GSL - Euroseas Ltd.: A Growing Underdog In The Challenging Marine Shipping Industry

2023-11-27 04:26:06 ET

Summary

- Euroseas Ltd. is a strong buy due to its potential for growth and profitability in the marine transportation industry.

- ESEA has the capacity to increase its market share in a growing industry, particularly in the Asia Pacific region.

- The company has low volatility and offers a high dividend yield, making it attractive for investors seeking income and capital appreciation.

Investment Thesis

Euroseas Ltd. ( ESEA ) warrants a Buy rating due to its strong potential for growth and profitability. Additionally, I believe ESEA represents a solid value based on its current fundamentals. While the marine transportation industry is expected to see only modest growth, ESEA demonstrates the capacity for increasing market share looking forward. Finally, ESEA has comparatively low volatility with a high dividend yield for investors seeking income in addition to capital appreciation.

Company Overview and Primary Competitors

ESEA is a Greek marine shipping company that provides seaborne transportation for containerized cargoes, including refrigerated cargos. The company has existed in one form or another for over 100 years and held an IPO in 2004. Primary competitors to ESEA according to its own annual report are Danaos Corporation ( DAC ), Costamare Inc. ( CMRE ), and Global Ship Lease ( GSL ). Euroseas operated an average of 19 vessels last quarter and is the smallest of these competitors by market capitalization.

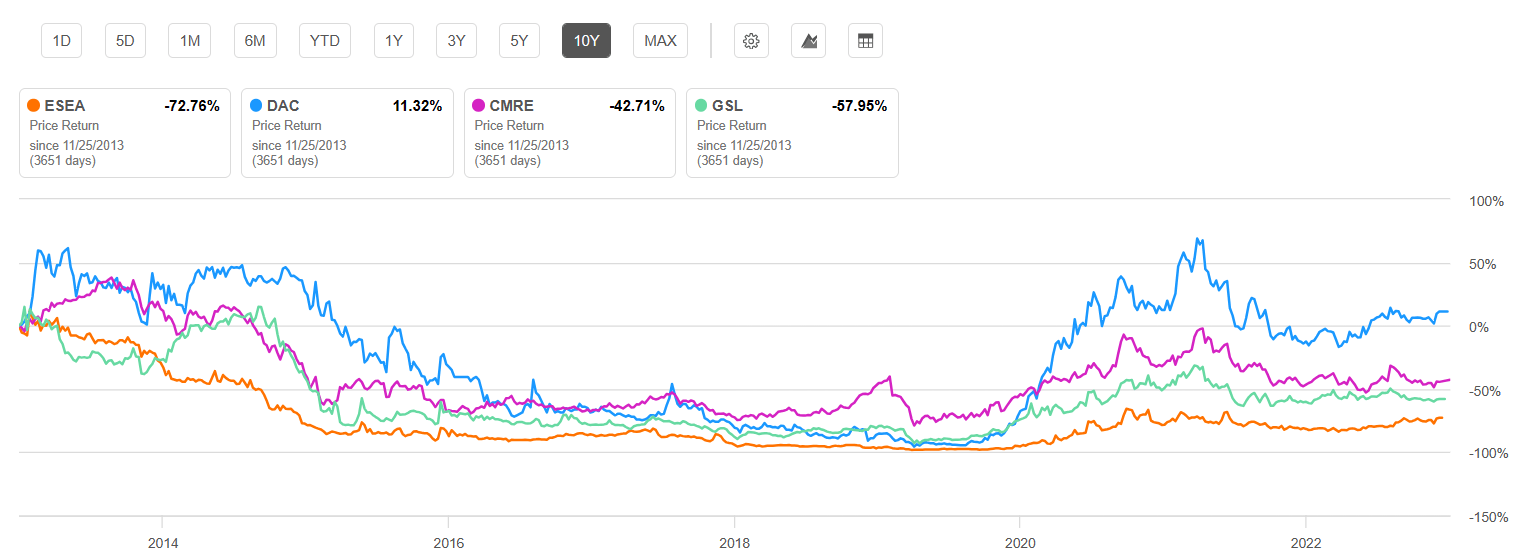

ESEA has historically lagged behind these primary competitors in share price. Looking back at its 10-year performance history, it had the worst performance due to low profitability and growth. That is, until recently. As I will cover with multiple fundamental metrics later, the company is shaping into an underdog, primed for growth beyond its competition and presenting a buying opportunity.

{kind=link}

10-Year Price Return: ESEA and Major Competitors (Seeking Alpha)

Growing Marine Transportation Industry

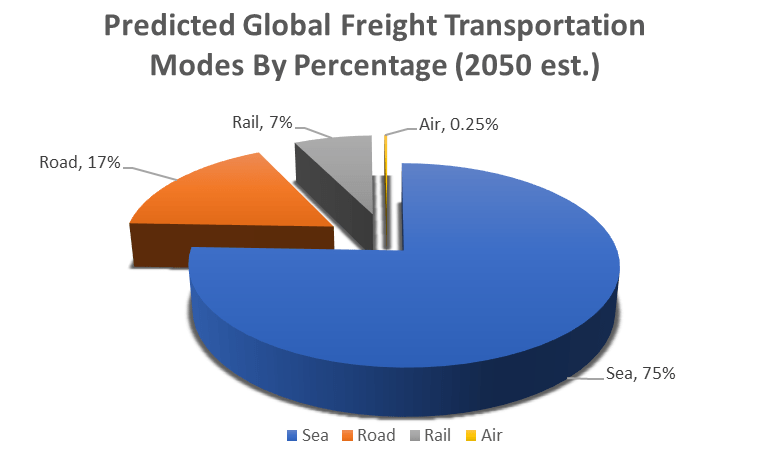

The marine containerized and dry bulk trade is expected to see between a 3.9% and 4.5% CAGR through 2026. The greatest growth is expected in the Asia Pacific region where major supplies are transported via ocean. In 2015, 70% of freight transported worldwide was by sea. This was the largest transportation mode, compared to road (18%), railway (9%), inland waterway (2%), and air (0.25%). This dominance in global transportation will only increase and is expected to be 75% by 2050 . In other words, maritime trade by volume is expected to double by 2050.

{kind=link}

Estimated Global Freight Transportation in 2050 (Created by Author with Data from Maritime-Executive.com)

In particular, the freight flow in the Pacific and Indian Oceans will see the greatest growth, about four-fold, between now and 2050. Atlantic Ocean maritime freight traffic will continue to remain busy with trade between the Americas, Europe, and Africa.

ESEA’s Potential for Increasing Market Share

Although global maritime transportation is expected to see modest but steady growth, ESEA is postured for growth beyond its competitors and therefore steal market share. First, ESEA’s gross profit has grown for the past four consecutive quarters. Additionally, Euroseas has seen the highest net income margin and highest net income (3-year CAGR) compared to peers.

In terms of profitability, ESEA has also seen the highest return on equity and return on assets. Looking forward, ESEA has the highest revenue growth ((FWD)), 27.6%, as well as operating cash flow growth ((FWD)), 25.15%, compared to three major competitors.

Growth, Net Income, and Cash Flow Metrics: ESEA and Competitors

| ESEA |

| DAC |

| CMRE |

| GSL |

| Revenue Growth ((FWD)) |

| 27.6% |

| 12.57% |

| 19.72% |

| 13.90% |

| Net Income Margin ((TTM)) |

| 60.14% |

| 59.29% |

| 37.12% |

| 48.37% |

| Operating Cash Flow Growth ((FWD)) |

| 25.15% |

| 18.64% |

| 1.46% |

| 17.71% |

| Net Income (3-year) ((CAGR)) |

| 244.23% |

| 58.96% |

| 199.63% |

| 101.30% |

Source: Seeking Alpha, 25 Nov 23

As evidence of its growth momentum, Euroseas is also expanding its fleet. In addition to its 19 carriers on the water, ESEA has 7 more vessels under construction to be delivered in 2024, according to its latest quarterly report . ESEA’s 3-year total assets CAGR is also higher than 3 major competitors. Despite this growth, the company has not appeared to dip into significant debt. ESEA’s long-term debt to total capital is 28.3%, lower than the average of the three larger competitors analyzed. Given these very strong fundamental metrics, ESEA is postured to increase its market share, representing the first indication of a buying opportunity.

Dividend Yield and Volatility

The second key factor driving ESEA as a buying opportunity is its significant dividend yield. ESEA’s forward dividend yield is currently at just over 7%, higher than both DAC and CMRE. Importantly, ESEA’s dividend appears sustainable with a payout ratio of 12.7%, lower than all three competitors examined. However, the company admits in its filing that its dividend is highly subject to reduction or elimination. The risks for maritime shipping, discussed later, all contribute to dividend safety, as a downside to the high yield.

Dividend and Volatility Metrics for ESEA and Competitors

| ESEA |

| DAC |

| CMRE |

| GSL |

| Dividend Yield ((FWD)) |

| 7.01% |

| 4.61% |

| 4.74% |

| 8.32% |

| Payout Ratio |

| 12.67% |

| 10.69% |

| 22.89% |

| 17.28% |

| Beta Value (5-Year) |

| 0.97 |

| 1.55 |

| 1.44 |

| 1.70 |

Source: Seeking Alpha, 25 Nov 2023

In addition to an attractive dividend yield for income investors, ESEA has one of the lowest beta values. With a 5-year beta of 0.97, it indicates a volatility roughly the same as the market overall. Therefore, pending any elimination of dividend yield, ESEA represents a buying opportunity for those seeking income in addition to capital appreciation.

Outlook and Valuation

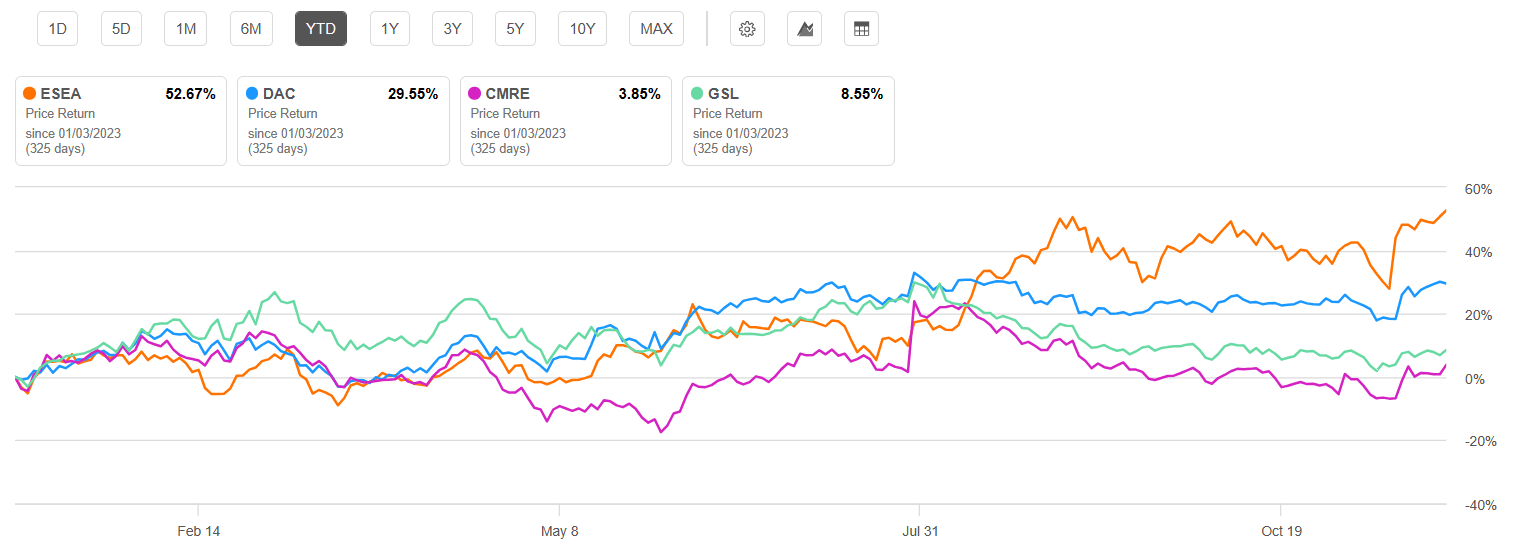

Perhaps the greatest factor driving a buy rating for ESEA is multiple indicators that it is undervalued. Even after a 52% YTD rise in share price and roughly at its all-time high, ESEA is a value buy for me with strong momentum moving forward.

{kind=link}

YTD Price Return for ESEA and Competitors (Seeking Alpha)

This is because ESEA has multiple favorable valuation metrics. First, ESEA has a P/E GAAP ((FWD)) of 1.81, the lowest of competitors and 91% lower than its sector. Additionally, ESEA holds an EV/EBITDA ((FWD)) of 2.40, below most of its competitors and 78% below its sector median. Additionally, that value represents 58% below ESEA’s own 5-year average.

P/E and EV/EBITDA Metrics for ESEA Compared to Three Primary Competitors

| ESEA |

| DAC |

| CMRE |

| GSL |

| P/E GAAP ((FWD)) |

| 1.81 |

| 2.39 |

| 3.44 |

| 2.04 |

| EV/EBITDA ((FWD)) |

| 2.40 |

| 1.96 |

| 5.76 |

| 2.99 |

Source: Seeking Alpha, 26 Nov 23

Euroseas also has energy moving forward. Its CAGR for total assets over the past 3 years is 53.5%. Already mentioned was its strong revenue and cash flow growth while sustaining a solid net income margin. Additionally, Euroseas has a price/book ((FWD)) of 0.76, 69% below its sector, and a price/cash flow of 1.67, 87% below its sector. Also impressively, ESEA holds a tangible book value 3-year CAGR of 116%.

Price Metrics for ESEA Compared to Sector Median

| Price/Sales ((FWD)) |

| Price/Book ((FWD)) |

| Price/Cash Flow ((FWD)) |

| ESEA |

| 1.05 |

| 0.76 |

| 1.67 |

| Difference to Sector |

| -21.18% |

| -69.10% |

| -87.64% |

Source: Seeking Alpha, 26 Nov 23

As demonstrated in its YTD return, Euroseas has begun setting its sails. Given its strong growth, profitability, and undervalued metrics, ESEA will likely outperform its competitors in 2024. Therefore, a price target of $40 in 2024 is not unreasonable which would represent roughly a 40% upside this next year.

Risks to Investors

Global maritime transportation presents multiple risks to investors. While global demand is expected to grow at a modest 3.9% to 4.5% CAGR , recessions have a direct impact on global shipping. Furthermore, conflict or trade wars between U.S. and China will have an immediate impact on the fastest-growing marine shipping routes in the Pacific.

Unpredictable regional instability, piracy, and terrorism could all also impact global shipping lanes or result in a vessel being captured or destroyed. Having operated just 19 vessels last quarter, even a loss of one ship would have a significant impact. While these man-made disasters represent a concern, environmental factors, and inclement weather could be equally destructive. One study by CNN Weather stated that the quantity of hurricanes and typhoons could double globally by 2050. While the vessels that Euroseas operates can withstand rough seas, loss of containers is not uncommon.

As a result of these numerous risks, ESEA’s continued growth and profitability could be jeopardized. Beyond a sharp decline in share price, ESEA’s dividend yield could be reduced or eliminated. While the current yield for ESEA is high with a low payout ratio, the company does not have years-long history of paying dividends.

Summary

Historically, ESEA has been an underperformer in the maritime transportation industry. As demonstrated with strong fundamentals, including growth and profitability, the tides are turning for the company. ESEA has seen the highest net income margin, the highest 3-year CAGR revenue, and the highest forward-looking cash flow growth by percentage, compared to leading competitors.

Furthermore, despite a share price increase of 52% YTD, ESEA has an attractive value. This is seen with P/E and EV/EBITDA ratios compared to major competitors and its industry. Finally, Euroseas offers a solid dividend yield and sustainable payout ratio. While there are distinct risks with the entire marine shipping industry, I believe ESEA represents a buying opportunity both for capital appreciation and income.

For further details see:

Euroseas Ltd.: A Growing Underdog In The Challenging Marine Shipping Industry