FRO - Euronav And Frontline: Lessons From The Shipping Industry

2023-10-30 20:33:29 ET

Summary

- The Tanker industry has seen a resurgence in recent months due to geopolitical events and rising oil prices.

- Euronav NV has a takeover bid from its largest shareholder, CMB.

- Frontline plc is acquiring 24 VLCCs from Euronav NV and is poised to benefit from the transaction.

- Frontline is likely to grow earnings and continue to pay out a quarterly dividend that currently yields 11.5% at the current market price.

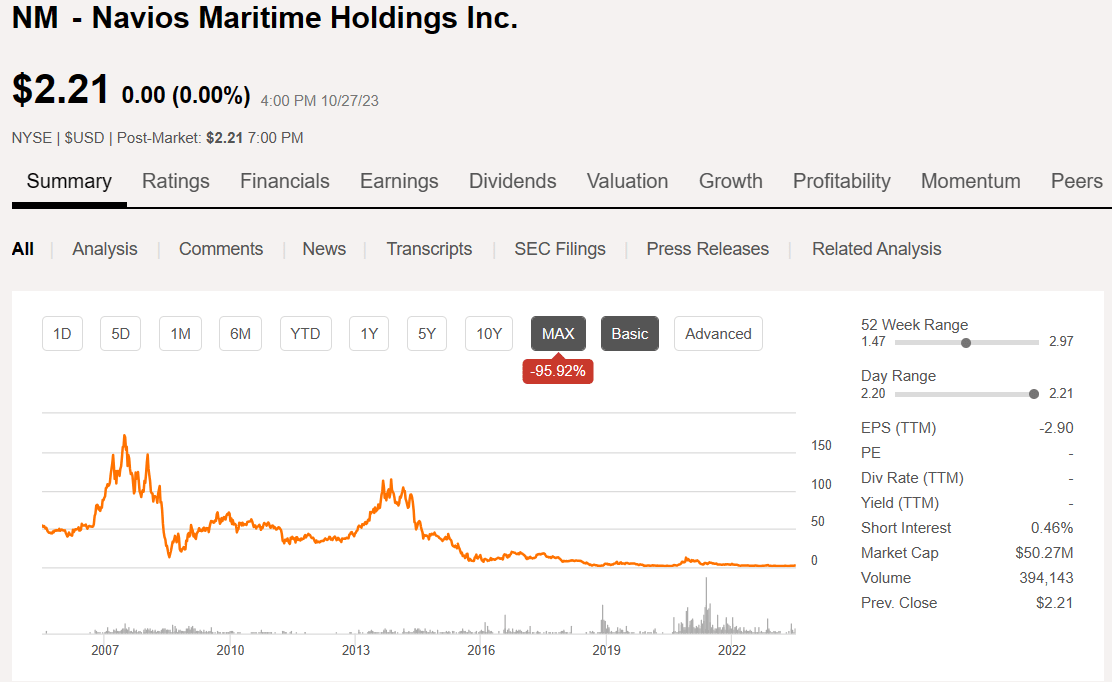

If you have been following the shipping industry as an asset class for investing for the past ten years or more, you will likely remember that it has not been a good place to invest in recent years. The Great Recession of 2008-2009 hit the industry hard. Initially, in late 2007 and early 2008, the demand for global shipping soared sending the prices of some companies sky-high. Companies like Navios Maritime Holdings Inc. (NM), a Dry Bulk shipping company, saw its stock go up to a high of over $170 in October 2007, then plummeted in 2009, rose to a lower new high of about $114 in 2014 and then dropped again and has never recovered since. In the past 18 years, NM has lost more than 95% of its value.

{kind=link}

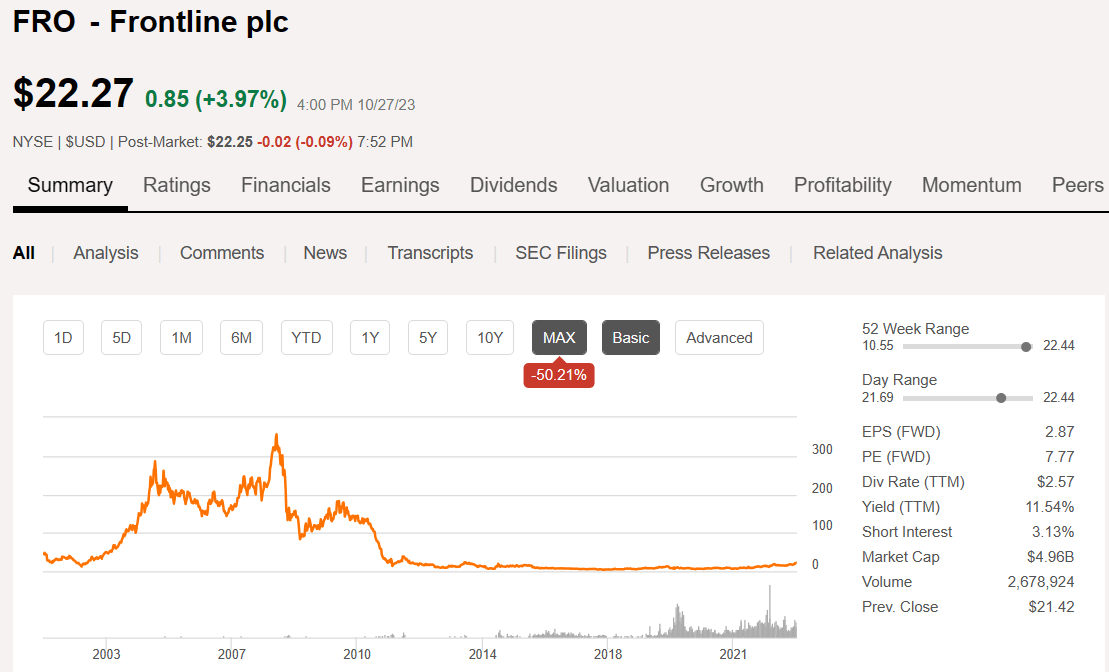

Another sector within the shipping industry, the tanker sector, suffered a similar history of poor returns until this year. Current geopolitical events such as the Russia/Ukraine war, rising inflation and oil prices, and other world events have led to a resurgence in tanker stocks. One of those stocks that is now recovering in recent months is Frontline plc (FRO), which had a similar-looking chart to NM until 2023.

{kind=link}

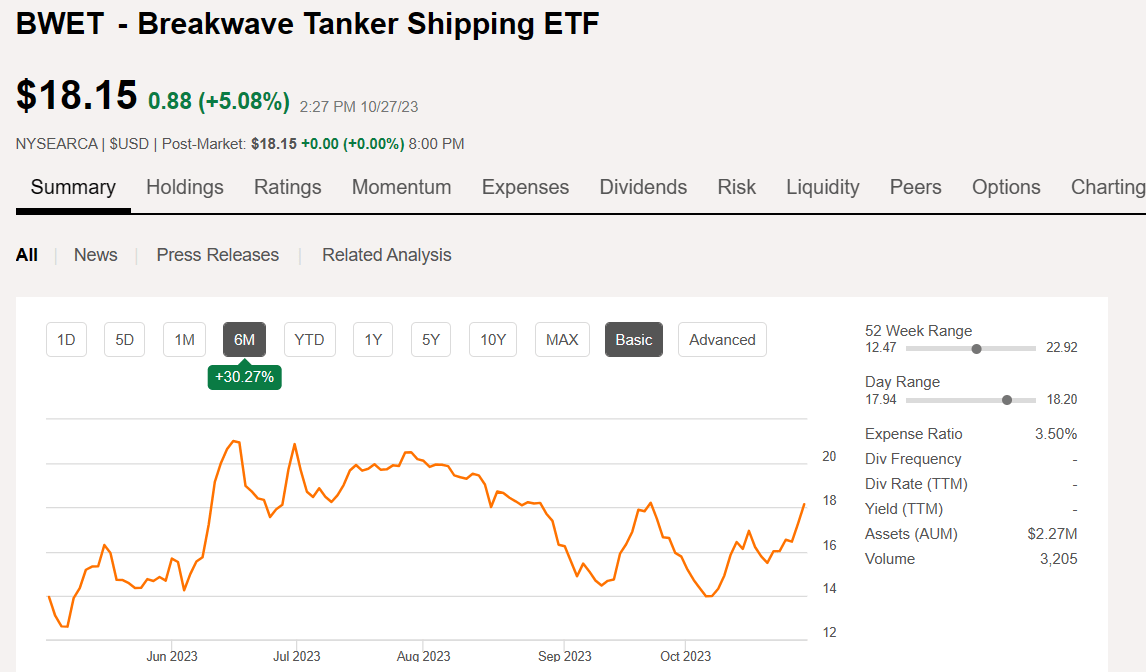

In fact, the tanker industry is doing so well this year that a new tanker ETF was formed in May 2023, the first-ever ETF focused on oil tanker shipping costs. Breakwave Advisors partnered with the ETF Managers Group to introduce the Breakwave Tanker Shipping ETF (BWET). BWET offers exposure to the crude oil shipping market using a portfolio of near-dated contracts on shipping indices.

Regarding the fund's launch, John Kartsonas, founder and managing partner of Breakwave Advisors stated: "The tanker market has recently shown its growing importance when it comes to energy security as well as the significant returns the sector can generate over the full cycle.”

“Today, the tanker industry is faced with high demand for oil transportation, a limited vessel orderbook, disruptions in the traditional shipping routes, and longer shipping distances as a result of the major geopolitical changes affecting the oil markets,” Kartsonas added.

The fund is up over 30% in the 6 months since it launched.

{kind=link}

In an article from June of this year, the growth in tanker demand is especially noted as one that is holding up better than other shipping sectors.

The impact of longer routes is most prominent in tanker shipping, with Russian oil flowing to China and India at a discount instead of making a short haul to Europe. Western countries (G7) on the other hand have shifted away from importing Russian crude and oil products, and have started to import more crude oil from Saudi Arabia and the US and refined oil products like a diesel from India. This is pushing the expected growth in global oil product shipping up to double-digit levels in 2023, while tonnage demand will increase by just 4%.

And now with the recent outbreak of war with Israel and the Gaza Strip, this growth in tanker demand and additional uncertainty in global oil markets is increasing yet again.

Euronav

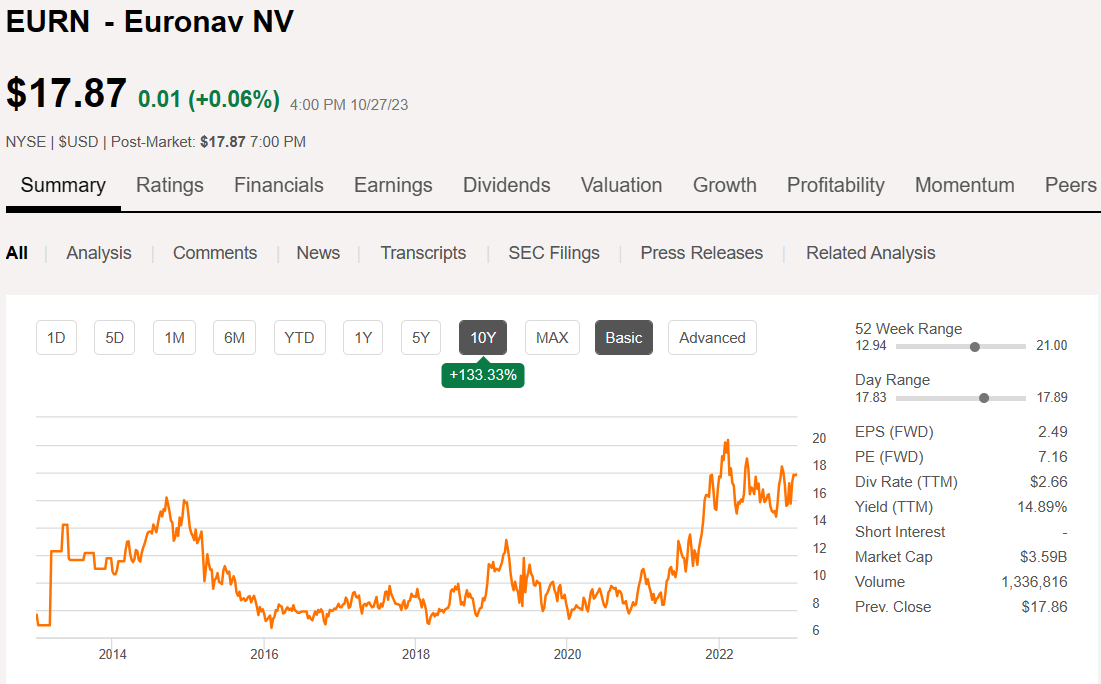

While some tanker companies have done better than others, Euronav NV (EURN), has returned more than 130% in the past 10 years, and most of that increase has been in the past 18 months or so.

{kind=link}

While EURN has been looking like a good tanker stock to invest in this year, recent news may cause one to hesitate to invest due to a takeover attempt that is now underway. The Euronav tanker takeover story actually began back in April 2022 when Frontline announced that they were merging with Euronav. At the time, the combined company would have had a market cap of about $4B with EURN shareholders holding 59% of the combined company shares and Frontline shareholders owning 41%. But the Savery family, whose Belgian shipping company CMB is the largest shareholder in Euronav, opposed the deal and the battle over control began.

Then on October 5, 2023, new statements were issued by the Savery Family and John Frederiksen , who owns a controlling interest in Frontline, that appeared to resolve the conflict.

The potential transaction has the following interdependent elements:

- CMB would acquire the 26.12% stake in Euronav held by Frontline and Fredriksen-affiliated Famatown for $18.43 per share to be followed by a public mandatory offer at the same price.

- Frontline would acquire 24 VLCC tankers from the Euronav fleet for $2.35 billion, subject to completion of the above-mentioned share purchase and approval by shareholders voting at a Special General Meeting. This option requires the application of the related party procedure under Belgian law.

- Euronav’s pending arbitration action against Frontline and affiliates would be terminated, conditional on the share sale.

Then on October 9, CMB issued this statement announcing their intention to complete a mandatory takeover bid for Euronav.

The price of the Mandatory Bid will be USD 18.43 per share, reduced on a dollar-for-dollar basis by the gross amount per share of any future distributions by Euronav to its shareholders with an ex-dividend date prior to the settlement date of the Mandatory Bid. The bid price will be paid in cash.

The deal is not done yet but there is a pretty strong indication that it will be completed. Both parties indicate that discussions are well advanced and there are regulatory approvals and clearances that the agreement is subject to, but otherwise, they agree and therefore the deal is likely to go through.

From a press release issued by Euronav, this statement sums up the agreement:

Lieve Logghe, Euronav CFO and interim CEO, stated: “After many months of uncertainty, the transaction announced today leverages the value that Euronav and its people have created through many years of hard work. It represents a balanced outcome for shareholders, who now have the choice between realising that value in cash or following Euronav in a new strategic direction under a new controlling shareholder.”

The most recent quarterly dividend from EURN was increased from $.70 per share to $.80 and was paid to EURN shareholders on September 19. If the agreement takes more than two additional months to complete, there should be another dividend (also $.80?) to be paid to EURN shareholders for Q4. That means that EURN shareholders will receive $18.43 minus whatever the next dividend payment equals. If that dividend payment is $.80 then the takeover price would be reduced to $17.63. The last closing price for EURN was $17.87 on 10/27/23 so there is no room for any arbitrage unless the terms of the agreement change or the amount of the dividend changes before the deal is completed.

If the takeover bid does not get approved or completed for whatever reason, then EURN will likely continue to perform well going forward but there will be more uncertainty around future revenue forecasts and dividend amounts, especially after selling 24 ships in their fleet to FRO. If I were an existing shareholder of EURN I would likely sell my shares in whatever tender offer is made pursuant to the agreement. I would not be a new buyer of EURN shares now that the price has risen to the point where there is very little room for arbitrage .

Frontline

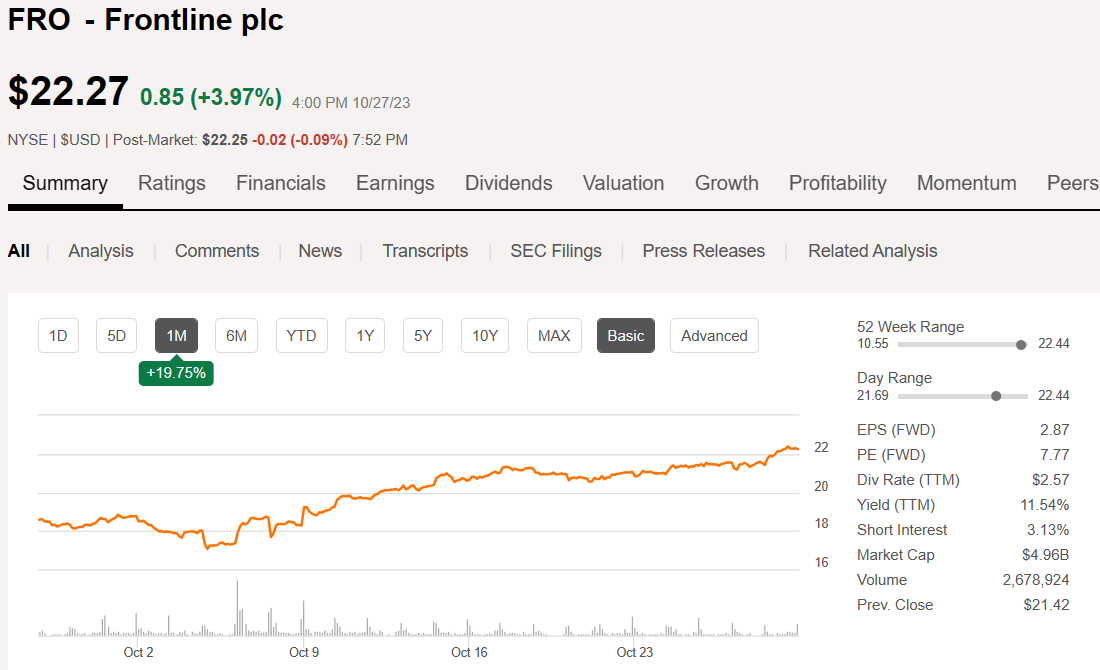

Meanwhile, I feel that FRO shareholders are getting a better deal now with the purchase of the 24 VLCC tankers from the Euronav fleet. The share price for FRO has risen nearly 20% since the deal was announced.

{kind=link}

FRO and other tanker stocks including Nordic American Tankers ( NAT ) and Teekay Tankers ( TNK ) should benefit from the tightly wound tanker market as explained in this recent report from Jeffries analyst, Omar Nokta:

Suezmax and Aframax crude tanker spot rates have surged from an average $27K/day during Q3 to ~$70K currently, highlighting a tight supply/demand balance and elevated risk premium with wars ongoing in Israel and Ukraine.

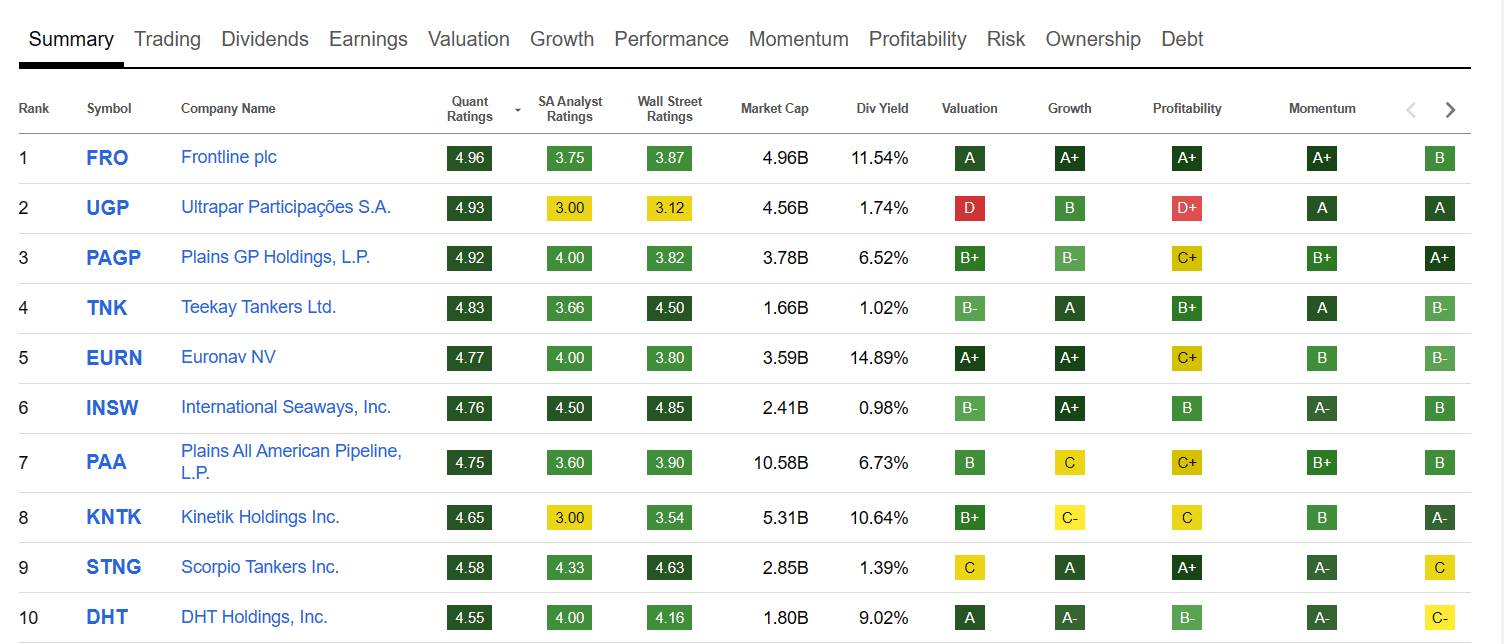

While EURN is ranked #5 in the SA Quant ratings for Tanker stocks, FRO is ranked #1 currently, while TNK is ranked #4.

{kind=link}

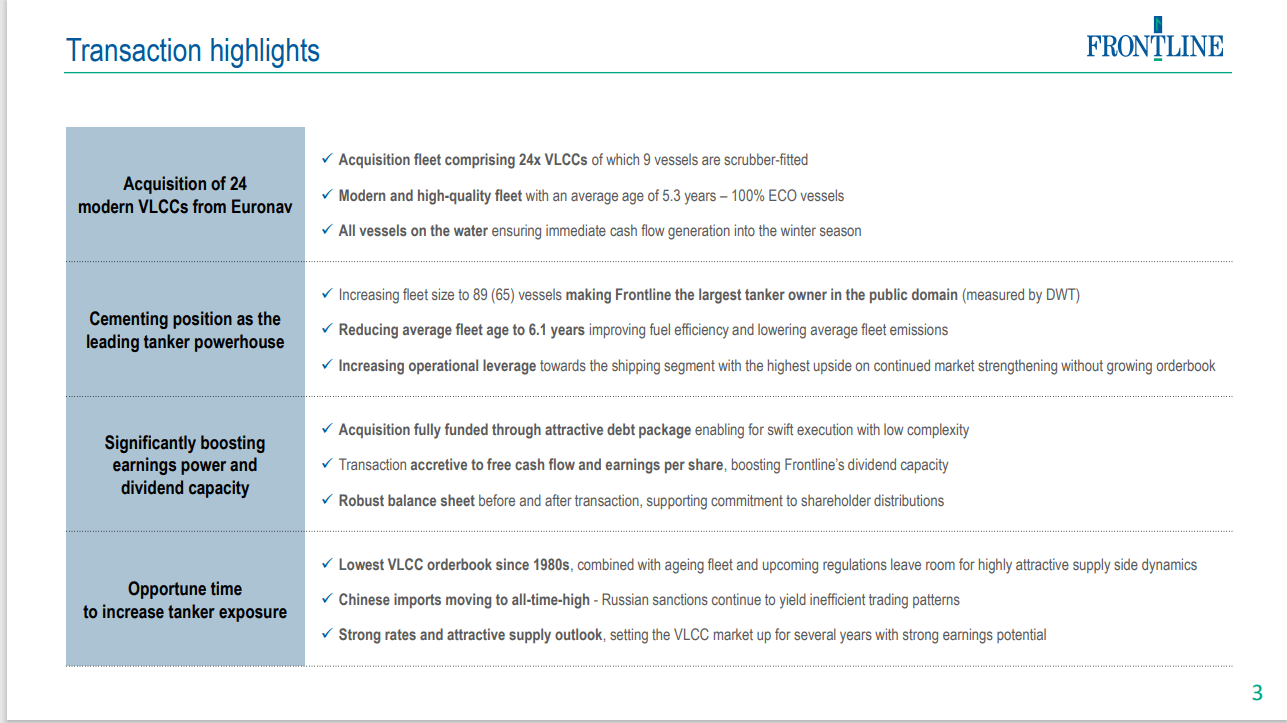

FRO represents a buying opportunity with the additions to their fleet. With the recent VLCCs acquired from Euronav, FRO will have the largest and youngest tanker fleet in the world, according to their October 9 presentation , at a very opportune time to be increasing the fleet.

{kind=link}

Another analyst on SA recently wrote a detailed article outlining the reasons why FRO is now a Strong Buy, including the 11.5% dividend yield based on the latest quarterly dividend of $.80 (paid September 29). The advantages of the fleet additions are summarized succinctly by the author, so I quote:

Frontline's fleet age profile will improve after its acquisition of Euronav vessels. That has a few implications/advantages. First, newer vessels are more efficient - in simple words, they will use less and cleaner fuel to cover the same distance. Strict air pollution restrictions put limits on shipping companies regarding the fuel they use. The older the ship, the more modifications are required to modify its equipment to meet regulatory requirements.

The second advantage is that the company is not forced to order new ships. This will significantly reduce its CAPEX. Besides, it is worth mentioning that shipyards have their books filled with orders for all types of vessels except VLCCs for the next few years. The chart below shows how the order book compares to the current VLCC fleet globally.

New ships are expensive, take years to build, and are limited by shipyard capacity. Therefore, FRO has an advantage over its competitors with a younger, larger fleet. According to a press release from Frontline, the acquisition is funded by a combination of the EURN share sales, cash, drawdowns on existing credit facilities, and a new 5-year secured loan, along with a loan from Hemen Holding, which is also a John Frederiksen company and Frontline’s largest shareholder .

Tanker rates rising

From the Frontline mid-year report as of June 30, 2023, cash flows have been increasing in 2023 due to rising tanker rates from the combination of increasing demand and constrained supply.

Net cash provided by operating activities in the six months ended June 30, 2023, was $553.2 million compared to $91.7 million in the six months ended June 30, 2022.

We estimate that average daily cash break-even TCE rates for the remainder of 2023 will be approximately $27,000, $23,400 and $16,600 for our owned VLCCs, Suezmax tankers, and LR2/Aframax tankers, respectively. These are the daily rates our vessels must earn to cover budgeted operating expenses including dry dock expenses, estimated interest expenses, scheduled loan principal repayments, bareboat hire, time charter hire and net general and administrative expenses. These rates do not take into account capital expenditures.

In an article dated June 22, 2023, the explanation for rising tanker rates and expectations for the second half of 2023 helps to explain why those cash flows have been improving and are expected to continue into 2024.

After sinking to fresh lows in the early part of the year, freight rates for U.S.-loading supertankers have skyrocketed as Asian refiners turn to the U.S. market amid production cuts elsewhere. Average spot rates for older very large crude carriers (VLCCs) climbed to $83,300 per day while rates for newer and more fuel-efficient VLCCs hit $91,000 per day.

Shipping rates tend to rise during periods of heightened demand or geopolitical tensions. Operators demand higher compensation to send their vessels into dangerous waters, and underwriters bump up the cost to insure ships and their cargo against potential threats, increasing war risk premiums. Sanctions on Russia’s energy and maritime shipping sectors have forced crude oil buyers in Europe to purchase their crude oil imports from other markets.

With a breakeven cost of $27,000 a day for VLCC and spot rates as high as $91,000 back in June, it is not surprising that FRO has seen tremendous cash flows. And rates have continued to increase with the additional conflict in Israel further bumping up the insurance premiums, although closer to $70K for spot rates now, according to other sources .

The demand for crude oil tankers is another moving target and tends to shift around depending on what is happening with the global economy and the latest developments in regional conflicts. For example, the US recently relaxed sanctions on oil from Venezuela to help boost global flows, which is likely to increase tanker demand.

Concluding Thoughts

According to one shipping expert in SA, product tanker rates in the summer and fall of 2023 have been exceptionally strong. This year may be the second strongest year on record and 2024 could be even better. With the recent acquisition of 24 VLCCs from Euronav, Frontline is poised to benefit greatly from the additional revenues and higher cash flows from the largest and youngest tanker fleet of any publicly traded company.

Euronav shareholders will benefit from the takeover bid if they are already holding shares purchased at lower prices than the current closing price of $17.87, but I would not expect that there is very much, if any upside remaining now that the agreement with CMB and Frontline has been made.

Frontline shareholders will likely benefit from an increasing share price based on future earnings upside along with a hefty dividend yield of 11.5% at the current price with good dividend coverage. There is some risk to the stock if tanker rates suddenly reverse and global demand drops, for example, if we go through another deep recession like what occurred in 2008-2009. My belief is that we are not on the precipice of another GFC but perhaps a milder recession in early to mid-2024, and even then, it may not be as detrimental to the tanker industry as it may be to other shipping sectors. There remains a limited supply of tankers and very few newbuilds on order, so the demand/supply balance still favors Frontline with its large and relatively young fleet.

I recently purchased shares of FRO for my income portfolio and look forward to realizing the benefits of a shareholder-friendly shipping company that has solid prospects for growth well into 2024 and beyond.

For further details see:

Euronav And Frontline: Lessons From The Shipping Industry