ESEA - Euroseas' End Markets Fell But The Company Is Still On The Hook

Summary

- Euroseas' end markets for container vessels have already fallen to prices close to pre-pandemic levels.

- At these prices the company would still be profitable, adding to very lucrative contracts for 2023 and 2024.

- However, prices are probably heading lower given the expected increase in supply for 2023 and 2024.

- ESEA still has to invest hundreds of millions in new ships, adding to debt and depreciation expenses.

- Those ships will lose value as soon as they are on the water and will not necessarily earn a good return, given current prices.

Euroseas ( ESEA ) is a Greek managed, Marshallese flag owner of containerships (intermediate and feeder size). The company saw its price soar and collapse in line with containership charter rates between 2020 and 2022.

In August I wrote a bearish recommendation on ESEA , on the basis that its industry was cyclical and overinvested, and that the company's management was not good at capital allocation. Since then the stock has fallen almost 28%.

In this review with 3Q22 data , I find that the containership market has already collapsed, and that ESEA has not changed course. The developments ahead are still terrible, with a lot of supply coming to market, increasing ESEA's depreciation expenses. ESEA is still very overvalued.

Note: Unless otherwise stated, all information has been obtained from ESEA's filings with the SEC .

Business description

Cyclical, commoditized industry : The containership industry has all the characteristics that lead to profit destruction: enormous fixed assets, high exit barriers, and a commoditized product. This has led to a classical industrial cycle of undersupply, prices rising very fast, during which a lot of new supply begins construction (with lead times of almost three years), after which prices collapse again and the market is bloated in supply. That supply is slowly decommissioned and the cycle begins again.

Management is not good at capital allocation : The only way to win in this type of industry is to play the cycle in reverse from a capital allocation perspective. Management has to accumulate cash without investing in the upper portion of the cycle and then buy capacity from strained competitors in the downward portion.

Unfortunately ESEA's management has not done that. As if they did not understand their own industry, or maybe thinking 'this time is different', the company invested heavily in the previous cycle (2003-2007), only to sell those ships at enormous impairment losses during the downward cycle (2008-2020). This time, they rushed to order new ships (9 in total, for $350 million) and buy second-hand ships at close to record prices. I can tell almost with certainty that enormous impairment losses wait ahead.

Not very clear family relationships : ESEA is controlled by its founder family. This generally is a good sign. However, ESEA has too many commercial relations with other companies from the founder family. It has purchased and sold ships to the family (at market prices but at terrible timing always). Most importantly, pays a hefty managerial canon to a company from the family. This service could easily be insourced, allowing for better cost control.

Latest developments

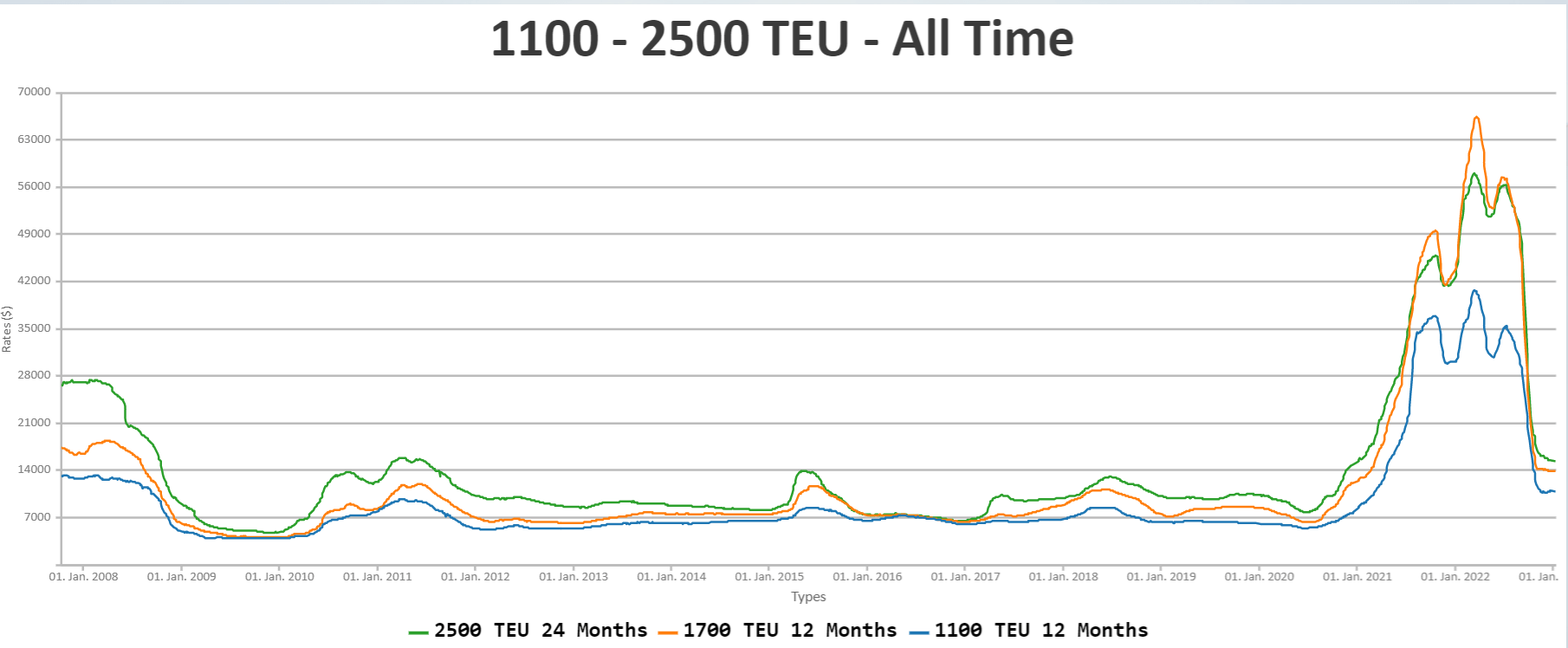

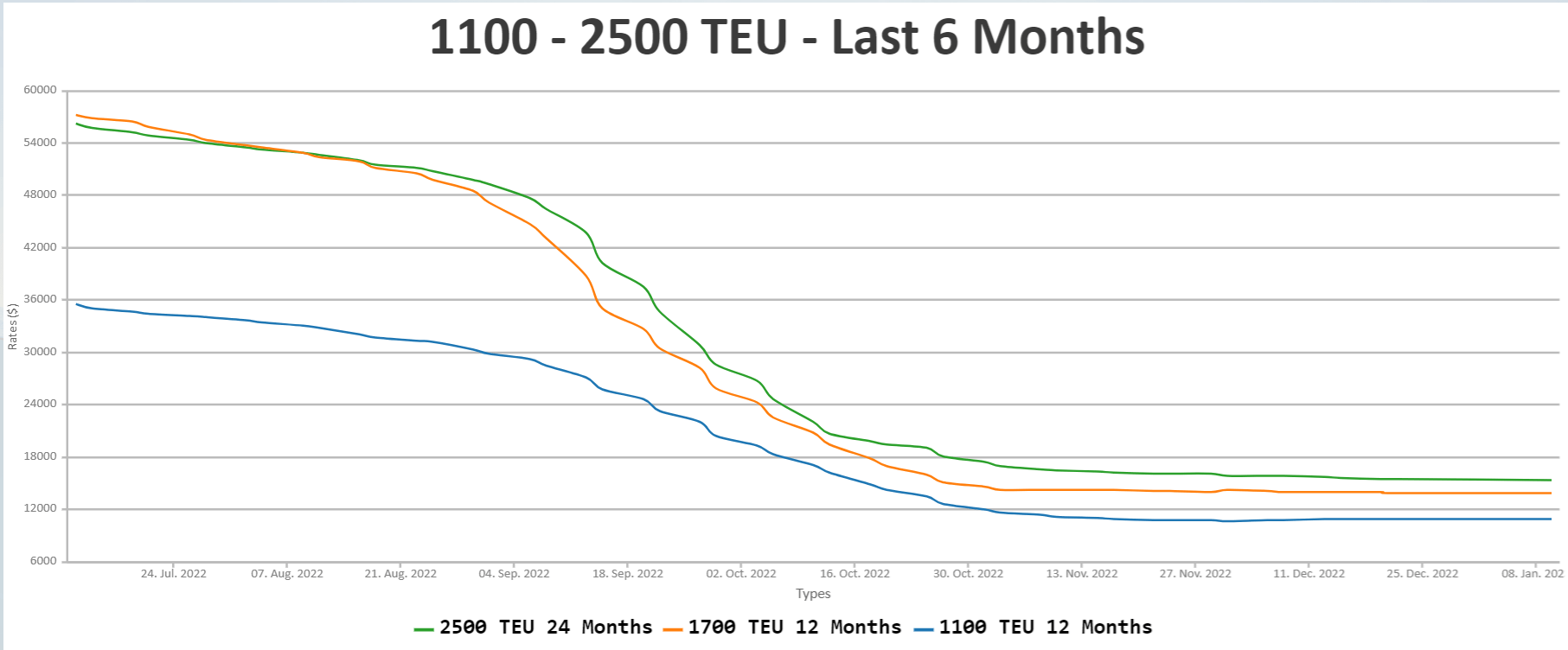

The price has already collapsed : The New Contex Container Index has already returned to close to pre-COVID, unprofitable prices. The prices seem to have at least temporarily stabilized around $15 thousand for the feeder category, and around $19 thousand for the intermediate category. I do not plan to forecast future prices, but it is possible that these do not fall below $10 thousand per day (as before COVID) given the inflation that the world has experienced.

{kind=link}

{kind=link}

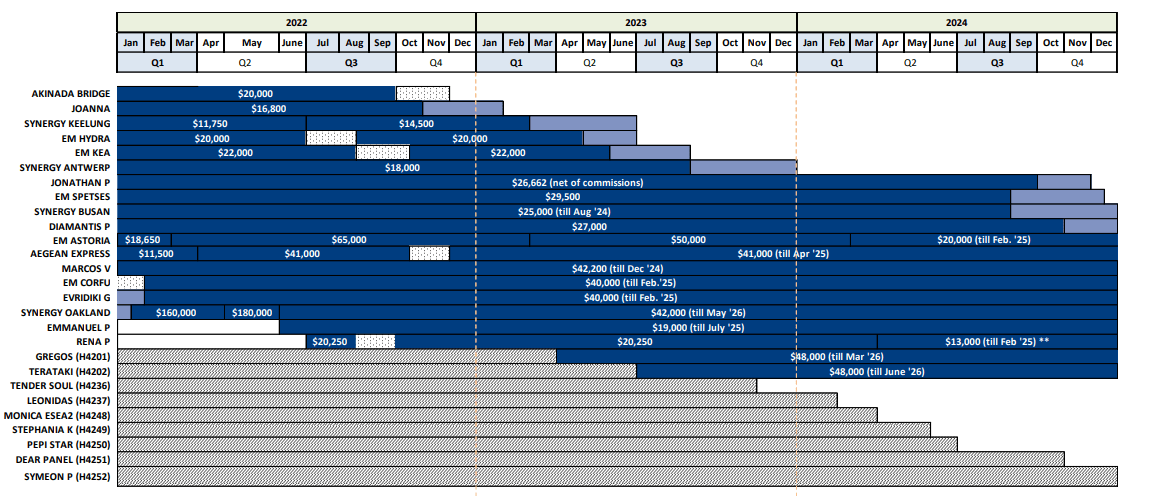

ESEA has two years of profitable contracts, and then market prices : A significant portion of ESEA's currently operating fleet is already chartered at record high prices, averaging $30 thousand per day per ship. The contracts mature in stages in 2023 and 2024.

ESEA's fleet chartered contracts (ESEA's investors presentation November 2022)

{kind=link}

These chartered contracts provide for profitability of the currently operating line until 2024. The new ships will probably be chartered at prices closer to current prices (given that the cycle has already reverted), except for two of them chartered at very good $48 thousand rates until 2026. After 2024, most ships will be chartered at prices close to current prices.

An explosion in depreciation and interest costs ahead : As ESEA starts receiving its 9 new boats in 2023 and 2024, it will start depreciating them. With average depreciation lives of 25 years, and costing $350 million, I anticipate $14 million in additional yearly depreciation expenses by 2025.

Because ESEA does not generate the cash necessary to pay for those ships, it will have to increase its debt levels. ESEA still has to pay $287 million, and has generated about $100 million in CFO TTM. Assuming the same level of CFO in 2023 and 70% of that in 2024, the company has to increase debts by $100 million to pay it for the new ships, reaching net debts minus cash of $190 million by the end of 2024.

ESEA's borrowing rate ( informed in the latest 20-F for FY21 , could have changed now) was LIBOR + 3.5%. The company's interest over average debt in 3Q22 shows an effective interest of 5% (lower than expected with LIBOR already above 4% by that period because of hedges for $60 million).

Considering a very easy rate of 5% for the long term, the company is expected to pay $10 million in interest by 2024.

Profitability calculations

As I showed in the August report, ESEA had a fairly consistent average operating cost of $10 thousand per day, including dry docking expenses.

By the end of 2024 the company will have vessels for $600 million gross cost depreciating at a cumulative rate of $25 million per year. That comes to about $1 million per ship or another $2.8 thousand per day. This is not the same as the market loss of value of the ship. According to info provided in the investors presentation from November , a 2,500 TEU ship losses $20 million of value in the first ten years of operation, from an original price of $40 million, implying that they lose value faster at the beginning of their operations.

Finally the $10 million in interest charges add another $1 thousand per day per ship. This all means ESEA needs an average charter rate after 2024 of $14 thousand per day just to break even. Given that depreciation is a non accrual, the company can dedicate $25 million to debt repayment per year in that case. In order to repay its debt principals it has to make even more.

Finally, with a current market cap of $140 million, rates should climb by another $1.5 thousand per day on average for the company to generate $14 million in after-tax profits. This implies a profitable charter rate of at least $15.5 thousand per day on average.

Prices are already quite close to those levels, and supply has not completely hit the market yet. According to ESEA, in 2022 the feeder fleet increased by 6%, and is expected to grow by another 8.5% in 2023 and 5% in 2024. For intermediate ships the rates climb to 10% in 2023 and 10% in 2024.

Conclusions

ESEA operates in an undesirable industry and has a less than stellar management team. It has consistently operated at a loss, destroying hundreds of millions in shareholder value. In this new cycle, the company repeated the bad decisions that led to under profitability and value destruction in the 2010s decade.

With that in mind, asking for a 10% return on ESEA's current market cap is being extremely generous. One could ask that same return on much higher quality companies in the current market.

However, even that return will be difficult to achieve in the long term given ESEA's mounting expenses, and the fragile condition of the containership market. Therefore, an investment today in ESEA does not even guarantee a very low required return for a very bad quality company. In my opinion, ESEA is clearly a no-go.

For further details see:

Euroseas' End Markets Fell But The Company Is Still On The Hook