ESEA - Euroseas: Margins Aren't Sustainable In The Long Run

2023-04-25 11:07:29 ET

Summary

- Euroseas Ltd has seen a massive increase in revenues as a result of the spiking shipping rates, but the future revenue seems uncertain.

- The company has managed to secure $425 million in contracts for the next 3 years, but after that, no one knows what the top line might look like.

- I think there is too much uncertainty here that will cause the valuation to stay suppressed and that makes me want to rate it a sell for now.

Investment Summary

Euroseas Ltd (ESEA) is a part of a global market as they both own and operate containerships that primarily transport dry and refrigerated cargo, both manufactured goods and perishable goods too. The company had massive revenue increases as global shipping prices rose quickly. But it seems the prices are coming down and the same margins and revenues that ESEA had don't seem sustainable. Shipping companies saw massive price hikes as supply chain issues began happening. In 2022 the company had 58% in net margins which I think is clearly not sustainable in the long term. Negative cash flows and shares being diluted at a rapid pace create a lot of red flags, enough to make me rate the company a sell. I think there are better sectors to be in than the shipping sector.

Market Overview

As the pandemic caused the shipping market to see increased demand and high prices, it seems the trend is reversing and staying that way. In a report by spglobal , they see the rates coming down to a more normal rate and only seeing a 2% fleet growth annually in the next several years. A company like ESEA has managed to secure some revenues for at least 3 more years, which can be seen across the board, but what happens after those contracts finish is any ones guess. But it seems the likelihood is the prices will decrease as supply chain issues start easing up and delays begin to be less common.

Shipping Market (spglobal)

It seems the prices will continue going in a more natural cycle where there are booms and busts. Here they expect the prices to come back to their long-term growth trend upwards. That's often why you see such different results from companies like ESEA quarter over quarter. I think it's clear looking back, the 2021 numbers were a perhaps once-in-a-lifetime event and that those who invested and benefited are most likely out already.

Quarterly Result

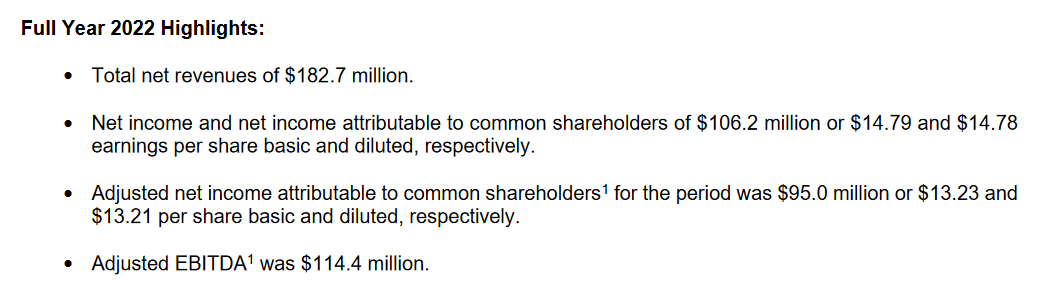

In the last earnings report , the company announced it had generated $42.9 million in revenues for the fourth quarter and in 2022 it had $182 million in revenues. This is twice as much as in 2021 and what is also impressive is the cost of the revenues. They didn't rise as fast which made the company able to have those incredible margins that were mentioned before.

{kind=link}

Looking at some comments from the report I think it's clear that these revenues aren't able to be kept up. The CEO Aristides Pittas had the following to say "During the fourth quarter of 2022, containership markets dropped more than 80% from their end-September levels as a result of reduced demand for trade and the reversal of port congestion and other transportation system inefficiencies". I think this comment really highlights some of the worries about companies in the sector. The same magical prices in 2021 are coming to an end and we are returning to a more normal environment. What might bring some comfort is that the company at least has a good order backlog, at 29% of the existing fleet. The management expects the market to be at a lower level for at least a few more years before any possible uptrend starts shaping. The CEO also mentioned that they have been able to have contracted revenues of $425 million in the next three years. What I think might be the reason for the very low valuation right now despite promised revenues is the fact investors are looking at the long-term, and right now it's pretty unclear.

Risks

I think one of the major risks with investing in a shipping company right now is that the prices aren't sustainable even after coming down a lot from a year ago.

{kind=link}

Above are some of the prices, it might seem great they are increasing a little for a company like ESEA, but compared to a year ago it's nowhere close. What ESEA has going for it is the contracted revenues, but after that, no one really knows what the revenues might look like. That places a lot of uncertainty in the company and that is never worth paying a premium for, which I think is a big cause for the p/e being so low.

Besides the future revenue is uncertain, the company has diluted the outstanding shares heavily from a few years ago. In 2022 it was around 7.2 million outstanding which is far higher than the 2019 levels of 2.9 million. The company has announced a $20 million buyback plan, but it will do little to satisfy investors in my opinion. That capital could be better spent on keeping a large cash position and making strategic investments if the shipping prices go down. Thankfully the net debt/EBITDA is very low, at 0.7 I think the company will be able to handle debt easily for the foreseeable future.

Valuation & Wrap Up

I think that the valuation of ESEA is questionable right now and in my opinion, it looks like a value trap. The last 12 months' revenues are not sustainable in the long run as 2021 saw incredible shipping rates and everything is pointing to it being a very long time until those numbers are seen again. Most companies in the shipping industry are valued at incredibly low multiples using the last 12 months' numbers, with ESEA for example being at 1.5. But when you look at future estimates that number goes up a lot. A yearly EPS decrease of around 19% is expected until 2025 which I think is because of the uncertainties about future revenues for ESEA for example.

{kind=link}

But as I said, this value trap isn't exclusive to ESEA, Seanergy Maritime Holdings Corp (SHIP) has a similar low p/e using the last 12 months. I don't want to speculate on what the margins might be for ESEA in 2026 when most of their contracts have run out because they will be directly impacted by the shipping rates of that environment. Anyone saying they can predict that would be a millionaire. If you want to have exposure to the shipping industry then you need to be aware that there is a lot of uncertainty, and a lot of companies have distributed massive dividends whilst also diluting shares too. The same goes for ESEA. I think there are more stable industries to be a part of and for that reason, I will be rating ESEA a sell for now. Buying right now feels like buying at the peak, instead of the beginning of a bull run.

For further details see:

Euroseas: Margins Aren't Sustainable In The Long Run