PBBIF - European Dividend Gems: Symrise AG

2023-03-16 07:12:22 ET

Summary

- Symrise is one of the top players in the highly concentrated aroma molecules, flavours, and fragrances market.

- Ingredients from this company are used in products we use on a daily basis, resulting in steadily increasing sales and strong margins.

- Investors have been well rewarded since the company IPO’d in 2006 through capital gains and yearly increasing dividends.

- I rate the stock a Hold due to the current overvaluation and antitrust investigations.

The investment thesis

This is the second article in my European Dividend Gems series . Today, I will discuss a very interesting under-the-radar business: Symrise AG ( OTCPK:SYIEF ). This company is currently part of the German DAX index ( DAX:IND ) and one of the top players in the highly concentrated aroma molecules, flavours and fragrances market. Ingredients from Symrise are used in products we use every day and play a crucial role in our decision making process whether to buy a product or not. All top players in the industry boast some significant competitive advantages, such as strong customer relationships, high switching costs, scale, and their ingredients are crucial for clients' end-products.

The strong market position has translated in high-single-digit sales and EBITDA CAGRs since the IPO in 2006. Shareholders have been well rewarded through a growing dividend and capital gains, resulting in market-beating total returns. The stock is currently overvalued for my desired return and the ongoing antitrust investigations should make investors cautious about buying shares at this price.

Business overview

Symrise AG was founded in 2003 through a merger of Haarmann & Reimer and Dragoco (872mln and 373mln EUR sales respectively). The company was listed on the Frankfurt stock exchange three years later, and it has delivered outstanding total returns for shareholders since then. Total sales amounted 4.6bn EUR in the most recent fiscal year and the market cap has grown to ~13.1bn EUR.

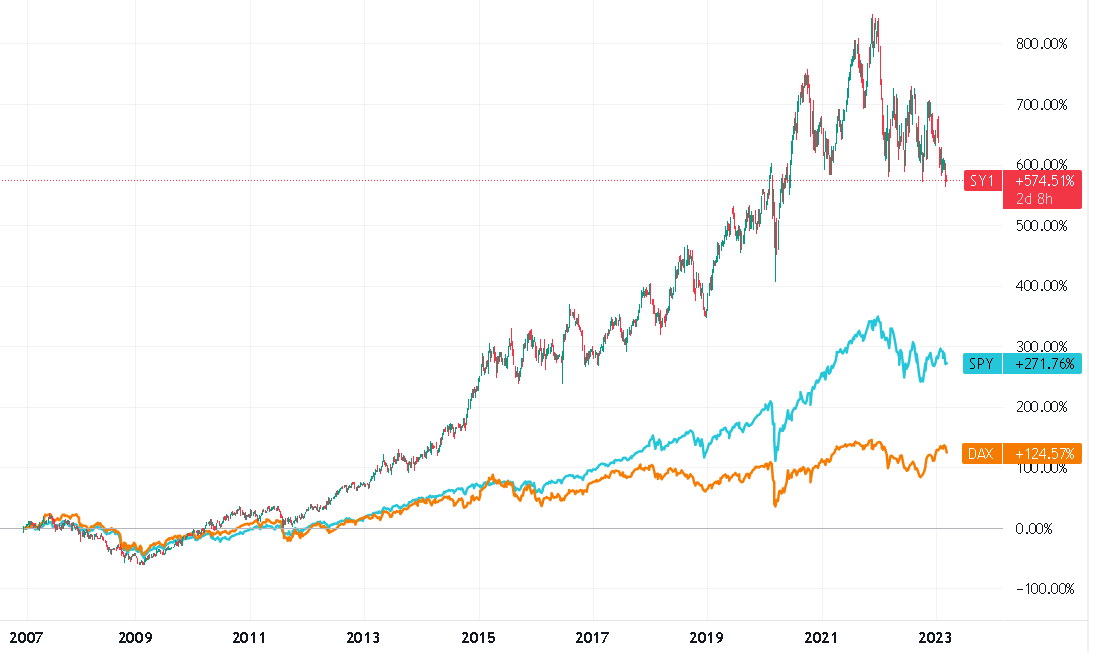

Symrise stock's total annual return was 12.7% since the IPO compared to 8.6% for the S&P 500 index ( SPY ) and 5.2% for the DAX index. Enough reason to take a closer look at this business.

Total returns for Symrise, SPY and the DAX index (Tradingview)

{kind=link}

Symrise is the perfect example of a company with a very simple business model but its products play a key role in people's daily lives. In short, the company is a global supplier of fragrances, flavourings, cosmetic active and functional ingredients. Its client base includes producers of food, beverages, pet food, perfumes, personal care products and cleaning products. Examples of well-known multinationals are Nestlé SA ( OTCPK:NSRGY ) and LVMH ( OTCPK:LVMHF ), but Symrise also serves regional players and discount/private label operators. From the 6,000+ client base, no single client accounts for more than 5% of revenue which reduces the dependency on individual customers.

In total, Symrise manufactures ~35,000 products from roughly ~10,000 types of raw materials, such as vanilla, citrus, or flower and plant materials. The ingredients from Symrise can be found in consumer products you use every day. It is estimated that people interact with Symrise's ingredients 20-30 times in just a single day.

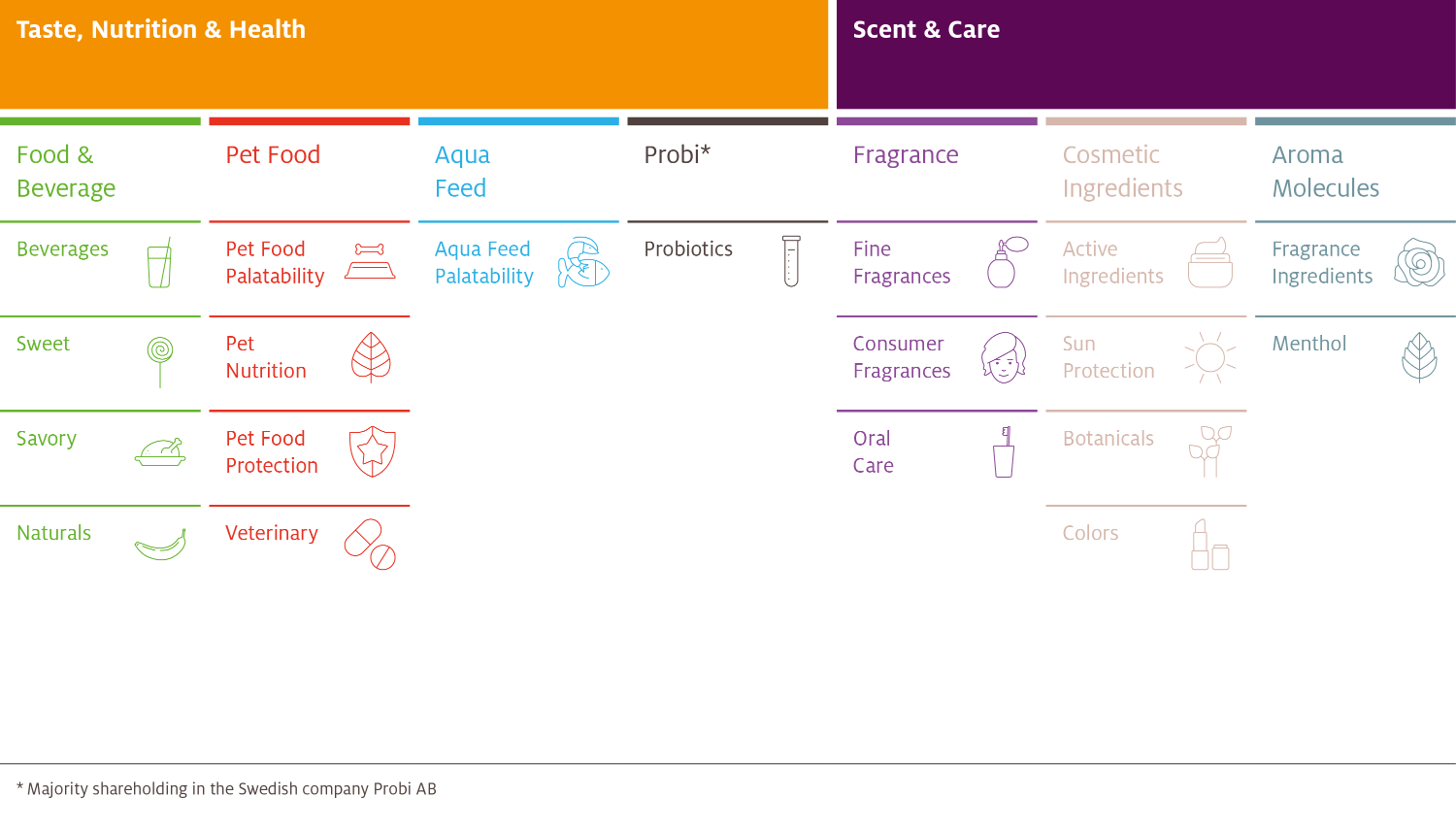

Revenue is reported in two segments: Taste, Nutrition & Heath (2.9bn EUR sales during FY2022) and Scent & Care (1.7bn EUR sales during FY2022). These two segments and all underlying sub-segments are shown in the following figure.

Segment overview (Investor Relations)

{kind=link}

The Taste, Nutrition & Health segment serves the markets of the food and beverages industry as well as producers of pet food and fish food. Within this division there are a number of sub-segments, including Food & Beverage, Pet Food, Aqua Feed, and Probi.

Within the food and beverage industry, Symrise's ingredients are used in a long list of products such as soft drinks, juices, spirits, sweets, chocolate, cereals, ice cream, soups, sauces, and snacks. Besides taste, ingredients could also have other functions such as increasing shelf life, reducing the sugar and salt content, and/or achieving health benefits. Within pet food, Symrise offers solutions to improve the taste and pets' acceptance of pet food, pet food safety and increasing animal health. Next, Aqua Feed includes the ingredients used by fish feed manufacturers for fish and shrimp farms. Finally, the fourth sub-segment relates to the Swedish company Probi AB ( OTC:PBBIF ) in which Symrise holds a majority interest of 60.3% . Probi produces probiotics for food supplements and functional foods. Probiotics are live micro-organisms that, in adequate amounts, offer health benefits to the consumer. For example, a probiotic called Osteo could reduce bone loss and support strong and healthy bones.

The Scent & Care segment consists of three sub-segments: Fragrance, Cosmetic Ingredients, and Aroma Molecules.

Symrise combines aromatic raw materials to make a range of complex fragrances. Fine fragrances are used in perfumery, consumer fragrances are used in personal and household care products, and the oral care sub-segment offers a wide range of ingredients for toothpaste, mouthwashes, and chewing gum. Cosmetic ingredients consist of active ingredients for product preservation, protection against solar radiation, ingredients for hair care, plant extracts, and tailor-made cosmetic colours. Finally, aroma molecules include menthol which is primarily used in oral care products and chewing gum, and aroma chemicals which are intermediate products for perfume oils. These aroma chemicals are used by Symrise for the production of its own perfume oils but also distributed to other companies in the flavour and fragrances industry.

All in all, Symrise has a very broad product portfolio and I really like the focus on defensive consumer end-markets. This brings a lot of consistency and predictability to Symrise's business model.

Market position & competitive advantages

Symrise is one of the world's top four players in the aroma molecules, flavours and fragrances market. It currently holds a market share of roughly 12% based on a total market volume of 39.0bn EUR. Its main peers are Givaudan SA ( OTCPK:GVDBF ), International Flavors & Fragrances Inc. ( IFF ), and Firmenich. The latter is not listed on a stock exchange yet, but it is expected to merge with Koninklijke DSM N.V. ( OTCPK:KDSKF ). The four players have a combined market share of >63%.

Being a leader in a highly concentrated market offers some significant competitive advantages. Multinational producers of food, drinks, fragrances, etc. tend to work with a small pre-defined set of ingredient suppliers. With Symrise being one of those suppliers, the company has exclusive access to product briefings and pitches from clients which creates high barriers to entry for new players in the market.

The aroma molecules, flavours and fragrances market is not a winner-takes-it-all type of market. Many ingredients are tailored to client needs and cannot be easily copied by a competitor. Switching costs are therefore high which makes it unlikely that a current client from Symrise will switch to for example Givaudan for a specific ingredient.

Besides customer relations, the scale of the top players' product portfolio, global footprint and supply chains are very hard to replicate. Scale also offers an advantage in terms of R&D investments and thus innovation capabilities.

Another benefit of this industry is that the percentage cost of Symrise's ingredients in client's end-products is extremely low. Management estimates that this percentage ranges from 1% to 5% . Meanwhile, flavour and scent often play a decisive role in consumer purchasing decisions. The fraction of product costs combined with the crucial role of ingredients in end-products enable Symrise to gradually increase prices and keep margins stable in the long run.

Financial performance

Historical performance

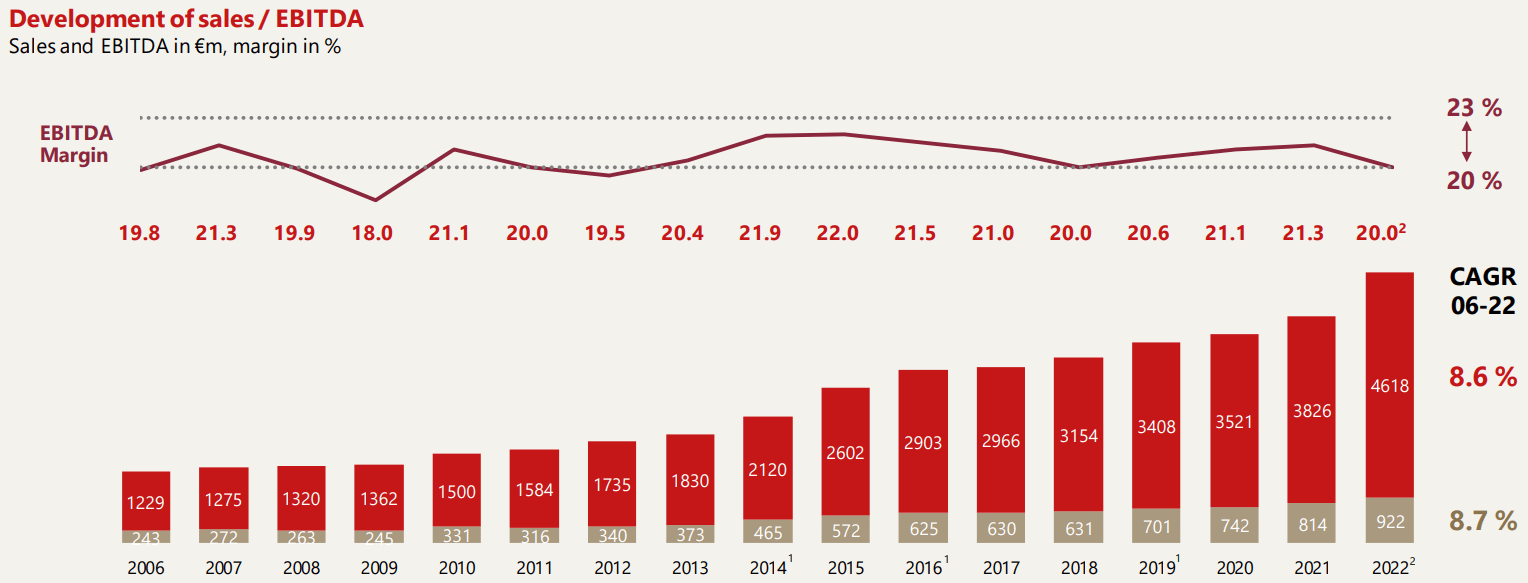

The industry in which Symrise operates is very non-cyclical. Sales growth is therefore mainly tied to population and disposable income trends, rather than cyclical, economic trends. The graph below shows a trend with steadily increasing sales and EBITDA. Between 2006 and 2022, sales grew with an 8.6% CAGR while the EBITDA expanded with at an 8.7% CAGR. The competitive advantages discussed in the previous section enable Symrise to maintain strong margins. This is shown by the EBITDA margin corridor in the graph.

Sales and EBITDA development (Investor Relations)

{kind=link}

Sales growth has been achieved through a combination of organic growth and acquisitions. The following figure shows that Symrise acquires smaller industry players nearly every year. All three businesses acquired in FY2022 had a combined acquisition cost of 449mln EUR and contributed 122 mln EUR to total sales.

M&A history since 2012 (Investor Relations)

I think that Symrise will continue to acquire businesses, further consolidating the aroma molecules, flavours and fragrances market. However, the currently elevated net debt position limits the ability for acquisitions. The long term range for the net debt/EBITDA ratio is 2.0 to 2.5x. At the end of FY2022, the leverage ratio amounted 2.9x including pension provisions. This is not a problem as Symrise has a very reliable cash flow producing business model. But, investors will not see major acquisitions in the near future.

Future outlook

Despite the defensive nature of the flavours and fragrances market, there are plenty of opportunities for new product offerings and innovation. New consumption patterns and trends fuel a growing desire for increasingly diverse solutions. As a market leader, Symrise continuously develops new products in accordance with the clients' needs.

Management defined the mid-term growth objectives a few years ago. They currently expect 5% to 7% organic sales growth through FY2025. The aroma molecules, flavours and fragrances market is expected to grow with a 5.4% CAGR through 2030 , so this outlook is definitely achievable.

M&A is expected to contribute 1% to 3% to total sales growth, translating in a 7% to 8% CAGR through FY2025 . Total sales are estimated to be in the 5.5bn to 6.0bn EUR range in that fiscal year.

The EBITDA margin is expected to lie within the 20% to 23% range which is in-line with historical performance. Maybe Symrise will achieve some margin expansion once raw material cost headwinds subside.

Dividend track record

As suggested by the title, Symrise is a true dividend gem. The most recent dividend increase was announced in the FY2022 results press release as the dividend is expected to grow from 1.02 to 1.05 EUR per share. This is not a huge increase, but I think it is good that management is conservative given the current market environment and the temporary elevated leverage ratio.

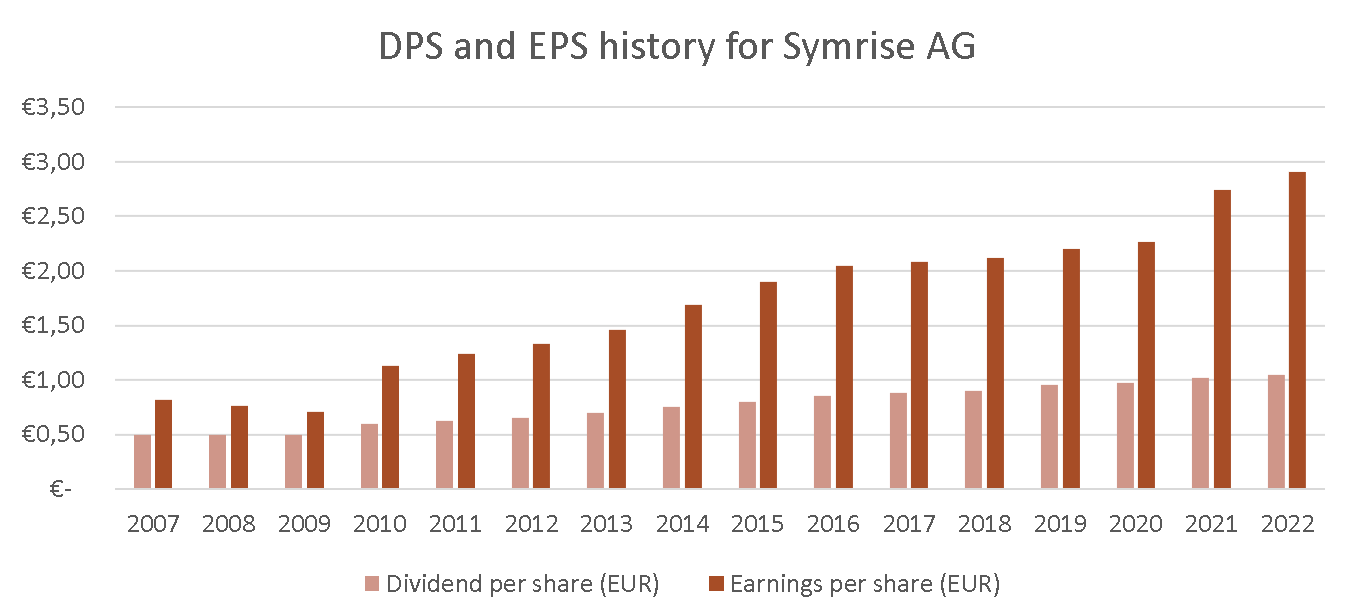

The graph below shows earnings per share, dividend per share, and the pay-out ratio since FY2007. The company officially started its dividend growth history in 2010. Since then, the dividend per share has grown with a 5.9% CAGR. This is significantly less than the 11.5% CAGR for earnings per share, lowering the pay-out ratio from 70.4% in 2009 to 36.1% in 2022. I like this development as it provides ample opportunities for Symrise to keep growing the dividend while at the same time reserving enough capital for future acquisitions.

Dividend and earnings per share since 2007 (Investor Relations; Author)

{kind=link}

Valuation

Now it's time to determine what would be a great price to pay for this business. I always like the discounted cash flow analysis as you can easily calculate the intrinsic value for different scenarios.

The general inputs, FY2022 sales, and FY2022 operating income can be found in the latest annual report .

Sales growth rates have been chosen in such a way that total sales in FY2025 are right within the middle of the guided range (5.5-6.0bn EUR). After FY2025 I assume a slowly declining sales growth rate. I think this is realistic as the overall market is estimated to grow at a 5.4% CAGR in the long term. Symrise will probably outgrow the industry organically and continue to make small acquisitions. Moreover, I assume a slowly increasing EBIT margin.

The income tax expense, D&A, capital expenditures, and change in working capital are excluded from the figure, but I made historically conservative assumptions for all I of them. Next, I calculated the free cash flow for every fiscal year. The resulting projected free cash flows are shown in the green cells. The following figure shows my key assumptions. All numbers are in EUR.

DCF model key inputs (Investor Relations; Author)

The output is a table with the fair value per share for different combinations between the required rate of return and perpetuity growth rate. At the current share price (93.36 EUR), Symrise stock is overpriced for most scenarios. For me it only makes sense to buy individual companies if they have the potential to outperform the index. My personal required rate of return is therefore 10% or higher. Assuming a required rate of return of 10% and perpetuity growth rate of 3%, I would be interested to buy Symrise below 80 EUR per share. This implies that the stock would have ~14% downside from today's share price.

DCF output sensitivity analysis (Author)

Key risks

I believe that considering the bearish arguments are as important or maybe even more important than the bullish arguments when researching a business. There can be multiple factors through which future revenue and margins could be lower than anticipated in my calculation.

(1): Rising raw material prices pressure margins : This risk is applicable to almost all businesses that use some types of raw materials to manufacture their products. While I think that these cost headwinds will eventually subside, it definitely has an impact on the bottom line results. Symrise's EBIT margin declined with 100 bps to 13.6% in the most recent fiscal year. This decrease is relatively small compared to other industries and it really shows Symrise's pricing power, but still we cannot neglect the impact of inflation. Current data suggests that inflation will decrease sharply over the course of this and next year, but there could be some macro events that further increase raw material prices.

(2): Increasing industry regulation : The presentation of Symrise's final financial figures of FY2022 on March 8th took a back seat in light of antitrust investigations by the Swiss competition commission COMCO, joined by the European Commission, the U.S. Department of Justice Antitrust Division and the UK Competition and Markets Authority. Agencies acted on the suspicion that Symrise and its peers coordinated their pricing policy and supplying of certain customers. The ingredients in question are mainly used in cosmetics, personal care products, detergents and cleaning products.

Will this have a significant impact on Symrise's business? Yes and no. First of all, none of the suspicions have proven to be true yet. The deadline for analysing and reviewing information gathered from the companies involved has been set early 2024. If Symrise has indeed violated the law, this could have multiple implications. The first possibility is that regulators impose a fine. Fines in antitrust proceedings usually have an upper limit of ten percent of the annual sales. Over the long-term Symrise could be impacted by regulations that weaken its negotiating power. Currently, we can only speculate and time will tell what the final impact will be.

Final thoughts

Symrise is a very interesting business to consider in the current market environment. Its ingredients play a crucial role in a consumer's purchasing decisions every day. The industry in which Symrise operates is mainly tied to population growth and disposable income, so there are little dependence cyclical trends.

Moreover, the industry in which Symrise operates boasts and number of significant competitive advantages. It is unlikely that a disruptor will enter the market due to strong customer relationships, high switching costs, scale, and the crucial role of Symrise's ingredients in end-products. Recent developments regarding antitrust investigations could impact the pricing power of Symrise and its peers in the future. I think it is too early yet to draw definitive conclusions about the impact, however investors should keep an eye on the progress of the investigations.

I am not going to adjust my fair value for the stock as I think that my assumptions are already conservative enough, but I give the stock a HOLD rating. Given the current overvaluation combined with uncertainty around ongoing antitrust investigations, I will be interested to initiate a position in Symrise in the 75-80 EUR per share range.

For further details see:

European Dividend Gems: Symrise AG