PZZA - Evaluating Papa John's Weaknesses Amidst Industry Disruptions

2023-07-12 11:56:37 ET

Summary

- Papa John's has differentiated itself in the restaurant industry but remains weaker than its larger peers, with flat margins and underwhelming growth.

- The company's franchising strategy is the correct one but we believe it should have contributed to further improvement, implying weakness in the brand.

- Industry developments are not wholly positive for PZZA and could contribute to further market share loss. This said, Management is doing a good job with product development.

- PZZA's valuation looks appropriate given its weakness relative to peers.

Investment thesis

Our current investment thesis is:

- PZZA has differentiated itself in the restaurant industry, however, is clearly a weaker participant relative to the larger businesses.

- Financial improvement has not been significant, as margins have remained flat and growth has been underwhelming.

- Continued franchising should support a de-risked trajectory, alongside margin improvement.

Company description

Papa John's ( PZZA ) is a global pizza delivery and carryout restaurant chain headquartered in the United States. With over 5,500 locations worldwide, the company is known for its quality ingredients, superior customer service, and commitment to innovation.

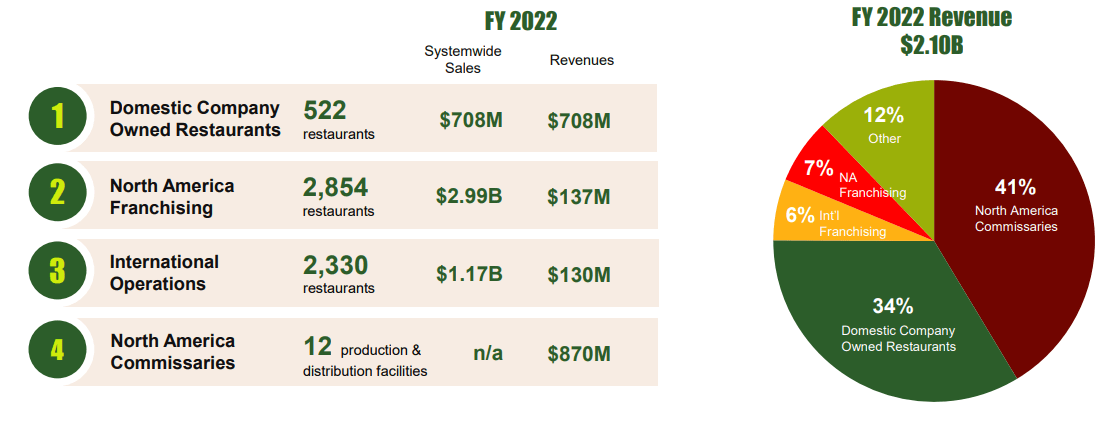

It operates through four segments: Domestic Company-Owned Restaurants, North America Commissaries, North America Franchising, and International Operations.

Share price

PZZA's share price has underperformed the stock market, although this has primarily occurred post-2022, as industry weakness and post-pandemic improvement seems to have investors hesitant. The general positive trajectory is a reflection of a consistent improvement in the business.

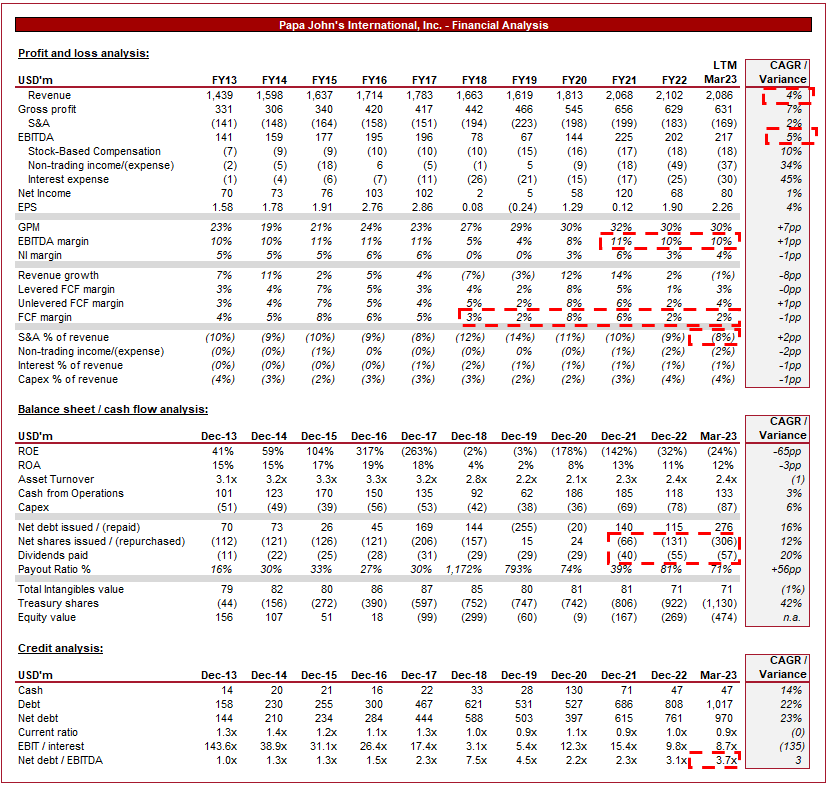

Financial analysis

{kind=link}

Presented above is PZZA's financial performance for the last decade.

Revenue & Commercial Factors

PZZA's revenue has grown at a mild CAGR of 4% in the last 10 years, partially due to the process of refranchising, which reduces revenue by providing the benefit of lower revenue volatility and reduced operational risk. During this period, the number of North American company-owned franchises declined by 22% while the number of franchises increased by 9%.

Business Model

PZZA prides itself on using high-quality ingredients, including fresh dough, vine-ripened tomatoes, and premium meats and cheeses. In addition to this, PZZA seeks to innovate and adapt its menu to changing consumer trends, seeking to refine and improve its offering to customers. This is how PZZA differentiates itself from its peers, while also providing a traditional restaurant experience for in-store dining.

Product (PZZA)

{kind=link}

PZZA primarily operates through delivery and carryout services, emphasizing convenience and speed to consumers, seeking to innovate in order to make this as seamless as possible for consumers.

Similar to the other large US QSR chains, PZZA operates on a predominantly franchised business model, allowing for rapid expansion and leveraging local market knowledge. This de-risks the business as it is no longer responsible for recruitment and running the store, while also reducing the size of its balance sheet. With several franchise partners, PZZA can grow at a faster rate, without the need to invest with its balance sheet. Since FY13, the number of overseas franchises has grown by 104%. PZZA's revenue and restaurant numbers are presented below.

Revenue profile (PZZA)

{kind=link}

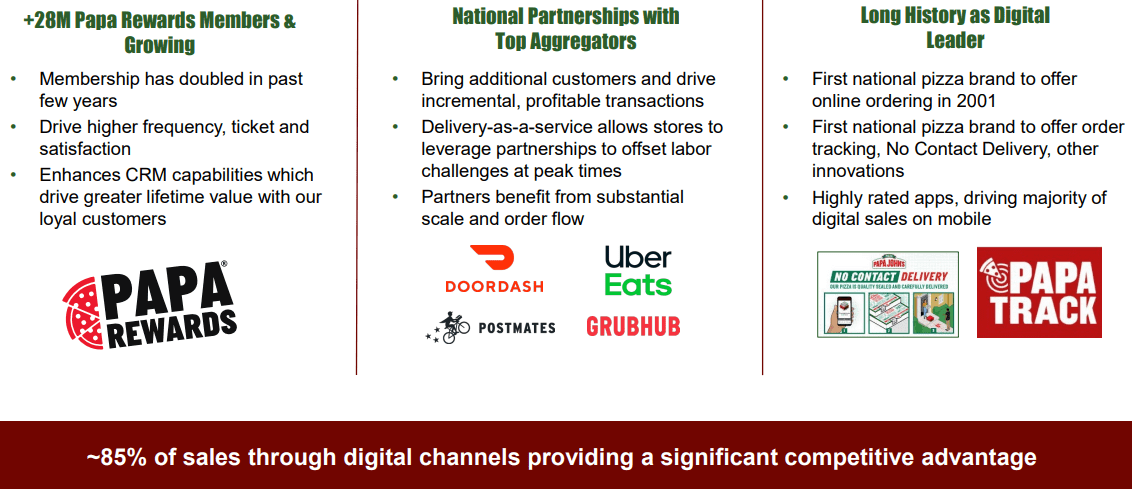

The company has invested in technology to enhance the customer experience, including online ordering, mobile apps, and loyalty programs (c.85% of sales are through the digital channel and so these factors are critical developments). Further, PZZA has developed an efficient delivery system, enabling timely and accurate order fulfillment. These factors seek to drive an improvement in customer conversion, as well as operational efficiencies to generate margin improvement.

Digital development (PZZA)

{kind=link}

The company has successfully expanded into international markets, leveraging its brand and franchisee choice to correctly adapt to local preferences. Despite this, its market penetration remains low relative to peers, especially in key markets. This presents the opportunity for further growth in the coming years.

Store penetration (PZZA)

These commercial and operational improvements in recent years have contributed to outsized underlying growth for the business, exceeding the industry average. The key value drivers we feel are the continued expansion of locations and the development of its digital capabilities.

Growth (PZZA)

{kind=link}

Restaurant Industry

Competitors in the restaurant industry look to differentiate themselves through menu offerings, pricing strategies, and delivery capabilities. PZZA is currently the 3rd largest Pizza QSR business, facing competition from other chains like Domino's ( DPZ ), Pizza Hut ( YUM ), and Little Caesars, as well as other QSR businesses like McDonald's ( MCD ), KFC, Subway, Burger King, Wendy's ( WEN ), Chipotle ( CMG ), and others.

Consumers are seeking convenient and quick dining options, driving the growth of delivery apps, such as DoorDash ( DASH ) and online ordering. Our view is that this has created increased competition for the traditional market participants, as consumers now have substantially more choices. Further, Pizza delivery was a classic option available to many, now most cuisines can be purchased conveniently. This adds a further level of competition.

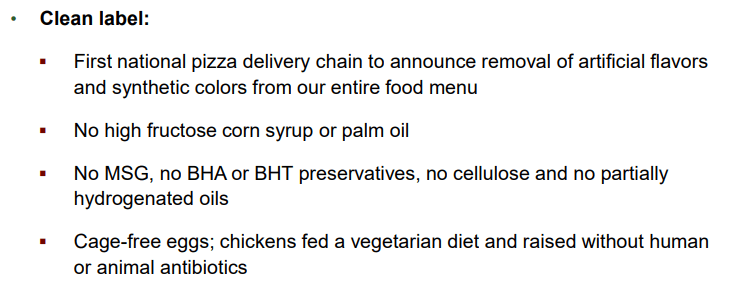

Growing consumer focus on health-conscious choices has contributed to increased competition for traditional QSR businesses, as consumers seek healthier options. This has contributed to the development of healthier options, as well as vegan and gluten-free. PZZA has rapidly expanded in this area, seeing it as an opportunity to develop a quality offering in this segment. This innovation continues with varying positive improvements following the launch of a host of vegan options.

Product improvement (PZZA)

{kind=link}

Economic & External Consideration

Current economic conditions present a near-term risk to PZZA, as stubborn inflation and elevated interest rates are squeezing consumers' finances. As a result of this, the feeling is that discretionary spending is softening, as consumers seek to carefully allocate funds.

In the most recent quarter, PZZA experienced a (3)% decline YoY, capping off three successive quarters of negative growth. This is primarily due to the refranchising of 90 locations, however, when excluding this, PZZA is growing slowly with system-wide sales up 2%. This reflects a degree of resilience although growth remains mild.

Margins

PZZA's margins have remained flat over the historical period, with an EBITDA-M of 10% and a NIM of 4%.

Margins development has been disappointing in our view, as the push to franchise locations should have contributed to improved margins but this does not look to be the case.

The company has faced offset pressures due to inflationary conditions, with wage and input inflation contributing to margin pressure. Due to the level of competition faced, it is not easy to increase menu prices.

Our expectation is for margins to progressively improve, as franchising begins to contribute to improvement and inflationary pressures subside.

Balance sheet & Cash Flows

Despite the high ND/EBITDA ratio, PZZA is moderately financed, with the majority of this representing lease liabilities.

Capital allocation has been focused on shareholder distributions, with both buybacks and dividends. Management has funded this in part with debt in recent years, growing the balance in line with profitability improvements.

Outlook

{kind=link}

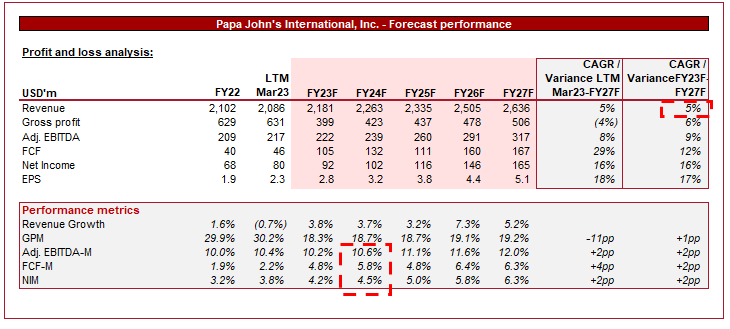

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting an improvement in revenue growth, as refranchising slows and new franchise locations are opened. Based on the company's current trajectory, this looks reasonable.

Margins are forecast to gradually improve, in line with our expectations, as cost pressures subside.

Industry analysis

Restaurant industry (Seeking Alpha)

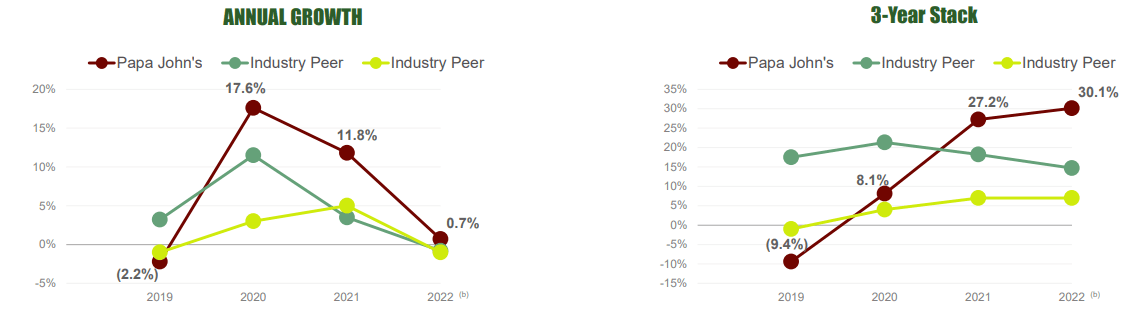

Presented above is a comparison of PZZA's growth and profitability to the average of its industry, as defined by Seeking Alpha (38 companies).

PZZA performs poorly relative to peers. From a growth perspective, the company lags behind its peer average on every revenue metric, implying the business is progressively losing market share. Profitability improvement is a reflection of its overly negative results in FY18-FY20.

Margins are equally disappointing, with a deficit in every metric barring efficiency. Even if the margin improvement expected is achieved, PZZA would remain below the industry average.

Based on this, we believe PZZA should trade at a noticeable discount to the peer group, reflecting its financial weakness.

Valuation

Valuation (PZZA)

{kind=link}

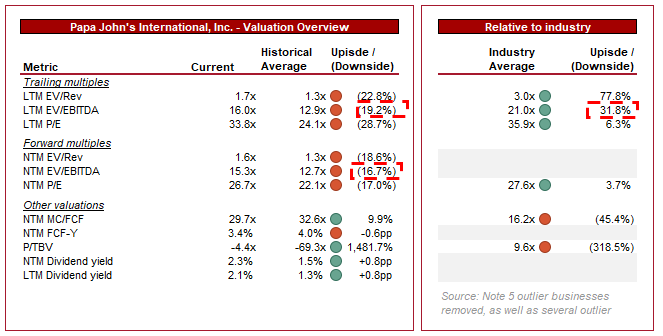

PZZA is currently trading at 16x LTM EBITDA and 15x NTM EBITDA. This is a premium to its historical average.

Our view is that a small premium is likely warranted for PZZA relative to its historical average. This is because PZZA has been able to successfully franchise globally, allowing the business to de-risk while increasing its chances of improving margins.

Relative to its peers, PZZA is trading at a noticeable discount. This reflects the company's weakness, although the difference shrinks on a NTM P/E basis.

Based on this, we believe PZZA is likely priced correctly. It is slightly overvalued on a historical basis but marginally undervalued on a peer comparison. This said, if the margin outlook develops beyond an EBITDA- of c.12%, we could see the business rapidly become undervalued.

Final thoughts

PZZA is a solid business, differentiating itself through the development of a higher-quality offering relative to its direct peers. This said, the company is clearly a second-rate participant in the market, significantly weaker than Pizza Hut and Domino's. This is reflected in its relative performance and inability to generate material margin improvement through franchising.

We believe PZZA looks well-priced. It is trading at a justifiable premium to its historical average but a required discount to its peers.

For further details see:

Evaluating Papa John's Weaknesses Amidst Industry Disruptions