ETV - ETW: A Reasonable Way To Get A 9.00% Yield At A Discount

2023-11-30 12:33:58 ET

Summary

- Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund employs an options strategy to generate high income without relying on high-yielding fixed-income assets.

- The ETW closed-end fund's share price performance has been disappointing, underperforming the S&P 500 Index over the past few months.

- The fund's distribution history shows consistent reductions in payouts, which may not appeal to investors seeking consistent income.

- The fund's strategy is employing naked options-writing, which is a riskier strategy than covered calls employed by other option funds.

- The fund did manage to cover its distribution in the first half of this year and is trading at a huge discount to intrinsic value.

Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund (ETW) is a closed-end fund, or CEF, that can be employed by those investors who are seeking to earn a very high level of income from the assets in their portfolios. This fund is a bit unusual among income-focused funds, however, as it does not employ the usual strategy of investing in junk bonds, preferred stock, or another high-yielding fixed-income asset. Rather, it employs an options strategy that is designed to give it a somewhat lower volatility than an ordinary common stock fund without completely removing the ability of the fund to benefit from the capital gains that generally accompany a common equity investment. The fund has been reasonably successful in this endeavor, as its current 9.00% yield is considerably higher than most common equity closed-end funds, but it is admittedly not as attractive as some junk bond or leveraged loan funds have managed to achieve in today's high-interest rate environment.

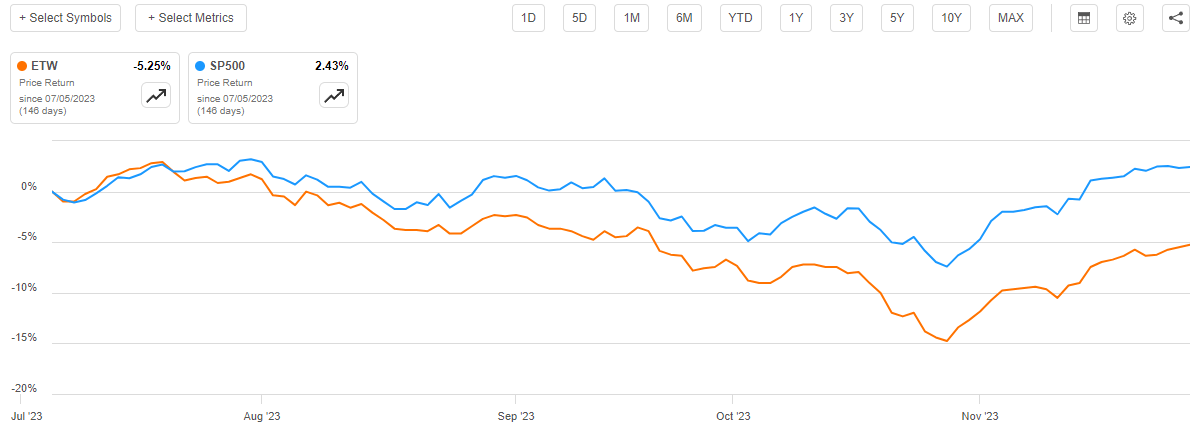

As regular readers may no doubt recall, we last discussed this fund in early July of this year. At the time, the fund traded at a reasonable price, but it only had an 8.47% yield. The higher yield today is the direct result of the fund's share price performance not being especially good over the intervening period. As we can see here, the fund's share price is down 5.25% since the date that my prior article was published:

{kind=link}

This is certainly disappointing, to say the least, as the fund's market price performance has been substantially worse than the performance of the S&P 500 Index ( SP500 ) over the same period. Interestingly, though, the fund's overall performance chart strongly resembles that of the broad market index. The difference is merely that this fund's price declined by more than the index during the market correction period that lasted from the middle of July until the middle of October.

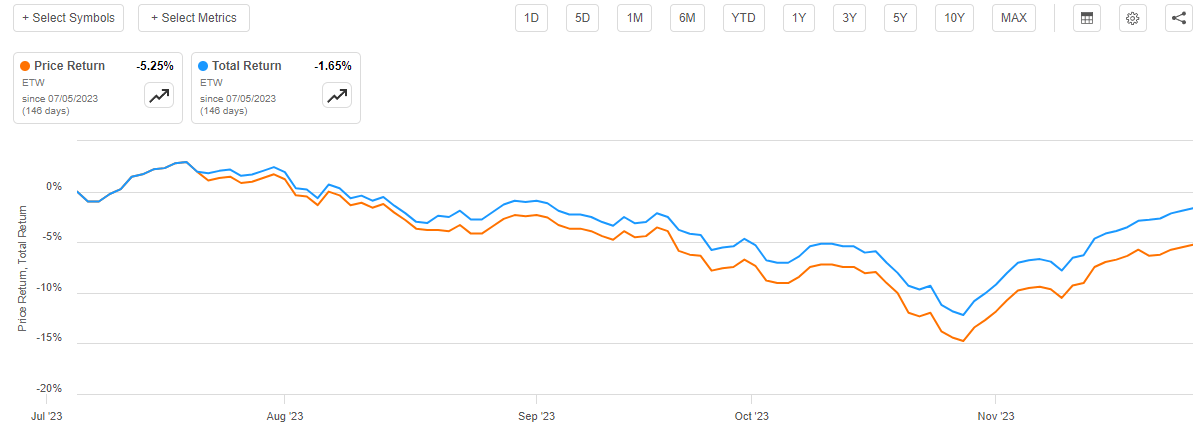

Fortunately, the fund's share price performance does not accurately reflect what investors in the fund actually received. This is because the fund pays a very large distribution and the money that the investors received from this source offset some of the share price declines. However, investors who purchased the fund on the date that my last article was published are still down 1.65% overall:

{kind=link}

As several months have passed since the date that my last article was published, it could be a good idea to revisit this fund and see if purchasing its shares makes sense today. After all, the fund's shares are currently trading at a discount to their intrinsic value.

About The Fund

According to the fund's website , the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund has the primary objective of providing its investors with a very high level of current income and current gains. Unfortunately, the website provides no insight into how exactly the fund is going to go about attempting to achieve this goal. This is a problem that most of Eaton Vance's funds share, as this fund house does not typically put a description of its funds on the webpage like every other sponsor does. The fact sheet does provide a description of the fund's basic strategy, however:

The Fund invests in a diversified portfolio of common stocks and writes call options on one or more U.S. and foreign indices on a substantial portion of the value of its common stock portfolio to seek to generate current earnings from the option premium. The Fund's portfolio managers use the adviser's and sub-adviser's internal research and proprietary modeling techniques in making investment decisions. The Fund evaluates returns on an after tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the fund.

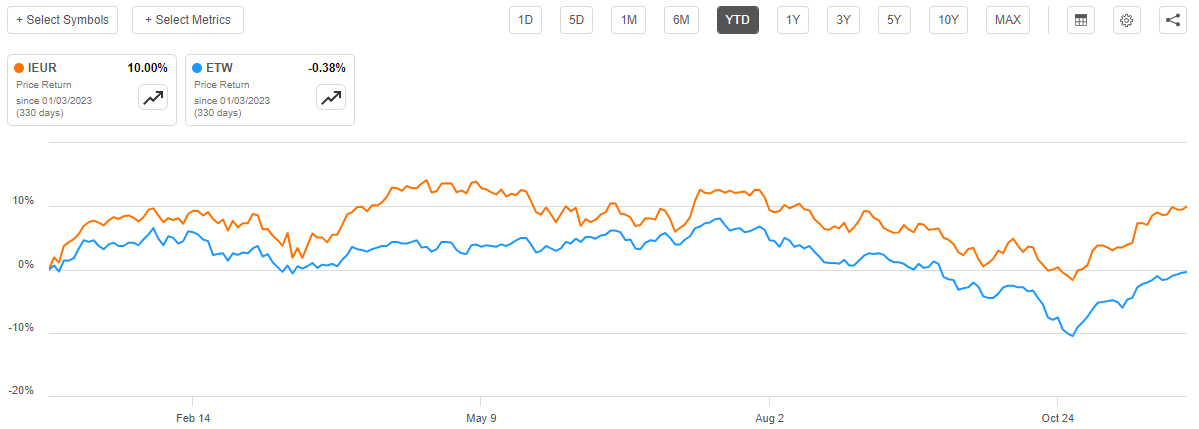

This is a similar strategy to many of Eaton Vance's other option-income funds. In fact, it is difficult to tell what the difference is between this fund and the Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV) that I discussed back in August. The only real difference is that the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund mentions that it might write options against a foreign index. The fund's fact sheet also apparently suggests that this fund is benchmarked against the MSCI Europe Index (IEUR), but if that is the case then its current portfolio makes absolutely no sense. This chart comes directly from the fund's fact sheet and shows how its portfolio compares to that index:

Fund Fact Sheet

A look at the three-year chart of this fund's price plotted against the MSCI Europe Index likewise shows that this fund's performance has been vastly different from the MSCI Europe Index year-to-date:

{kind=link}

The difference in performance almost certainly comes from the fact that 57.37% of this fund's assets are invested in North American companies:

Fund Fact Sheet

If this fund is actually trying to benchmark itself against the MSCI Europe Index, then it makes absolutely no sense for more than half of its positions to be invested in North American companies.

With that said, the fund's most recent financial report , which corresponds to the six-month period that ended on June 30, 2023, does not specifically state what the benchmark index for this fund is. Rather, that document simply includes a table that compares the fund's performance against the S&P 500 Index as well as a few foreign indices:

{kind=link}

The fund's average annual total returns seem to most closely resemble those of the MSCI Europe or the CBOE S&P 500 BuyWrite Index, depending on the time period in question. The fund is actually writing call options against the Dow Jones Euro Stoxx 50 Index, the FTSE 100 Index, the NASDAQ 100 Index, the S&P 500 Index, and the SMI Index. As of June 30 though, the outstanding notional value of the call options written against the two American indices vastly exceeds that of the foreign indices. Thus, despite the fact sheet apparently claiming that the fund is benchmarked against the MSCI Europe Index, that does not appear to be the case.

In a recent article , I discussed how a fund could use covered call options as a way of generating income without an abnormal amount of risk. In fact, the only real problem with a covered call strategy is that the investor who writes the options sacrifices some of the upside potential of the stock. However, that is not the strategy that this fund is using. As just mentioned, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund has options written against both American and a handful of foreign broad market indices. However, this fund does not actually own any of these indices. All it owns is 285 stocks from a few companies around the world. Thus, this fund is technically writing naked options, which is a rather risky strategy that could expose it to potentially infinite losses. The fund theoretically can close out its options positions if they are losing prior to expiration, but even that can be potentially risky. While the fund can hope that its portfolio will deliver similar returns to the indices in order to reduce the overall risk, it does not negate the fact that this fund is using a riskier strategy than Eaton Vance's own covered call funds. Those investors who are more risk-averse should take this into account when making their decisions about whether or not to purchase this stock.

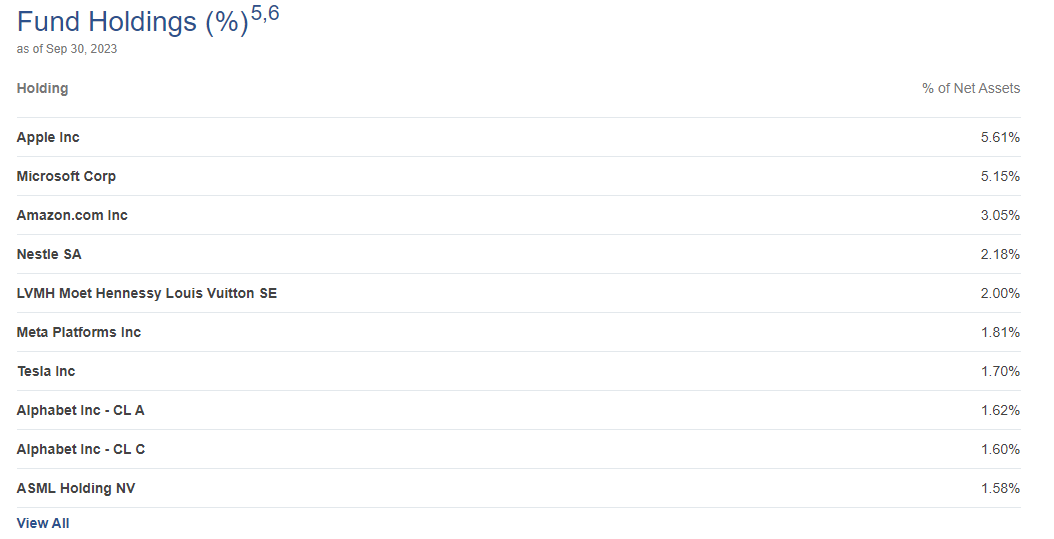

As I have pointed out in various previous articles, Eaton Vance's closed-end funds have a tendency to invest very heavily in a handful of mega-cap American technology companies. This fund is no exception to this rule, as we can see by looking at the largest positions in the portfolio:

{kind=link}

We can see six of the "Magnificent 7" stocks here, and in fact, these are the only American companies in the top-ten holdings. This does somewhat make sense considering that the fund is writing index call options against the S&P 500 Index. After all, as I pointed out in a recent article (linked earlier), essentially all of the returns of the S&P 500 Index year-to-date have been due to seven stocks. These stocks, with the exception of NVIDIA ( NVDA ) are all among the largest positions in this fund. Thus, that probably works pretty well to offset the risk of the naked call options against both the S&P 500 Index and the NASDAQ 100 Index, as those stocks alone deliver pretty similar returns to the entire index. It is a bit strange that a fund writing index options against foreign indices would only have three foreign companies among its largest holdings though, even if these are some of the largest companies in their respective nations.

There has only been one major change to the fund's largest positions list since the last time that we discussed it. This change is that Fast Retailing Co. (FRCOF) was removed from the list and replaced with Tesla (TSLA). The remainder of the firms on the list are the same as they were in July, although the weightings of several of the stocks have changed. That could simply be caused by one company outperforming another in the market and may not necessarily be a sign that the fund is actively attempting to change its positions. The fund's 12.00% annual turnover certainly suggests that this fund is not engaging in a great deal of trading, as that is one of the lowest turnovers of any equity closed-end fund in the market. This is nice as it indicates that the fund's managers are probably not incurring a significant level of trading expenses. This should help keep the fund's expenses down.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund is to provide its investors with a very high level of current income and current gains. In order to accomplish this objective, the fund invests in a portfolio of various stocks issued by companies primarily from North America and Europe, although it does have some Asian exposure. The fund then writes call options against a few different American and foreign equity indices. The general objective is to receive the option premium and have the option expire worthless, allowing the fund to keep all of the received premiums. This can result in a very high level of income when executed successfully. The fund also might be able to realize capital gains by selling off appreciated stocks. The money earned from these two activities is combined into a pool of cash that is then paid out to the investors, net of the fund's own expenses. When we consider the earnings potential from the options strategy, we can guess that this would result in the fund having a very high current yield.

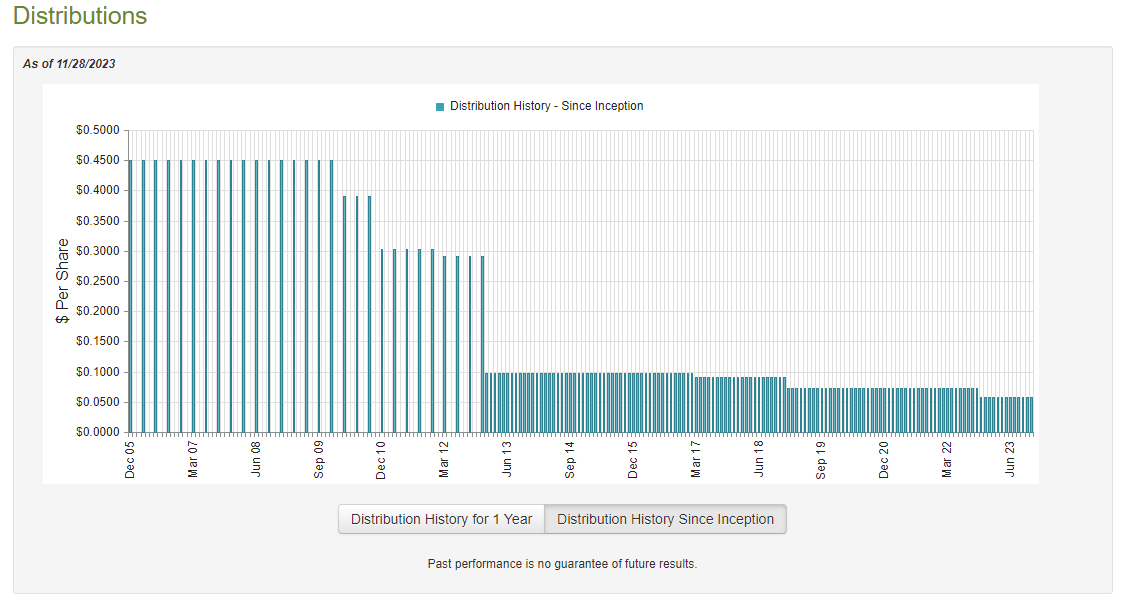

This is certainly the case, as the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund pays a monthly distribution of $0.0582 per share ($0.6984 per share annually), which gives it a 9.00% yield at the current price. Unfortunately, the fund's distribution history leaves a lot to be desired, as the fund has been consistently reducing its payout over the past decade:

{kind=link}

This is not something that will appeal to those investors who are seeking to earn a safe and consistent level of income that they can use to pay their bills or finance their lifestyles. This is particularly true today as inflation has steadily reduced the purchasing power of the fund's distributions over the past two years, yet the fund has actually decreased its distribution.

With that said, the most important thing is how well the fund can sustain its current distribution at the current level. After all, anyone buying the fund today will receive the current distribution at the current yield and will not be affected by the actions that the fund has had to take in the past. Today's buyer simply wants to ensure that the fund will not have to cut again and reduce their income.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report (linked earlier) corresponds to the six-month period that ended on June 30, 2023. This is a newer report than the one that we had available the last time that we discussed this fund, which is nice to see. After all, the first half of 2023 was characterized by a great deal of optimism and market euphoria, as investors widely expected that the Federal Reserve would cut interest rates in the very near future and bid up asset prices in expectation of this event. While this eventually proved to be incorrect, the fund may have still had the opportunity to profit from the market's expectations by selling appreciated stock or options into a market that was bidding up asset prices.

During the six-month period, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund received $12,723,788 in dividends and surprisingly no interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $13,080,215 during the period. The fund paid its expenses out of this amount, which left it with $7,804,285 available for the shareholders. That was, unfortunately, nowhere close to enough to cover the $38,271,547 that the fund paid out in distributions to its shareholders during the period. At first glance, this could be concerning as the fund clearly does not have sufficient net investment income to cover its payouts.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, the core part of the fund's strategy is to write index options and receive the premiums. The money that it receives from this process is not included in net investment income, but it clearly represents money that the fund could distribute to its shareholders. The fund might also be able to realize some capital gains by selling appreciated stock. That is also not included in net investment income but can certainly be distributed to the shareholders. Fortunately, the fund did enjoy success at this task during the period. The fund reported net realized losses of $6,518,054 but these were offset by $106,726,476 net unrealized gains. The fund's net assets went up by $69,741,160 after accounting for all inflows and outflows during the period. As such, the fund did manage to cover its distributions during the period with an enormous amount of money left over.

With that said, the fund's net assets are still down over the trailing eighteen-month period. As of January 1, 2022, the fund had net assets of $1,189,319,344 but this was down to $988,699,439 on June 30, 2023. Thus, the fund failed to cover its distribution during the trailing eighteen-month period. In addition, the fund only managed to cover its distributions during the most recent period because of net unrealized capital gains. As everyone reading this is no doubt aware, unrealized capital gains can be erased in a market correction. As such, the fund's distribution is certainly not perfectly safe, although its net asset value is up 5.24% year-to-date so it has managed to cover its distributions so far.

Valuation

As of November 28, 2023 (the most recent date for which data is currently available), the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund has a net asset value of $8.83 per share but the shares currently trade for $7.77 each. This gives the fund's shares a 12.00% discount on net asset value at the current price. This is a very reasonable discount, although it is not as good as the 14.06% discount that the shares have had on average over the past month. As such, it might be possible to obtain a better price by waiting for a bit, but realistically a double-digit discount is always a very reasonable price to pay for a fund. Thus, right now could certainly be a decent time to enter into a position if you want to add this fund to your portfolio.

Conclusion

In conclusion, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund is an interesting fund that uses a rather unique strategy. The fund writes naked options against a few American and foreign indices and hopes that its portfolio can perform well enough to avoid losing money. It is not as safe of a strategy as a covered call-writing options strategy, but this fund has historically managed to make it work.

A nice thing about Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund right now is that the 9.00% distribution yield is fully covered, and the fund's shares are trading at a very reasonable price. The only real issue here is that the fund is heavily exposed to the Magnificent 7 stocks, so it will do little to increase the overall diversification of your portfolio.

For further details see:

ETW: A Reasonable Way To Get A 9.00% Yield At A Discount