XYLD - ETY: A Very Reasonable Option-Income CEF For Purchase

2023-09-11 12:03:54 ET

Summary

- The Eaton Vance Tax-Managed Diversified Equity Income Fund has underperformed the stock market over the past year.

- The fund's strategy of writing call options against the S&P 500 Index may have contributed to its poor performance.

- Despite its underperformance, the fund still offers a high current distribution yield and is trading at a discount to its net asset value.

- The fund cut its distribution late last year, but it appears that the new one is easily sustainable.

- The fund has consistently outperformed the other Eaton Vance option-income funds, so it could be the one to buy.

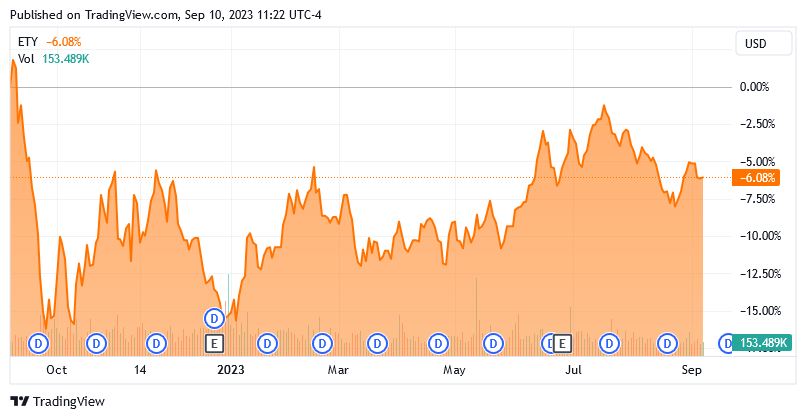

The Eaton Vance Tax-Managed Diversified Equity Income Fund ( ETY ) is a fairly popular closed-end fund that is used by investors who are seeking both a relatively high level of income and exposure to the upside potential of a common stock portfolio. Unfortunately, the fund has not performed especially well over the past year, as its share price is down 6.08% over the period:

{kind=link}

This is despite the fact that the stock market itself has been fairly strong over the same period. In fact, the S&P 500 Index ( SPY ) is up 11.27% over the same period, in direct defiance of interest rates and concerns that the United States might soon enter a recession. The poor performance of this fund is probably at least partly due to the strategy that this fund uses. As I pointed out in my last article on this fund, the Eaton Vance Tax-Managed Diversified Equity Income Fund writes call options against the S&P 500 Index, which will somewhat cap its potential gains during particularly strong markets. The fact that the fund had to cut its distribution back in November also did it no favors, particularly in an environment in which it is fairly easy to obtain an acceptable yield by sitting in a money market fund.

There may still be some reasons to consider purchasing this fund today. For example, the fund's 8.02% current distribution yield is still well above the risk-free rate as well as being above the rate of inflation. As such, this is one of the few assets in the market that boasts a positive real yield. That can be attractive for any income-seeking investor. In addition, the fund's shares are currently trading at a discount to the net asset value, so the price is not altogether unreasonable. Finally, this fund should be able to outperform the broader market index in the event of a stock market correction, which some analysts and experts think could occur in the near future.

Therefore, let us investigate and see if this fund could be a reasonable addition to your portfolio today.

About The Fund

According to the fund's webpage , the Eaton Vance Tax-Managed Diversified Equity Income Fund has the stated objective of providing its investors with a high level of current gains and current income. This is not particularly surprising for a closed-end fund. After all, the general way that a closed-end fund works is that it will pay out all of its investment profits to the shareholders in the form of distributions. This tends to result in a high level of current income because it results in fairly high distribution yields if the fund is successful in managing its portfolio. However, it can be difficult to get current income and current gains from an equity portfolio, and this fund invests primarily in common equities. In fact, as of the time of writing, 99.13% of the fund's assets are invested in common equities:

CEF Connect

As we all know, common stock does not always go up consistently. In fact, the S&P 500 Index was slightly down over the past month:

{kind=link}

The index was also down for the full-year 2022 period. While it is true that stocks will usually deliver positive returns over a long enough time frame, there are occasionally periods in which current gains are difficult to get. It is even more difficult to obtain income from a common stock portfolio, as common stocks almost always have incredibly low dividend yields. As of the time of writing, the S&P 500 Index yields 1.46%, and even the U.S. Utility Index ( IDU ), which is frequently considered to be an index of very high-yield stocks, only yields 2.68% right now. These yields are both well below the current rate of inflation as well as below the yield of a typical money market fund. Thus, we can quickly see that a common stock portfolio is a very unusual choice for a fund aiming to deliver a high level of current income to its shareholders.

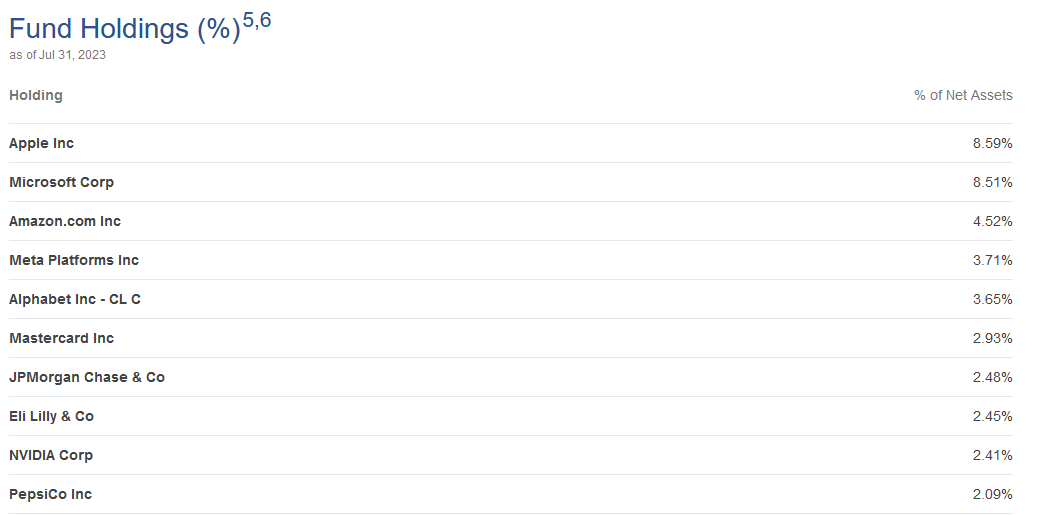

As is the case with most Eaton Vance funds, the portfolio of the Eaton Vance Tax-Managed Diversified Equity Income Fund is a very strange one for any fund targeting current income as one of its objectives. Here are the largest positions in the fund as of the time of writing:

{kind=link}

The reason why this is a strange portfolio for an income-focused fund is because most of these stocks have very low yields:

| Company |

| Current Dividend Yield |

| Apple Inc. ( AAPL ) |

| 0.54% |

| Microsoft Corp. ( MSFT ) |

| 0.81% |

| Amazon.com Inc. ( AMZN ) |

| N/A |

| Meta Platforms Inc. ( META ) |

| N/A |

| Alphabet Inc. ( GOOG ) |

| N/A |

| MasterCard Inc. ( MA ) |

| 0.55% |

| JPMorgan Chase & Co. ( JPM ) |

| 2.78% |

| Eli Lilly & Co. ( LLY ) |

| 0.77% |

| NVidia Corp ( NVDA ) |

| 0.04% |

| PepsiCo Inc. ( PEP ) |

| 2.87% |

A ten-year Treasury is yielding 4.27% as of today. A regular money market fund is yielding 5% or higher. Clearly, this fund is not going to be able to provide its investors with any sort of a reasonable yield simply by collecting dividends from this portfolio.

The twist comes from the fact that this fund is using an option strategy as a way to generate income. I explained this in my previous article on the fund:

The fund invests in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend-paying stocks and writes (sells) S&P 500 Index call options with respect to a portion of the value of its common stock portfolio to generate cash flow from the options premium received.

I honestly do not know how this fund can claim to favor dividend-paying stocks given the above portfolio. As we can clearly see, 11.88% of the portfolio is invested in Amazon, Meta Platforms, or Alphabet and not one of these pays a dividend. This does not even consider the fact that the above charts only show the ten largest positions in the fund and so deliberately exclude the fact that the fund will undoubtedly be invested in other non-dividend-paying stocks. Thus, despite the fund's claim that it is focusing its attention on dividend-paying stocks, it does not appear that this is the case.

The fund does, however, appear to be attempting to create a portfolio that has a similar performance to the S&P 500 Index. It is trying to do it using fewer stocks though as the fund only has seventy positions as of the time of writing. Here are the largest positions in the S&P 500 Index:

State Street

We certainly see a great deal of similarity here. The only companies in the largest index weightings that are not present in the fund are Tesla ( TSLA ), Berkshire Hathaway ( BRK.B ), and UnitedHealth Group ( UNH ). Alphabet ( GOOGL ) Class A shares are also not included in the fund's largest positions, although the Class C shares are. As I noted in the previous article, the fund is actually writing naked call options, which can be a very risky strategy. It will want a portfolio that should perform similarly to the S&P 500 Index in order to reduce its risk. With that said, I do not know why it does not assemble a portfolio of dividend-paying stocks along with an S&P 500 Index ETF and just write call options against that exchange-traded fund. That strategy would probably result in a higher income for the fund. It may not be able to match the capital gains potential, however. That was especially true over most of the past decade as long-duration non-dividend paying stocks outperformed value-oriented blue chips.

The fund's largest positions have changed a bit since the last time that we discussed it. In particular, the Eaton Vance Tax-Managed Diversified Equity Income Fund removed its positions in UnitedHealth Group, Proctor & Gamble ( PG ), and Chevron ( CVX ) from the largest weightings in the portfolio. In their place, we have Meta Platforms, JP Morgan Chase, and Nvidia. This reinforces the belief that the fund's management is trying to outperform the S&P 500 Index as these stocks have benefited from the artificial intelligence mania that was driving the market upward over the first half of 2023. This buying activity in a handful of stocks believed to be driving artificial intelligence forward came at the expense of more value-oriented plays such as the ones that were removed from the largest positions list.

Performance Comparison

Eaton Vance is somewhat famous for its option-income funds, such as the Eaton Vance Tax-Managed Diversified Equity Income Fund. The fund house has a number of funds that all use nearly the same strategy:

- Eaton Vance Tax-Managed Diversified Equity Income Fund.

- Eaton Vance Tax-Managed Buy-Write Income Fund ( ETB ).

- Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ).

- Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund ( ETW ).

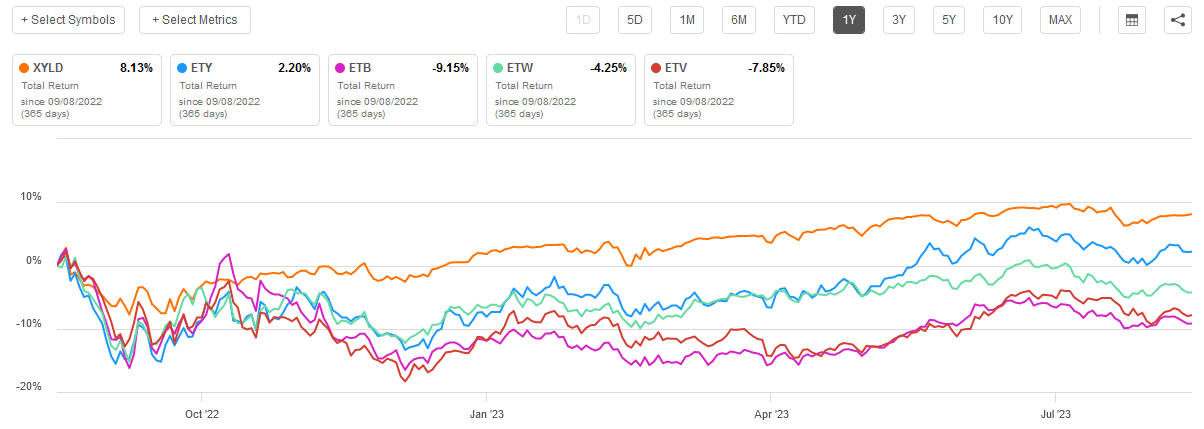

Admittedly, Eaton Vance's quick reference guide about these funds makes the claim that the first fund, which is the primary topic of this article, is different from the other three. In particular, this document claims that it invests in high-yielding stocks while the other three basically just hold portfolios that are pretty close to the index itself. However, as we have already seen, the Eaton Vance Tax-Managed Diversified Equity Income Fund is most certainly not investing in high-yielding stocks. In fact, only two of the largest positions in the fund have a yield above the S&P 500 Index. As such, we should be able to compare these four funds against one another to see which one has historically given its investors the best results. For the purposes of this analysis, I will add the Global X S&P 500 Covered Call ETF ( XYLD ), which mechanically buys the index and then writes an at-the-money call option against it on a monthly basis.

Here is how the five assets compared over the past year:

{kind=link}

Needless to say, this is a very bad showing for all of the Eaton Vance closed-end funds as they all underperformed the comparable index fund. However, the Eaton Vance Tax-Managed Diversified Equity Income Fund did manage to deliver the best showing.

In many cases, closed-end funds have higher yields than their comparable indices. As a result, these funds can sometimes deliver much better total returns than their price action would indicate. This is the case here, but none of these funds has a higher yield than the index. This actually results in the difference between the total return of the index fund and the total return of the Eaton Vance funds being much greater than looking at the price action alone:

{kind=link}

Once again, we can see that the Eaton Vance Tax-Managed Diversified Equity Income Fund managed to outperform its sister funds, but it still underperformed the index by quite a lot. Another point to note is that only this fund and the index managed to deliver positive total returns over the period.

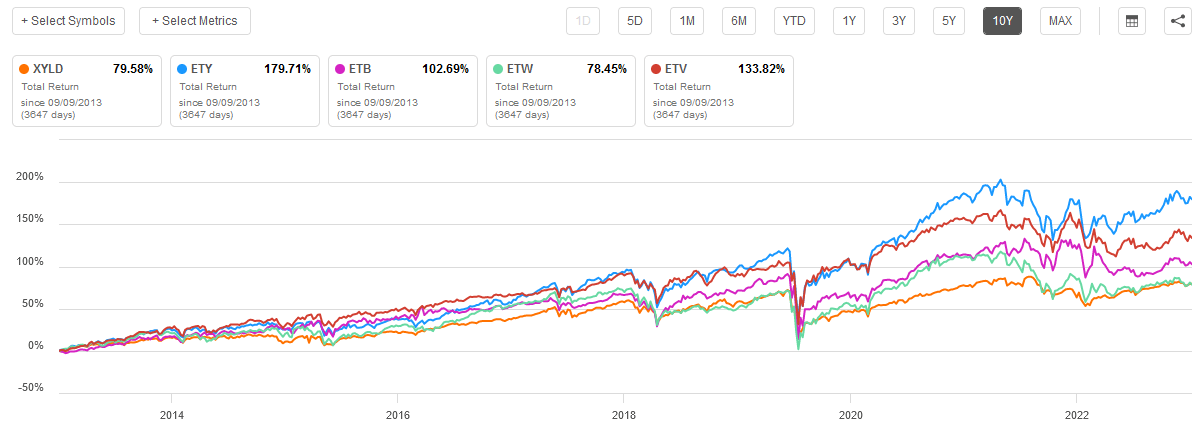

Fortunately, things do change a bit when we look at a much longer period. For example, here is the same total return chart over the trailing ten-year period:

{kind=link}

This clearly illustrates the advantages that active management can provide when it comes to options strategies. Three of the four Eaton Vance funds managed to outperform the index over the period. Only the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund failed to beat the index, and it did not lag it by very much.

Once again, we see that the Eaton Vance Tax-Managed Diversified Equity Income Fund proved to be the best performer over the long term on a total return basis. While past performance is certainly no guarantee of future results, it does appear that this fund is probably the best choice out of any of Eaton Vance's option-income funds for most investors, with a possible exception being those investors who are only planning to hold their positions for a very short period of time. However, most income-focused investors do not engage in such short-term activity. As such, this fund might be worth considering for those interested in earning income through its option-focused method.

Distribution Analysis

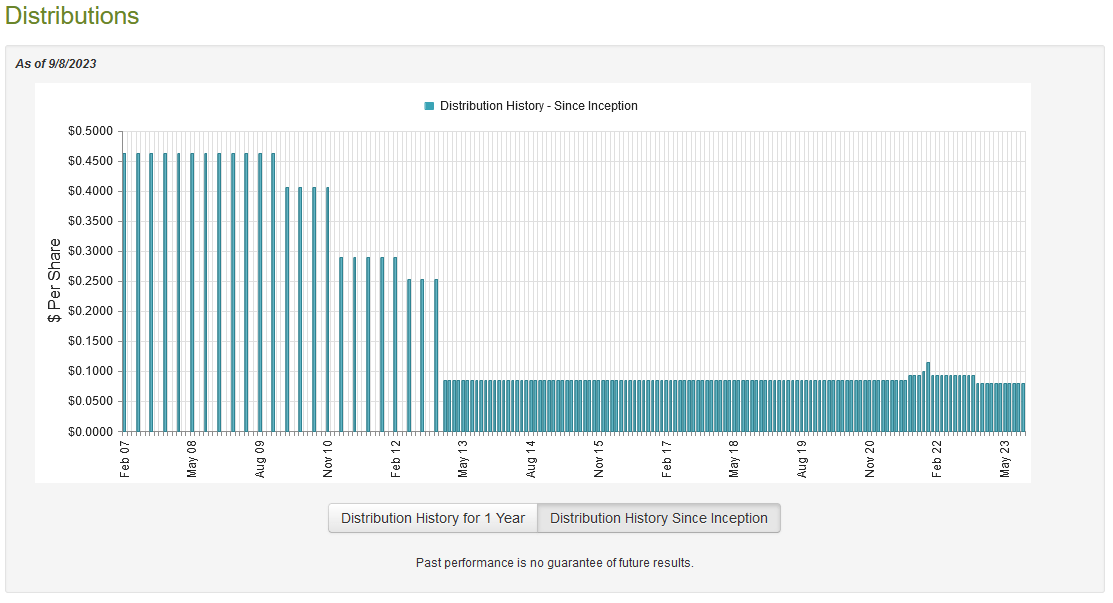

As mentioned earlier in this article, the primary objective of the Eaton Vance Tax-Managed Diversified Equity Income Fund is to provide its shareholders with a very high level of current income. In order to achieve that, it invests in a portfolio consisting mostly of domestic equities. The fund then writes call options against the S&P 500 Index, hoping to collect the premium as a source of income without the option becoming in the money. The fund might also be able to realize some capital gains from the portfolio. The options strategy in particular can result in a very high yield when it works properly, and the potential for realized capital gains is just icing on the cake. The fund then pays its investment profits out to its investors. This can be expected to result in the fund having a very high yield, which is indeed the case. It currently pays a monthly distribution of $0.0805 per share ($0.966 per share annually), which gives it an 8.02% yield at the current price. The fund used to be pretty consistent with its distribution, but it did have to cut it back in November of 2022:

{kind=link}

We do see that the fund previously increased its distribution in response to the euphoria that the market experienced in 2021 when all of the newly printed pandemic stimulus money flooded it. Thus, some might see the cut as simply the fund reducing its payout to something approaching more usual levels. However, the recent distribution cut reduced its payout to below the level that it had prior to that distribution rise. The current monthly payout is the lowest that this fund has ever possessed. Overall though, this is still a better distribution history than most other closed-end funds possess and it might be sufficient to appeal to those investors that are seeking a stable and consistent source of income to use to pay their bills or finance their lifestyles.

As is always the case, we do want to ensure that the fund can actually afford the distribution that it pays out. After all, we do not want to be the victims of another distribution cut, as that would reduce our incomes and almost certainly cause the fund's share price to decline.

Fortunately, we do have a fairly recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is nice because this document should give us some idea of how well the fund was able to take advantage of the strong market that existed during the first half of this year. It is also a much newer document than the one that we had available the last time that we discussed this fund, so it should provide us with better insight into exactly how well it is managing to cover its distribution at the new lower level.

During the six-month period, the Eaton Vance Tax-Managed Diversified Equity Income Fund received $14,235,601 in dividends from the assets in its portfolio. Surprisingly, the fund had no interest income, so the received dividends constituted all of its investment income during the period. The fund paid all of its expenses out of this amount, which left it with $4,631,001 available for shareholders. Obviously, that was not nearly enough to cover the distributions that the fund paid out during the period. This fund paid out a total of $75,915,689 in distributions during the six-month period. At first glance, this might be concerning as the fund clearly failed to cover its distribution solely with net investment income.

With that said, the fact that the distribution was larger than the fund's net investment income is not as big of a problem for equity funds as it is for fixed-income funds. This is because equity funds tend to get a lot of their investment profits via capital gains, which are not included in net investment income. This fund also receives money from option premiums, which are also not included in net investment income. During the six-month period, the fund reported net realized gains of $73,894,023 and had an additional $80,668,302 net unrealized gains. Overall, the fund's net assets increased by $86,475,372 after accounting for all inflows and outflows during the period. In other words, this fund actually performed well enough during the first six months of its fiscal year to cover the distribution for the entire fiscal year. Unless it suffers very large losses over the next few months, it should not have any trouble sustaining its distribution for quite some time.

Valuation

As of September 7, 2023 (the most recent date for which data is currently available), the Eaton Vance Tax-Managed Diversified Equity Income Fund has a net asset value of $12.44 per share but the shares currently trade for $12.05 each. This gives the fund's shares a 3.14% discount on net asset value at the current price. This is a bit better than the 2.40% discount that the shares have averaged over the past month. Thus, the current price seems to be quite reasonable.

Conclusion

In conclusion, the Eaton Vance Tax-Managed Diversified Equity Income Fund seems to be doing a reasonably good job at delivering a solid performance for its shareholders, but it is not following the dividend-focused strategy that is discussed on its website. This has not really hindered its performance though as this is the best-performing of Eaton Vance's domestic option-income funds when measured on a total return basis. It has also done much better than a mechanical buy-write strategy used by a similar index. That is not necessarily surprising though as option strategies are difficult to execute without the benefit of active management. The recent distribution cut is not likely to win the fund many friends, but it is not having any difficulty covering the current payout so we probably do not need to worry about another cut in the near future. Overall, this fund is probably a very reasonable purchase right now.

For further details see:

ETY: A Very Reasonable Option-Income CEF For Purchase