RNP - Evaluating A Switch From RNP To RFI

2023-08-13 08:00:00 ET

Summary

- Cohen & Steers Total Return Realty Fund invests in REIT equities, with some exposure to their preferreds or bonds.

- The Cohen & Steers REIT & Preferred Income Fund is about evenly split between REIT equities and their preferreds/bonds.

- The article reviews the holdings, distributions, price, and NAV of both CEFs and compares their portfolio strategies.

- Looking at where the economy is and the possibility we are near the peak in interest rates, I give the RNP CEF a Buy rating and decided to hold onto our RNP shares.

(This article was co-produced with Hoya Capital Real Estate )

Introduction

My wife owns the Cohen & Steers REIT & Preferred Income Fund ( RNP ) in her Roth account with reinvestment activated. Just after COVID struck, we sold Cohen & Steers Total Return Realty Fund ( RFI ) to buy RNP, the theory being the leverage employed by RNP would provide "umph" as the market rallied and the leveraging costs dropped. Turns out that added 200bps in CAGR but with leveraging costs rising now, is it time to switch back? This article reviews both CEFs and tells me to stay the course which also then translates into a Buy rating for the RNP CEF.

assets-prod.cohenandsteers.com logo

Cohen & Steers Total Return Realty Fund review

I will start with the CEF we do not currently own, which Seeking Alpha describes as:

The fund seeks to invest in stocks of companies operating in the real estate sector, including real estate investment trusts. It invests in stocks of companies across all market capitalizations. It benchmarks the performance of its portfolio against the FTSE NAREIT Equity REIT Index, the S&P 500 Index, and a blended index composed of 80% FTSE NAREIT Equity REIT Index and 20% BofA Merrill Lynch REIT Preferred Securities Index. Cohen & Steers Total Return Realty Fund, Inc. was formed on September 4, 1992.

Source: seekingalpha.com RFI

RFI has $305m in AUM 89bps based on managed assets. The Forward yield is 8.3%.

The manager’s description of their fund is:

The investment objective of the Fund is to seek to achieve a high total return through investment in real estate securities. Real estate securities include common stocks, preferred stocks and other equity securities of any market capitalization issued by real estate companies, including real estate investment trusts (REITs) and similar REIT-like entities.

Source: resources.cohenandsteers.com RFI

RFI holdings review

resources.cohenandsteers.com RFI sectors

The Other weighting consists of Office, Shopping Centers, and Manufactured Housing REITs. To me, the important takeaway from the sector allocations is that RFI has 11% in corporate bonds, and another 9% in preferred stocks, much less than RNP's exposure.

RFI is a very top heavy CEF with the largest ten positions comprising 50% of the portfolio despite holding almost 200 securities.

resources.cohenandsteers.com RFI holdings

These are all REITs. The largest preferred stock position is the DigitalBridge Group Inc 7.15% Pfd I at .51%; the largest corporate bond position is the Charles Schwab Corp Flt Perp Sr:I at .33%. RFI also sold options against ten positions; they are long just one.

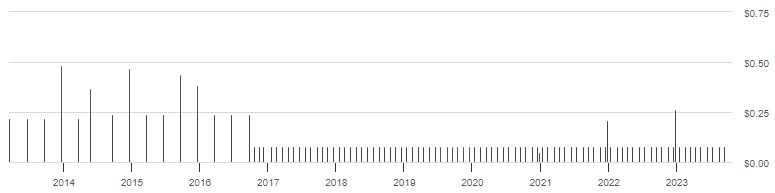

RFI distributions review

{kind=link}

seekingalpha.com RFI DVDs

At the end of 2022, RFI paid a special dividend of $.266. The current monthly rate is $.08, in effect since switching from quarterly to monthly payouts in 2016. In 2022, the total payout of $1.226 consisted of: $.062 Qualified; $.395 Not Qualified; $.539 Cap Gains; $.23 Section 199A. In 2021, the sources for the $1.17 in distributions were: 3.6% Qualified; 81.9% CGs; 14.5% 199A.

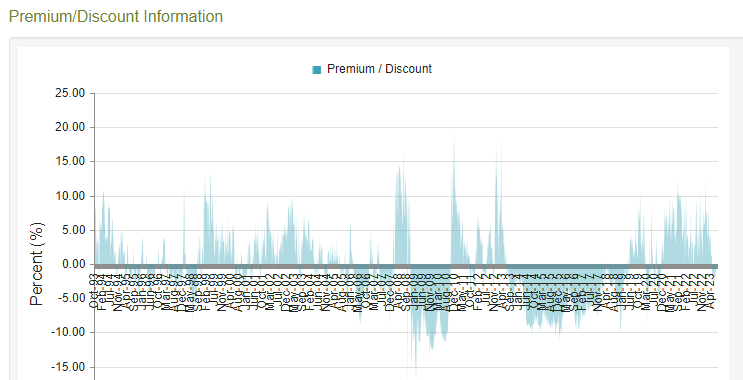

RFI premium/discount review

{kind=link}

CEFConnect.com

RFI has a long history of selling for a premium (up to 15%) or 10% discounts. Currently, it sells at a .09% premium after spending most of the recent months at a discount near 2%. This makes RFI a good CEF to try cashing in on the discount/premium reversal that seems to be underway. Its z-score has moved from a 1-year negative value (which is good) to a positive value for the last three months.

Cohen & Steers Total Return Realty Fund review

Seeking Alpha describes this CEF as:

It seeks to invest in the stocks of companies operating in the real estate sector including real estate investment trusts. For its fixed income portfolio, the fund typically invests in debt and preferred securities of companies operating across diversified sectors. It employs fundamental analysis to create its fixed income portfolio with a focus on the issuer’s creditworthiness, corporate and capital structure, placement of the preferred or debt securities within that structure, momentum and other exogenous signals, and relative value versus other income security classes and for its equity portfolio also it employs fundamental analysis to create its portfolio with a focus on growth potential, earnings estimates, and the quality of management. The fund benchmarks the performance of its portfolio against the FTSE NAREIT Equity Index, S&P 500 Index, Merrill Lynch Fixed Rate Preferred Index, and FTSE NAREIT Equity REIT Index. The predecessor CEF started in 2003.

Source: seekingalpha.com RNP

RNP has $1.4b in AUM 89bps based on managed assets. The Forward yield is 8.46%.

The manager’s description of their fund is:

The primary investment objective of the Fund is high current income through investment in real estate and diversified preferred securities. The secondary investment objective is capital appreciation.

Source: cohenandsteers.com RNP

RNP holdings review

RNP provides two breakdown, which is informative considering their portfolio is even split between REIT equities and preferreds.

resources.cohenandsteers.com RNP sectors

The asset mix is: 48% REITs, 24% bonds, 24% preferreds, 3% convertibles, 1% other. With a higher security count, RNP is less concentrated than RFI, with the Top 10 only being 31% of the portfolio. Both of those facts, plus the use of leverage, highlight the major differences between RNP from RFI.

resources.cohenandsteers.com RNP holdings

If you compare the Top 10 lists, they are the exact same REITs, only in a slightly different order. Like RFI, the Charles Schwab Corp Flt Perp Sr:I is the biggest preferred position at .84%, with the Emera 6.75% 6/15/76-26 the biggest bond position at .81%. RNP also has interest-rate swaps.

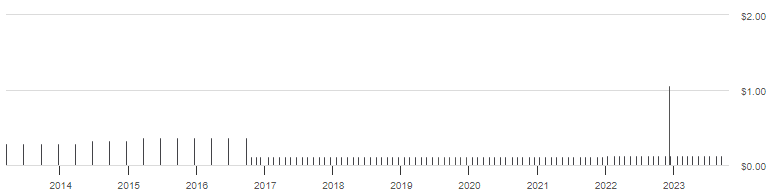

RNP distributions review

{kind=link}

seeingalpha.com RNP DVDs

At the end of 2022, RNP paid a special dividend of $1.07. The current monthly rate is $.136, in effect since 2021. Prior to that, since switching from quarterly to monthly payouts in 2016, it was $.124. In 2022, the total payout of $2.703 consisted of: $.86 Qualified; $.234 Not Qualified; $1.39 Cap Gains; $.23 Section 199A. In 2021, the split was 34%/66% between Qualified and CGs for the $1.488 in distributions.

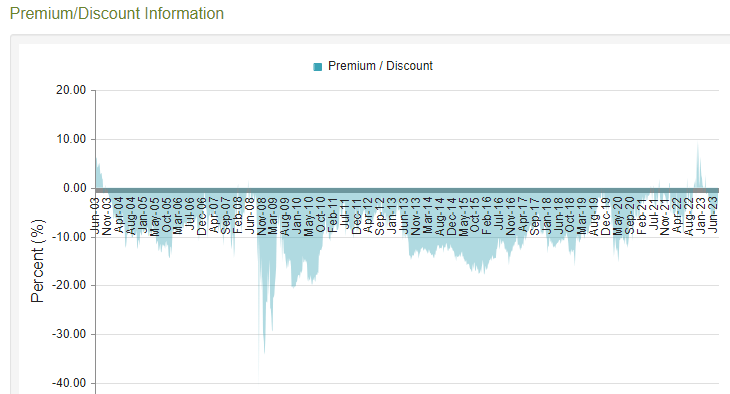

RNP premium/discount review

{kind=link}

CEFConnect.com

Unlike RFI, RNP has spent most of its time selling at a discount, often at ones greater than 10%. The current discount is only 2.87%, which results in a three-month z-score of 1.83, slightly higher than RFI's z-score.

Comparing CEFs

| Factor |

| RFI |

| RNP |

| AUM |

| $305m |

| $1.4b |

| Managed Asset Fees |

| 89bps |

| 133bps |

| Leverage |

| 0% |

| 32% |

| Yield |

| 8.3% |

| 8.5% |

| # of Holdings |

| 200 |

| 343 |

| Premium/Discount |

| .1% |

| -2.9% |

| Equity/PFD-FI allocation |

| 80%/20% |

| 48%/52% |

| Top 10 concentration |

| 50% |

| 31% |

The two CEFs have shown similar return and risk data since 2003 but the past decade has seen RNP doing better.

{kind=link}

PortfolioVisualizer.com

Portfolio strategy

Choosing between these two Cohen & Steers CEFs boils down to how investors feel about the following points.

- They want or do not want leverage exposure (RNP if yes, RFI if no)

- They want the best performer (leaning RNP)

- They want the best risk/return performer (toss up)

- They want the most income (RNP has slight edge)

- They want CEF that maintained its NAV better ((RNP))

- They want US-focused portfolio ((RFI))

- They want the most equity exposure ((RFI)), thus RNP for those believing preferreds and bonds are better allocation at this time.

- Buying at a discount (RNP but close)

- Lower concentration risk ((RNP))

My decision

Based on the following observations, I decided to keep our exposure to RNP and not switch.

- RNP had a smaller drawdown during both the 2020 COVID and the 2023 banking meltdowns.

- RNP held up better over the past year when the FOMC made the biggest upward push in interest rates the US ever saw.

- Most statistics were too close to warrant switching, something I do look out for when there are similar funds. NAV maintenance strongly favors RNP.

- We have little exposure to leveraged CEFs, so that did not play a part. I did then compare RNP against the RQI CEF and again chose not to switch.

Looking at where the economy is and the possibility we are near the peak in interest rates, I give the RNP CEF a Buy rating.

Final thoughts

As both the RFI CEF and RNP CEF are popular with Seeking Alpha readers, they have been reviewed regularly, most times, as I did here, compared against other funds with similar investment goals, though I did not see any article where RFI was matched up with RNP. Those articles would be good reads as part of any due diligence effort. Here is brief information on many of the tickers covered recently when compared to RFI or RNP.

{kind=link}

seekingalpha.com HCIB

For further details see:

Evaluating A Switch From RNP To RFI