FPXE - Europe's Out-Performance Could Continue For A Few Key Reasons

2023-05-14 08:00:00 ET

Summary

- European equities have been a surprise out-performer in 2023. This momentum has been a welcome sign for investors in the region, and there is a chance it could continue.

- Key factors include below-average valuations, well-capitalized banks, and higher levels of investment than in the UK.

- Market sentiment is also fairly negative, meaning this top-performing sector idea is actually still a contrarian play.

- There are still multiple risks to this idea - aside from equity prices being at elevated levels. Other headwinds are the Russian-Ukrainian conflict and earning cuts/downgrades.

Main Thesis & Background

The purpose of this article is to evaluate the state of the large-cap European equity market, its out-performance in 2023, and the tailwinds and headwinds facing the sector that will determine whether this out-performance continues in the second half of the year.

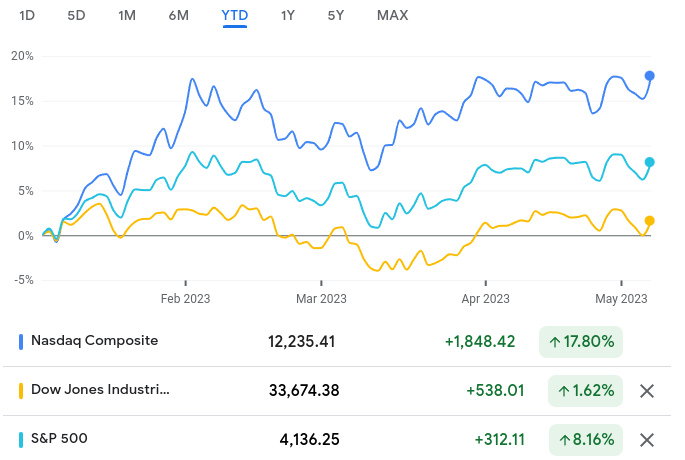

First, a little perspective. As a domestic-oriented US investor, 2023 has been a challenging year but miles better than 2022. We have seen Tech shares rebound strongly and all the major indices are in the green for now:

{kind=link}

US Market Performance (YTD) (Google Finance)

Great news, right?

The answer is "mostly" yes. Strong gains are never something to scoff at, to be sure, and the NASDAQ's rise is a welcome development after the poor performance we saw in the last calendar year. But as with everything else, these gains need perspective. With the exception of the DOW, the S&P 500 and the NASDAQ has pumped out what looks like strong gains that don't necessarily warrant any "under the hood" analysis. After all, who wouldn't like 8 -18% gains in five months?

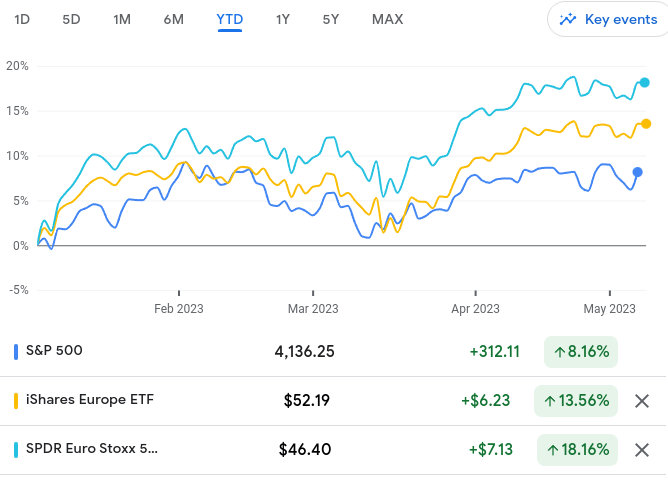

I know I am just pleased with those returns. But what is striking is the gain from the S&P 500 is actually well below what large-cap European ETFs have delivered this year. Below shows the S&P 500 against two popular Euro-ETFs:

{kind=link}

YTD Performance (US vs. Europe) (Google Finance)

Again, this doesn't make the S&P 500 "bad" for this year. Quite the contrary. But it does at the very least warrant an examination on why Europe is doing so well and how likely that is to continue. After some research, I see a number of key elements behind the surge in shares prices that justify a continued buy case going forward. Of course, there are risks I will examine as well. But the overriding theme is the bullish momentum is strong and justifiable for now.

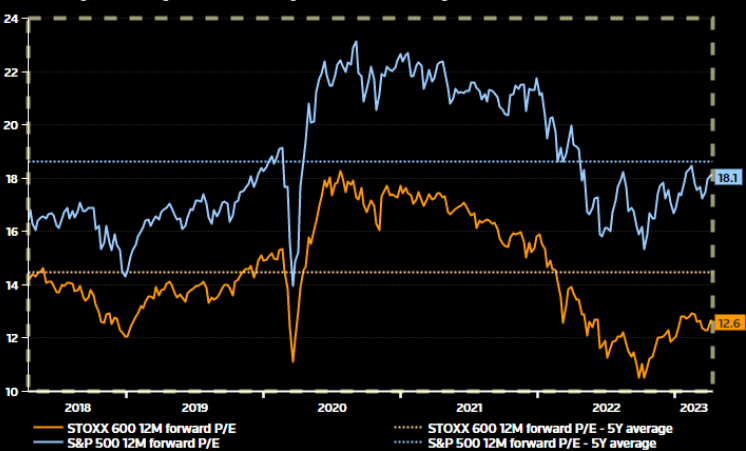

P/E Has Risen, But Remains Cheap Compared To US

One easy reason for Europe's performance in 2023 was the price to own it. Last year, Europe did not perform particularly well and the world was keenly focused on the Russia-Ukraine military conflict. This pushed down sentiment, forward expectations, and the number of buyers in the region. The net result was a sharp drop in the P/E for equities as earnings were supposed to come under pressure in a big way. Fast forward to today and, even with the surge in equity prices, we see that Europe is still cheap on both a historical basis and compared to US equities (as measured by the P/E of the S&P 500):

{kind=link}

Large-Cap Stock PE's (US vs. Europe) (Reuters)

This exercise tells me a number of things. One, value-oriented investors saw the value in Europe when the broader investment community fled it. This has worked out, and absolute P/E values suggest more gains are likely. So, for those who missed the boat and still want value - Europe still has it.

Two, an earnings depression didn't materialize. The world has learned to cope with the conflict in eastern Europe and large-cap European companies are managing just fine. This isn't to ignore the humanitarian nightmare occurring in the region. But as investors we have to be realists. The biggest corporations in places like Germany, France, Switzerland, and Spain are international companies. Not only are they removed geographically from the conflict given the buffer zone the rest of eastern Europe provides, they do business all over the globe. Therefore, the headwind from supply-chain issues and demand concerns in eastern Europe are not all-inclusive on their balance sheets.

Three, demand has picked up in places such as North America and Asia. This has allowed earnings to be better-than-expected in late 2022 and early 2023, keeping P/E ratios low despite rising share prices.

The broader takeaway here is that Europe had value when the year started, and it still does today. That doesn't mean gains are automatically going to continue. And I would certainly exercise some caution given the rapid rise in share prices to-date. But it does mean that a positive catalyst that existed six months ago still exists today. That means a buy case can easily be made.

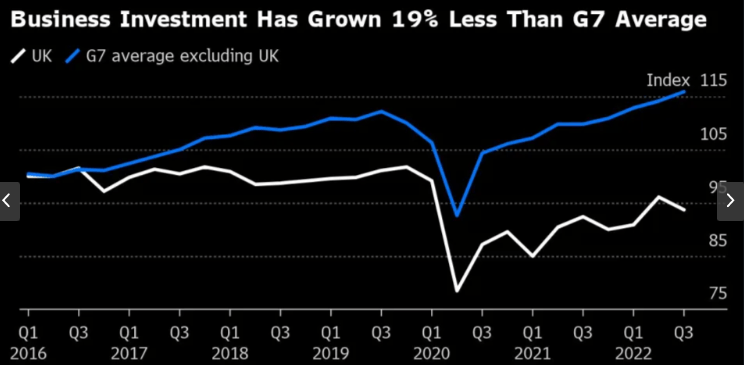

EU-Zone Investment Dwarfs UK's

A second reason to consider Europe has to do with its attractiveness compared to the United Kingdom. This is the second biggest powerhouse in the region and the largest outside the EU-zone. Therefore, for investors looking across the pond for opportunity, a comparison of British and European-domiciled firms is a practical exercise to undertake.

With respect to British large caps, they have been doing quite well in 2023 also. But let us consider the future outlook. Britain continues to be plagued by issues stemming from the pullout of the EU, and consumer and investor confidence are on the decline within the island. This has led to a drop in business investment growth, which is simultaneously on the rise within the G7, including France, Germany, and Italy - all of which are in the EU:

{kind=link}

Business Investment Growth (UK vs. EU-Zone) (Bloomberg)

For the longer term this is a big concern of mine. I saw a lot of value in British equities last year when they were completely out of favor. But now big gains have been realized - in US, European, and British equities. The question going forward is which region is best positioned to keep on delivering. While I remain a US-focused investor for the most part, non-US developed markets play a key role in my diversification strategy. I like Canada and the UK too, but Europe seems to offer a better investment climate for the time being.

*I own the iShares MSCI United Kingdom ETF ( EWU ).

European Banks Are Well-Capitalized

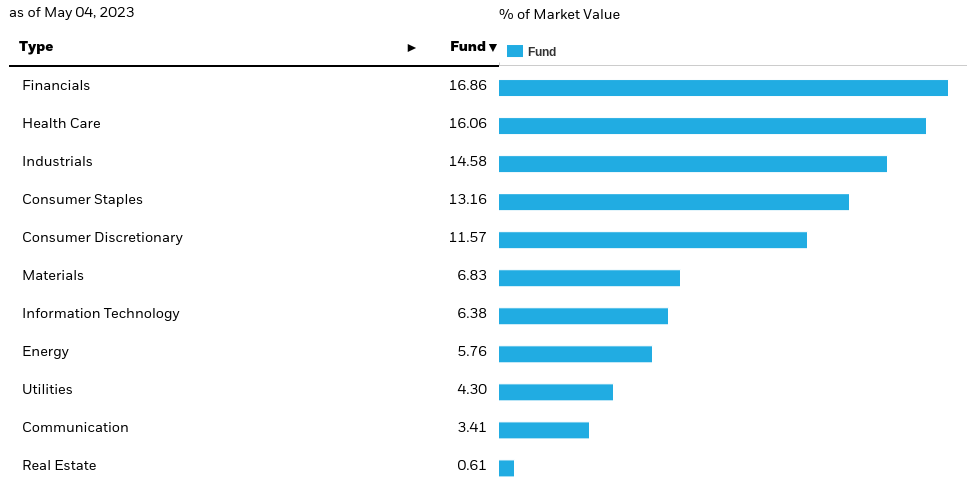

I will now dig into what it means to buy broad-based Euro exposure. For many US investors this means turning to passive ETFs. A popular one that is on my radar is the iShares Europe ETF ( IEV ). While this is a simple way to approach the region, readers may be alarmed to see the largest sector weighting is Financials. With the ongoing banking saga going on in the US, this may seem like an odd place to go long at the moment:

{kind=link}

IEV's Top Sector Weightings (iShares)

This leads to the obvious question of why anyone would want to own this space right now. Why would I suggest buying a fund (or region) with a large allocation to banks/financials given the macro-climate?

The key principle here is that Europe is not the US. While many regional US banks are under pressure, this is a unique problem punishing smaller institutions. It is actually benefiting some of the largest US banks (albeit not immediately) as they bring in new deposits and customers. As households shed their regional or smaller bank exposure, they aren't going to put the money (or accounts) under the mattress. They are going to move to larger, and perceived as safer, banks.

This ties back to funds like IEV in two ways. One, the fund doesn't hold smaller or regional US banks. Two, the banks it does own are some of the largest names in Europe. So even if there is a contagion spread to smaller financial firms in the EU-zone, these are not the names likely to be most impacted.

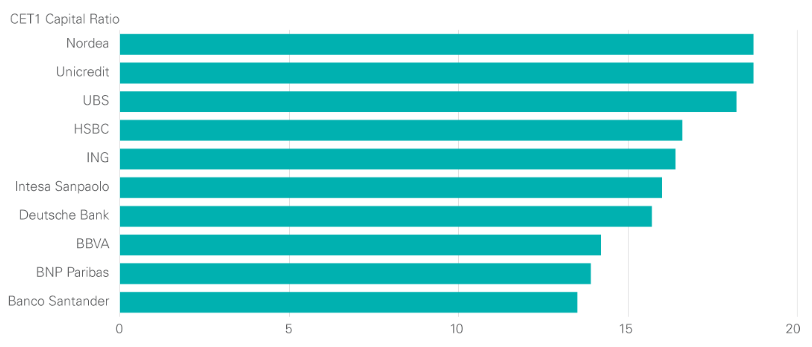

For perspective, the largest European banks are well capitalized (for now), and many of these same companies are the top financial holdings within funds like IEV (and others):

{kind=link}

Tier 1 Capital Ratios (Major European Banks) (FactSet)

My takeaway is that this sector exposure is not necessarily something that needs to be avoided right now. With financial crises can spread quickly - often with little justification - I believe the sector's problems will be contained with federal support and a calming of investor nerves. Case in point is the UBS Group ( UBS ) takeover of Credit Suisse ( CS ) earlier this year. This was a major story that broke less than two months ago - major for both the banking sector and central Europe as a whole. Yet, equities resumed their path higher, and the sector (in Europe) has been relatively calm by comparison with the US. This tells me to stay level-headed when evaluating this exposure and not to automatically rule out European banks because of mismanagement by smaller institutions here at home.

*I may initiate a long position in IEV in the coming week. Another ETF I would recommend for this thesis is the SPDR EURO STOXX 50 ETF ( FEZ ).

Investment Community Not Convinced?

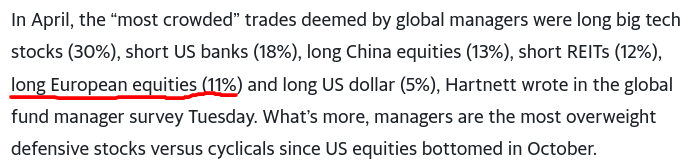

My final bull point has to do with investor sentiment. It is clear Europe has been a winner this year. So this doesn't make it a "real" contrarian play because the gains have resulted in out-performance. But the reason it is at least a partial contrarian idea is that many investors don't believe the rally has legs. What I mean is, many fund managers are of the belief that a handful of successful plays this year are worn out, including being long Euro equities:

{kind=link}

Crowded Trade Ideas (Opinion) (Bank of America Investment Manager Survey)

This does not suggest extreme pessimism by any means so I don't want to oversell the contrarian thesis here. But it does show that professional money managers are cooling on the idea, despite all the bullish momentum. This inherently tells me there is probably still value in the space.

US Facing Major Political Battle

I will now turn to a reason for diversifying away from US equities. This is relevant to European stocks, but really for any non-US developed market play.

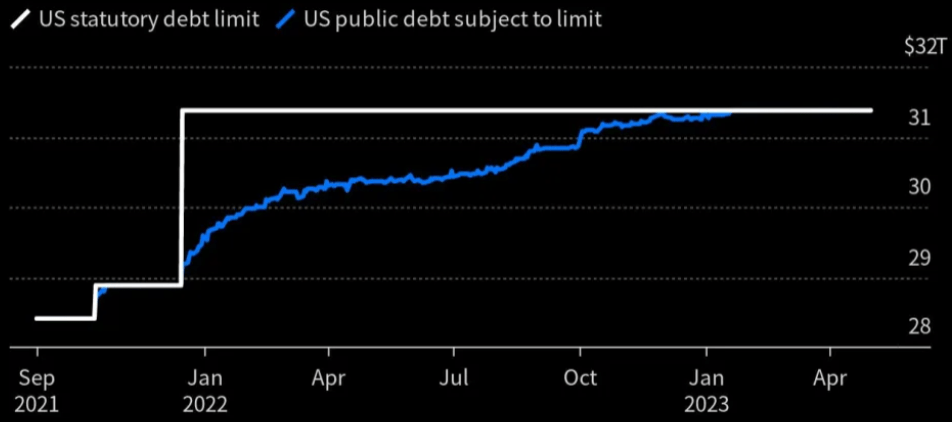

The crux of it is I am increasingly concerned about the upcoming debt ceiling battle in Congress. Investors might remember in 2011 how volatile the market got in reaction to any lack of progress between then-President Obama and House Majority Leader Boehner. The market was taking daily tumbles as a shutdown wore on, and I have been raising cash on the prospect than a similar scenario is going to play out this time around. While this has been making headlines for a while now, it was mostly under the radar. But markets are finally waking up to this as an immediate concern, with the debt limit about to be breached within the next few months, at most:

{kind=link}

US Debt Limit (US Treasury)

Ultimately, the US government will come to an agreement and a major crisis will be avoided as it always has. But not without drama. The current Congressional session and president are not the greatest of pals. I personally feel I have taken enough chips off the table domestically that I am prepared for any volatility. But as a working professional I have monthly income I want to deploy in the market. With the debt ceiling having potential to create a domestic debacle, I am putting fresh cash overseas. This includes Canada, the UK, and now, Europe.

Let's Talk Risks: Russia, Earning Downgrades

Through this review I have laid out the case for being a bull on European equities. But we have to talk the risks to this thesis. One in particular is that these stocks have already seen massive gains over the past year. So, a slowdown or turnaround would make plenty of sense. So, factor that into any forward-thinking analysis.

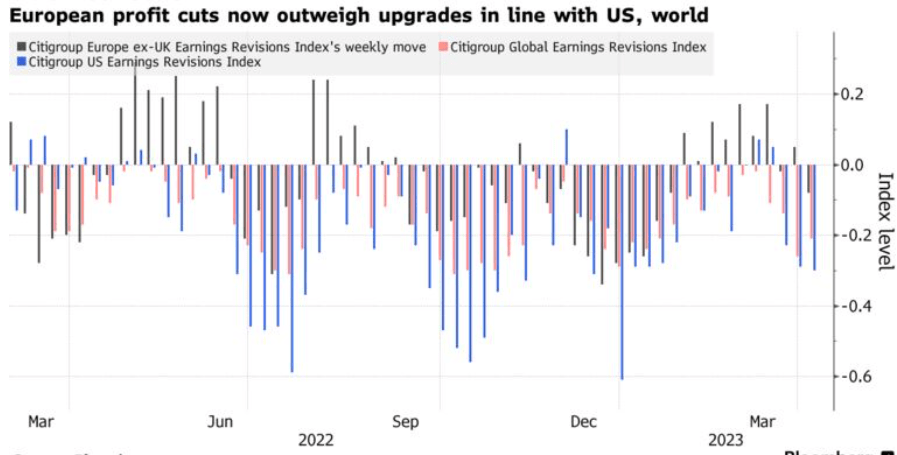

Beyond the obvious "what has gone up could come down" risk, there are others. One in particular is that earnings revisions are starting to trend towards the negative. This puts Europe in-line with the rest of the world on that front, creating an obvious headwind:

{kind=link}

Upgrade vs Downgrades (Profit estimates) (Bloomberg)

This puts some pressure on the idea than European equities are "cheap". While the P/E ratio is attractive, that can change if earnings come in lower. This pushes up the ratio even if share prices stay the same, making the buy-in point more expensive by comparison. This makes the Q2 earnings season an important area to focus on for investors who buy in now if they plan on staying long for a while.

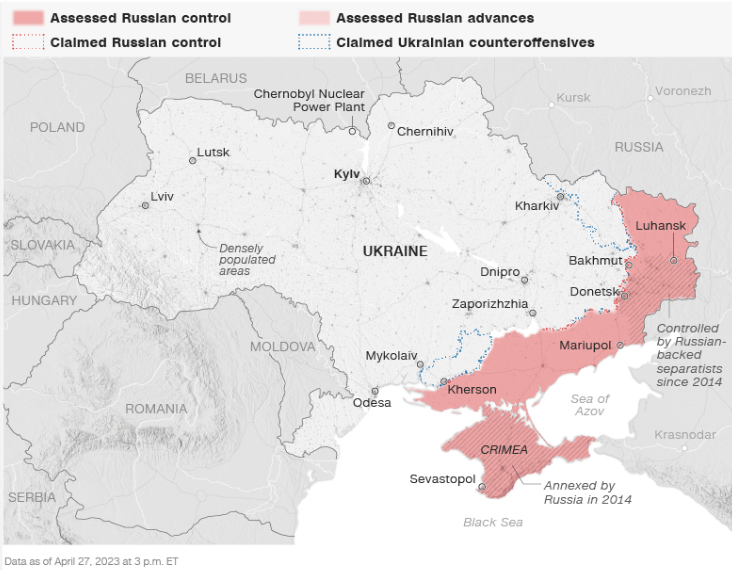

The other major headwind continues to be the military conflict in Ukraine. This is another pain point that investors have learned to live with - which could be a costly mistake. The invasion continues and, in my view, will escalate before it gets better. Personally, I believe Russia will "win" the war in the sense that the conflict will end with Russia annexing Ukrainian territory. Until that happens, fighting will continue. To support this, just look at how widespread the conflict is across the border regions:

{kind=link}

Current State of Russia-Ukraine Conflict (World Bank)

It simply seems unlikely to me that this conflict ends soon or amicably. There is really not supporting evidence to justify this idea.

As Sun Tzu said:

Hostile armies may face each other for years, striving for the victory which is decided in a single day ."

Source: Art of War

This war will not end with Russia withdrawing without some type of gain. They have lost too much to do that now, and Putin is not the sort of individual willing to admit defeat. This concerns the investment thesis because it means more European countries could be drawn into the conflict and/or result in support by Western powers that could sap government resources which would otherwise be used to boost domestic economies. This is a fundamental risk to global equities, but European ones disproportionately.

Bottom-line

I have tended to favor Canadian, Australian, and British/Irish, equities over mainland Europe in years past. In 2023, that outlook has changed a bit. Large-cap Euro stocks have been shining starts and there are multiple reasons this trend could continue in the second half of the year. While I would caution against getting too optimistic here, I do believe more gains are on the way. Therefore, I will be supplementing my foreign exposure with some Euro-focused ETFs in the coming weeks and suggest readers give the idea some thought at this time.

For further details see:

Europe's Out-Performance Could Continue For A Few Key Reasons