ERRFY - Eurofins Scientific: A Buy On Any Further Pullback

Summary

- Eurofins Scientific printed cash during the COVID pandemic as its testing capacity was running at full utilization.

- There shouldn't be any massive post-COVID blues as growth in other domains should offset the decreasing COVID-related revenue.

- The company is now trading at about 10x EBITDA and 16x earnings.

- I would for sure be a buyer at slightly lower prices.

Introduction

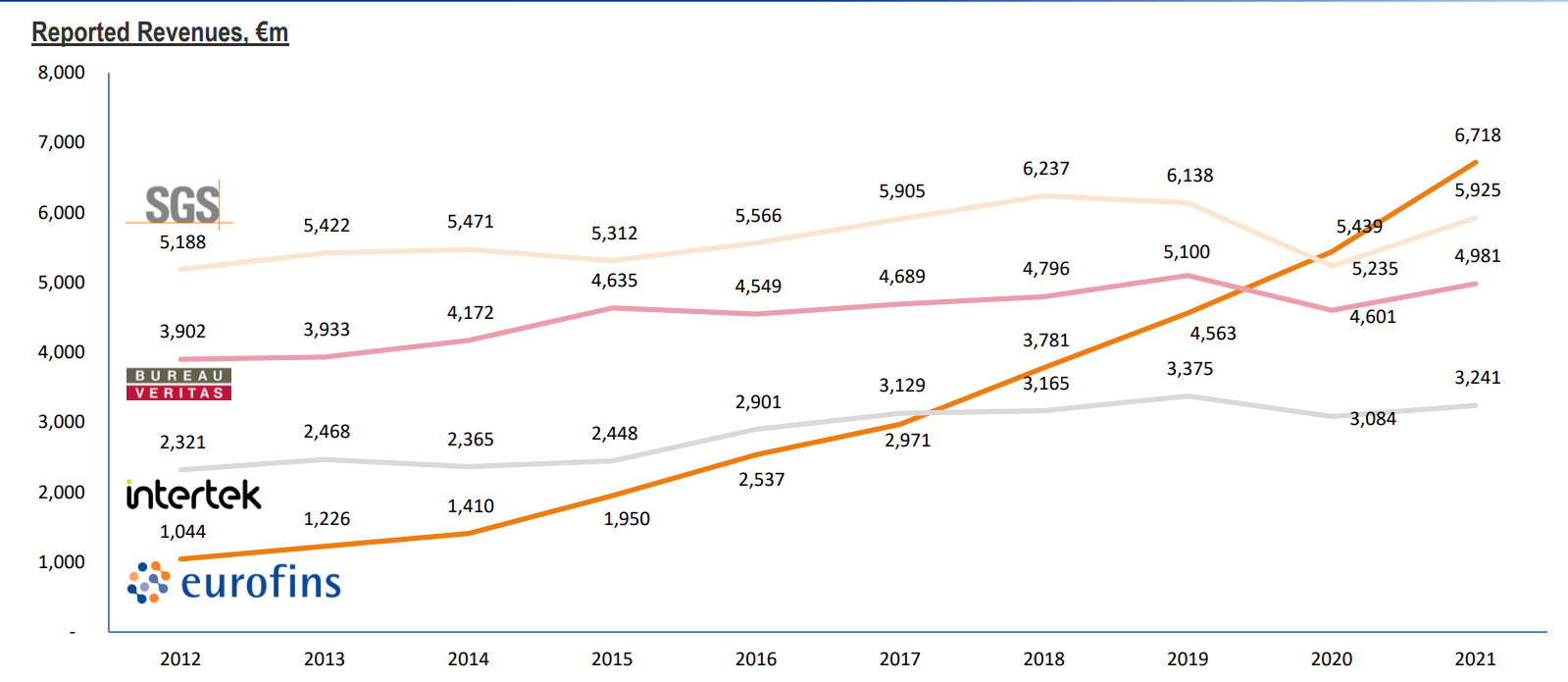

The last time I discussed Eurofins Scientific ( OTCPK:ERFSF ) ( OTCPK:ERRFY ), the stock was trading at almost 700 EUR per share, 67 EUR per share adjusted for the 10:1 share split which has occurred since). Back in 2020, I thought Eurofins stood to benefit from the COVID pandemic as it is one of the best regarded lab testing companies in the world and the surge in COVID tests would for sure result in an increased demand for its services. My hunch was correct as Eurofins' share price increased by in excess of 70% during 2021. Over the past decade, Eurofins saw its revenue increase much faster than any of its peers.

{kind=link}

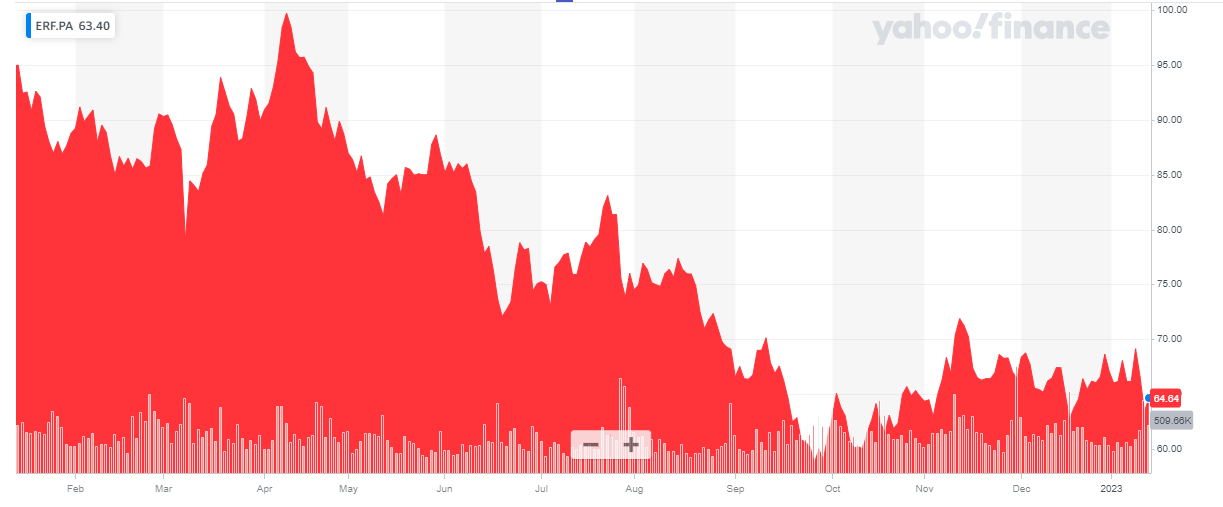

Eurofins has its primary listing on Euronext Paris where it's trading with ERF as its ticker symbol . The average daily volume in Paris is just over 430,000 shares per day. There are currently 192.7M shares outstanding, resulting in a market capitalization of approximately 12.5B EUR. Given the superior liquidity on its Paris listing, I would strongly recommend using Euronext Paris to trade in Eurofins' shares.

{kind=link}

The COVID windfall is over, but that doesn't mean Eurofins has no value

As explained in my previous article, Eurofins Scientific is one of the world's largest companies providing lab testing services to several key players of the food and health industry. Eurofins is active with in excess of 900 laboratories in 54 countries and recently improved its brand recognition as one of the largest independent labs testing for COVID-19 in Belgium, the Netherlands, Germany and France. Although this does provide a nice boost in the financial results, the core expertise of Eurofins isn't just medical testing as it conducts hundreds of tests per year across all sectors.

{kind=link}

And on top of those 'larger' markets, Eurofins is also penetrating five specific niche markets which don't account for a large portion of the revenue yet but could become more important in the future.

{kind=link}

Between 2019 and 2021, the company's revenue increased by approximately 50% while the adjusted EBITDA more than doubled. 2021 likely was the 'peak year' for a while for Eurofins as the 2022 EBITDA result will come in lower and as the need for COVID tests continues to decrease there will be more pressure on that front. That being said, Eurofins is very active in other sectors and the organic growth in other test work should offset the lower COVID test work volumes from 2023 on.

Eurofins Investor Relations

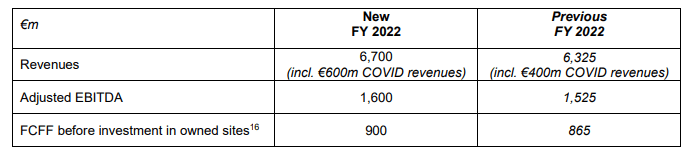

This doesn't mean 2022 will be bad. When the company released its H1 results, it provided an updated revenue and EBITDA guidance. The total revenue for this year is anticipated to be 6.7B EUR , of which just under 10% will be COVID related. The adjusted EBITDA should be 1.6B EUR, resulting in a free cash flow result of 900M EUR, excluding the (non-maintenance) additional investments in its facilities.

{kind=link}

The company only publishes detailed financial statements every semester which means that we have to work with the H1 2022 financial statements and the Q3 trading update .

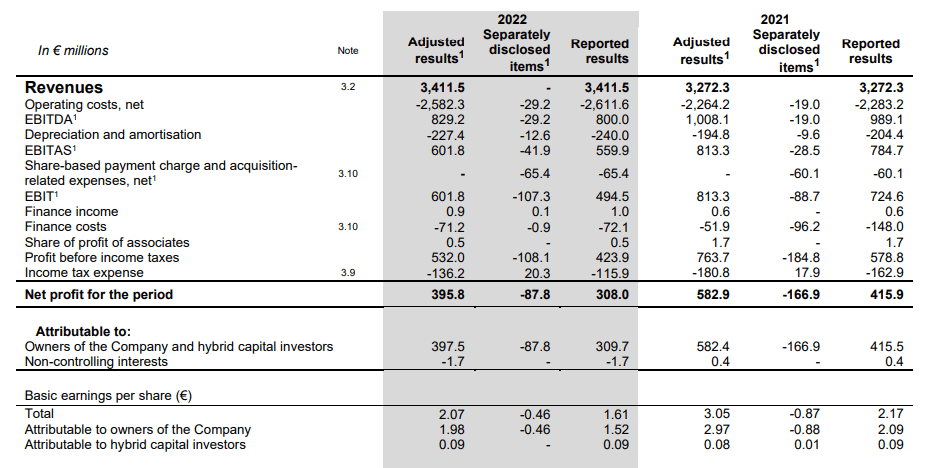

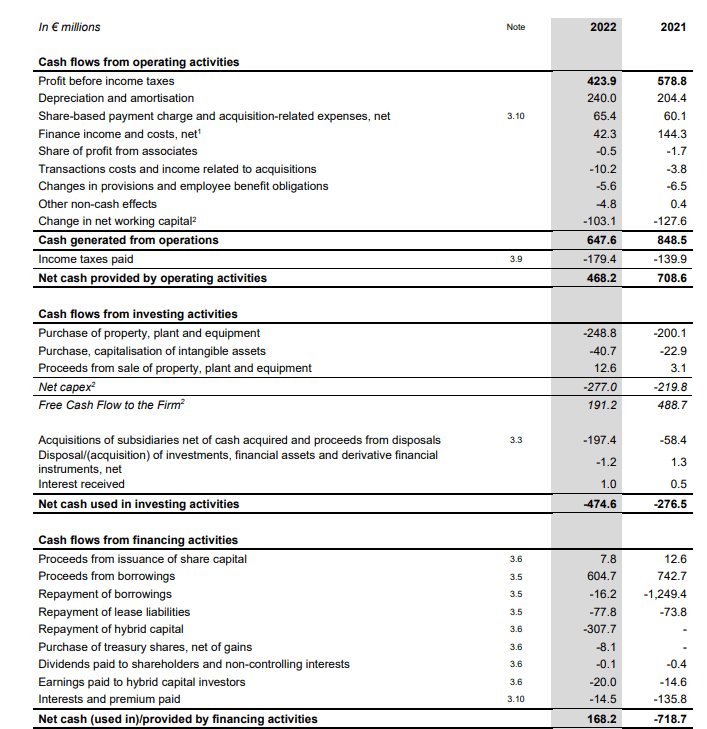

In the first half of 2022, the company reported a total revenue of 3.4B EUR, resulting in an EBITDA of 800M EUR and an EBIT of 495M EUR. The total amount of finance costs came in at 72M EUR, resulting in a pre-tax income of 424M EUR and a net income of 308M EUR.

{kind=link}

About 1.7M EUR of losses were attributable to non-controlling interests, which means the net income attributable to the shareholders of Eurofins was 310M EUR, for an EPS of 1.61 EUR per share. Eurofins also has hybrid securities outstanding which are so deeply subordinated they are accounted for as equity which means the coupon payments on these hybrid securities are not reported as an interest payment but rather come out of the net income. The net income per share after taking care of those coupons was 1.55 EUR per share.

As you can see on the income statement, this included about 88M EUR in exceptional items (related to integration and reorganization expenses as well as discontinued operations and other non-recurring items), and excluding those, the underlying net income per share would have been 1.98 EUR after making the coupon payments on the hybrid securities.

The cash flow statement uses the 424M EUR in pre-tax income as starting point. The reported operating cash flow was 468M EUR, but a few corrections are needed. First of all, the company made almost 180M EUR in cash tax payments although the income statement shows only 116M EUR was due for the first half of this year. This means we need to add back 64M EUR. Additionally, the operating cash flow includes a 103M EUR investment in the working capital position, but excludes the 15M EUR in interest payments, 20M EUR in payments to the hybrid securityholders and the 78M EUR in lease payments.

{kind=link}

After taking all these adjustments into consideration, the adjusted operating cash flow generated in the first half of the year was approximately 522M EUR. The total capex was 299M EUR (including intangible assets), resulting in an underlying adjusted free cash flow of 323M EUR.

That being said, in the first half of the year, only 191M EUR of the capex was not related to the purchase and development of owned sites. And although that 191M EUR will for sure contain some growth and improvement capex, it does provide a fair representation of Eurofins' investing needs.

{kind=link}

This also means that if we would use the 'normalized' 191M EUR capex in the first half of the year, the underlying sustaining free cash flow result was approximately 420M EUR. And as there are 192.7M shares outstanding , the underlying free cash flow per share was approximately 2.18 EUR per share.

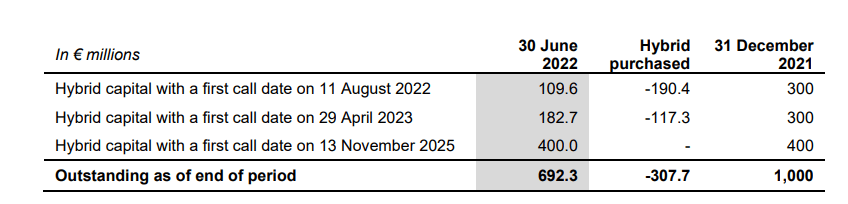

Considering the H2 EBITDA should also be roughly 800M EUR (given the full-year guidance of 1.6B EUR in EBITDA), we can expect a similar free cash flow performance in the second half of the year. While Eurofins called a substantial portion of its hybrid capital , it also issued a new 2029 bond with a 4% coupon so although the payments on hybrid securities will decrease, the interest expenses will increase. The silver lining: those interest expenses are a cost while the payment on the hybrid securities had to be paid out from the after-tax profits.

Eurofins Investor Relations Eurofins Investor Relations

{kind=link}

{kind=link}

Investment thesis

Eurofins Scientific isn't cheap, but as the leader in many domains, it likely will never get cheap. Assuming a stable EBITDA result of 1.6B EUR and 500M EUR in depreciation and amortization expenses as well as 40M EUR in interest expenses, the pre-tax income should come in at 1.06B EUR. Applying an average tax rate of 25% means the net income will likely be somewhere around 800M EUR or just over 4 EUR Per share. The EBITDA excluding lease payments should be roughly 1.45B EUR and with a net debt position (excluding lease liabilities) of 2.1B EUR, the stock is currently trading at an EV/EBITDA multiple of 10.

Am I willing to pay 16 times earnings at this point? Not immediately. But I noticed the option premiums are nice enough for me to write an out of the money put option while waiting for the share price to come down a little bit. A P52 expiring in June has an option premium of 1.70 EUR which means that - if exercised - I would be buying Eurofins at just over 12 times earnings. Looking further ahead, a P50 for September has an option premium of approximately 2.30. At 50 EUR per share, the EV/EBITDA ratio is 8 (assuming the net debt doesn't decrease any further).

So rather than buying the stock right now, I will likely write an out of the money put option while waiting for the share price to come down a little bit.

For further details see:

Eurofins Scientific: A Buy On Any Further Pullback