EEFT - Euronet Worldwide: Revenue Growth Continues Despite Inflationary Pressures

2023-10-30 04:37:19 ET

Summary

- Euronet Worldwide has the potential for longer-term upside due to continued revenue growth and an attractive P/E ratio.

- Q3 2023 earnings show net income up by 7% YoY and revenues up by nearly 8% YoY.

- While there has been pressure on earnings, I continue to take a bullish view due to the company's revenue growth and attractive valuation.

Investment Thesis

I take the view that in spite of pressure on earnings, Euronet Worldwide ( EEFT ) can continue to see longer-term upside on the basis of continued revenue growth and an attractive P/E ratio.

In a previous article back in August, I made the argument that Euronet Worldwide is to see further upside from here, on the basis of continued revenue growth across the EFT Processing segment, in addition to a decline in the long-term debt to total assets ratio.

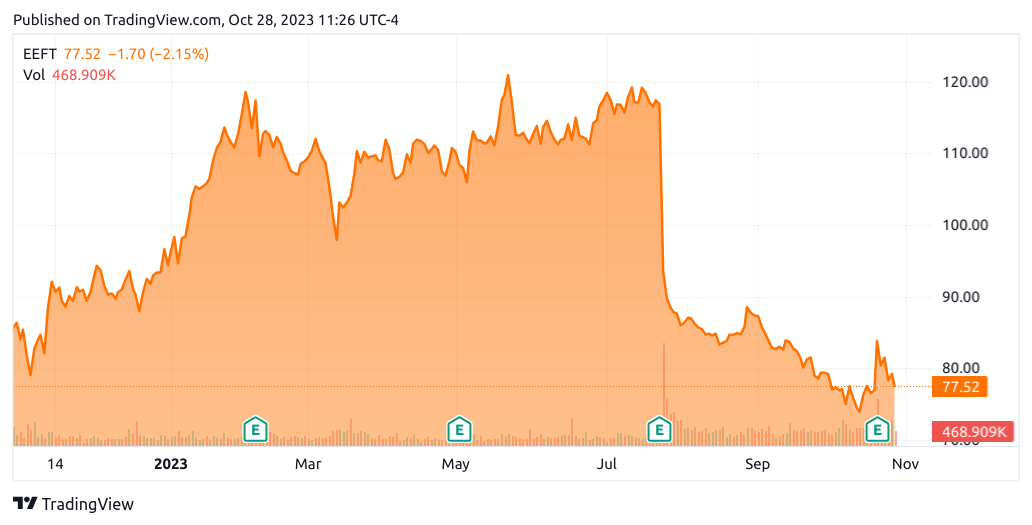

Since then, the stock has descended to a price of $77.52 at the time of writing:

{kind=link}

TradingView.com

The purpose of this article is to assess whether Euronet Worldwide has the ability to see a rebound in growth from here taking recent performance into consideration.

Performance

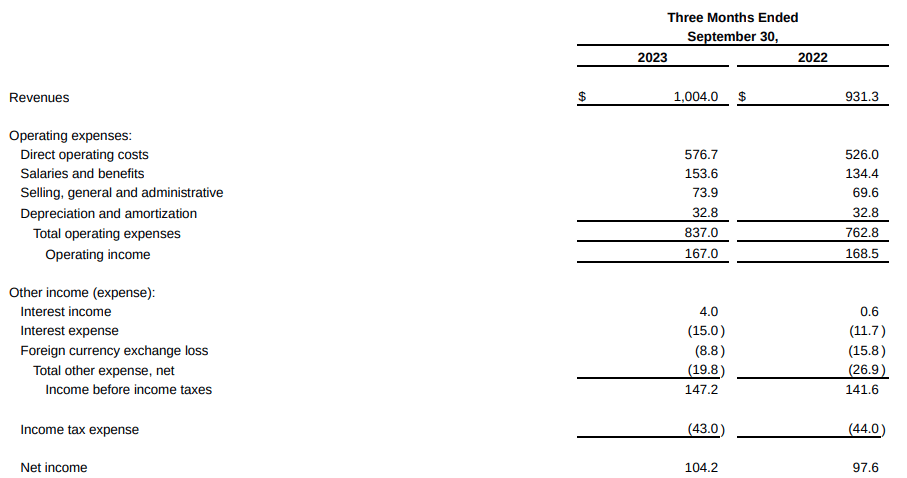

When looking at Q3 2023 earnings results for Euronet Worldwide, we can see that net income is up by just under 7% YoY, with revenues up by nearly 8% YoY over the same period.

{kind=link}

Euronet Worldwide: Q3 2023 Financial Results

Additionally, the EFT Processing segment has continued to see growth in revenue - up by just over 8% from that of the same quarter last year.

Revenue figures (in millions of U.S. dollars) sourced from Euronet Worldwide Historical Form 10-Qs. Heatmap generated by author using Python's seaborn visualization library.

The EFT Processing segment is Euronet's largest segment by revenue - followed by Money Transfer and ePay. For EFT Processing, revenue growth has primarily been driven by expansion into growth markets such as Asia as well as continued growth in the point-of-sale acquiring business. However, this segment had also seen a decrease in adjusted EBITDA of 8% to $128.7 million in the most recent quarter (12% on a constant currency basis) - with inflationary pressures leading to a decline in travel as well as Croatia's switch from the kuna to the euro at the start of this year leading to less international transactions.

In this regard, while overall revenue and transaction volume have increased - the segment has seen pressure on earnings growth. The ePay segment also saw a decrease in adjusted EBITDA of 1% to $30.1 million (5% on a constant currency basis) - which was driven by declines in promotional campaigns from the same quarter in the previous year that were discontinued this year, as well as inflationary pressures impacting operating expenses as well as challenges from the Indian market.

The only segment to see positive earnings growth was the Money Transfer segment - which saw strong growth in adjusted EBITDA of 24% (20% on a constant currency basis) from $48.9 million to $60.7 million, which was driven by growth in US-outbound transactions, initiated transfers in Europe, Middle East and Asia as well as an 18% growth in foreign exchange transactions.

From a balance sheet standpoint, we can see that with regards to short-term liquidity, the quick ratio of Euronet Worldwide (calculated as cash and cash equivalents plus trade accounts receivable all over total current liabilities) has seen a decrease from that of the previous quarter - standing at 0.54 in September as compared to 0.59 in June of this year.

| Dec 2021 |

| Sep 2022 |

| Dec 2022 |

| Jun 2023 |

| Sep 2023 |

| Cash and cash equivalents |

| 1260.5 |

| 967.1 |

| 1131.2 |

| 1137.5 |

| 1074.4 |

| Trade accounts receivable, net |

| 203 |

| 225.2 |

| 270.8 |

| 242.6 |

| 300.6 |

| Total current liabilities |

| 1852.6 |

| 2170.4 |

| 2354.1 |

| 2337.2 |

| 2568.8 |

| Quick ratio |

| 0.79 |

| 0.55 |

| 0.60 |

| 0.59 |

| 0.54 |

Source: Figures sourced from Euronet Worldwide Form 10-Qs (Q3 2022, Q4 2022, Q2 2023, Q3 2023). Figures provided in millions of USD, except the quick ratio. Quick ratio calculated by author as cash and cash equivalents plus trade accounts receivable all over total current liabilities.

With that being said, we can also see that the long-term debt to total assets ratio still remains lower than that seen in the previous September - down from 0.30 to 0.24.

| Dec 2021 |

| Sep 2022 |

| Dec 2022 |

| Jun 2023 |

| Sep 2023 |

| Debt obligations, net of current portion |

| 1420.1 |

| 1428.5 |

| 1609.1 |

| 1306.5 |

| 1263.0 |

| Total assets |

| 4744.3 |

| 4827.8 |

| 5403.6 |

| 5221 |

| 5162.9 |

| Long-term debt to total assets ratio |

| 0.30 |

| 0.30 |

| 0.30 |

| 0.25 |

| 0.24 |

Source: Figures sourced from Euronet Worldwide Form 10-Qs (Q3 2022, Q4 2022, Q2 2023, Q3 2023). Figures provided in millions of USD, except the long-term debt to total assets ratio. Long-term debt to total assets ratio calculated by author.

In this regard, the fact that Euronet Worldwide has been decreasing its long-term debt is encouraging, and I take the view that investors would be more willing to tolerate a quick ratio below 1 for as long as we continue to see a decrease in long-term debt.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, we have seen that continued revenue growth across EFT Processing has not been sufficient to induce growth in the stock - as inflationary pressures and slowing market conditions have placed downward pressure on earnings growth.

In this regard, I take the view that the trajectory for the stock will be dependent in significant part on the broader macroeconomic climate going forward. Should we continue to see weakness in economic growth - and particularly a continued decline in travel leading to lower international transactions - then this will continue to place pressure on earnings going forward.

I had previously made the argument that in spite of challenges - Euronet Worldwide continues to trade at good value on a price to earnings basis with the P/E ratio having been at a 5-year low with earnings per share continuing to climb near a 5-year high.

ycharts.com

We see that this continues to be the case. If the P/E ratio were to grow from here and earnings per share were to remain at $5.24 - then the following target prices would be yielded:

| P/E Ratio |

| Target Price |

| 20 |

| $104.80 (20 * 5.24 = 104.80) |

| 40 |

| $209.60 (40 * 5.24 = 209.60) |

| 60 |

| $314.40 (60 * 5.24 = 314.40) |

Source: Target prices calculated by author.

From this standpoint, I take the view that while Euronet Worldwide has been facing pressure on earnings - the fact that revenues are continuing to see growth is encouraging and for this reason, I continue to take the view that Euronet Worldwide has significant scope for upside once economic conditions improve.

Conclusion

To conclude, Euronet Worldwide has seen pressure on earnings growth as a result of inflationary pressures. However, the stock continues to be attractively valued from an earnings standpoint and revenue growth continues to remain vibrant. For these reasons, I continue to take a bullish view on Euronet Worldwide stock.

For further details see:

Euronet Worldwide: Revenue Growth Continues Despite Inflationary Pressures