PEP - ETY: Valuation Comes Down To A Better Level

Summary

- ETY enjoyed trading at some premiums in recent years, but the distribution cut brought it back down to flirt with a discount.

- This fund is more attractively valued at a discount as, historically, it has exhibited trading more at a discount than a premium.

- Waiting for an even further discount before pouncing on this one could be wise, but the distribution yield remains attractive despite the cut for income investors.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 18th, 2023.

Like most of Eaton Vance's equity funds, Eaton Vance Tax-Managed Diversified Equity Income Fund ( ETY ) didn't escape the chop. As I've mentioned on several of the other funds, that's mostly just opened up an opportunity rather than something investors should run away from. In this case, we see once again that the fund was trading at more elevated premiums but is now going back toward discount territory.

It's important to remember that the actual distribution yield doesn't dictate the returns going forward. They'll rely on capital gains to fund their distribution as an equity fund. Of course, they also have the options writing overlay on indexes that can also help generate capital gains. However, the ultimate direction of returns will come from how the underlying portfolio performs and the income it generates.

So when a fund cuts its distribution, it isn't as if now the expected returns going forward are reduced. If anything, it could mean stronger results going forward as they erode less of their capital away. By paying out a more sustainable distribution, they'll have more assets to rebound with when it eventually occurs.

The Basics

- 1-Year Z-score: -1

- Discount: 0.17%

- Distribution Yield: 8.42%

- Expense Ratio: 1.07%

- Leverage: N/A

- Managed Assets: $1.801 billion

- Structure: Perpetual

ETY is a fairly simple fund on the surface; the fund's policy is to "invest in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend-paying stocks and writes (sells) S&P 500 Index call options on a portion of the value of its common stock portfolio to generate current cash flow from the options premium received." Their objective with this strategy is to "provide current income and gains, with a secondary objective of capital appreciation."

An expense ratio of around 1% is quite low for a closed-end fund. That being said, it is fairly normal for Eaton Vance funds and BlackRock ( BLK ) option-based funds. ETY doesn't employ leverage, so with volatility and interest rates rising, there is no additional damage being done to the fund - at least on that front.

Performance - Discount Appears

It's been almost a year since we covered ETY. Since that time, the fund has put up comparable results to the S&P 500.

ETY Performance Since Prior Update (Seeking Alpha)

In this case, the fund is targeted toward the S&P 500. However, instead of just weighing its portfolio similar to the index, they also have an options strategy. They write calls against the index to generate option premium. In a down year, we should expect outperformance as these premiums are produced to offset the overall decline.

Of course, it isn't the most defensive strategy, so with the deep losses that we saw in something like 2022, it isn't going to change the end result completely. It generally has been the case with the other option writing funds we follow. So seeing similar or even slightly reduced results here is, admittedly, disappointing as they failed to meet my expectations in at least the last year.

When looking at their annual report for the fiscal year-end October 31st, 2022, we see that options premiums contributed a healthy portion of capital gains.

{kind=link}

So, in this case, it would appear that positioning and position sizing could have been the culprit. The higher expense ratio would have also contributed to the end result. While it's a relatively lower expense ratio, it's still higher than the expense ratio of zero on an index.

What an index can't offer, though, is investing in a fund at a discount. The discount today for ETY isn't anything that's screaming a buy. However, it is something worth keeping an eye on. It's also much more attractively priced than just a few months ago at a large premium. Getting to the average discount of the last decade still requires a bit of a drop from here.

Ycharts

Distribution - Options Writing Helps Provide Gains

No one likes distribution cuts, but it also doesn't automatically mean it's time to sell. What might make this cut sting more than usual is that the EV line-up of funds went through last year and increased most of the distributions for their funds. It almost seems as if investors would have been happier with no raise rather than a short-lived raise. I can sympathize with that, too, as consistency and predictability are important for income investing.

{kind=link}

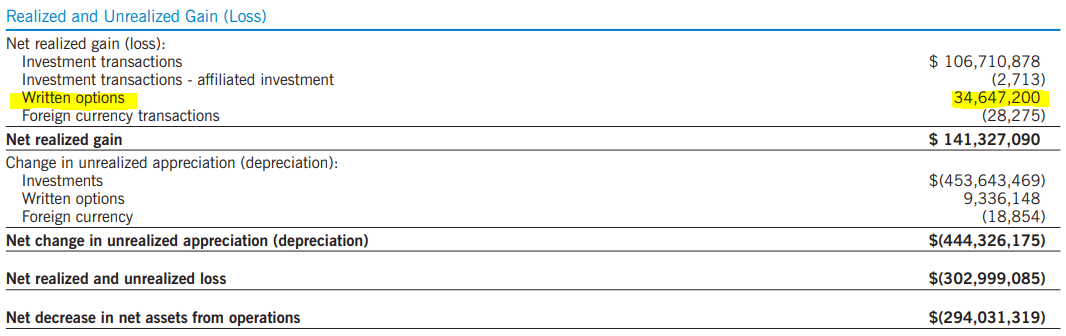

However, funding their distributions requires a sizeable amount of capital gains. In the last fiscal year, net investment income covered only around 5.15% of the $173,983,563 paid out to shareholders. Including the $141.327 of capital gains realized in the fund meant that coverage was light. As we showed above, of those capital gains generated, around $34.5 million was from option premiums.

{kind=link}

Options premiums can be collected in good times, bad times and the in-between times. So that can sometimes be a more stable source of capital gains for a fund to distribute.

That being said, in good years, the strategy can lose money since they write against indexes. When writing options against indexes, you can't own the underlying directly, so you aren't technically "covered." It involves cash-settled trades, so cash can leave the fund if the index rises too much.

In order to limit potentially unlimited losses, you invest in the components that make up the underlying portfolio. That's why ETY's portfolios are going to be larger, familiar names that we see in the S&P 500 Index. In that way, the fund is hedged as if they are losing on its options strategy, which means its underlying portfolio is winning and vice versa.

That's also why call-writing funds such as ETY can underperform in years when the markets are rallying. It's also why we should expect outperformance during down years, and seeing ETY's performance in the last year is disappointing, as mentioned above. Simply put, the index isn't writing options and collecting that premium, so the premium should be reducing the declines experienced. That wasn't the case, as the underlying portfolio lagged the benchmark.

How option writing impacts the portfolio is important to understand because when it comes to taxes, it has a meaningful impact.

For their fiscal 2022, they are showing that the bulk of their distribution is identified as long-term capital gains. However, last year they ended up classifying most of the distribution as return of capital despite a relatively similar amount of realized gains. This is a good example of the underlying coverage of the distribution not lining up with the tax character.

{kind=link}

The realized gains of last year would have been higher, but the written options lost the fund $44.11 million in fiscal 2021. They can mitigate potential tax obligations by generating losses on one side of their portfolio. ROC is a way to defer taxes as it reduces an investor's cost basis. Interestingly, it would appear that they decided to harvest gains.

At the end of the day, management has a lot of flexibility in their decisions. So for tax-sensitive investors, CEFs often won't have enough consistency to be placed into a taxable portfolio. At the same time, if you have flexibility regarding taxes, these tax classifications are still ultimately tax-friendly.

ETY's Portfolio

ETY is more active than the other EV option-based funds. Generally, they have quite a limited turnover, but ETY reported last year a turnover of 55%. This could also be why the fund is showing more long-term capital gains in recent years if they are more actively harvesting gains.

This fund will overwrite their portfolio at roughly 50%, whereas something like Eaton Vance Tax-Managed Buy-Write Income Fund ( ETB ) also focuses on the S&P 500 but overwrites nearly 100% of their portfolio. That's one of the pieces that set these two funds apart.

In attempting to replicate a similar exposure as the S&P 500, ETY does so in only 66 holdings . With such a minimal number, relatively speaking, we can begin to see why some divergences in expectations can pop up. While the general trajectory should be similar, there will be discrepancies. That's even when, on the broader level, the sector exposure of the fund is quite similar.

ETY Sector Allocation (Eaton Vance)

However, when looking at the top holdings, we start to see heavier weightings in ETY, even if these positions overlap.

ETY Top Ten Holdings (Eaton Vance)

The top ten here make up 38.5% of the fund. For the S&P 500, their top ten make up 24.21%. The largest holdings of Apple ( AAPL ), Microsoft ( MSFT ), Alphabet ( GOOG ) and Amazon ( AMZN ) for ETY are also heavily represented in the index.

Instead of holding both classes of GOOG and ( GOOGL ) that the S&P 500 does, it appears that ETY has chosen GOOG. Otherwise, these four companies represent 17.09% of the index, and for ETY, it is 23.4%. That shows us how much weight these companies carry over all the other exposures here.

Despite the higher turnover reported by ETY, the fund showed quite a few similarities to last year. At the broadest level, the top ten weightings was a similarly hefty 39.9% of the fund. The mega-cap tech names made up 25.1% of the fund.

Getting into the smaller allocations here, the names are quite different, interestingly. UnitedHealth Group ( UNH ) makes another appearance. However, last year we also saw JPMorgan ( JPM ), Intuit ( INTU ), Danaher ( DHR ), Bank of America ( BAC ) and Eaton Corp ( ETN ).

Those were replaced with PepsiCo ( PEP ), Mastercard ( MA ), Eli Lilly ( LLY ), Chevron ( CVX ) and Procter & Gamble ( PG ). These are all essentially well-known names for most investors, so the overall theme of the fund hasn't changed. Even further, all of these names are still in ETY's portfolio; it simply changed between what the weightings were and what the weightings are now.

Conclusion

ETY is a more attractively priced fund. However, investors with some patience should probably wait for an even further discount to open up before getting too excited. Otherwise, a dollar-cost averaging approach could be appropriate to take advantage of averaging in over time.

For further details see:

ETY: Valuation Comes Down To A Better Level