. I believe that ETV is an attractive tool that investors can leverage in their own income portfolios. That said, a more patient investor could wait for that elusive discount to open up on this fund or dollar-cost average into the position.

For further details see:

ETV: Attractive Fund For The Long-Term