EWCZ - European Wax Center: Price Unlikely To Reach 2022 Highs This Year

Summary

- EWCZ is a fundamentally sound business and a leader in the industry, with strong FCF and competitive advantages.

- However, the shares plunged 53% in 2022, significantly lower than broad market.

- We discuss several risk factors that might have made investors sell the stock.

- In the near term, the valuation (P/E, EV/EBITDA), leverage, and two more macro concerns might limit the upside to share price.

Despite European Wax Center's (EWCZ) strong brand and the successful business performance of the franchise, we believe the stock is expensive and the premium priced into its EV/EBITDA multiple relative to its peer group isn't justified.

Sound Business

European Wax Center is a leading personal care franchise brand, which offers an out-of-home (OOH) waxing experience by highly trained estheticians within the privacy of clean, individual waxing suites. The company has good brand recognition due to effective marketing, and shows strong growth in the number of locations, as well as same store sales growth. As of Dec. 31, 2022, its network included 944 centers nationwide . EWC is an industry disrupter in the OOH hair removal category, focusing on quality waxing experiences, offering proprietary skincare product lineup and effective, timely, clean and less painful services, compared to other OOH waxing solutions. The business is resilient to macro fluctuations, as the client base is generally more affluent, less affected by inflation, and views the service as more of a staple than discretionary expense.

Financial Health: Asset-Light, Predictable Revenue Stream, High Margins, High FCF

EWCZ is well positioned in the market - the nature of its business warrants high customer loyalty and predictable revenue stream, as most clients become accustomed to the hair removal procedure and view it as part of their self-care routine rather than a discretionary spend. Another advantage is the asset-light business model, since it's a franchise, and individual franchisees maintain the waxing centers and cover personnel overhead costs, and what inventories there are (proprietary product lineup, mainly wax) are inexpensive and not logistically complicated to maintain a supply of. On top of that, according to company filings, there is a large, underpenetrated total addressable market worth $18Bn, of which EWCZ currently has 4%, and much of the rest is represented by fragmented, unaffiliated service providers. EWCZ is determined to capitalize on this opportunity.

Financially, the company enjoys considerably higher margins than the consumer discretionary sector average. According to Gurufocus, a typical operating margin would be 5.96% as of end-of-year 2022 , but according to company filings, for EWCZ's 2021 operating margin was 12-17%. (2021 operating income 24.7M / sales 178.6M). Consequently, free cash flow is also strong compared to peers, at $41M in 2021 . Superior profitability is a significant factor in determining share price and one of the reasons asset managers model its stock's price objective based on 22x EV/EBITDA multiple vs 14x EV/EBITDA average for a group of similar franchisors.

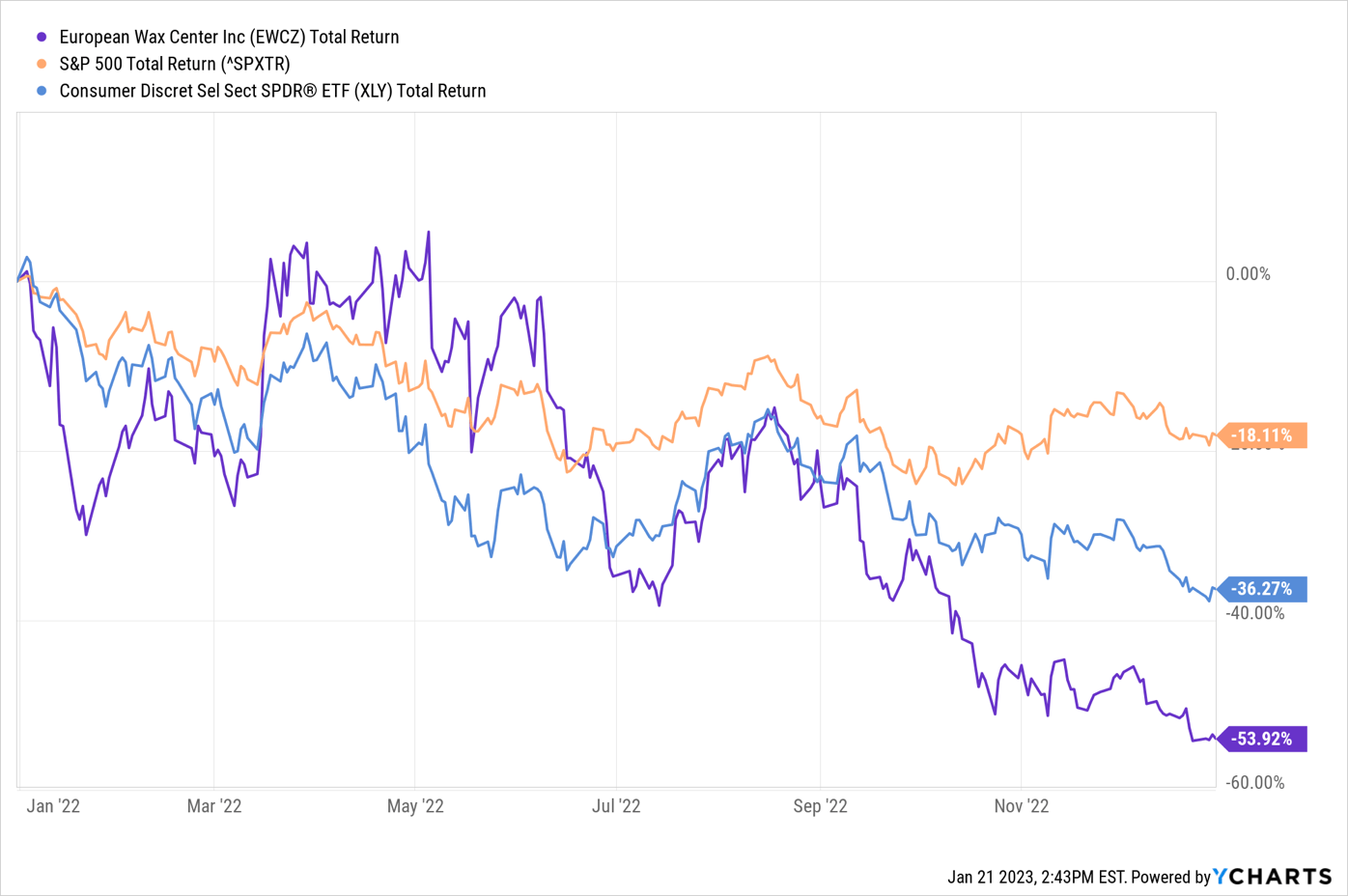

Shares Plunged in 2022

Considering business advantages and strong fundamentals of EWCZ, it was unexpected to see its shares plunge 53.92% in 2022, significantly more than S&P broad market and consumer discretionary sector.

{kind=link}

EWCZ's price trajectory in 2022 loosely correlated with the general market, which rose in March and July and dropped in June and August-September, although EWCZ displayed more volatility and wider swings. However, the shares never really recovered after August-September, unlike the market, which rose back. Were there company-specific risks that caused investors to stay away from the stock? Are these risks still relevant in 2023? Let's discuss several concerns next.

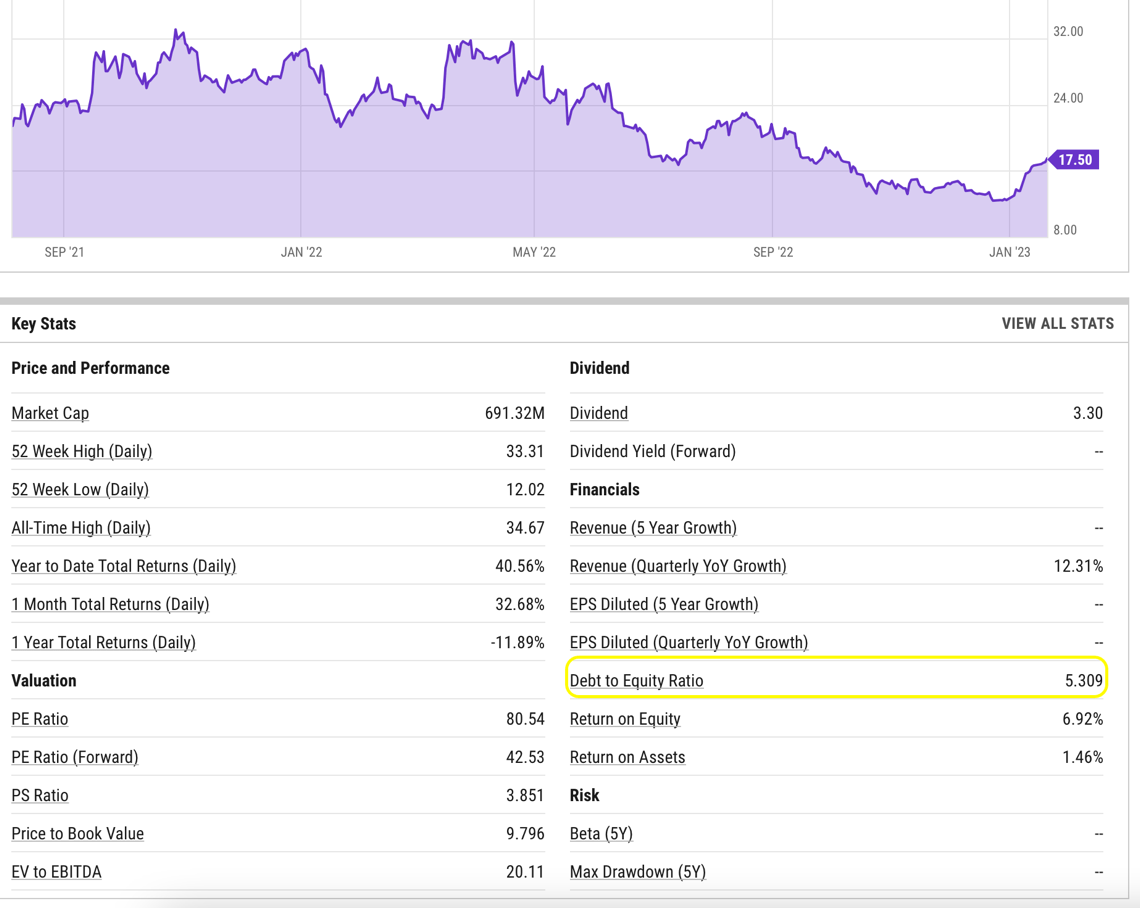

Leverage

Around April, total liabilities doubled from roughly $272Mm to $475Mm when the company issued a new $400Mm round of debt at 5.5%, thus increasing leverage ratios. Currently, the debt-to-equity ratio is 5.3, while generally, a good debt ratio is around 1 to 1.5. This is bound to put downward pressure on the stock price.

{kind=link}

In and of itself, higher leverage is not a problem, when growth prospects are good. And they would generally be good, given that the pandemic wiped out around 10% of independent waxing businesses, plenty (400+) of new locations are available and earmarked for franchising, and the business created a lot of loyal repeat customers. However, during earnings call in November 2022, management disclosed that only about 20% of clients are sticking to the expected frequency of appointments, while a large portion of the other 80% of clients are slowing down the pace. This is understandable at the time of high inflation, when a lot of people cut extra spending. So, in context, such high leverage ratio should be a big red flag.

Another concerning factor is current valuation.

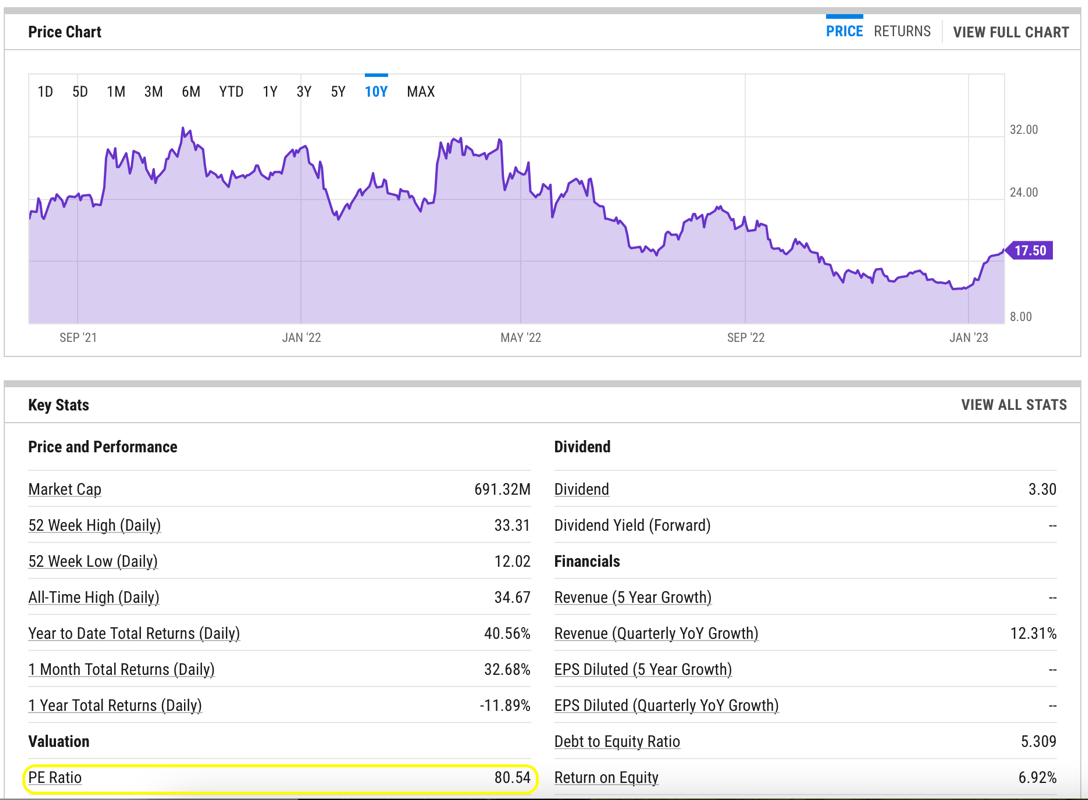

P/E and EV/EBITDA Ratios Much Higher Than Peers

The current P/E ratio is a whopping 80x. The stock is significantly overvalued vs. its peers (the S&P average P/E ratio is 17-19x), given current growth rates. Either the price needs to come down, or EPS growth rate needs to pick up.

{kind=link}

The same argument goes for EV/EBITDA premium. Sector average is 14x, while EWCZ's share price is currently implying 20x EV/EBITDA. If growth concerns were to materialize not only would the stock fail to appreciate to the target of $20-23, to justify a multiple of 20x, but it could lose value all the way down to around $11, to reflect 14x EV/EBITDA peer group multiple.

On top of that, there are at least two major macroeconomic factors relevant this year.

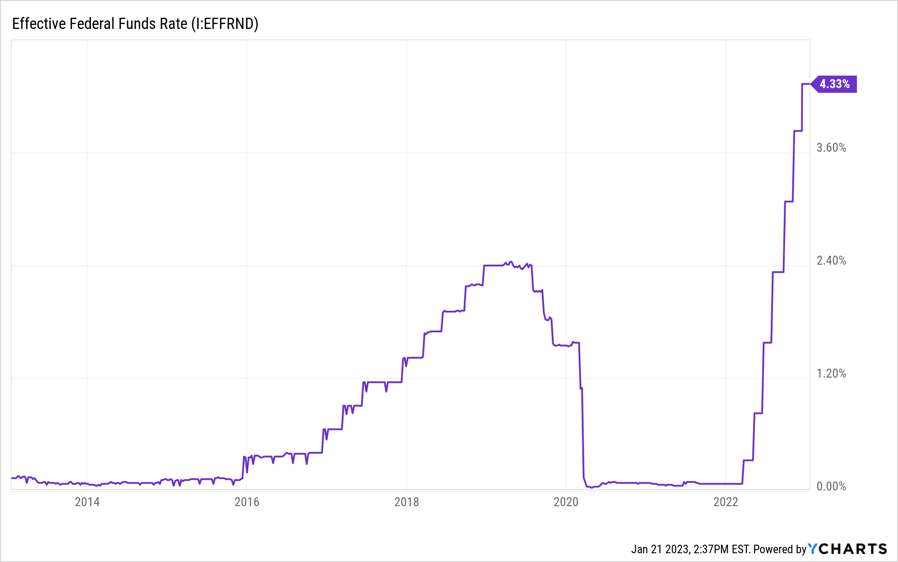

Rising Interest Rates

At the time of writing this article, the Fed funds rate is at 4.3% compared to 0.8% a year ago. Should borrowing costs become high enough to prevent franchisees from opening new locations, it would negatively affect franchise growth.

{kind=link}

As a side note, the company itself has entered into an interest rate cap agreement, effective from 2018 till 2024. (An interest rate cap agreement, explained in simple terms, is a sort of an insurance agreement, where a company pays fixed amounts periodically in exchange for the counterpart paying variable rates on their behalf.) Thus, the interest rate risk is not a significant concern to the core business at this point. As per the company's 2021 10-K :

In December 2018, we entered an interest rate cap derivative instrument which was designated as a cash flow hedge at inception. Our objective is to mitigate the impact of interest expense fluctuations on our profitability resulting from interest rate changes by capping the LIBOR component of the interest rate at 4.5% on $175.0 million of our long-term debt, as the interest rate cap provides for payments from the counterparty when LIBOR rises above 4.5%. The interest rate cap has a $175.0 million notional amount and is effective December 31, 2018, for the monthly periods from and including January 31, 2019 through September 25, 2024. The interest rate cap has a deferred premium; accordingly, the Company will pay a monthly premium for the interest rate cap over the term of the agreement. The annual premium is equal to 0.11486% on the notional amount.

Low Barriers to Entry

One of the constant risks in the waxing industry is low barriers to entry. Should there be a business willing to challenge EWCZ's market position, it is relatively straightforward and inexpensive to start a rival waxing brand, or an alternative to waxing, such as sugaring. Although EWCZ is the leader in the sector currently, and the brand recognition is strong, with an appropriate amount of financing its position could be challenged.

EWCZ has a number of competitors, both public - like OneSpaWorld Holdings ( OSW ) - and private - such as Waxing the City (A Self Esteem Brands company) and SugaringNYC. There are companies in the adjacent sectors, like hair salons (Great Clips), fitness-wellness (LA Fitness, The Beachbody Company ( BODY )) and many others that could become competitors in the future. This area of consumer discretionary spending is known to be profitable and ever growing, thus attracting investors.

Low barriers to entry and a competitive market create uncertainty when projecting future performance for EWCZ, and any uncertainty can put downward pressure on the stock price.

Conclusion

Having considered the reasons why the price collapsed in 2022, you might wonder what changed in 2023. Year to date, EWCZ's shares are up 40%. Our short answer is that not much has changed and such quick and significant appreciation is unwarranted. Perhaps neither was the 53% drop, and fair value is somewhere in between - but nowhere near the 2022 highs of $30. Until there is more clarity on growth prospects, when we can see steady repeat business from more than the 20% of highest paying clients, we will rate the stock a hold.

For further details see:

European Wax Center: Price Unlikely To Reach 2022 Highs This Year