URTH - ETW Vs. IGA: 2 Call-Writing Funds With A Global Tilt

2023-03-27 11:45:08 ET

Summary

- ETW and IGA are similar funds in the way they operate; they sell index or index ETF calls and hold a basket of equity positions with a global tilt.

- However, the positioning that they've chosen to take differs, and that's played a significant role in their past performance and should going forward as well.

- I hold positions in both, and I believe they can be good complementary investments when held simultaneously due to their differences.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 10th, 2023.

Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund ( ETW ) and Voya Global Advantage and Premium Opportunity Fund ( IGA ) are two funds trading at fairly attractive discounts. Additionally, they're two funds that, on the surface, might appear quite similar.

Both hold a portfolio of common stocks with a global tilt. They also will write calls against indexes, but IGA will also write calls against indexes and index ETFs. While that might not seem like a big difference on the surface, there can be an important difference between writing calls on an index and covered calls because an index can't be owned directly. The ETFs IGA is writing against aren't covered either because they don't own them. Therefore, they are selling naked calls.

We've discussed this in detail further previously , but the main important point to remember is that by being naked or not owning an index directly, they can produce potentially unlimited losses, in theory. However, we know in practice that isn't the case because both of these funds carry portfolios that mirror what these indexes and ETFs are going to be doing; in effect, they are indirectly being 'covered.'

With all that being said, these funds focus on two different market areas, which has had significant consequences on historical performance. While that doesn't guarantee future results, the portfolios are still designed very differently, indicating that future results will also be vastly different. If one incorporates positions in both funds, I believe it can provide sufficient diversification. Of course, that's if one is looking for a call writing global fund in the first place.

ETW Basics

- 1-Year Z-score: -1.05

- Discount: -6.52%

- Distribution Yield: 8.85%

- Expense Ratio: 1.11%

- Leverage: N/A

- Managed Assets: $957.4 million

- Structure: Perpetual

ETW will "invest in a diversified portfolio of common stocks and write call options on one or more U.S. and foreign indices on a substantial portion of the value of its common stock portfolio to seek to generate current earnings from the option premium."

The tax-managed focus comes in with the "fund evaluating returns on an after-tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the Fund." The investment policy is designed to achieve their main objective; "to provide current income and gains, with a secondary objective of capital appreciation."

IGA Basics

- 1-Year Z-score: -1.49

- Discount: -13.12%

- Distribution Yield: 9.15%

- Expense Ratio: 0.99%

- Leverage: N/A

- Managed Assets: $158.8 million

- Structure: Perpetual

IGA's investment objective is "a high level of income; capital appreciation is secondary." They intend to write " call options on indexes or ETFs, on an amount equal to approximately 50-100% of the value of the Fund's common stock holdings."

IGA is much smaller than ETW, which can mean less liquidity due to lower daily trading volume. That's something to consider if you want to take a large position or potentially attempt to trade in and out of the fund. There could be more limited opportunities to do so.

Performance Comparison

In a recent article, I highlighted why global positioning could be important in the first place. As some of us investors have only been investing in the last decade or so, we've only seen U.S. investments outperform. So it might come as a shock, but that hasn't always been the case. We just happen to be in a rather extended period where that has been happening.

Cycles of Global/U.S. Performance (JPMorgan)

Further, when looking at valuations from around the world, we can see that U.S. investments are particularly expensive relative to other international markets.

Global Valuations (JPMorgan)

A change in valuation could be enough to make international investments outperform going forward. Of course, that isn't guaranteed, but it gives us an idea of why international positions could be worth considering.

Now, between ETW and IGA, we've had a clear historical winner in the last decade. The outperformance of ETW has been quite clear and without any doubt. It wasn't even close on a total share price and total NAV return basis. IGA is the loser here.

YCharts

However, in the last year, we've seen something very different. This is a rolling 1-year period as of March 10th, 2023. We can see that IGA actually provided slightly positive results on both a total share price and NAV return basis. ETW had been the major laggard in this case. While this is only a short period of time, there could be a reason it could continue.

YCharts

This simply comes down to positioning, and so while on the surface, these funds are investing in global equities below that, they are quite different.

Value Vs. Growth

Roughly 45% of ETW's portfolio is invested outside of the U.S. IGA is a bit more concentrated in U.S. holdings, with only roughly 34% of their portfolio outside of the U.S. If you were looking for global funds with a sole focus outside the U.S., these two clearly wouldn't be it. That's why I mention "global tilt" because U.S. exposure is still quite dominant in their portfolio.

One wrinkle between the two that can have another impact is that ETW's overwrite policy is to run at nearly 100% being overwritten. IGA is a bit more flexible in targeting a 50% to 100% overwritten portfolio. IGA last reported being overwritten by 49.93%. However, we've seen this as low as 37% before - meaning, well below its target range.

However, the biggest factor comes down to value vs. growth investments. ETW's portfolio is heavily concentrated in tech weightings. Here's a look at the weightings as of the end of 2022. A specific period in time, but this is regularly the case for the fund carrying a higher weighting to tech.

ETW Sector Allocation (Eaton Vance)

With that, seeing the usual mega-cap tech names take commanding positions in the fund isn't necessarily shocking. Again, these are regular holdings over the years.

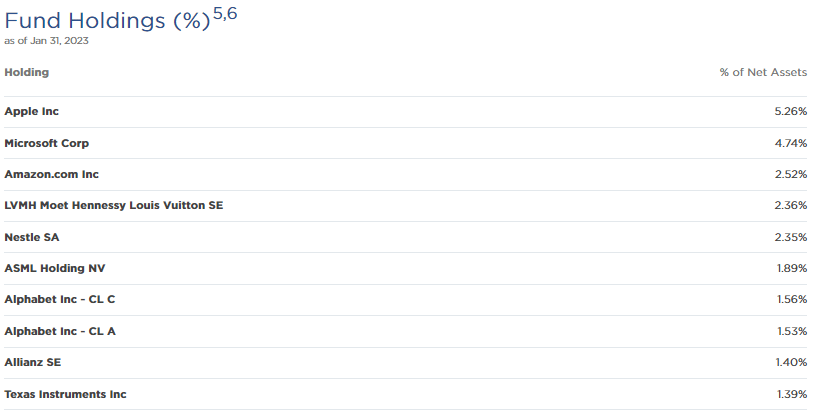

ETW Top Ten Holdings (Eaton Vance)

{kind=link}

When looking at IGA, we see a drastically different portfolio, one that is primarily value-oriented. Tech weightings aren't even breaching 7% of an allocation for this fund at this time.

IGA Sector Allocation (Voya)

With those sorts of weightings, it probably isn't too surprising to see the top ten names quite different relative to ETW. Perhaps what might be surprising is that, despite financials making up the largest weighting, we don't have a single financial stock in the top ten. Instead, we have healthcare behemoths represented in the top ten, reflecting the healthcare sector being the second-largest weighting in the fund.

IGA Top Ten Holdings (Voya)

Going back to performance here to help illustrate the performance difference due to portfolio position, ETW clearly underperformed IGA in the last year, as we saw above. However, it basically came in line with the S&P 500 ETF ( SPY ) and iShares MSCI World ETF ( URTH ). Those represent straight equity funds, with SPY being U.S.-focused and URTH providing some context for global investments. When we look at Invesco QQQ ( QQQ ), representing the Nasdaq 100 performance, we can see that ETFs do much more poorly.

YCharts

Their annual report also provides their own benchmarks, which can be more appropriate as they represent buy/write indexes. Therefore, they are representing the option writing that ETW and IGA do. In that case, we see ETW outperforming the CBOE Nasdaq 100 Buy/Write Index in 2022, the MSCI World Index, and the S&P 500 Index.

ETW Annualized Result Benchmark Comparison (Eaton Vance)

{kind=link}

Other Derivatives Help IGA

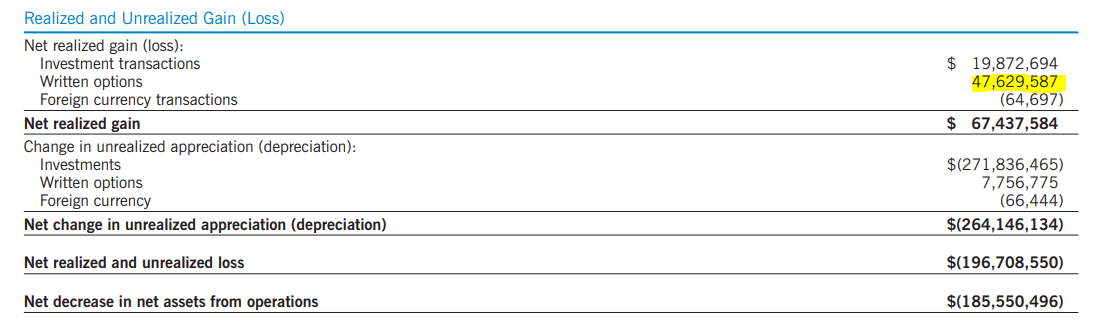

One other thing that IGA does that differs from ETW is they've been able to reap some significant benefits from foreign currency contracts. This comes down to different derivative contracts outside of the writing options, which is the main focus of both of these funds.

Here are the gains that IGA was able to produce on their forward foreign currency contracts, and I've also highlighted what they've been able to pull in for gains on their written options.

IGA Realized/Unrealized Gains/Losses (Voya)

{kind=link}

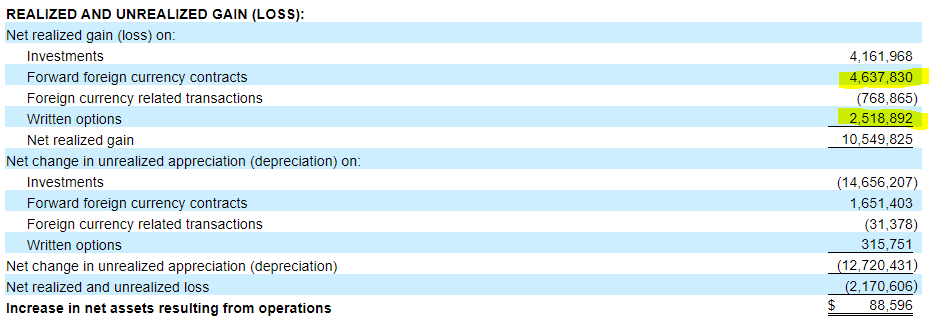

In this case, ETW only reflects other foreign currency transactions, which was a loss for both funds but not material. Meaning, they weren't involved with any forward foreign currency transactions that showed a benefit to IGA in a material way. However, we can highlight the gains they've been able to take in from writing options .

ETW Realized/Unrealized Gains/Losses (Eaton Vance)

{kind=link}

This can be important for both funds because they will rely on capital gains to fund their distributions.

IGA had net investment income distribution coverage of 35.26% for the six months that ended August 31st, 2022. ETW's NII distribution coverage for the year ended December 31st, 2022 came to 13.35%. This once again reflects the growth vs. value orientation of each fund. Naturally, IGA's portfolio produces larger relative yields, whereas ETW's growth portfolio takes the cash those companies have and reinvests it in themselves.

For IGA, the capital gain shortfall was $4.148 million, which was easily covered by their currency contracts and written options. That's without factoring in the investment gains realized.

The shortfall for ETW was $72.433 million, which the options written didn't cover. There was still a shortfall even after realizing gains from their underlying portfolio.

Overall, global investments were weaker-performing compared to the U.S., as we discussed above. That results in distribution cuts along the way for both funds. ETW was the latest to trim, doing so in 2022. The stronger results from IGA kept the yield more moderate.

YCharts

Going forward, both have NAV distribution rates of around 8%. That isn't at a critical level, so we shouldn't see distribution cuts soon, but that's subject to change based on the outcome of the broader equity picture too. Should we see a recession as expected later this year, we could definitely see distribution cuts.

That being said, with a call-writing strategy, they could be better positioned to take on such a decline. This is because these are capital gains that can be produced no matter the market direction.

Conclusion

Both are trading at fairly attractive discounts, with IGA sporting an absolute deeper discount.

YCharts

However, that tends to be the case over time, with the fund carrying a larger relative discount. So, on a relative basis, that's why both appear to be fairly attractive, as they're both trading under their decade-long average. The more recent distribution cut for ETW was the likely culprit for at least some of that pressure.

Going forward, the difference in portfolio positioning is why I believe it will come down to one's outlook if the growth vs. value story continues to favor value as it did in most of the last year. To start off 2023, we saw investors moving back into growth names. I believe it highlights how hard it can be to predict the future. Alternatively, it also highlights why I believe owning both funds can complement each other.

For further details see:

ETW Vs. IGA: 2 Call-Writing Funds With A Global Tilt