URTH - ETW: Discount Widening After Latest Distribution Trim

Summary

- A couple of months ago, the Eaton Vance suite cut most of their equity fund distributions.

- These trims were to reduce the distribution rates to more manageable levels.

- With this, we saw the discount return or widen out on some EV funds, presenting a more attractive time to consider them.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on December 9th, 2022.

Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund (ETW) was one of the Eaton Vance equity funds to trim their distributions. It was hard to avoid as it was most of the funds except for two.

That being said, since that time, the fund's discount has widened back out to levels where it was earlier this year. That creates a potential opportunity for investors to consider a position in this fund now that it's back at a better valuation.

The fund's performance relative to the S&P 500 since our last update shows that the fund has fallen further than this broader market gauge. The fund utilizes a call-writing strategy, as well as having a global positioning in its portfolio. Therefore, the S&P 500 isn't an appropriate benchmark, but it can give us some context to how things have been going for the fund.

ETW Performance Since Previous Update (Seeking Alpha)

After the cut, the distribution should be more manageable at this time too. However, like any equity fund in a bear market, it will always be susceptible to more cuts.

The Basics

- 1-Year Z-score: -1.85

- Discount: -7.30%

- Distribution Yield: 9.01%

- Expense Ratio: 1.09%

- Leverage: N/A

- Managed Assets: $899.7 million

- Structure: Perpetual

ETW will "invest in a diversified portfolio of common stocks and write call options on one or more U.S. and foreign indices on a substantial portion of the value of its common stock portfolio to seek to generate current earnings from the option premium." They last reported being overwritten at 90% of the portfolio. This is fairly aggressive.

The tax-managed focus comes in with the "fund evaluating returns on an after-tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the Fund." The investment policy is designed to achieve their main objective; "to provide current income and gains, with a secondary objective of capital appreciation."

Performance - Discount Back To More Opportune Levels

Distribution cuts aren't all bad. After the distribution trim, the fund's discount is back down to the level it was around earlier in the year for our May 2022 update. At that time, the fund's discount was 6.76%. At the current level, it is pushing it back below its decade-long average of around 3%.

The fund doesn't employ any leverage, and that could be one of the silver linings during these bear market years. Had it employed leverage, the losses could be even steeper this year. Incorporating some funds that take an income approach via writing calls over leveraging up can help provide broader diversification in one's portfolio.

Even more interesting to note, on a total NAV return basis, ETW has outperformed the SPDR S&P 500 ETF ( SPY ). Due to the global tilt of the portfolio, I've also included the iShares MSCI World ETF ( URTH ).

Given the fund's index call writing strategy and portfolio positioning, I believe that's why the fund had slightly better performance. Albeit, we've seen several other offerings from BlackRock that did an even better job of mitigating losses. Of particular note , the BlackRock Enhanced Global Dividend Trust ( BOE ) has shown better performance on both the total share price and total NAV return basis.

Ycharts

I don't think that means one is better than the other, but that both are positioned differently. ETW still retains a lot of exposure to the mega-cap tech names that are incorporated into SPY. BOE also writes covered calls on single positions in the portfolio vs. ETW's index writing. The outperformance also isn't necessarily the most dramatic difference that we could have seen.

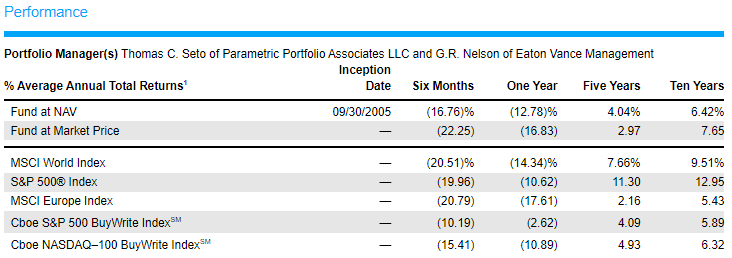

In their reports, they provide several benchmarks for measuring the annualized returns of their fund. This can give us a better idea of the performance over the longer term.

{kind=link}

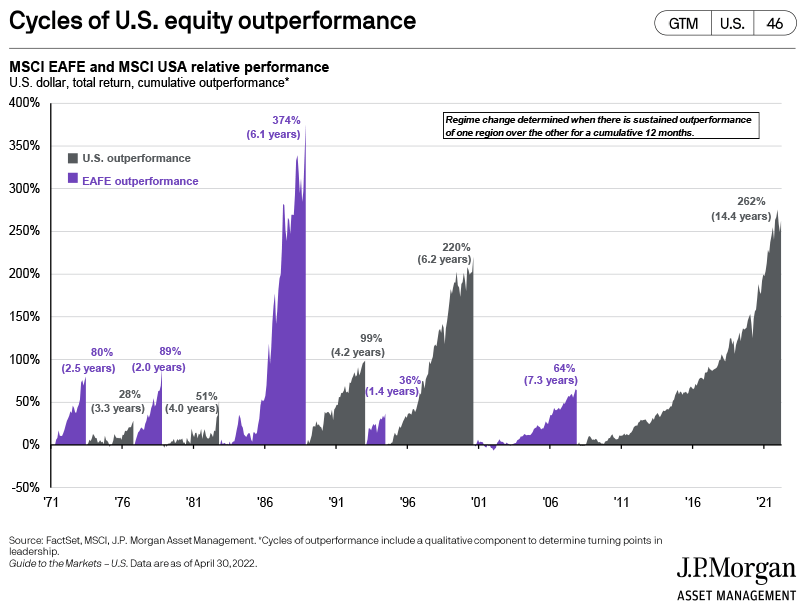

One of the main arguments for investing in international holdings is for greater diversification. It might seem like it never happens, but international markets do, in fact, have their moments of outperformance relative to U.S. investments. We frequently touch on this topic when discussing international funds, and it is always worth mentioning.

Here's a chart provided by JPMorgan showing the relative performance between the markets.

{kind=link}

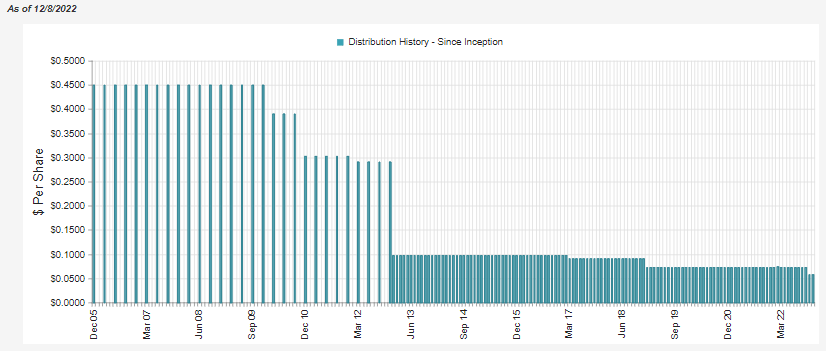

Distribution - Trimmed

ETW has added yet another distribution cut to its record. The latest cut brought the fund's NAV distribution rate down from over 10% to a more manageable 8.35% at this time.

Again, this goes back to international vs. U.S.-based investments. In most of the last decade, U.S.-focused funds had shown fewer distribution cuts relative to those invested globally simply because they could support a higher distribution. In our prior update, we noted that since equities were performing poorly, we were at risk for cuts. So it wasn't totally unexpected.

Since equity markets have been performing poorly, equity CEFs are at risk of distribution cuts. This is because they rely on capital gains to fund their distributions. While they can navigate through some periods of decline, the more prolonged or sharp the decline, the harder it becomes to come across gains.

With equity funds, the underlying performance of holdings plays a big role in making sure the distributions are covered. When they are paying 8% to 10% distribution rates, there is often little room for downside potential before trims start to happen. Other equity funds that maintain 10%+ NAV distribution rates are probably only doing so to their longer-term detriment. When they do have to cut, if a rebound doesn't come swiftly, it could be an even larger cut.

{kind=link}

Thus, when we are in a bear market, you can expect distribution cuts to happen. In 2020, the COVID crash was so quick that we hardly saw any cuts. For longer downturns like 2022's bear market is turning out to be, there will be more pain felt.

That's why despite even the recent distribution trim, we can't necessarily rule out another one sometime next year. When they make a cut, it would be anticipated that they are doing enough not to have to turn around and cut again next month. However, if we go down another 10% to 20% in six months, it is always possible we will see another trim.

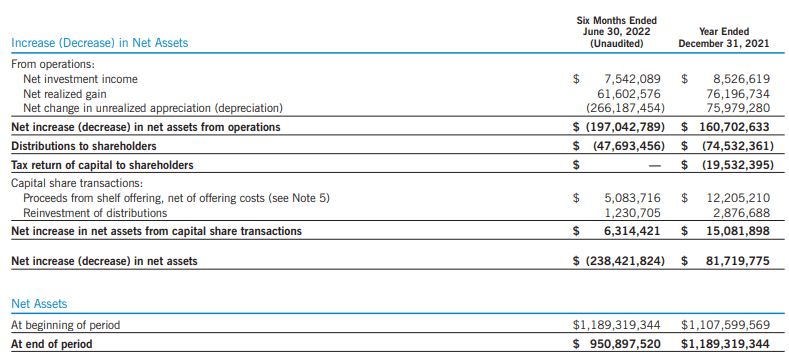

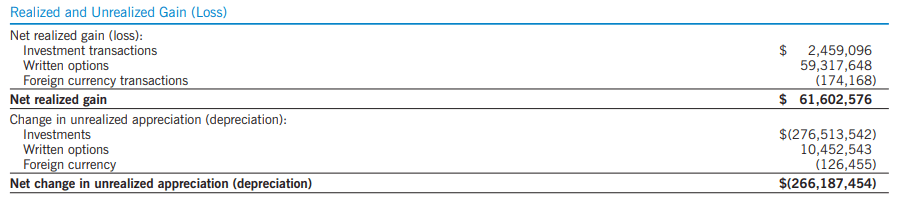

Looking at the last semi-annual report , net investment income coverage came to 15.81%.

{kind=link}

At the time, they had actually realized enough capital gains to fund the distribution for the first six months at $61.6 million compared to the payout of $47.693 million. Going forward, with 109,460,437 shares outstanding based on the annualized distributions of $0.6984, we should anticipate total distributions paid of $76.447 million.

The premium received from selling index options is helping to generate some of those realized gains besides selling underlying positions that have appreciated. In fact, it was the overwhelming primary source, bringing in $59.318 million for the fund in the first six months.

{kind=link}

What is interesting is that the first six months technically would have generated enough to cover the payout at the time. Since assets have declined since then, they likely had to stop selling as many contracts. Thus, a decline in options premiums in the future is something we should expect. We will get a clearer picture when the annual report is available for this year.

They also could have been realizing losses from their underlying portfolio to continue in their tax-managed approach. When realizing losses, they can generate return of capital distributions rather than short or long-term capital gains. These are more tax-friendly to investors since it reduces an investor's cost basis, making it a way to defer taxes until an investor sells. ROC distributions are a regular staple in ETW's distribution.

{kind=link}

ETW's Portfolio

The turnover for ETW's portfolio is generally very low. It has been between 1% and 7% in the last five years, which means that they really aren't switching up their portfolio that much. Instead, they write those index options as the "active" portion of their portfolio.

The average number of days to expiration is 16 days when they last reported . So they are writing these fairly frequently. It was on 96% of the stock portfolio and 9.4% out of the money.

ETW Option Writing Stats (Eaton Vance)

In that same fact sheet, they list the geographic mix of the portfolio. The largest weighting is to North America, with Europe being a fairly significant weighting. They also have a fairly meaningful weighting in the Asia/Pacific region. One thing that would seem to help this fund going forward would be a resolution to Russia's invasion of Ukraine. That could see some relief for European investments.

ETW Geographic Exposure (Eaton Vance)

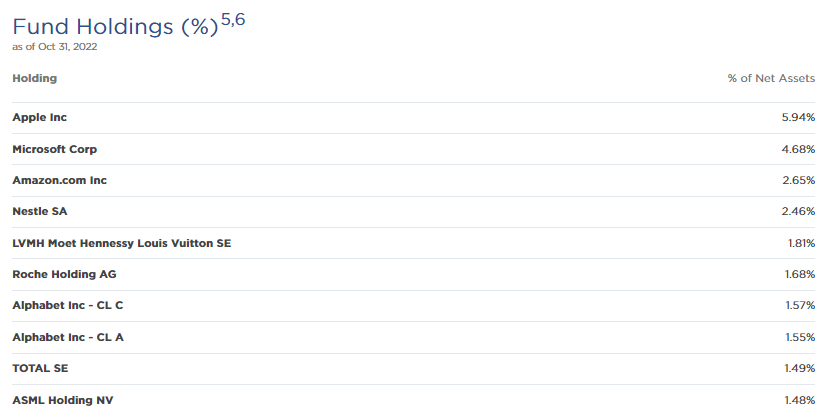

Looking at the top ten positions, we see the usual mega-cap tech names.

{kind=link}

Apple ( AAPL ) has retained its top spot. The weighting moved up a bit from our last update. We also have Microsoft ( MSFT ), seeing its weight increase a touch. Amazon ( AMZN ) maintains its position as the third largest, but its weighting has essentially stayed flat.

ETW includes both classes of Alphabet shares ( GOOG ) and ( GOOGL ). Combined means that the exposure to Alphabet would increase to the third largest weighting.

One notable position removed from the fund's top ten is Tesla ( TSLA ). Making its way on the top holdings list is TotalEnergies ( TTE ). TTE was a position in the fund previously, and TSLA is still the twelfth largest position. The difference in what makes it in the top ten seems to be simply due to performance between the two.

What is maybe more interesting is that between the updates is that TSLA has fallen so sharply lately, before this October update. Elon Musk buying Twitter was a big reason for this. For ETW, the weighting of TSLA only went from 1.46% to 1.40%. Additionally, TTE hasn't done anything remarkable during this time but seemingly just enough to edge out TSLA from a top spot.

Ycharts

Conclusion

ETW is back at a more attractive discount, lower than what it has averaged in the last decade. That could present a more opportune time to buy shares than our last update. The distribution trim seemed to be at least partly to blame for this widening discount, as the fund was flirting with a premium level just a couple of months ago.

ETW Discount/Premium History (CEFConnect)

So a distribution cut isn't all bad news, as it can create a better buying opportunity and leave the fund with a more manageable payout. More manageable generally means less detrimental to the fund in the long term.

For further details see:

ETW: Discount Widening After Latest Distribution Trim