HTD - ETV: Likely To Outperform In The Current Market But Price Is Still Too High

2023-03-29 13:22:07 ET

Summary

- Investors are desperately in need of income simply to maintain their lifestyles in today's inflationary environment.

- Eaton Vance Tax-Managed Buy-Write Opportunities Fund uses an interesting strategy of owning a portfolio of stocks and writing call options against the S&P 500 and NASDAQ 100 to generate income for investors.

- The ETV closed-end fund is incredibly tech-heavy, which is a risk as these companies are unlikely to perform well until the bull market returns.

- The fund recently had to cut its distribution due to severe losses in 2022, but it still yields 9.12%, and this is probably sustainable barring another market collapse.

- The fund is at a more attractive valuation than normal, but it still looks overpriced.

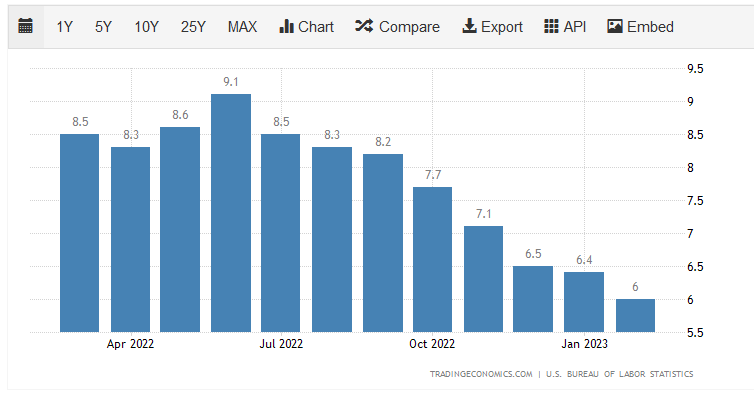

There can be little doubt that one of the biggest problems facing most Americans today is the rapidly rising cost of living. This is quite clearly shown by looking at the consumer price index, which has been at least 6% higher in every month over the past year when compared to the same month of the prior year:

{kind=link}

This is the highest rate of inflation that our country has seen since the early days of Paul Volcker’s tenure as the Chairman of the Federal Reserve four decades ago. As much, many young and even middle-aged people have no experience dealing with such rapid price increases. This particular spurt of inflation has been particularly devastating among those of lesser means since it is primarily centered on food and energy, which are generally considered to be necessities for life today. As such, many households have been forced to take on second jobs or enter the gig economy just to boost their incomes enough to buy food and sustain their lifestyles.

Fortunately, as investors, we do not have to engage in such tactics in order to boost our incomes. This is because we can put our money to work for us in an income-generation capacity. One of the best ways to do this is to purchase shares of a closed-end fund that specializes in the generation of income. Admittedly, these funds are not talked about very often in the investment media and many financial planners are unfamiliar with them. This is a shame because these funds provide an excellent way to obtain a diversified portfolio of assets that can use certain strategies that allow it to earn a higher yield than any of the underlying assets possess.

In this article, we will discuss the Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ), which is one fund that can be used for the purposes of income generation. This fund currently pays an attractive 9.12% yield, and its investment strategy is quite profitable in flat markets like the one that we have today. I have discussed this fund before, but that was six months ago so obviously, a great many things have changed since that time. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances. Let us investigate and see if this fund could be a reasonable addition to your portfolio today!

About The Fund

According to the fund’s webpage , the Eaton Vance Tax-Managed Buy-Write Opportunities Fund has the objective of providing its investors with current income and gains. This is not a particularly common objective for an equity fund since those tend to have total return as their objective. The generation of current income is most commonly seen as the focus of fixed-income funds, but this one is entirely invested in equities:

CEF Connect

The reason why this is an unusual objective is that equities are not usually considered to be an income vehicle. After all, the S&P 500 Index (SP500), which consists of the common stocks of the largest companies in the United States, only yields 1.63% as of the time of writing. Rather than being a vehicle for income, common stocks are normally targeted by investors for their total return potential since they deliver both a dividend and capital gains over time. Admittedly, there are some funds out there like the John Hancock Tax-Advantaged Dividend Income Fund ( HTD ) that invest in dividend-paying stocks and have an income objective, but even those funds usually aim to provide some combination of income and capital gains.

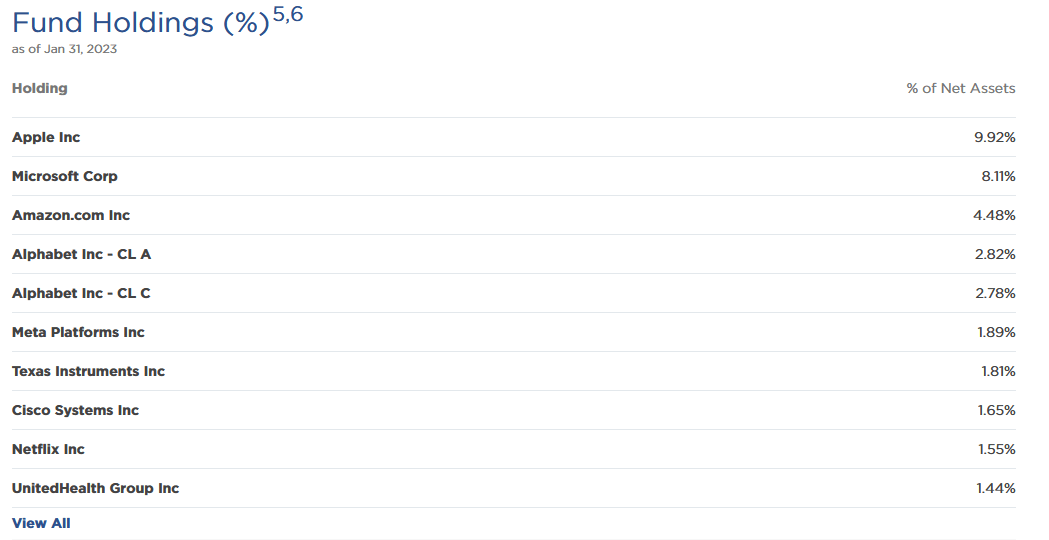

A quick look at the portfolio of the Eaton Vance Tax-Managed Buy-Write Opportunities Fund will reveal that this one is definitely not seeking dividend income:

{kind=link}

The first thing that we immediately see here is that this fund has incredibly high exposure to the technology sector. The technology sector is generally disliked by dividend investors because the companies in it have little or no yield. For example, here are the current yields of the companies listed above:

| Stock |

| Current Dividend Yield |

| Apple ( AAPL ) |

| 0.58% |

| Microsoft ( MSFT ) |

| 0.99% |

| Amazon.com ( AMZN ) |

| 0.00% |

| Alphabet – Class A ( GOOGL ) |

| 0.00% |

| Alphabet – Class C ( GOOG ) |

| 0.00% |

| Meta Platforms ( META ) |

| 0.00% |

| Texas Instruments ( TXN ) |

| 2.79% |

| Cisco Systems ( CSCO ) |

| 3.10% |

| Netflix ( NFLX ) |

| 0.00% |

| UnitedHealth Group ( UNH ) |

| 1.40% |

The only company on that list that has a respectable yield is Cisco Systems, and even it currently pays out a smaller yield than an ordinary savings or money market account. Thus, this fund is definitely not trying to earn dividend income from this portfolio.

A look at the fund’s fact sheet provides some insights into its income-generation strategy. In short, the fund is writing call options against various U.S. and foreign indices. Despite stating that it will write options against both American and foreign indices, as of December 31, 2022, the fund only had outstanding contracts written against the S&P 500 Index and the NASDAQ 100 Index ( QQQM ). This makes a great deal of sense considering that all of the companies on the list above are in one or both of these indices.

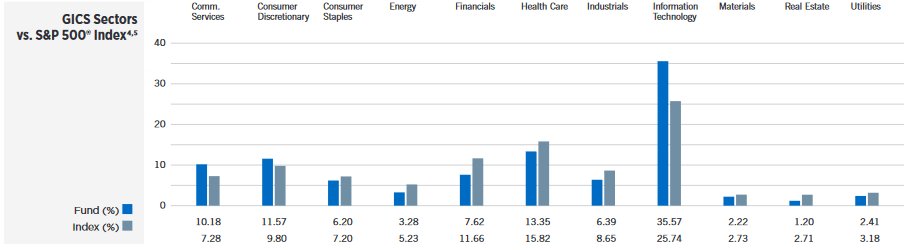

With that said, the fund is not writing covered calls. It is writing options against the indices, but it does not actually own the indices. In fact, the fund only has 188 positions, which is far less than the S&P 500 contains. This exposes the fund to a significant amount of risk should the option be exercised against it. In theory, these losses can be unlimited since the fund will have to pay any price to obtain the index in order to deliver to the counterparty on the option. The company’s portfolio, theoretically, is designed in a way that it should deliver a comparable return to the indices and offset this risk. However, the fund’s portfolio is substantially more exposed to the technology sector than the S&P 500 Index:

{kind=link}

This was not a good portfolio to have in 2022 since it is more heavily exposed to the technology sector, which underperformed the index in that year, and less heavily exposed to both energy and healthcare, which both outperformed. A few commenters on previous articles mentioned that my criticism here amounts to an attempt to time the market, but it was pretty obvious in 2021 that the technology sector was overvalued and would collapse as soon as the Federal Reserve turned off the free money policy that dominated 2020 and 2021. That is precisely what happened.

The fund’s strategy does generally do pretty well during bear markets though, and this showed itself in 2022. The fund had a total return of –17.55%, which beat the –18.11% of the S&P 500 Index and the –32.38% total return of the NASDAQ 100 Index. The biggest reason for this is that the fund received premiums from the options that it sold. As the market declined, it reduced the risk that any of these options would be exercised against it. That allowed the fund to pocket the premiums and thus offset some of the losses from its portfolio. This is likely to continue to be the case over the next year or two, as it looks quite likely that we will have a flat or declining market. This is especially true considering that there are some signs that the Federal Reserve is attempting to push the economy into a recession to stop inflation, and it appears to be having some success considering that we are seeing signs that the American consumer is weakening. As I pointed out in a previous article , the major technology companies were responsible for a significant portion of the gains of the S&P 500 Index over the past decade and it is unlikely that they will return to their former bubble valuations without a reduction in interest rates. The Federal Reserve is unlikely to cut interest rates in the near future barring a recession, so we are very likely to have a flat market. A bear market is also a possibility, particularly if the market realizes that the Federal Reserve will not pivot and unleash quantitative easing. This is the sort of environment in which this fund should be able to outperform, although it would still be nice to see it reduce its technology exposure and become more diversified.

As my long-time readers on the topic of closed-end funds are no doubt well aware, I generally do not like to see any individual asset account for more than 5% of a fund’s portfolio. This is because that is approximately the point at which the asset begins to expose the portfolio to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market in aggregate. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then it will not be completely diversified away. Thus, the concern is that some event may cause the price of a given asset to decline when the market does not and if that asset accounts for too much of the portfolio, then it will end up dragging the entire fund down with it. As we can see above, there are three companies (Apple, Microsoft, and Alphabet) whose weightings exceed that 5% threshold. As such, anyone purchasing this fund should be certain that they are willing to take on the individual risks of those three companies before buying.

Distribution Analysis

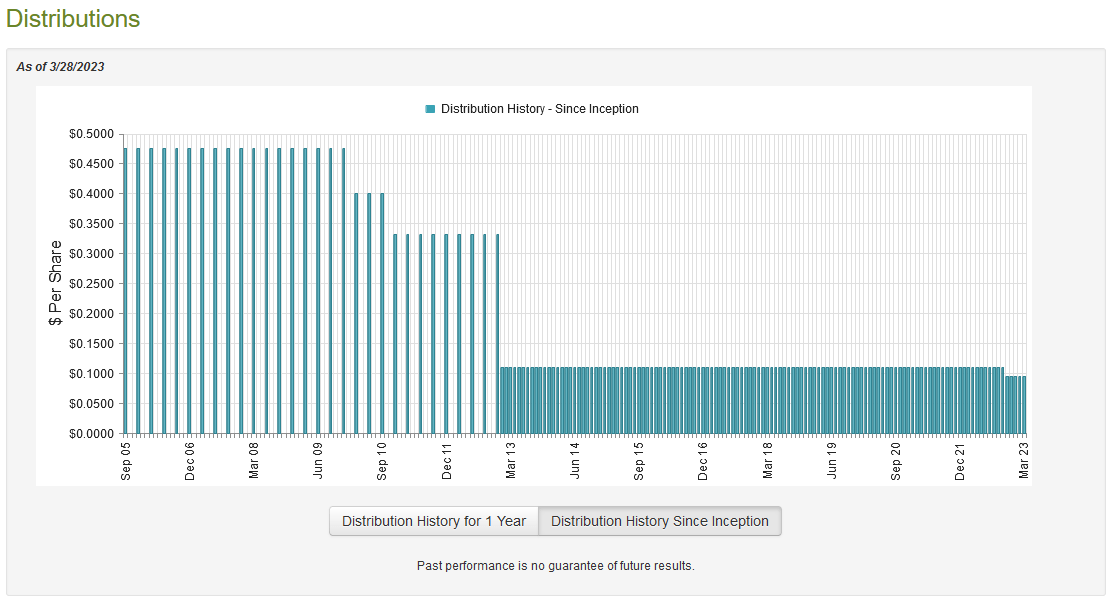

As mentioned earlier in this article, the Eaton Vance Tax-Managed Buy-Write Opportunities Fund has the stated objective of providing its investors with a high level of current income and gains. In order to achieve this goal, the fund holds a portfolio of common stocks and writes call options against the S&P 500 and NASDAQ 100 Indices as its source of income. When properly executed, a call-writing strategy can indeed result in a great deal of income. This is particularly true in markets that are not raging bull markets, such as the one we have today. As such, we might assume that this fund boasts a reasonably high distribution yield. That is certainly the case as it currently pays out a monthly distribution of $0.0949 per share ($1.1388 per share annually), which gives it a 9.12% yield at the current price. The fund was formerly quite reliable and consistent with its distribution, although it was forced to cut it a few months ago:

{kind=link}

The reason for this distribution cut probably has to do with that enormous weighting to a handful of mega-cap technology companies. Regardless, it may reduce the fund’s appeal in the eyes of those that are looking for a reliable and stable source of income with which to pay their bills, despite the fact that the fund managed to maintain its former distribution for almost a decade. The fund’s past is perhaps not the most important thing for potential investors today, though. After all, anyone purchasing shares today would receive the current distribution at the current yield and are not really impacted by the fund’s history. Thus, the most important thing for investors today is how well the fund can maintain its current distribution.

Fortunately, we have a very recent document that we can consult for this purpose. The fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2022. This is one of the most recent financial reports that we have available to us for any closed-end fund, and of course, it is much newer than what we had available the last time that we discussed this fund. Overall, this report should give us a pretty good idea of how the fund weathered the challenging market conditions that dominated 2022. During the full-year period, the Eaton Vance Tax-Managed Buy-Write Opportunities Fund received $21,502,064 in dividends and, curiously, no interest from the assets in its portfolio. That dividend income was therefore the fund’s total income during the period. The fund paid its expenses out of that amount, which left it with $5,714,232 available for shareholders. As might be expected considering the size of this fund, that was nowhere close to enough to cover the distribution. The fund actually paid out $140,296,490 in distributions to the shareholders over the period. At first glance, this will likely be concerning as the fund clearly did not earn sufficient net investment income to cover its distributions.

However, the fund does have other methods through which it can earn the money that it needs to cover the distribution. For example, the premiums that the fund receives from the sale of call options are not considered to be part of its net investment income. These payments are instead classified as either capital gains or as a return of capital, depending on the situation. In addition to this, the fund might have capital gains from stock appreciation, although that is unlikely considering its portfolio and the market conditions last year. Fortunately, the fund did manage to achieve net realized gains of $90,186,028 but this was offset by $390,409,205 net unrealized losses. While those net realized gains were admirable, they were insufficient to cover the fund’s distributions, even when combined with the net investment income. This explains the recent distribution cut. The fund’s assets overall decreased by $373,364,625 over the full-year period after accounting for all inflows and outflows of cash. It remains to be seen if this new distribution is sustainable or not, but it will probably be pretty close unless we have another market crash.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Tax-Managed Buy-Write Opportunities Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. Unfortunately, that is not the case with this fund today. As of March 28, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $12.36 per share but the shares currently trade for $12.53 a piece. This gives the fund’s shares a 1.38% premium to the net asset value at the current price. This is much better than the 6.22% premium that the shares have averaged over the past month, but it is still a premium and it is generally not a particularly great idea to purchase any fund at a premium to the net asset value. Thus, it would be best to wait for the shares to come down a bit in price before purchasing them.

Conclusion

In conclusion, the Eaton Vance Tax-Advantaged Buy-Write Opportunities Fund uses a somewhat novel strategy to generate a high level of income for its investors, and it accomplishes that goal reasonably well. The fund’s portfolio is perhaps not the best right now though as it has substantially higher exposure to a few stocks that are still trading with bubble valuations and could suffer in another market downturn. The fund’s strategy does allow it to outperform during flat or bear markets though, and this will likely offset some of the risks. The fund recently had to cut its distribution as a result of huge losses in 2022, but it can probably sustain the new one barring any more losses. The real problem is that the Eaton Vance Tax-Managed Buy-Write Opportunities Fund is still rather expensive today, and it may make sense to wait until the price comes down before buying it.

For further details see:

ETV: Likely To Outperform In The Current Market, But Price Is Still Too High