MCN - ETY: Riskier Than Some Peers But Not Really Too Bad

2023-11-15 13:33:05 ET

Summary

- Eaton Vance Tax-Managed Diversified Equity Income Fund uses an options strategy to generate income for investors.

- The ETY closed-end fund has underperformed the S&P 500 Index in recent months but has generally been more stable during market downturns.

- The ETY fund pays a monthly distribution with an 8.36% yield, although it has cut its distribution in the past.

- The fund is technically writing naked call options, which is a lot riskier than a covered call option strategy.

- ETY appears to be covering its distribution and trades at a discount on NAV.

The Eaton Vance Tax-Managed Diversified Equity Income Fund ( ETY ) is a closed-end fund, or CEF, that is widely employed by investors who are seeking to earn a very high level of income from the assets in their portfolio. The fund is reasonably decent at this task, although it only has an 8.36% yield at the current price. That is clearly unable to compete against the yields that can be found amongst fixed-income funds, but this one is not a fixed-income fund. Rather, the Eaton Vance Tax-Managed Diversified Equity Income Fund uses an options strategy to generate a high level of income for its investors. The fund’s yield is acceptable among funds like this:

| Fund |

| Current Distribution Yield |

| Eaton Vance Tax-Managed Diversified Equity Income Fund |

| 8.36% |

| Madison Covered Call and Equity Strategy Fund ( MCN ) |

| 10.27% |

| BlackRock Enhanced Capital and Income Fund ( CII ) |

| 6.65% |

| First Trust Enhanced Equity Income Fund ( FFA ) |

| 7.34% |

| Virtus Dividend, Interest, & Premium Strategy Fund ( NFJ ) |

| 8.67% |

As we can see, investors will not really be giving up too much yield by choosing the Eaton Vance Tax-Managed Diversified Equity Income Fund compared to one of its peers. The exception to this is obviously the Madison fund, but that one also tends to trade at a premium price, which presents a problem for more conservative investors.

As regular readers can undoubtedly recall, we last discussed this fund back in September. Its return since that time has certainly left something to be desired, as the fund has delivered its investors a negative 3.68% total return since that date. This is worse than the S&P 500 Index ( SP500 ), which has been flat over the same period:

{kind=link}

If we look at solely the fund’s share price performance, it has done even worse. However, the distribution is such a core component of the investment return of most closed-end funds that we should not look just at the share price performance when evaluating them.

We do generally see what we would expect from an option-income fund in the chart above though. As I noted in my previous article on this fund, as well as in a variety of articles over the years, option-income funds usually outperform the market during flat or bear markets but underperform when market prices are rising because the written options put a cap on the gain. This is generally what we see above, as this fund did not really start to underperform until the S&P 500 Index started to appreciate in value. As such, it is a trade-off, as this fund will probably be somewhat more safe and reliable than buying the index but investors will also have to sacrifice some potential gains.

About The Fund

According to the fund’s website , the Eaton Vance Tax-Managed Diversified Equity Income Fund has the primary objective of providing its investors with a high level of both current income and gains. This makes sense for an option-income fund, but unfortunately, the website does not provide any information about how the fund will accomplish this goal. This is one of the annoying things about Eaton Vance funds, as the generally spartan webpage means that you have to dig a bit deeper to figure out what the fund’s basic strategy is than would be necessary with funds from other sponsors.

Fortunately, the fact sheet provides more in-depth information about the fund’s strategy than the website. Here is what that document has to say about it:

The Fund invests in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend paying common stocks and writes (sells) S&P 500 Index call options with a respect to a portion of the value of its common stock portfolio to generate cash flow from the options premium received. The Fund evaluates returns on an after tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the fund.

In other words, this fund is writing index call options, but it holds a portfolio of ordinary common equities. As such, it is technically writing naked call options, which can be a very risky strategy. After all, naked call options can expose the fund to potentially unlimited losses because common stocks have no theoretical maximum value. Thus, a worst-case scenario could involve the fund having to pay a potentially unlimited price to acquire the index to deliver to the option buyer upon the exercise of the option. Granted, index options are typically cash settled so in reality the fund could potentially just have to pay an unlimited amount of money to the option buyer upon exercise of the option. That is a much riskier strategy than writing covered call options, as most option-income funds from other fund houses do.

Basically, what this fund is doing is writing call options against the SPDR S&P 500 Index ETF Trust ( SPY ) without owning the index fund. This aspect of its strategy could certainly concern those investors who are highly concerned about risk mitigation or avoiding losses. This is a category that would include most retirees, who might actually find it easier to sleep at night with something like the Eaton Vance Enhanced Equity Income Fund ( EOI ) instead. That fund writes covered call options, so the worst-case scenario is simply that it has to sell the option buyer stocks that it already owns.

In an attempt to offset the risks inherent in writing naked call options, the Eaton Vance Tax-Managed Diversified Equity Income Fund invests in a portfolio of common equities that it hopes will deliver a similar performance to the S&P 500 Index. Here are the largest positions in said portfolio:

{kind=link}

This portfolio certainly goes against the fund’s statement in its fact sheet that it “emphasizes dividend-paying stocks.” After all, many of these companies either do not pay a dividend or have such a low dividend yield that they may as well not pay a dividend. We can see that here:

| Company |

| Current Yield |

| Microsoft ( MSFT ) |

| 0.81% |

| Apple ( AAPL ) |

| 0.51% |

| Amazon.com ( AMZN ) |

| N/A |

| Alphabet ( GOOG ) |

| N/A |

| Meta Platforms ( META ) |

| N/A |

| Mastercard ( MA ) |

| 0.57% |

| Eli Lilly & Co. ( LLY ) |

| 0.74% |

| NVIDIA Corp. ( NVDA ) |

| 0.03% |

| Walmart ( WMT ) |

| 1.36% |

| AbbVie ( ABBV ) |

| 4.49% |

The S&P 500 Index in aggregate has a 1.45% trailing twelve-month yield right now, so all of these companies except for AbbVie are lower than the index. A fund that is looking to emphasize dividend-paying stocks would certainly not be investing in these companies.

With that said, this portfolio does make sense for the current environment if the fund is trying to offset the risks inherent in the index option-writing strategy. As the Motley Fool points out , most of the returns of the S&P 500 Index this year have been due to the appreciation of seven stocks. These are Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla ( TSLA ), and Meta Platforms. Six of these seven stocks are included in this fund’s largest positions, with Tesla being the sole absentee company. Visual Capitalist makes a similar observation, pointing out back in May that twenty stocks (including the seven just mentioned) were responsible for basically all of the S&P 500’s total return during the first half of the year.

Thus, it makes sense for the fund’s portfolio to include many of these companies among its largest positions, even though they are terrible from a dividend or yield perspective. The fund is trying to deliver a return that is comparable to the S&P 500 Index using only 65 stocks. If the portfolio underperforms the S&P 500 Index by too much, then the options strategy could result in very large losses. This is one unfortunate problem with this fund’s strategy. An ordinary covered call strategy would probably work better from a risk management perspective, due to the simple fact that the fund can invest in any stocks that it wants and then write options against those stocks with a minimal level of risk. At least, such a strategy would allow for much more sector diversity across the portfolio.

Fortunately, the fund does have more sector diversity than might be expected given the concentration of technology companies in the top ten holdings list. The fact sheet states that only 27.75% of the fund’s assets are invested in the information technology sector:

Fund Fact Sheet

The fact sheet’s index weightings appear to be outdated. As of November 14, 2023, the information technology sector accounts for 29.17% of the S&P 500 Index:

State Street

The fact sheet is simply dated “3Q23” so the increase in the information technology sector in the S&P 500 Index came over the past month or two. This reinforces the statement that was made earlier about the overwhelming majority of the index’s returns coming from just a handful of technology stocks.

Fortunately, the fund does include these stocks so it should benefit from this appreciation, even if they do very little in terms of the provision of income that the fund can pay out to its shareholders. The income component for this fund comes mainly from the option premiums that it receives whenever it writes call options against the index.

Recent Performance

As mentioned in the introduction, the Eaton Vance Tax-Managed Diversified Equity Income Fund has generally underperformed the S&P 500 Index over the past two months. However, this is less true when we look at the performance of the fund’s portfolio. My previous article on this fund was written on September 11, 2023. Here is how the fund’s market price and portfolio have compared to the S&P 500 Index on a total return basis since that time:

{kind=link}

We can see that the Eaton Vance Tax-Managed Diversified Equity Income Fund’s portfolio did underperform the S&P 500 Index during the period of recent strength that the market experienced, which is largely what we would expect based on its strategy. However, its underperformance over the past two months was not nearly as bad as the share price would have you believe. The fund’s portfolio only lost 0.96% over the period, but anyone who bought the fund’s shares on the date that my previous article was published lost 3.68%. That could actually present a buying opportunity for new investors right now, as the fund’s shares are clearly not performing as well as they should be. We will discuss this in more detail later in this article.

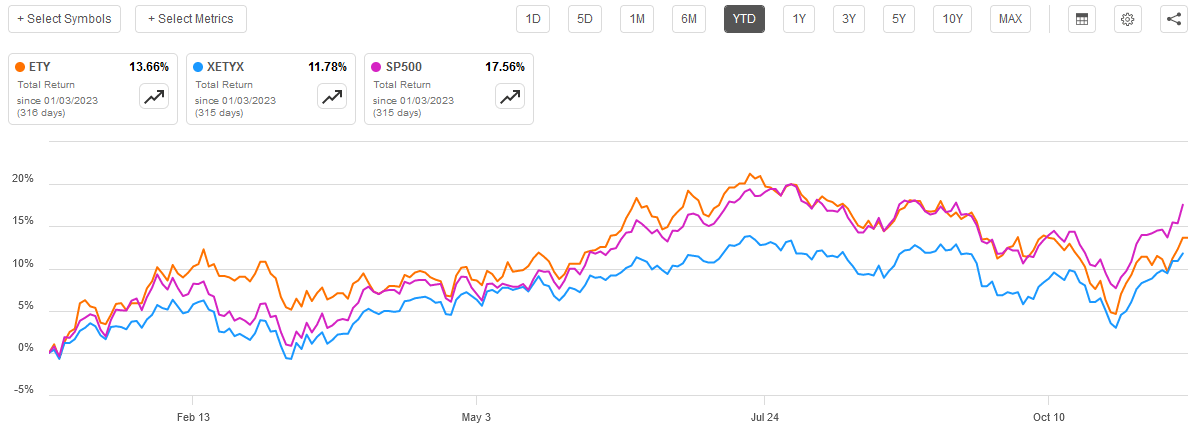

It could be more instructive to look at the performance of the fund year-to-date against the index, however. After all, most people who are reading this are probably not the type to go in and out of an asset on a whim. In addition, this has been a very interesting year for the market as we have witnessed both euphoria (during the first half of the year as well as over the past three weeks or so) as well as a bear market characterized by investors dumping pretty much everything. As such, a look at the fund’s year-to-date performance should give us a good idea of how well it manages to perform in any market environment. Here is the same chart as above, this time extended to cover January 1, 2023, until today:

{kind=link}

This is interesting, as the fund’s share price performance has generally been better than the actual performance of its portfolio. This is concerning as it is a sign that the fund’s shares have become more expensive than they were at the start of the year. The fund’s shares still underperformed the S&P 500 Index though.

We also see exactly what we would expect to see from an options strategy. For example, notice how the fund’s portfolio tends to be much more stable than the index. It does not appreciate nearly as much during bull runs, but it also does not decline as much when the index falls. That is something that could make this fund rather appealing to someone who is simply looking to preserve their assets while generating a reasonably respectable amount of income from their assets.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Tax-Managed Diversified Equity Income Fund is to provide its investors with a very high level of current income and current gains. This basically means that the fund is looking to generate a lot of money in the short term that can be paid out to the shareholders. In order to accomplish this task, the fund has constructed a portfolio of common stocks that is designed to somewhat resemble the S&P 500 Index. It then writes call options against the index in order to generate income via the options premiums. It may also collect dividends from the companies in the portfolio as well as realize capital gains from stock sales. The fund pools the money that it collects from these various sources and then pays it out to the shareholders, net of the fund’s expenses. It might be expected that this would result in the fund having a fairly high yield.

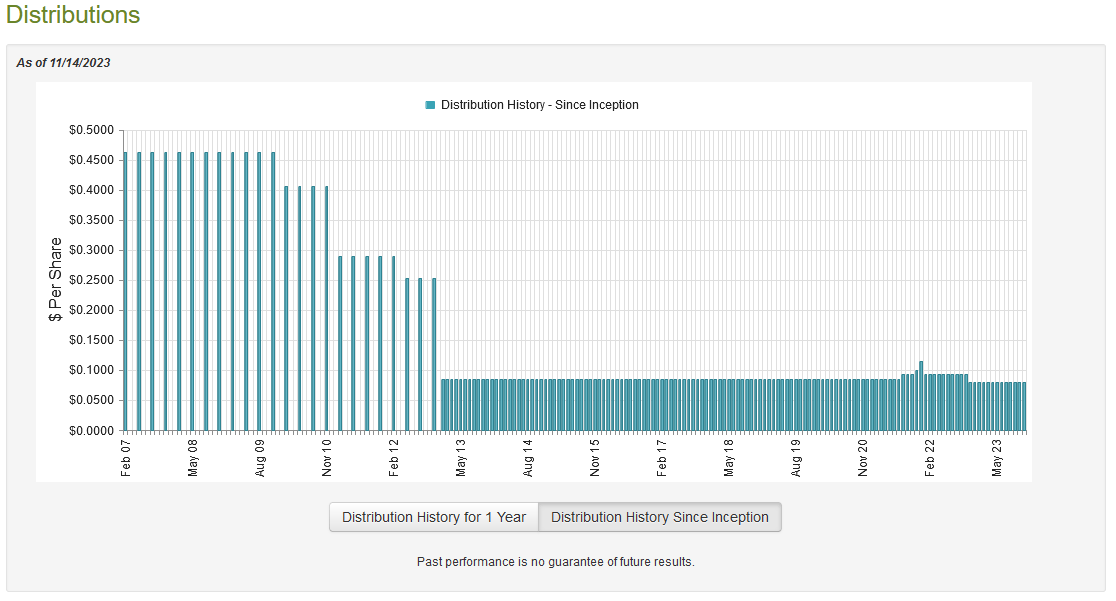

This is indeed the case, as the Eaton Vance Tax-Managed Diversified Equity Income Fund pays a monthly distribution of $0.0805 per share ($0.966 per share annually), which gives it an 8.36% yield at the current share price. That is a reasonable yield, although it certainly cannot compare with fixed-income funds. In the past, this fund was very consistent with respect to its distribution, but it has fallen off somewhat in recent years:

{kind=link}

As we can see, the fund was quite consistent over most of the pre-pandemic period. However, it then raised its distribution in response to the euphoric market of 2021 but was then forced to cut it late last year when the higher payout proved to be unsustainable. We have discussed this situation in past articles on the fund and do not need to repeat it here. The current distribution is just a bit below the $0.0843 per share per month that the fund paid out prior to the pandemic so it is still more stable than most funds over the long-term.

As I have pointed out before, anyone who is buying the fund’s shares today will not be impacted by actions that the fund has taken in the past. Rather, they will simply receive the current distribution at the current yield. As such, the most important thing today is how well the fund can sustain its current distribution. We should have a look at the fund’s finances to determine how well it can accomplish that task.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, it will not include any information about the fund’s performance over the past six months. That is unfortunate because it would have been nice to see how well this fund handled the bear market that ran from July until late October. A look at the fund’s net asset value suggests that it held out pretty well until October:

{kind=link}

We do not have the financial documents to reinforce or disprove this conclusion, however.

During the six-month period, the Eaton Vance Tax-Managed Diversified Equity Income Fund received $14,235,601 in dividends from the assets in its portfolio. It received no interest income, rehypothecation income, or income from any other source. Thus, the fund’s dividends received constituted the entirety of its total investment income during the period. The fund paid its expenses out of this amount, which left it with $4,631,001 available for the shareholders. That was obviously nowhere close to enough to cover the distributions that the fund actually paid out. This is a fairly large fund, and its distributions totaled $75,915,689 during the six-month period. At first glance, this may be concerning as the fund’s net investment income was nowhere close to enough to cover the distributions.

The fund does have other methods through which it can obtain the money that it needs to cover the distributions, however. For example, it receives premiums from the options that it sells. This money is not considered to be part of net investment income, but it clearly represents money coming into the fund that could be paid out to the shareholders. In addition, the fund might be able to realize capital gains from the stocks in its portfolio. This is also not part of net investment income, but it can still be paid out to shareholders. Fortunately, this fund enjoyed a great deal of success at these tasks during the period. The Eaton Vance Tax-Managed Diversified Equity Income Fund reported net realized gains totaling $73,894,023 and had another $80,668,302 in net unrealized gains. Overall, the fund’s net assets went up by $86,475,372 over the period. This is a clear sign that the fund did manage to cover its distribution.

As I have pointed out a few times in the past, unrealized gains can quickly be erased by any correction in the market. As such, we should not count on them to support a fund’s distribution. Fortunately, we do not have to in this case, as the fund’s net investment income plus net realized gains totaled $78,525,024 over the six-month period. That alone was sufficient to cover the distribution during the six-month period. Thus, the fund’s distribution seems to be fine based on this information. That does not necessarily mean that the fund managed to fully cover the distribution during the second half of the year, but the generally stable net asset value does provide some reasons for optimism. This fund is probably fine overall.

Valuation

As of November 14, 2023, the Eaton Vance Tax-Managed Diversified Equity Income Fund has a net asset value of $12.43 per share but the shares currently trade for $11.60 each. This gives the fund’s shares a 6.68% discount on net asset value at the current price. That is a better price than the 5.66% discount that the shares have traded at on average over the past month. As such, the current price looks like a reasonable entry point for anyone who wants this fund.

Conclusion

In conclusion, the Eaton Vance Tax-Managed Diversified Equity Income Fund is an interesting option-income fund that investors may want to use to earn a high level of income. The fund is technically using a risky options strategy, but as long as the fund’s portfolio delivers a similar performance to the S&P 500 Index, it should be fine. The fund is heavily weighted to technology companies that do nothing to provide it with income, but the index itself also has this problem and the fund cannot allow its portfolio’s performance to differ too much from the index. While the fund’s distribution cut last year certainly reduced its appeal to some income investors, it has been able to cover the payout at the new level. The shares also trade at a discount to their intrinsic value.

The biggest problem here is that Eaton Vance Tax-Managed Diversified Equity Income Fund’s strategy is riskier than that of other covered call funds and the fact that it is forced to invest in very low-yielding assets could make it harder for the fund to generate income than some of its peers that only write options against individual stocks.

For further details see:

ETY: Riskier Than Some Peers, But Not Really Too Bad