FRO - Euronav: May Not Be Able To Benefit From The Market Conditions

2023-04-11 15:20:34 ET

Summary

- The VLCC and Suezmax tanker rates are relatively high and despite OPEC+ recent cut announcement, the ton-mile demand is expected to increase.

- However, the management struggle between CMB, Famatown, and EURN’s board members is still going on.

- The company may not be able to benefit from the increased tanker rates and/or stick to a consistent strategy.

- The stock is a hold.

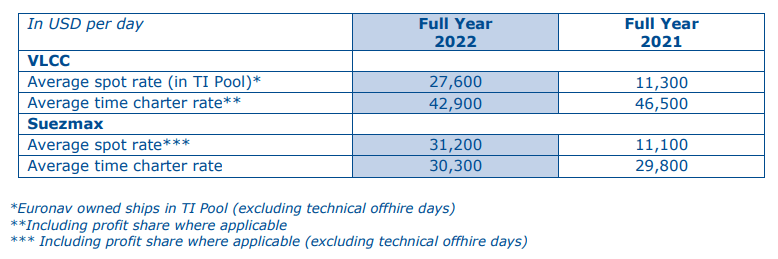

In 2022, Euronav NV ( EURN ) reported revenue of $855 million, up 104% YoY, driven by hiked spot rates. According to Figure 1, EURN’s VLCC average spot rate increased from $11300/d in 2021 to $27600/d in 2022. Also, its Suezmax spot rate increased from $11100/d in 2021 to $31200/d in 2022. It is important to know that EURN’s VLCC 2022 average time charter rate which didn’t change so much compared to 2021, was 55% higher than its VLCC average spot rate. The company’s loss of $339 million in 2021 turned into a profit of $203 million in 2022. Considering the net interest expenses of $106 million, and depreciation of tangible and intangible assets of $223 million, Euronav reported a 2022 EBITDA of $534 million, compared with $86 million in 2021. The tanker shipping market outlook is in favor of EURN. However, the war between a great portion of board members, Famatown, which owns 25% of EURN, and Compagnie Maritime Belge ((CMB)), which also owns 25% of EURN is not finished yet and could limit the management's ability to pursue a consistent strategy, likely imposing great risks on other shareholders.

Figure 1 – EURN’s TCE rates

{kind=link}

Due to Compagnie Maritime Belge’s ((CMB)) call, a special meeting of Euronav shareholders was held on 23 March. CMB is a large minority shareholder of EURN and asked shareholders to replace the Supervisory Board with five directors that it had handpicked. Euronav announced that this would make CMB effectively take the control of the company, change its strategy and governance and affect the share price negatively. Here is the story:

CMB has been against the merger with Frontline ( FRO ). However, even after the termination of the merger EURN’s board has remained in favor of the merger as it believes that a growth strategy is the right one. Also, EURN’s board claimed that FRO had no right to terminate the merger, and was pursuing a lawsuit against Frontline. As CMB is against the merger with FRO, it called a meeting to change the leadership.

In its presentation at the special general meeting, Euronav argued against CMB’s claims, mentioning that CMB’s ideas are not in favor of shareholders at all. Also, it mentioned that CMB’s selected directors have low alignment with other shareholders’ interests. As CMB proposed replacing the 5 members of the supervisory board, Famatown Finance, which is against CMB’s ideas, proposed the appointment of John Fredriksen (the biggest shareholder and one of the directors of Frontline, and the owner of Famatown) and Cato Stonex. The Euronav board supported the Famatown’s resolution. Finally, on 23 March, shareholders approved CMB’s resolution to terminate the mandates of two of the independent board members (out of five) and voted to maintain three of the independent directors. Shareholders also approved the appointments of four new directors: Fredreksen and Stonex, representing Famatown; and Marc Saverys and Patrick De Brabandere, representing CMB.

It means that there is still a war going on in Euronav, and it is not obvious in the war between Famatown and CMB, which one can be the winner. However, for now, according to the result of the recent special shareholders meeting, it seems that CMB has not been able to take the control of the company entirely.

The market outlook

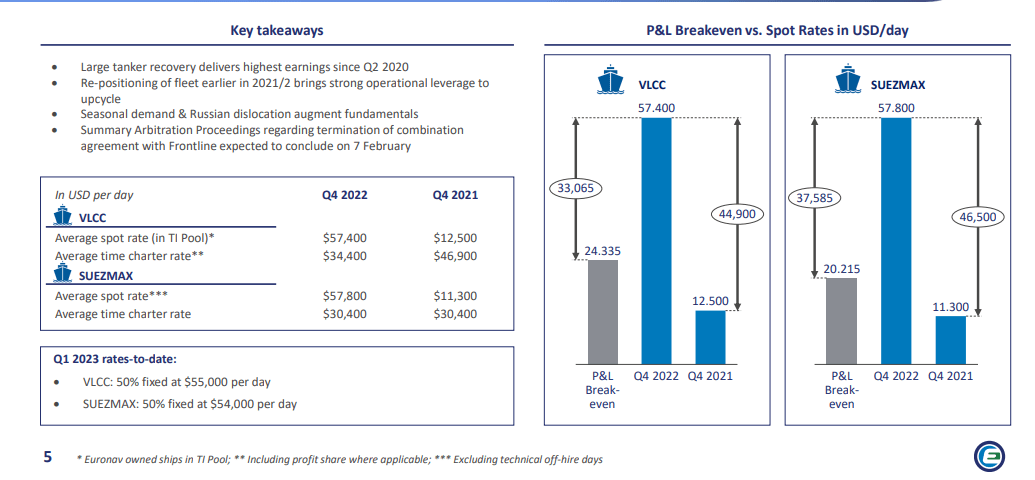

For the first quarter of 2023, EURN had 50% of its VLCC and Suezmax’s available days fixed at $55000/d and $54000 per day, respectively. Figure 1 shows that for its VLCC and Suezmax vessels, the company’s profit & loss breakeven points are 24335/d and $20215/d, respectively (see Figure 2).

Figure 2 – EURN’s profit & loss breakeven point

{kind=link}

60% of EURN vessels are VLCCs and 40% are Suezmax tankers. Euronav revenues are directly linked to the demand for crude oil and dirty products. According to EIA , global petroleum and other liquids consumption in 2023 and 2024 is expected to increase by 1.5% and 1.8%, respectively. Also, the EIA estimated the global petroleum and other liquids consumption in 2H 2023 to be higher than in 1H 2023, driven by higher consumption from China and Europe. It is worth noting that U.S. consumption in 2Q 2023 is expected to be higher than in 1Q 2023. The continuing change in the oil trade flows may increase tanker freight rates in the following months. Europe is still trying to displace Russian oil from the distant market. Also, Russia is trying to find new destinations for its oil as EU sanctions have come into effect on February 2023. European countries can import oil from the United States and the Middle East. Thus, the trade flows can continue changing, causing more ton-mile demand in 2023 and 2024. Meanwhile, the net fleet growth is at record lows. Thus, the market condition is in favor of tanker stocks. However, you should keep an eye on the crude oil prices and the measures of OPEC+ to support oil prices. Last week, OPEC+ announced an oil output cut of 1 million barrels per day, causing oil prices to increase. These kinds of measures have the potential to limit the crude oil demand temporarily, hurting VLCC TCE rates. However, based on the other factors that affect tanker TCE rates, I expect VLCC TCE rates to remain high in the long run. Figure 3 shows the VLCC and Suezmax tanker rates which are now significantly higher than a year ago. However, as a result of higher oil prices, they remained flat in the week ending 5 April 2023.

Figure 3 – Weekly time charter estimates

www.hellenicshippingnews.com

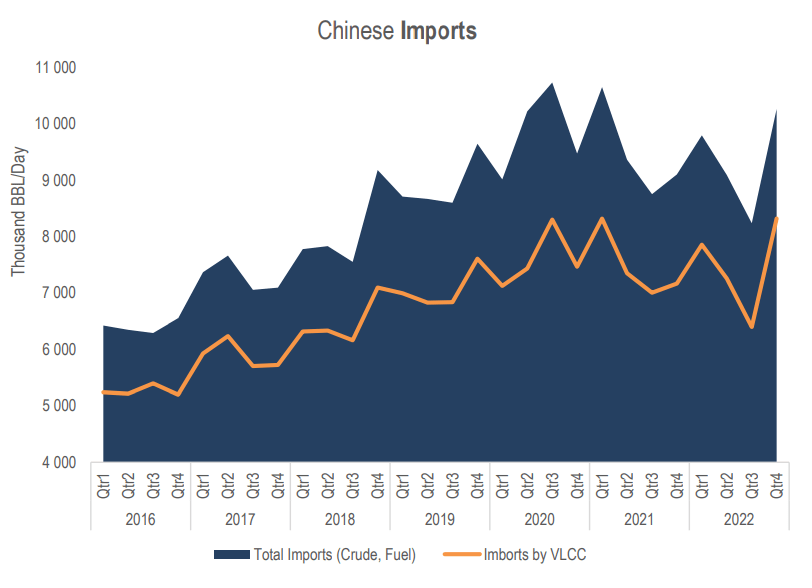

VLCC’s shipment to China is now at its all-time high. According to Figure 4 , Chinese crude oil and fuel imports by VLCCs increased from about 6.5 million barrels per day in 3Q 2022 to about 8.5 million barrels per day in 4Q 2022 and are still increasing. We can see that China’s share of imports by VLCCs jumped in the last quarter of 2022. Driven by hiked U.S. exports, the world crude oil exports are back to the pre-pandemic level. Higher exports from the U.S. to Europe and China mean higher distances, higher demand for tankers, and higher ton-mile demand, that support TCE rates for VLCCs.

Figure 4 – China’s crude oil and fuel imports

{kind=link}

EURN performance

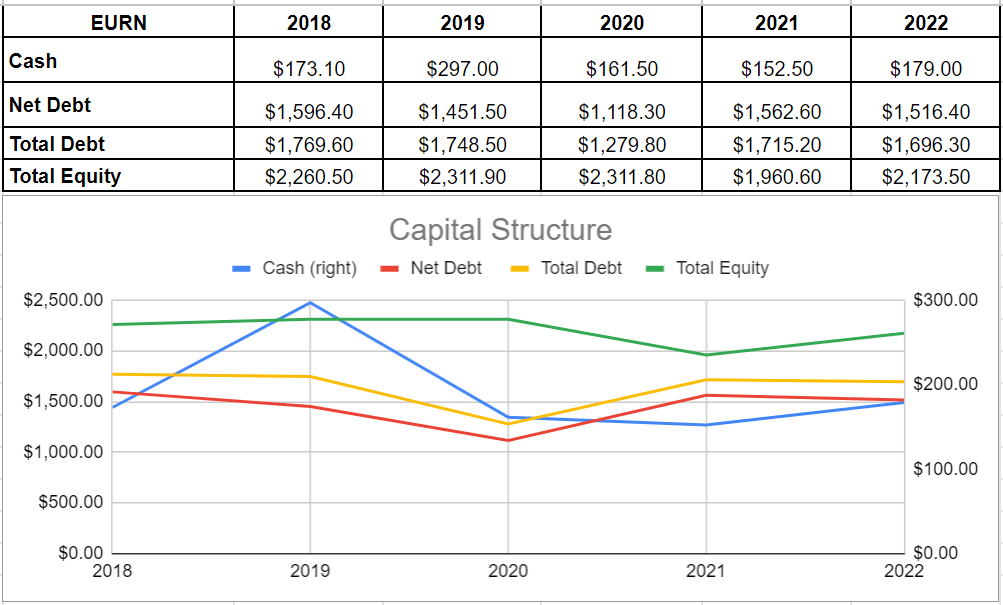

After a deep decline in the company’s cash balance in 2020 and 2021 due to the COVID-19 pandemic, EURN could recover successfully and increase levels back to $179 million of cash and equivalents in 2022. Also, the company saw a decline in its debt level slightly to $1.69 billion in 2022 compared with its level of $1.71 billion at the end of 2021. A combination of lower debt and higher cash generation led to a decline in the net debt of $1.51 billion in 2022 as compared to $1.56 billion in 2021. Furthermore, EURN’s total equity improved slightly by 10% to $2.17 billion in 2022 compared with its previous amount of $1.96 billion at the end of 2021. Thankfully, EURN’s net debt is well beneath its equity level, which could tailor a scope of capacity to bring benefits for its shareholders and assimilate upcoming risks. Thus, Euronav’s capital structure indicates a position that enables the company to be able to pay back its obligations (see Figure 5).

Figure 5 – EURN’s capital structure (in millions)

{kind=link}

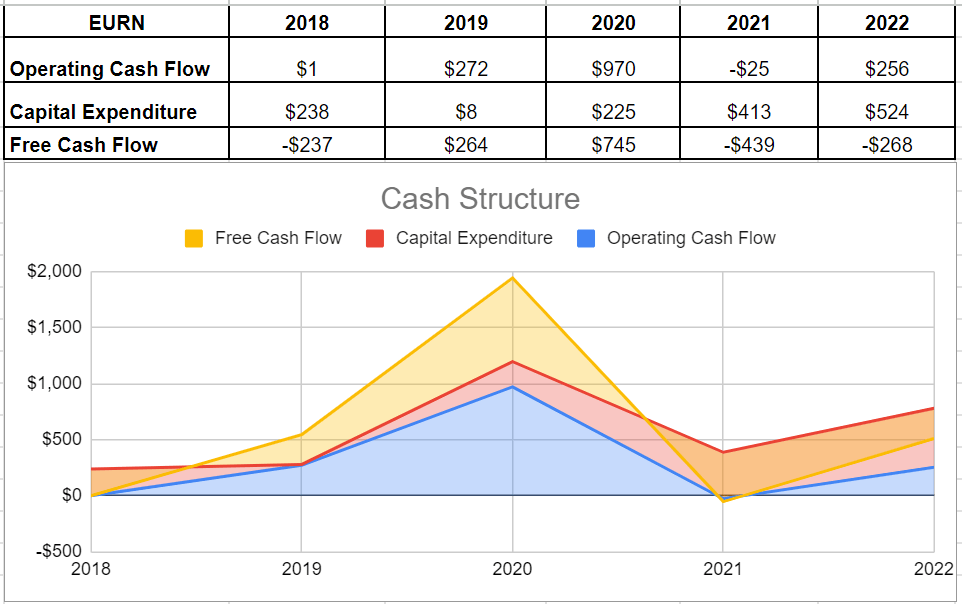

After the downturn of 2021 due to the COVID-19 pandemic, the company increased its cash from operations considerably to $260 million in 2022 versus its previous negative amount of $(25) million in 2021. Additionally, the company increased its capital expenditure to $524 million and thereby leading to $(268) million of free cash flow. Notwithstanding EURN generated a positive amount of cash from operations and decreasing its negative free cash flow in 2022 compared with a free cash flow of $(439) million during 2021, the company still has no cash on hand for more distributions and thus this could be a sign of EURN’s poor financial health (see Figure 6).

Figure 6 – EURN’s cash structure (in millions)

{kind=link}

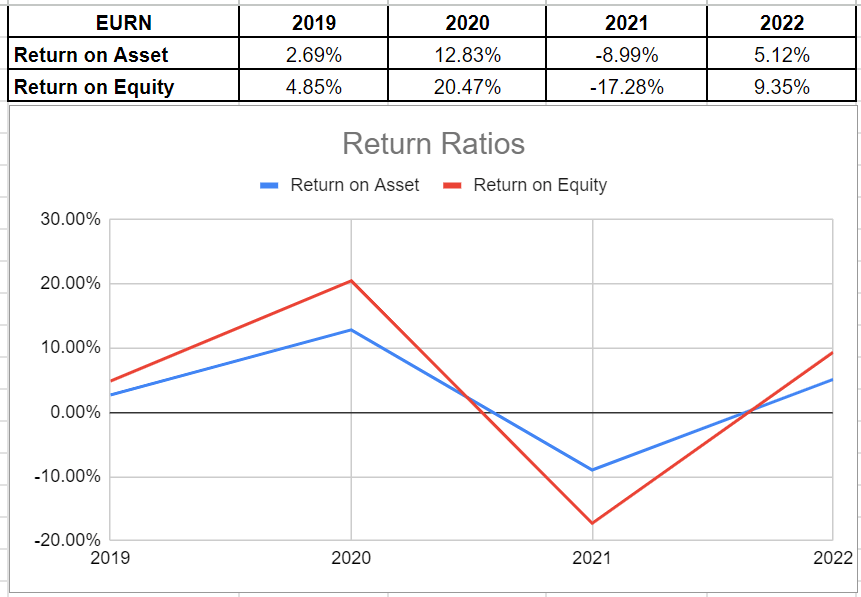

To wrap up the company’s performance outlook, I looked into EURN’s return on equity and return on assets ratios to show how well the company can tailor returns to its shareholders. The ROA ratio illustrates the amount of profit a company may produce for each dollar of its assets. The ROA ratio of (8.9)% for Euronav in 2021 was boosted by 1411 bps to 5.12% in 2022. However, it is still far lower than its 20% of return on assets at the end of 2020. Additionally, its return on equity of 9.35% in 2022 is considerably higher than the negative amount in 2021. The ROE ratio shows the company's net income concerning shareholders' equity and is paramount since it calculates the rate of return on the capital invested in the business. Thus, as it is obvious, EURN’s negative return ratios were signs of the business’s inability to obtain the expected benefits and were generating losses. However, albeit with relatively unchanged assets and equity, Euronav improved the return ratios by boosting its net income to $203 million in 2022. Thus, despite a good recovery after the pandemic, I believe Euronav needs to provide a more solid financial structure (see Figure 7).

Figure 7 – EURN’s return ratios

{kind=link}

Summary

Due to the hiked VLCC and Suezmax tanker rates, the company’s revenue in 2022 increased. Euronav’s return on assets and return on equity improved considerably to 5.12% and 9.35%, respectively, in 2022. However, despite a good increase in cash from operations, the company generated negative free cash flow for the second year in a row in 2022. The market outlook is in favor of EURN. But, the management war in the company’s board is still going on, hurting its operations. The stock is a hold, therefore.

For further details see:

Euronav: May Not Be Able To Benefit From The Market Conditions