YRI:CC - Evaluating The Proposed Acquisition Of Yamana By Agnico And Pan American

Summary

- Win-win transaction for all parties involved.

- Yamana shareholders receive a superior offer relative to Goldfields with lower closing costs.

- Increased probability of transaction closing.

- Agnico benefits by consolidating ownership of Malartic mine while Pan American significantly bulks up its South American exposure.

Pan American Silver ( PAAS ) and Agnico Eagle ( AEM ) have made a joint offer to acquire Yamana Gold ( AUY ). Under the terms of the offer, Pan American would acquire Yamana, while Agnico would acquire Yamana's Canadian assets. The offer totals $5.02 per share of Yamana, which represents a 23% premium to the company's closing price on the day before the offer was made and a 15% premium to the offer made by Gold Fields ( GFI ). The Yamana board has determined that the new offer is superior to the one made by Gold Fields. This is in part because the deal between Gold Fields and Yamana was not viewed favorably by investors in Gold Fields, as the potential synergies of the deal were not effectively communicated. As a result, the probability of the deal between Gold Fields and Yamana closing was considered to be low.

{kind=link}

This transaction will be a win-win for all parties involved. For Yamana shareholders, the new offer from Pan American and Agnico represents an incremental value with lower transaction closing risk compared to the previous offer from Gold Fields. This is likely because the new offer is considered a superior proposal by the Yamana board and because the deal with Gold Fields was not viewed favorably by investors in Gold Fields.

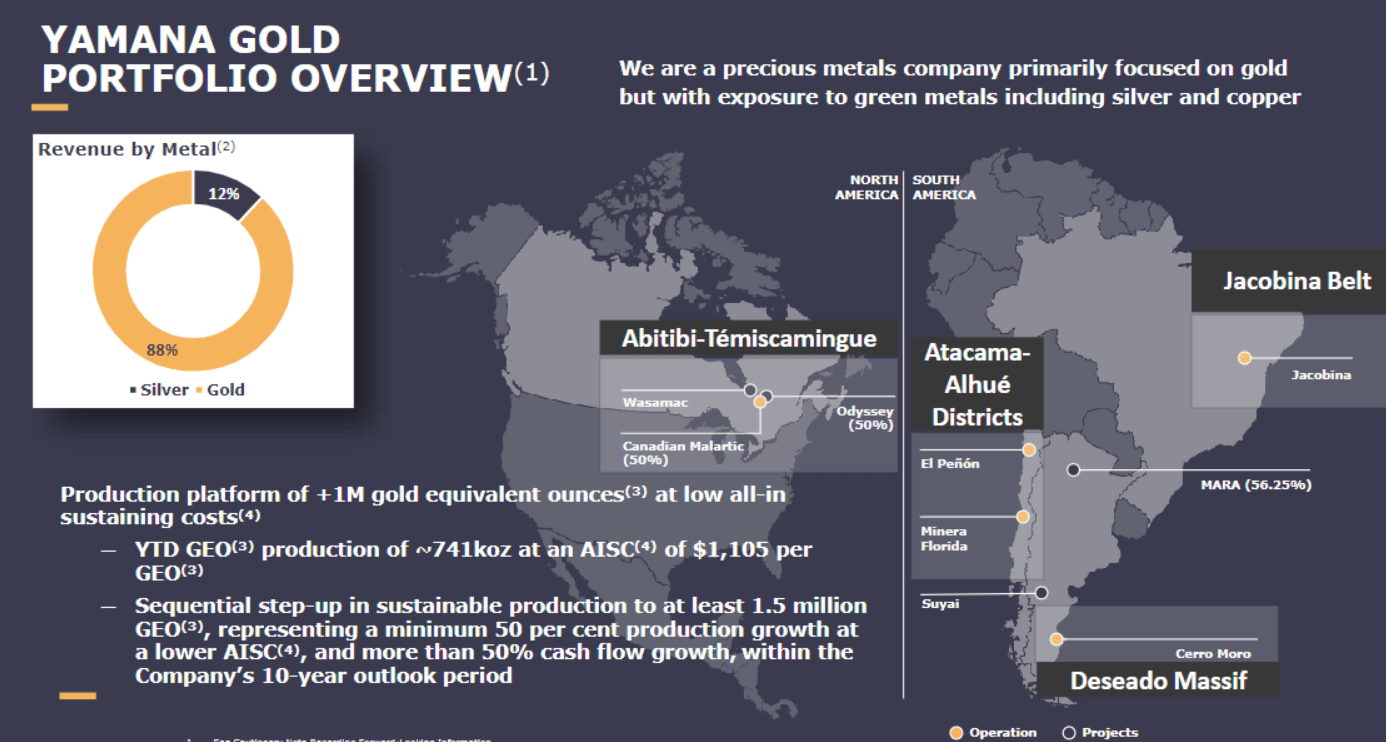

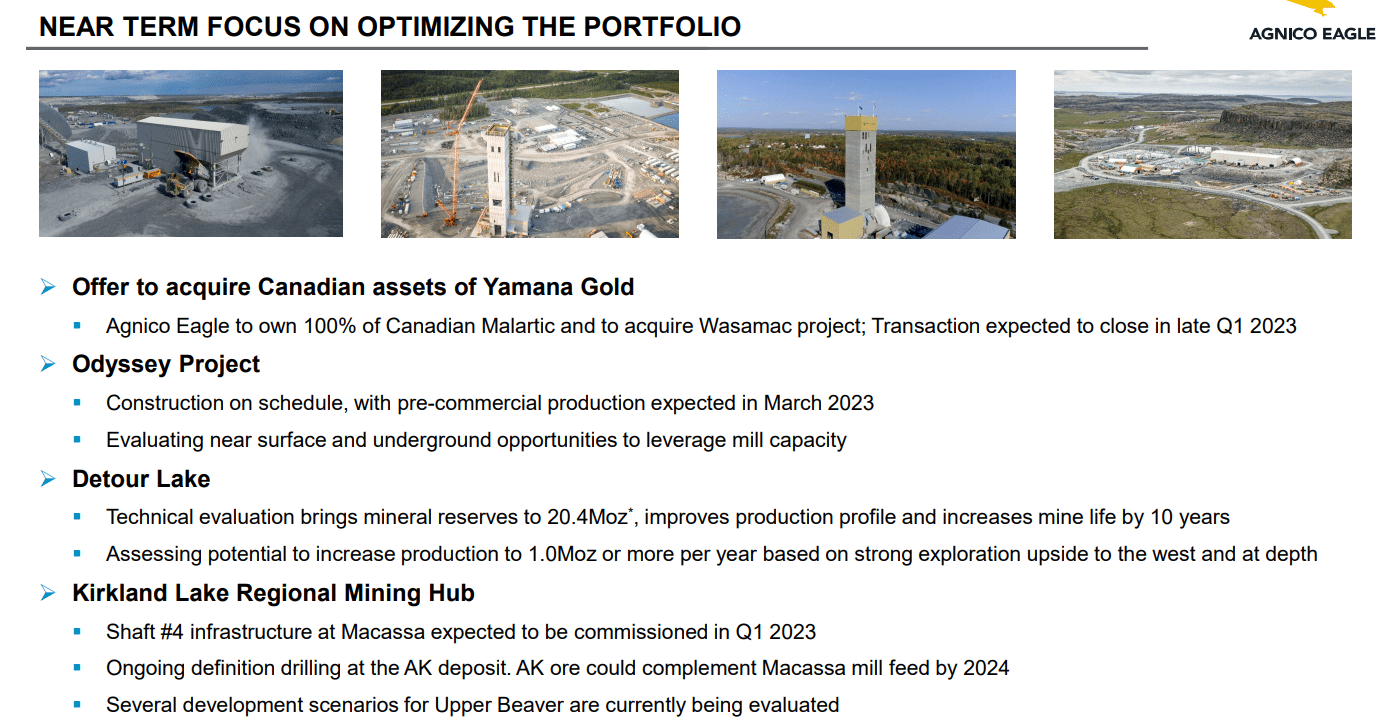

Pan American stands to benefit from the acquisition by gaining increased scale, diversification, and financial capacity in Latin America at an attractive price. Agnico would benefit by consolidating control of the Canadian Malartic mine and by transitioning it into one of the world's largest underground mines. The acquisition would also give Agnico access to a 55ktpd mill located nearby.

For Gold Fields, the new offer from Pan American and Agnico represents a potential way out of a transaction that was poorly received by the market. The company would be able to walk away from the deal with Yamana with a $300 million break fee. Overall, it appears that the proposed acquisition could be a mutually beneficial arrangement for all parties involved.

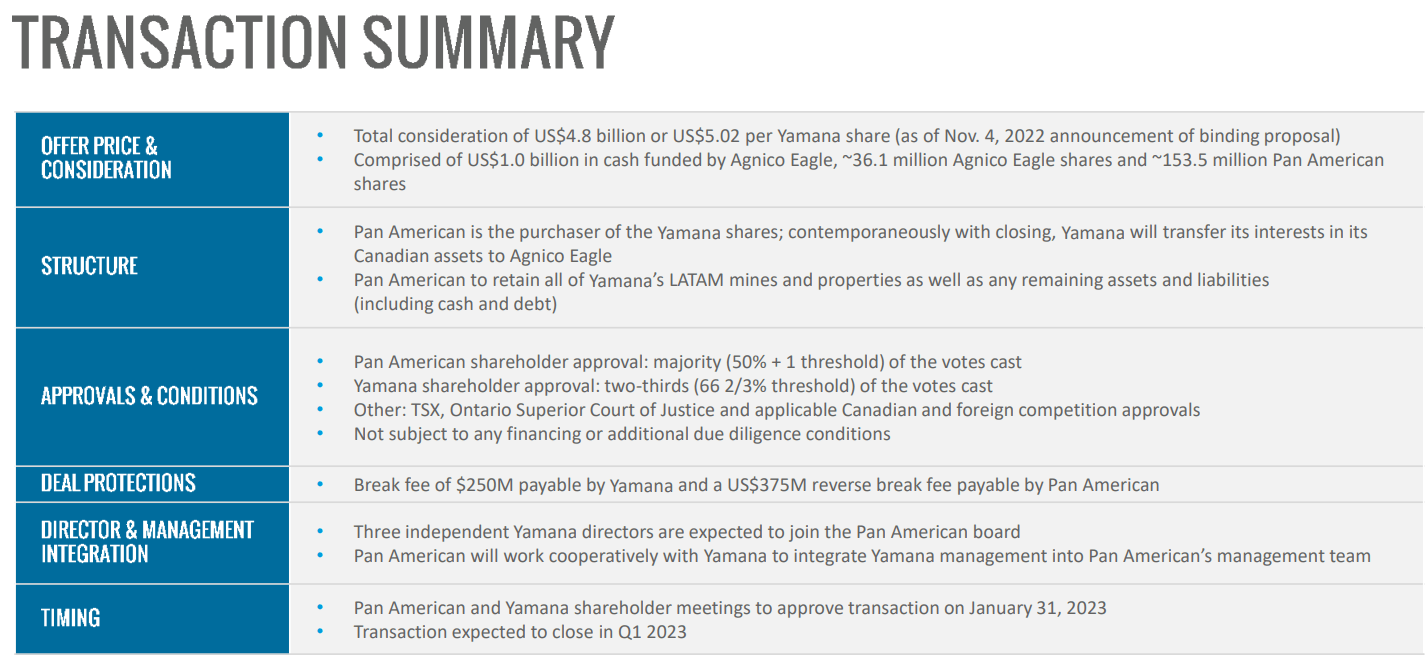

Under the terms of the offer, Agnico Eagle Mines will contribute 51.5% of the $4.8 billion valuation, or $2.5 billion, in the acquisition of Yamana Gold. This includes $1.0 billion in cash and $1.5 billion in AEM shares. The acquisition is being valued at approximately 1.0 times the net asset value ((NAV)) of Agnico, based on analyst consensus. Prior to the announcement of the acquisition, Agnico was trading at approximately 0.8 times its NAV, according to analyst consensus. The acquisition is expected to have minimal dilution to Agnico's NAV. The price for the acquisition is considered attractive as it will allow Agnico to consolidate ownership of one of Canada's key gold mines, which is expected to grow in both resource ounces and production capability with the potential for a second shaft and an underutilized mill.

Pan American Silver, on the other hand, will contribute 48.5% of the consideration for the acquisition, or $2.3 billion in PAAS shares. This values the acquisition at approximately 0.7 times the NAV of Pan American, based on analyst consensus. Prior to the announcement, Pan American was trading at approximately 0.8 times its NAV, according to analyst consensus. The acquisition is expected to be approximately 14% accretive to Pan American's NAV, net of the break fee.

{kind=link}

Key Transaction Details for Yamana Shareholders:

- The total consideration for the acquisition of Yamana Gold is $5.02 per YRI share, which includes 0.1598 Pan American shares, 0.0376 Agnico shares, and $1.0 billion in cash from Agnico.

- The new offer values Yamana at $4.8 billion, representing a 23% premium to Yamana's share price and a 15% premium to the offer made by Gold Fields.

- The Yamana board has determined that the new offer is a superior proposal to the one made by Gold Fields, and Gold Fields has the right to match the offer within 5 business days. If the Gold Fields transaction is terminated, Yamana will pay a $300 million break fee.

- The acquisition is not conditional on financing or additional due diligence, and only requires a simple majority shareholder vote (50%+1) from Pan American. Closing is expected in late Q1 of 2023.

- At closing, Pan American and Yamana shareholders will own 58% and 42% of Pan American, respectively, and Agnico and Yamana shareholders will own 93% and 7% of Agnico, respectively.

- Agnico plans to purchase up to $150 million of Pan American shares in the open market as a strategic investment, but the purchases are at Agnico's discretion.

How Does This Transaction Affect Agnico and Pan American?

For Agnico:

- Agnico is consolidating its ownership of Canadian Malartic, one of its key assets in Val d'Or, which is expected to grow both in terms of resource size and as a larger operation with the potential for a second shaft. The acquisition also gives Agnico increased optionality with a nearby 55ktpd mill that could be used for its operations or future projects in the region.

- The acquisition is expected to be slightly dilutive to Agnico's NAV, but accretive on current financial and operating metrics. It is also expected to be modestly near-term accretive to EBITDA, FCF, and production per share.

- The acquisition will increase Agnico's leverage, but the company is forecast to have over $700 million in cash by the end of 2022 and is expected to generate over $1 billion in annual FCF, which should allow it to deleverage quickly. Agnico is funding the $1.0 billion cash component of the acquisition through its $1.2 billion credit facility.

{kind=link}

For Pan American:

- The acquisition of Yamana Gold will increase Pan American Silver's scale as a producer of both gold and silver, with the majority of the production coming from Latin America.

- The acquisition will also provide diversification for Pan American, with a total of 12 operating assets in 7 different jurisdictions and the potential for a 13th mine in a 9th jurisdiction. The pro forma revenue split, excluding the Escobal mine, is expected to be approximately 75% gold and 25% silver at current spot prices.

- The acquisition will also provide additional cash flow and balance sheet capacity for Pan American as it moves towards construction on the La Colorada skarn deposit in the coming years.

- The acquisition is expected to be 14% accretive to Pan American's earnings, but neutral to its consensus NAV at current spot prices.

- This being said, the heavy lifting for Pan American will begin after the transaction closes. Its portfolio of a dozen operating assets is bloated and will require significant trimming. While the company adds scale, it will need to demonstrate that the assets it has acquired can be operated effectively and contribute to cash flow in the medium term. Investors seem to be realizing the work that lies ahead and as a result, PAAS shares have underperformed its peers since the acquisition was announced.

Summary : The acquisition of Yamana by Agnico and Pan American is more sensible when viewed through the lens of synergies and fit versus the Gold Fields proposal. In my view, Agnico walks away the ultimate winner in this transaction as it consolidates the ownership of the Malartic mine which is one of the crown jewels of the Canadian gold mining industry. Pan American also stands to benefit but it faces near term challenges digesting the newly acquired projects. The biggest beneficiaries are the Yamana shareholders who now face an easier path towards closing at a sweetened price.

For further details see:

Evaluating The Proposed Acquisition Of Yamana By Agnico And Pan American