RJN - European Sparks And Darks Tell A Fascinating Story

Summary

- To what extent are fuel prices, capacity constraints and risk premia respectively the drivers of European electricity prices? Spark and dark spreads are the best way to assess these issues.

- The driver of high spot power prices in Germany is not limitations on generating capacity - it is the high fuel prices. High forward prices may reflect generating capacity issues as well as a high risk premium.

- The German dark spread for 2 quarters ahead is over €1000, and the UK dark spread is over €600. In other words, it’s good to own a coal plant!

While writing the post on European electricity prices, I was wondering about the drivers. How much due to fuel prices? How much due to capacity constraints? Risk premia?

Spreads, specifically spark and dark spreads, are the best way to assess these issues. Spark spreads are the difference between the price of electricity and the cost of natural gas necessary to generate it. And no, dark spreads are not the odds that Europe will shiver in the dark this winter - though I’m sure that you can find a bookie that will quote that for you: a dark spread is the difference between the price of power and the cost of coal required to generate it. In essence, spark and dark spreads tell you the gross margin of generators, and the value of generation capacity. High spreads indicate that capacity is highly utilized; low spreads that capacity constraints are not a major issue.

Sparks and darks depend on the efficiency of generators, which can vary. Efficiency is measured by a “heat rate,” which is the number of mmBTU necessary to generate a MWh of electricity. Efficiency can be converted into a percentage by dividing the BTU content of electricity (3,412,000).

Electricity is a highly “spatial” commodity, with variations across geographic locations due to the geographic distribution of generation and load, and the transmission system (and the potential for constraints thereon). Moreover, since electricity cannot be stored economically (although hydro does provide an element of storability), forward prices for delivery of power at different dates can differ dramatically.

Looking at sparks and darks in Europe reveals some very interesting patterns. For example, comparing the UK with Germany reveals that German day ahead “clean” sparks (which also adjust for carbon costs) are negative for relatively low efficiency (~45 percent) units, and modestly positive (~€35) for higher-efficiency (~50 percent) generators. In contrast, UK day ahead sparks are much higher - around €200.

Another example of “identify the bottleneck.” The driver of high spot power prices in Germany is not limitations on generating capacity - it is the high fuel prices. (Presumably, the lower-efficiency units are off-line in Germany now, as their gross margin is negative.) Conversely, generation capacity limits are evidently much more binding in the UK.

But if you look at forward prices, the story is different. Quarter ahead clean sparks in Germany are around €200, while in the UK they are over €300. Two quarter ahead (the depth of winter) are almost €600 in Germany and a mere €300 or so in the UK. (All figures for 50 percent efficiency units).

These suggests that capacity will be an issue in both countries, but especially Germany. Way to go, Germany! Relying on solar in a country with long nights ain’t looking so good, is it?

The wide sparks also undermine attempts to blame it all on Putin. Yes, high gas prices/gas scarcity courtesy of Vova is contributing to high power prices, but that’s not the entire story. Though, to be fair, more gas generating capacity wouldn’t help that much if they become energy-limited resources due to a lack of Russian gas.

The high forward prices may also reflect a high risk premium. My academic work from the 2000s showed that there is an “upward bias” in electricity forward prices. That is, forward prices are above - and often substantially above - expected future spot prices. My interpretation was that this reflects “spikeaphobia”: power prices can spike up, but they are supported by a floor. This means that being caught short is much riskier than being long. This creates an imbalance between long hedging (to protect against price spikes) and short hedging (to protect against price declines that are likely to be far smaller than upward spikes). This creates “hedging pressure” on the long side: if speculative capital to absorb this imbalance is constrained, this hedging pressure drives up forward prices relative to expected spot prices.

The imbalance is likely exacerbated by the fact that there are large fuel price spike risks too. Moreover, the price and liquidity risks that speculators absorbing the imbalances must shoulder is likely raising the cost of speculative capital in electricity trading, meaning that there is both a demand pull and cost push driving the risk premium. Thus, I conjecture that some portion - perhaps a hefty portion - of the large spark spreads for German and the UK is risk premium. (Back in the days I started to estimate the risk premium in the US markets in the late '90s, the risk premium was as much as 50 percent of the forward price. That decline substantially over the next decade to about 10 percent for summer peak as the electricity markets became more “financialized.” Financialization, by the way, is usually a pejorative, which drives me nuts. Financialization typically reduces the cost of hedging.).

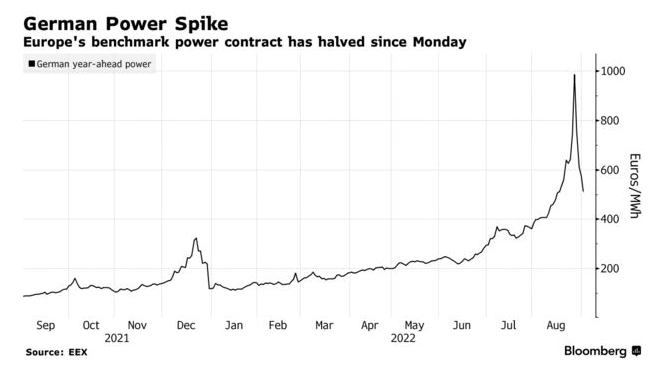

In the aftermath of the mooting of EU proposals to intervene massively in electricity markets, especially through price controls, forward power prices have plummeted: the above figures are from before the collapse. Price controls would impact both the expected spot price and the risk premium - because they take the spikes out of the price. However, as I noted in my prior post, this is not good news: if prices cannot clear the market, rationing will.

{kind=link}

Dark spreads also tell a fascinating story. They are huge . The German dark spread for 2 quarters ahead (Jan-Mar) is over €1000, and the UK dark spread is over €600. In other words, it’s good to own a coal plant! By the way, these are clean darks, so they take into account the cost of carbon. Meaning that the market is sending a signal that the value of coal generation - even taking into account carbon - is very high. This no doubt explains why despite massive green and renewable rhetoric in China, the Chinese are building coal capacity hand over fist. It also points out the insanity of European policies to eliminate coal generation. Even if you believe in the dangers of carbon, the way to deal with that is to price it, rather than to dictate generation technology.

To give some perspective, the above figures imply that a 500MW coal plant in Germany was anticipated to produce €870 million in value in Q3 '23 (24 hours/day x .80 operating rate x 91 days/quarter x 500 MW x €1000/MW). That’s more than the cost of a plant. Even if you cut that in half to take into account today’s power price collapse, it’s a huge number.

Think about that for a minute.

In sum, spreads tell fascinating stories about what is happening in the European electricity market, and in particular, the roles of input prices and capacity constraints and risk premia in driving the historically high prices. But perhaps the most fascinating story they tell is the high price that Europe is paying to kill coal.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

European Sparks And Darks Tell A Fascinating Story