EEFT - Euronet Worldwide: A Drop In Valuation Makes For A Buy Case

2023-08-20 02:19:27 ET

Summary

- Fintech companies like Paysafe and PayPal have faced criticism for lacking strong margins, but Euronet Worldwide Inc. has seen its stock price drop despite continued growth.

- EEFT operates in the financial sector, providing payment and transaction processing solutions for various clients globally.

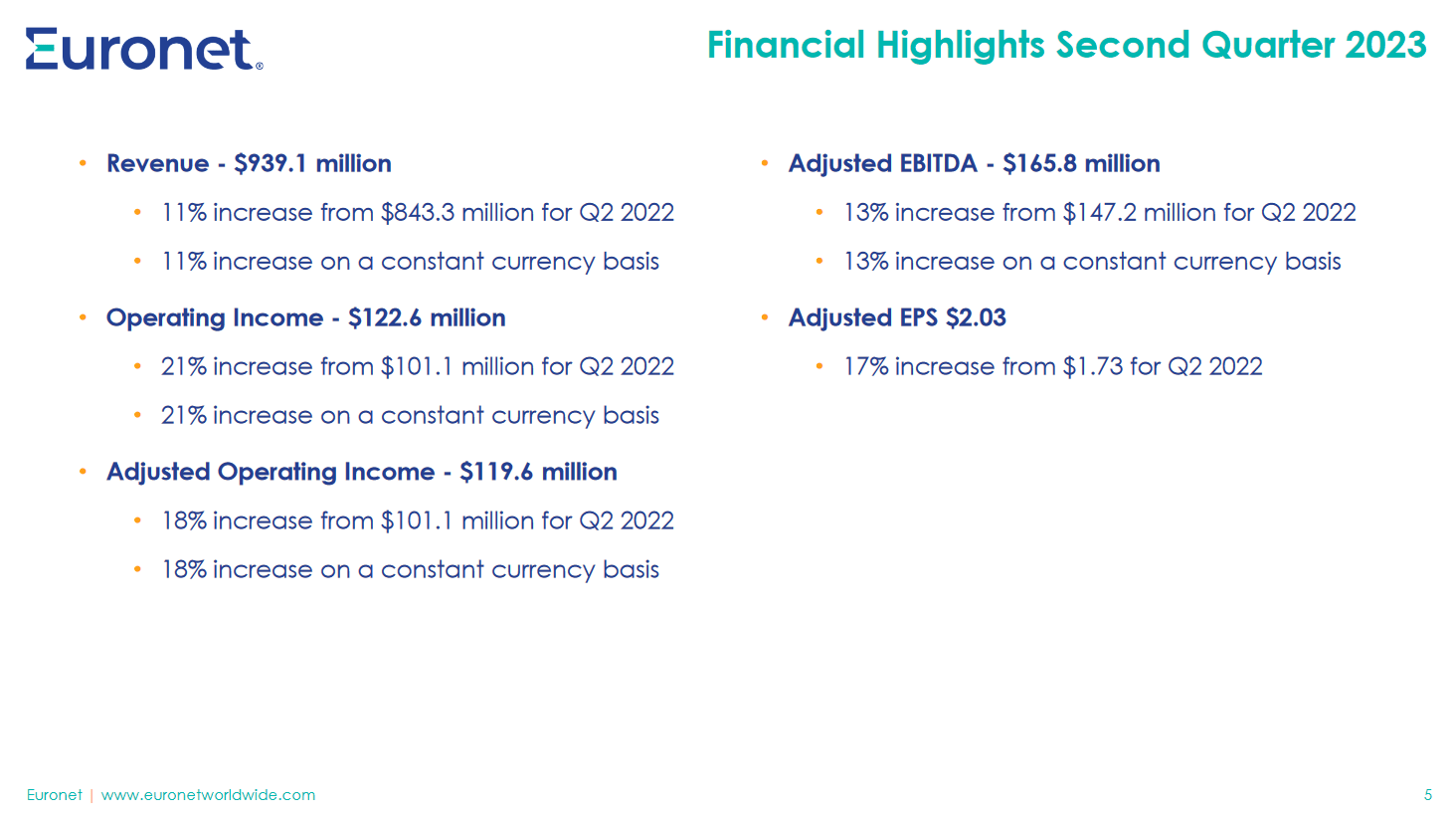

- The company's growth has slowed slightly, but it continues to deliver solid results, with double-digit growth in both top and bottom lines. The epay segment is growing rapidly.

Introduction

Fintech companies have been getting a lot of heat after the run-up in 2021 as a lot of them were lacking strong margins, some companies that come to mind are Paysafe ( PSFE ) but also larger institutions like PayPal (PYPL), which at least have decent margins. But for Euronet Worldwide, Inc. ( EEFT ) the price has come down quite a lot and now trades at a p/e of just 11, which is slightly above where most financial companies are at today. But since the company is included as a growth stock then any form of a miss on earnings will send the share price tumbling, which is what happened when the last report came out. The share price dropped nearly 30% despite growth continuing. It might not be like it was last year but seeing 17% YoY growth for EPS should constitute a higher price than where it's right now.

I like the prospects of the company and it seems the worst has passed following the share price drop after earnings and getting in now looks very appealing. Rating EEFT a buy as a result.

Company Structure

As we know, EEFT is included in the financials sector but more specifically focuses on providing payment and transaction processing and distribution solutions for a variety of customers and clients. Some of these clients include financial institutions, retailers, and individual consumers on a global scale.

The company has divided its operations into three various segments which are Electronic Fund Transfer Processing, epay, and lastly Money Transfer. Within the first segment, the operations revolve around providing electronic payment solutions which include ATM and cash withdrawals. Besides that, they also offer credit and debit card outsourcing and merchant acquiring services.

{kind=link}

Growth has been consistent over the last few years as the company continues to deliver solid results. But the perhaps slight slowdown that has been noticeable from the last report was not appreciated by the market and a lower premium was set to the stock as a result. In terms of the actual performance from the quarter, I think it was solid, double-digit growth for both the top and bottom lines. EPS came in at $1.73 for the quarter and resulted in EEFT having a TTM net margin of 7.71% right now.

epay (Investor Presentation)

The epay segment of the company is growing rapidly and last quarter showcased a 15% growth rate on a YoY basis. This has been driven by strong initiatives by the company like signing agreements for distributions and ensuring their product is one of the first things customers get to use.

Earnings Transcript

Seeing as the growth was slowing down somewhat getting some comments from the management about their views on the market and recent performance I think will shed some much-needed light on the future potential here. The CEO Rick Weller said the following in the last earnings call.

-

“As we have discussed in prior quarters over the last three years, our international transactions have generally recovered consistently with the recovery of international travel. Beginning in the latter part of the quarter, we began to see a divergence from the recovery of international travel, leading to a flattening of our international transaction growth year-over-year”.

I don’t think anything was anticipating a swift recovery in travel but a more steady upwards trend of activity and bookings. This is why the company is not likely to see such sharp climbs in the top and bottom lines as in previous years. I think these are short-term headwinds and the long-term outlook remains very solid as the company continues to grow, just not at the same pace as previously.

-

“Margins in epay remained relatively constant year-over-year. Money Transfer revenue grew 7% with operating income and adjusted EBITDA growing 15% and 12%, respectively. This growth was the result of 11% growth in U.S. outbound transactions, 11% growth in transfers initiated largely in Europe and 12% growth in transfers initiated in the Middle East and Asia, and 30% growth in xe transactions, partially offset by a 17% decline in U.S. domestic business”.

What I think is slightly missed is the solid margin retention the company has been able to have in recent quarters. Despite higher interest rates they continue being able to grow efficiently. This should be rewarded with a higher premium than what they currently are getting, which is what leads to my buy rating.

Risk Associated

As we look ahead, my perspective revolves around the primary concern of EEFT potentially encountering a deceleration in its revenue growth trajectory. This apprehension gains relevance in scenarios where economic conditions take a downturn, subsequently impacting the demand for cash withdrawal services – a cornerstone of Euronet's operations.

Furthermore, another aspect to consider is the inherent susceptibility to a plateau in travel demand. Should travel demand reach a saturation point from its current trajectory, it could exert a notable influence on the demand for cash withdrawal services. This could, in part, contribute to the recent decline observed in the company's stock value.

Segment Growth (Investor Presentation)

It's important to acknowledge the multifaceted nature of these potential challenges. While the growth of EEFT has been impressive, external factors like economic fluctuations and shifts in consumer behavior can disrupt the company's revenue stream. This seems to have been the case in recent quarters as growth hasn't been at the same levels as years prior. The company is still quite small in the financial sector with a market cap of just above $4 billion. But seeing as they are a growing company, any slight missteps or failures to meet expectations will likely be met by having the share price slashed as much as it was in recent weeks.

Investor Takeaway

One of the main appeals right now with EEFT I think is the unjustified contraction the share price got following the last report. It may have been a miss on revenues by just $2.8 million, but dropping nearly 30% in value seems harsh. I think that the quarter was solid and given the macroeconomic challenges that still exist, the company did well regarding margin retention and expanding the EPS by 17% YoY.

I think a p/e of around 13 - 14 should be applied and given that the company is standing below that I am rating EEFT a buy right now.

For further details see:

Euronet Worldwide: A Drop In Valuation Makes For A Buy Case