IEV - Europe's Inflation Outlook Depends On How Corporate Profits Absorb Wage Gains

2023-06-26 21:45:00 ET

Summary

- Rising corporate profits account for almost half the increase in Europe’s inflation over the past two years, as companies increased prices by more than spiking costs of imported energy.

- Europe’s businesses have so far been shielded more than workers from the adverse cost shock.

- Should wages increase more significantly - by, say, the 5.5 percent rate needed to guide real wages back to their pre-pandemic level by end-2024 - the profit share would have to drop to the lowest level since the mid-1990s (barring any unexpected increase in productivity) for inflation to return to target.

By Niels-Jakob Hansen, Economist, Western Hemisphere Department; Frederik Toscani, Economist, European Department, IMF; Jing Zhou, Economist, Germany team, IMF’s European Department

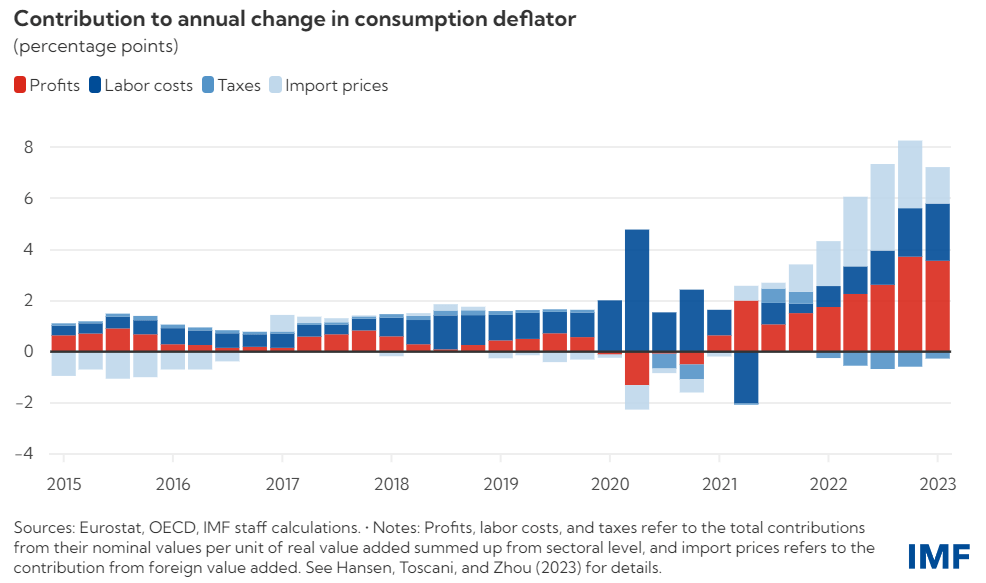

Higher prices so far mostly reflect increases in profits and import costs, but labor costs are picking up.

Rising corporate profits account for almost half the increase in Europe’s inflation over the past two years, as companies increased prices by more than spiking costs of imported energy. Now that workers are pushing for pay rises to recoup lost purchasing power, companies may have to accept a smaller profit share if inflation is to remain on track to reach the European Central Bank’s 2 percent target in 2025, as projected in our most recent World Economic Outlook .

Inflation in the euro area peaked at 10.6 percent in October 2022 as import costs surged after Russia’s invasion of Ukraine and companies passed on more than this direct increase in costs to consumers. Inflation has since retreated to 6.1 percent in May, but core inflation - a more reliable measure of underlying price pressures - has proven more persistent. This is keeping the pressure on the ECB to add to recent interest rate rises even though the euro area slipped into recession at the start of the year. Policymakers raised rates to a 22-year high of 3.5 percent in June.

As the Chart of the Week shows, the higher inflation so far mainly reflects higher profits and import prices, with profits accounting for 45 percent of price rises since the start of 2022. That’s according to our new paper , which breaks down inflation, as measured by the consumption deflator, into labor costs, import costs, taxes, and profits. Import costs accounted for about 40 percent of inflation, while labor costs accounted for 25 percent. Taxes had a slightly deflationary impact.

Inflation drivers

Corporate profits now account for nearly half of all euro area inflation.

{kind=link}

In other words, Europe’s businesses have so far been shielded more than workers from the adverse cost shock. Profits (adjusted for inflation) were about 1 percent above their pre-pandemic level in the first quarter of this year. Meanwhile, compensation of employees (also adjusted) was about 2 percent below trend. This is not the same as saying that profitability has increased, as discussed in our paper.

Previous episodes of surging energy prices suggest that labor costs’ contribution to inflation should grow going forward. In fact, it has already picked up over recent quarters. At the same time, the contribution from import prices has fallen since its peak in mid-2022.

This lag in wage gains makes sense: wages are slower than prices to react to shocks. This is partly because wage negotiations are held infrequently. But after seeing their wages drop by about 5 percent in real terms in 2022, workers are now pushing for pay rises. The key questions are how fast wages will rise and whether companies will absorb higher wage costs without further increasing prices.

Assuming that nominal wages rise at a pace of around 4.5 percent over the next two years (slightly below the growth rate seen in the first quarter of 2023) and labor productivity stays broadly flat in the next couple of years, businesses’ profit share would have to fall back to pre-pandemic levels for inflation to reach the ECB’s target by mid-2025. Our calculations assume that commodity prices continue to decline, as projected in April’s World Economic Outlook.

Should wages increase more significantly - by, say, the 5.5 percent rate needed to guide real wages back to their pre-pandemic level by end-2024 - the profit share would have to drop to the lowest level since the mid-1990s (barring any unexpected increase in productivity) for inflation to return to target.

As noted in our recent review of the euro area economy, macroeconomic policies thus need to remain tight to anchor expectations and maintain subdued demand. This would coax firms to accept a compression of the profit share and real wages could recover at a measured pace.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Europe's Inflation Outlook Depends On How Corporate Profits Absorb Wage Gains