ERRFY - Eurofins Scientific Still Plans To More Than Double Its FCF By 2027

2023-08-05 10:40:00 ET

Summary

- Eurofins is dealing with a revenue decrease due to the lack of COVID testing and the sale of reagents.

- Excluding the COVID-related revenue, the H1 2023 revenue would have increased by a high single digit percentage.

- The company slightly reduced its 2023 FCF guidance to around 700M EUR but reconfirmed the 2027 guidance.

Introduction

Eurofins Scientific ( ERFSF ) ( ERRFY ) printed cash during COVID thanks to its excellent position in the testing sector, but that (easy) revenue is now drying up . It already fell back in 2022 as restrictions were lifted and will see a further decline in 2023. That’s also why we need to keep an eye on Eurofins’ underlying results as while the reported results appear to be weak (due to the unfair comparable basis when more COVID measures were in effect), the underlying performance excluding COVID-related revenue was actually very strong.

{kind=link}

Eurofins has its primary listing on Euronext Paris where it's trading with ERF as its ticker symbol . The average daily volume in Paris is approximately 390,000 shares per day. There are currently 193M shares outstanding , resulting in a market capitalization of approximately 11.6B EUR using the closing price of 58.00 EUR on Wednesday. Given the superior liquidity on its Paris listing, I would recommend using Euronext Paris to trade in Eurofins' shares. There are also options available in Paris.

H1 2023: lower in absolute numbers but a strong result adjusted for COVID

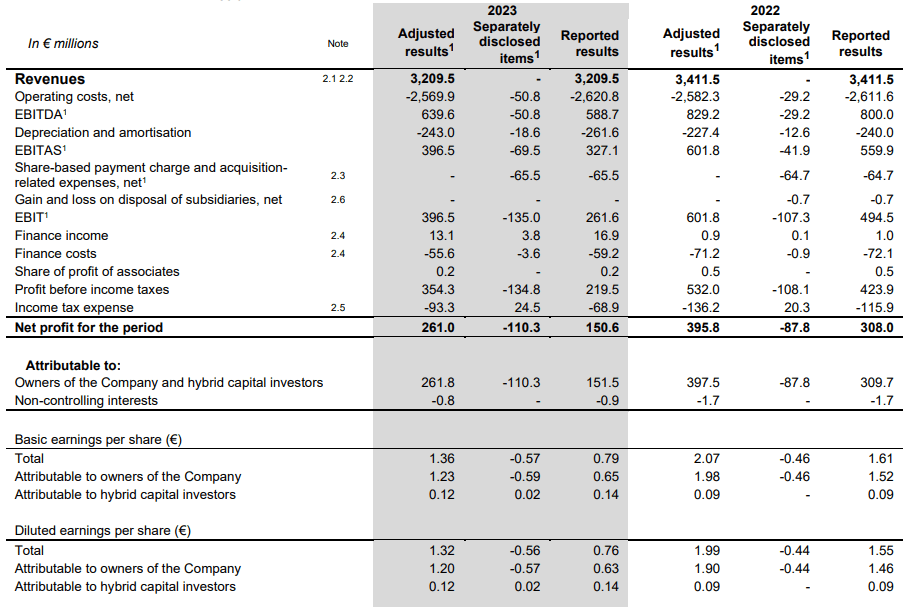

While I will discuss the company’s financial results on a reported basis, I wanted to prelude the analysis by explaining why the lower revenue compared to the first semester of last year isn’t necessarily an issue. The total reported revenue decreased by almost 6% to ‘just’ 3.2B EUR but this is entirely related to the lower demand for COVID-19 testing and reagents.

{kind=link}

While those two elements contributed about 470M EUR to the total revenue in the first semester of last year, the revenue from these two things dropped to just 20M EUR in the first half of this year. This means that the revenue from the core business (which excludes the COVID-19 related elements) actually increased by approximately 7% thanks to Eurofins’ North American division which performed very well.

{kind=link}

As mentioned, the total reported revenue came in at 3.21B EUR and as the operating costs increased as well, the EBITDA came in at just 588M EUR, a decrease from the 800M EUR in H1 2022. Not only was the COVID era a virtual gold mine for Eurofins’ revenue, the company’s margins on the testing and reagents was pretty strong as well. On an adjusted basis, the EBITDA came in at 630M EUR which is approximately 23% lower than in the first half of this year.

The reported net income was just 150.6M EUR and about 151.5M EUR was attributable to the shareholders of Eurofins which works out to approximately 0.65 EUR per share (after taking the payments to the owners of hybrid securities into account). While that was obviously a disappointing headline result, keep in mind the adjusted EPS was approximately 1.23 EUR after taking the income attributable to the hybrid security investors into account.

While I’m not necessarily a big fan of using ‘adjusted’ results, I understand Eurofins feels the need to provide all relevant information to its shareholders. About half of the pre-tax impact on the results is caused by acquisition-related expenses and other non-recurring items. For FY 2023, Eurofins estimated these elements to have a negative impact of 100M EUR on the EBITDA . In the longer run, these elements will be reduced to 0.5% of the revenue (which would be a few tens of millions per year).

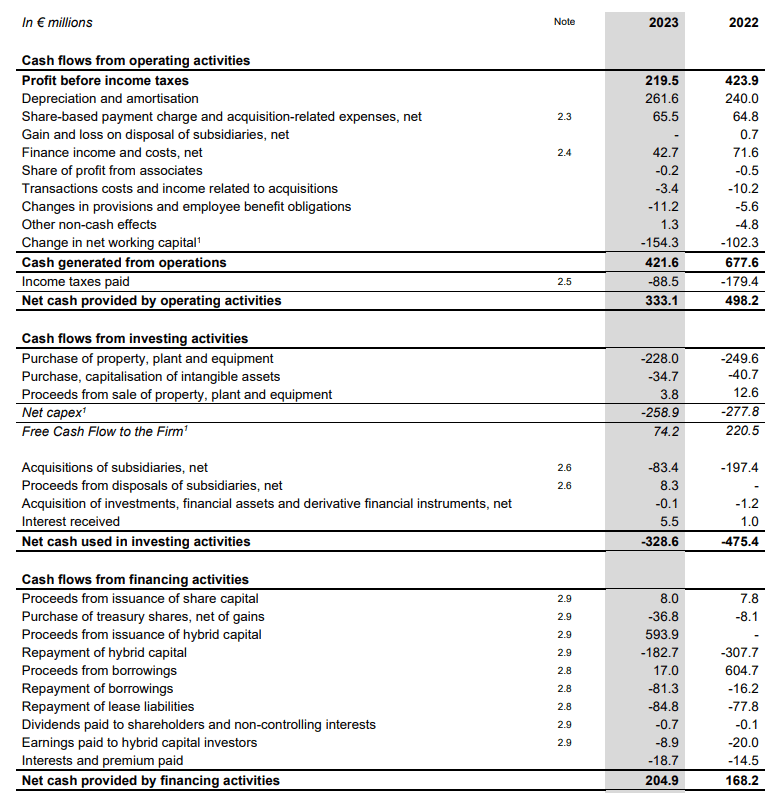

The total operating cash flow in the first half of the year was roughly 333M EUR but this includes about 20M EUR in additional tax payments that were not owed based on the H1 income statement. Additionally, this includes a 154M EUR net investment in the working capital position but excludes the 19M EUR in interest expenses, the 9M EUR paid to hybrid investors and the 85M EUR in lease payments.

{kind=link}

This means that on an adjusted basis, the operating cash flow in the first half of the year was 394M EUR. The total capex was 263M EUR resulting in an official free cash flow result of 131M EUR.

Keep in mind this was impacted by about 110M EUR in non-recurring items while the total capex level is substantially higher than the sustaining capex. The H1 depreciation and amortization expenses were just 262M EUR while Eurofins spent about 350M EUR on capex and lease payments. Eurofins is guiding for a full-year capex of 600M EUR (excluding lease payments) of which about 400M EUR would be ‘normal’ capex and about 200M EUR will be invested in owned sites.

So while a free cash flow result of 68 cents per share appears to be low, if I would use the normalized capex and exclude the non-recurring elements, the underlying free cash flow per share would actually have been just over 1.5 EUR per share. While it wouldn’t be fair to exclude all non-recurring items as Eurofins is expecting an annualized impact of about 15M EUR per semester, it is clear the underlying results were much stronger than what the income and cash flow statement show you. And that barely contains any positive impact from COVID testing anymore.

The 2023 guidance was lowered, the 2027 guidance remains intact

While the first half of 2023 was a bit lighter than I had expected on a reported basis and slightly below my expectations on an adjusted basis, Eurofins also didn’t want to sugarcoat anything and has slightly reduced the adjusted EBITDA guidance and the free cash flow guidance. The free cash flow result before the 200M EUR capex to be invested in ‘owned sites’ will come in at around 670-720M EUR and the midpoint would result in a free cash flow result of 3.6 EUR per share (subject to change sin the working capital position).

{kind=link}

Fortunately the long-term objectives for 2027 remain unchanged. As explained in my previous article : Eurofins expects to generate close to 10B EUR in revenue in FY 2027 and anticipates a 24% EBITDA margin on that revenue. That’s a pretty bold outlook given the anticipation of a 50% revenue increase and a very substantial margin increase from less than 21% in 2023 to 24% in 2027. This also implies the FY 2027 EBITDA result will be approximately 2.4B EUR, which would be 71% higher than the upper end of the 2023 guidance. The 2.4B EUR in EBITDA should result in approximately 1.5B EUR in annual free cash flow (excluding growth investments).

Investment thesis

As far as I’m concerned, Eurofins is still on track to meet its longer term guidance. While 2023 will be slightly lighter than expected, let’s not forget the current free cash flow yield of 6% is still pretty reasonable considering the net impact of non-recurring elements should be peaking this year. It will be impressive if Eurofins reaches its 1.5B EUR annual free cash flow result by 2027, but even if it blatantly misses that objective and only realizes 1B EUR in free cash flow (which would be a horrible miss by all standards), the net free cash flow per share would still exceed 5.20 EUR per share for a free cash flow yield of close to 9%. And that still makes Eurofins a buy at the current levels.

I currently have no position in Eurofins as I have been writing put options which all expired out of the money. I was waiting for the H1 results to be published before committing to writing additional put options and I may do so in the very near future. A P56 for December for instance has a current option premium of approximately 2.10 EUR (the spread can be pretty wide) and would result in an average purchase price of less than 54 EUR per share for a 7% free cash flow yield.

For further details see:

Eurofins Scientific Still Plans To More Than Double Its FCF By 2027