ERRFY - Eurofins Scientific: Short Term Pain But Keep Your Eyes On The Long-Term Potential

Summary

- Eurofins is a large life sciences company, but its COVID tailwinds are coming to an end.

- Apparently the market is surprised by this. I am not.

- The current share price weakness offers an excellent opportunity for investors with a 5-year investment horizon.

- Eurofins' 2027 targets imply a 70% EBITDA increase from the anticipated 2023 result.

Introduction

In a January article, I explained why I liked Eurofins Scientifics’ ( OTCPK:ERFSF ) ( OTCPK:ERRFY ) long-term guidance and its plan to deal with the post-COVID era. Eurofins printed cash during COVID thanks to the rigorous testing regimes all over the world, but that (easy) revenue is now coming to an end. It already fell back in 2022 and will see a further decline in 2023. Apparently the market didn’t see that coming as it sent Eurofins’ share price sharply lower upon announcing the FY 2022 financial results. I’m surprised because this shouldn’t really come as a surprise. In this article I will explain what the lower guidance for 2023 means and why I have a much longer term outlook than the next twelve months.

{kind=link}

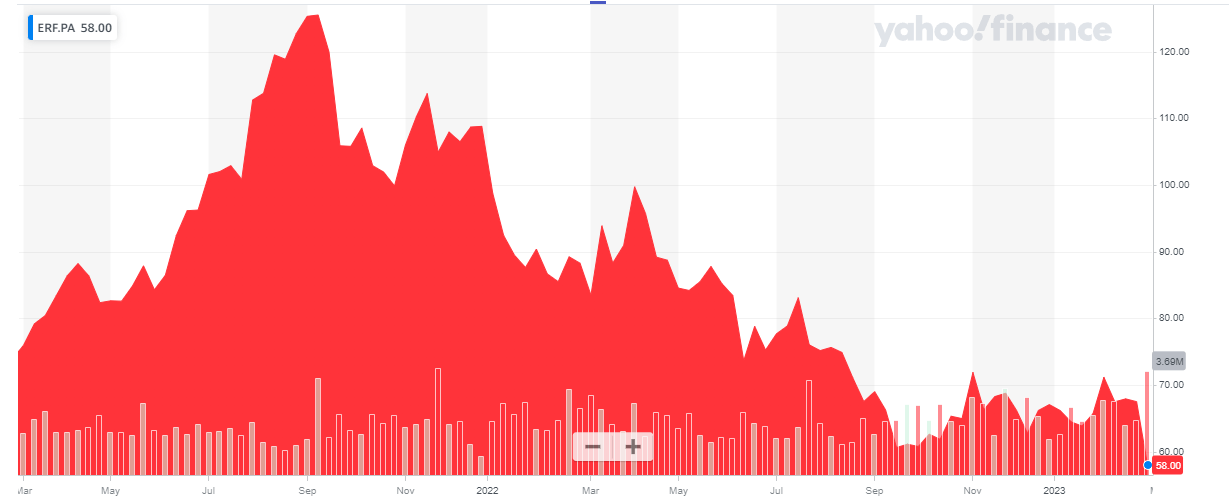

Eurofins has its primary listing on Euronext Paris where it's trading with ERF as its ticker symbol . The average daily volume in Paris is just over 400,000 shares per day. There are currently 192.8M shares outstanding , resulting in a market capitalization of approximately 11.2B EUR using the closing price of 58.00 EUR on Wednesday. Given the superior liquidity on its Paris listing, I would recommend using Euronext Paris to trade in Eurofins' shares.

While the company missed its FY 2022 guidance, I’m not too worried

For a better overview of the company’s business model and how COVID-19 has impacted its results, I’d like to refer you to my previous article . In this article, I will focus on the 2022 results, the 2023 guidance and what the longer-term 2027 guidance means for the company and its shareholders.

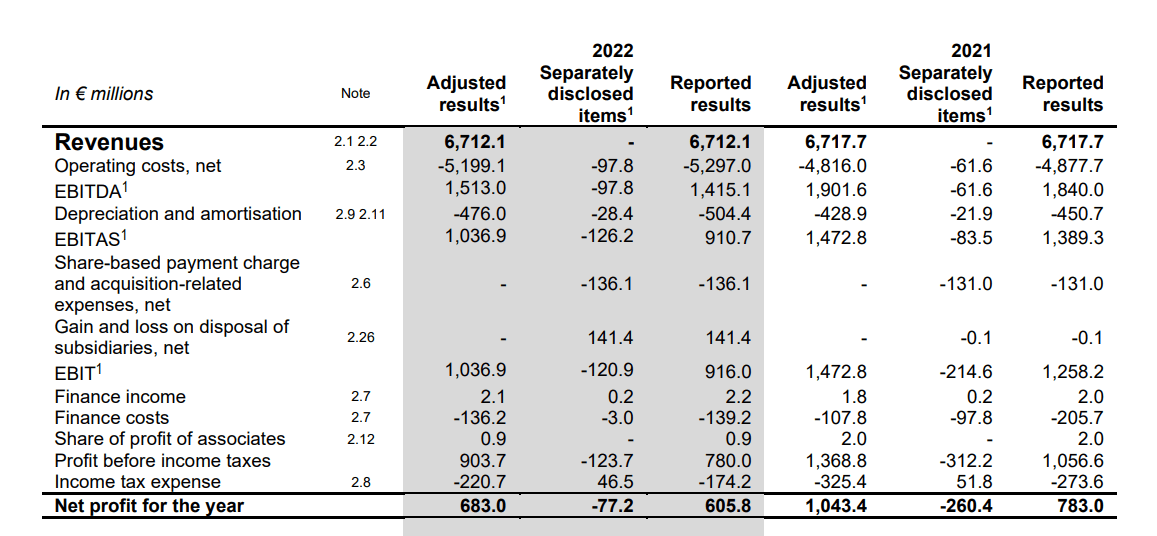

Eurofins didn’t meet its (updated) guidance in 2022. It should not come as a surprise to see a double digit net income decrease as the COVID-related revenue is rapidly decreasing, but unfortunately Eurofins’ adjusted EBITDA of 1.513B EUR came in below expectations.

{kind=link}

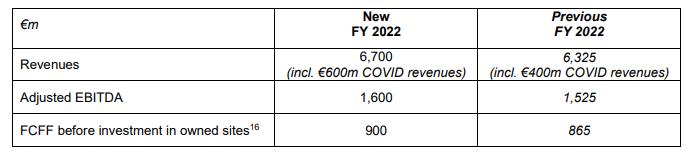

And while the company missed its EBITDA target, let’s not forget it had actually hiked its preliminary EBITDA target. As you can see below, the original EBITDA target came in at 1.525B EUR and if Eurofins would not have hiked it after publishing its H1 results, it basically would have (almost) met its initial guidance.

{kind=link}

While walking back on an earlier EBITDA promise is never good news, we should also not exaggerate the impact on the longer-term outlook of the company (which I will discuss in the second part of this article).

But let’s first circle back to the cash flow results of Eurofins. In my January article I did use the free cash flow generation as the main reason to increase my level of interest in Eurofins.

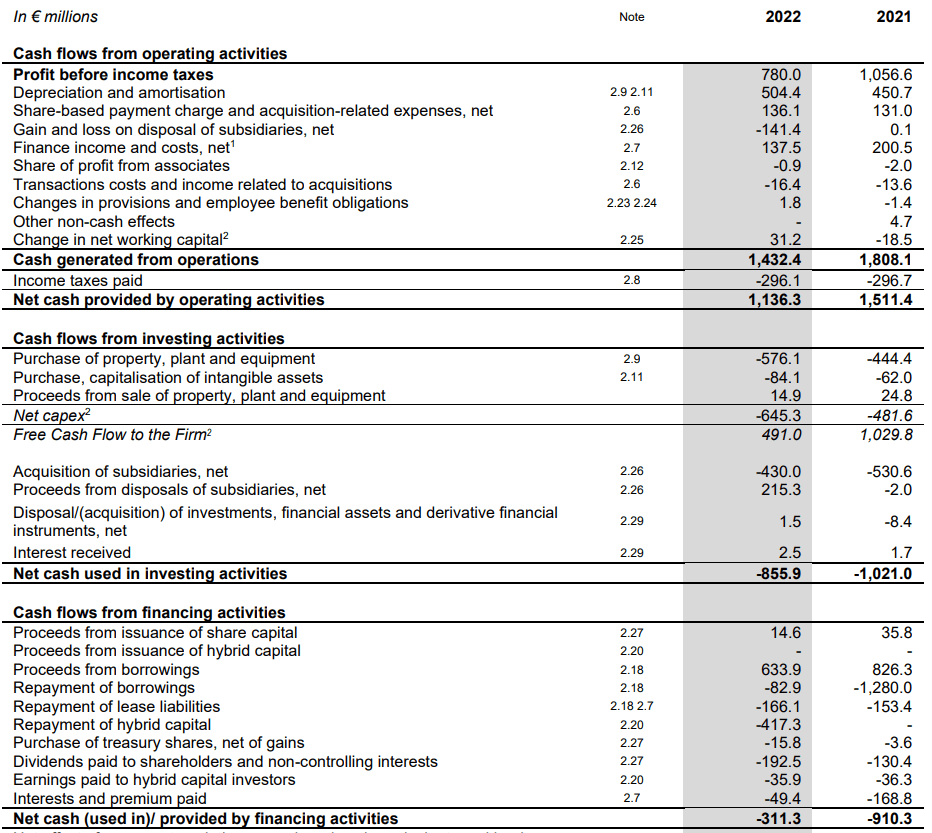

Eurofins reported a total operating cash flow of 1.14B EUR , which includes about 296M EUR in cash taxes while only 174M EUR was owed after taking the separately disclosed items into account (and even if you would ignore those adjustments, the tax bill on the income statement was still just approximately 220M EUR). The 1.14B EUR also includes a 31M EUR contribution from working capital changes, but does not include the 166M EUR in lease payments and the 85M EUR interest and hybrid coupons.

{kind=link}

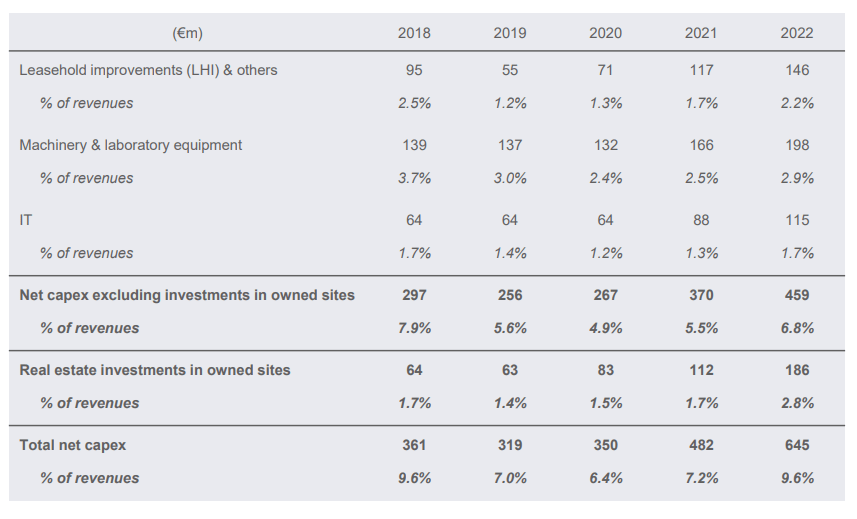

On an adjusted basis, the operating cash flow was approximately 975M EUR and 978M EUR if you include the interest received. And although we see the total capex was 660M EUR in the image above (excluding the proceeds from the sale of assets), only a small portion of that consists of sustaining capex. About 459M EUR of the capex was spent on assets excluding investments in own sites and as you can see below, this still included almost 150M EUR in leasehold improvements.

{kind=link}

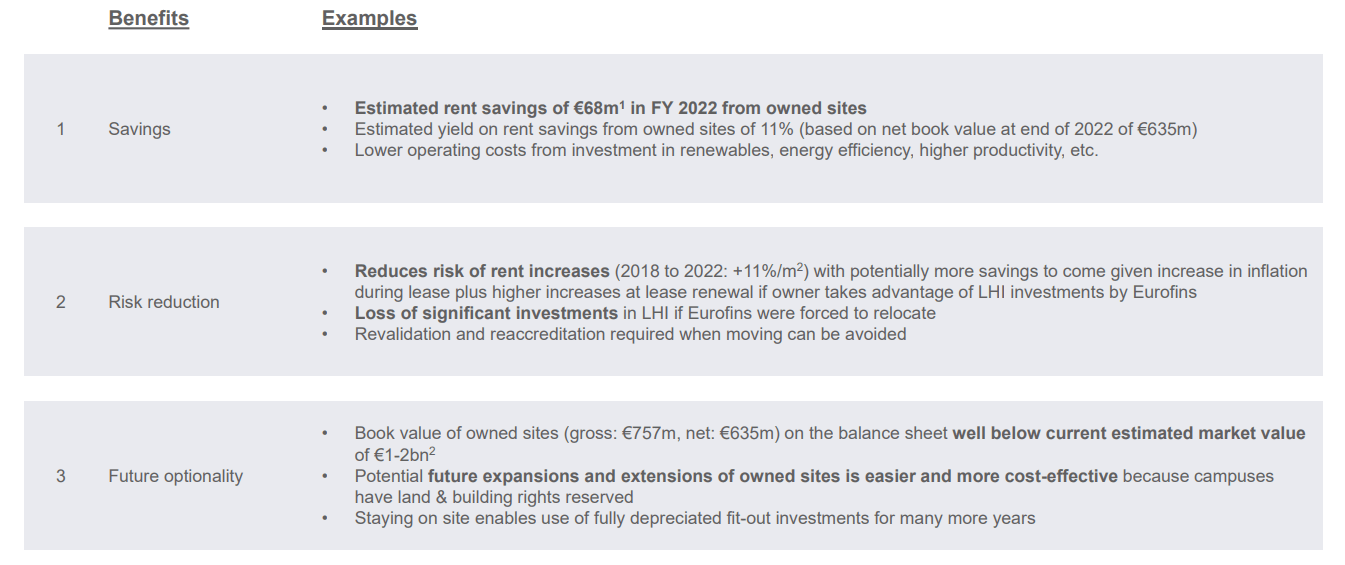

It actually makes sense for Eurofins to start owning its buildings. While the opposite was true in the past few decades, Eurofins calculated annual rent savings of 68M EUR which were generated through the purchase of 635M EUR in assets. This means Eurofins is adding assets at a 11% rental yield so I fully support the decision to own more of the real estate assets – if they can be acquired at a decent price.

{kind=link}

So despite the EBITDA decrease, Eurofins was still throwing off very healthy amounts of free cash flow. And the long-term plan calls for even more free cash flow.

Expect another (small) EBITDA decrease before pursuing long-term growth

Perhaps it wasn’t just the EBITDA miss which caused the markets to send the share price down by a double digit percentage. While 2022 was definitely still okay (although slightly below expectations), Eurofins guided for another EBITDA decrease in 2023 as the company now estimates it will generate an adjusted EBITDA of 1.35-1.4B EUR.

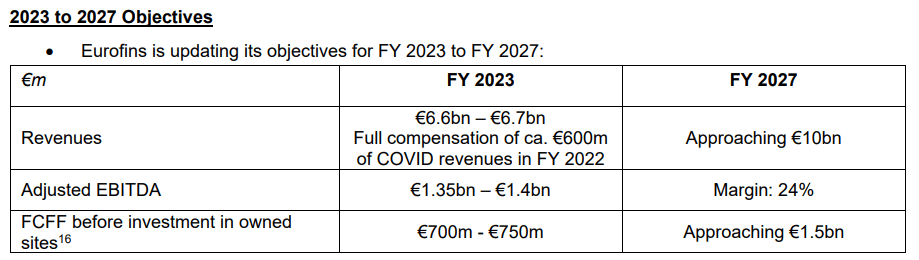

While that sounds like a disappointment, keep in mind that the past three years the revenue and EBITDA was boosted by a black swan event: the COVID pandemic. As the world is now (fortunately) normalizing, the ‘downside’ is that companies like Eurofins will generate a lower COVID-related revenue. I do believe this year will be the turning point as Eurofins’ guidance for 2027 implies a pretty aggressive growth pattern over the next five years.

{kind=link}

Eurofins expects to generate close to 10B EUR in revenue in FY 2027 and anticipates a 24% EBITDA margin on that revenue. That’s a pretty bold outlook given the anticipation of a 50% revenue increase and a very substantial margin increase from less than 21% in 2023 to 24% in 2027. This also implies the FY 2027 EBITDA result will be approximately 2.4B EUR, which would be 71% higher than the upper end of the 2023 guidance. The 2.4B EUR in EBITDA should result in approximately 1.5B EUR in annual free cash flow (excluding growth investments).

That’s the guidance. I’m not sure what Eurofins has in mind when it comes to interest expenses, but I do expect the cost of debt to increase as Eurofins has to refinance existing debt. Right now, debt with a 6-year term is trading at just over 4.6% while the existing 2031 bonds offer a yield to maturity of approximately 5%. I think that’s relatively high (compared to other issuers)

{kind=link}

The total gross debt (including the 2.1B EUR in Eurobonds shown above) is 3.3B EUR. A 250 basis point interest rate increase would result in an increase of the interest expenses by 80-85M EUR and about 60M EUR on an after-tax basis. So even if we would assume Eurofins misses its guidance and only generates 9B EUR in revenue at a 22% EBITDA margin and subsequently misjudges its interest bill by 80M EUR, the free cash flow result would still likely come in at 1.2-1.3B EUR. Which would be north of 6 EUR per share.

Investment thesis

In my article I mentioned Eurofins is a buy on any pullback and I think it is an even stronger buy now. While the free cash flow result will likely still be under pressure (expect 3.5-3.75 EUR per share this year, based on the official guidance), the stock is now getting pretty attractive as the free cash flow yield has increased to about 6%.

The 2027 guidance calls for a FCFPS of 7.7 EUR per share which would represent a free cash flow yield of 13% based on the current share price. And even if Eurofins would miss its expectations, the scenario mentioned above where the company would generate 1.25B EUR in free cash flow would still result in an FCF yield north of 10%.

This makes Eurofins a buy in my books. Don’t expect anything in the short term, but for long-term investors with a 5-10 year investment horizon, I think Eurofins could be a good idea. I currently have no position but I will likely go long in the next few days or weeks.

For further details see:

Eurofins Scientific: Short Term Pain, But Keep Your Eyes On The Long-Term Potential