EVEX - Eve Air Mobility: Way Too Early To Get Excited

2023-08-14 13:34:02 ET

Summary

- Eve Air Mobility is a pre-revenue company developing an eVTOL aircraft and urban air traffic management system.

- Eve's enterprise value of $2 billion exceeds Embraer's entire traditional aircraft business, despite generating no revenue.

- Eve's development timeline is behind its key competitors, raising doubts about its ability to achieve commercial operations by 2026.

Executive Summary

Eve Air Mobility ( NYSE: EVEX ) is a pre-revenue company that is working on developing an electric vertical take-off and landing or eVTOL aircraft as well as an urban air traffic management system. Eve was formed in 2020 when it was spun off from the Brazilian aircraft manufacturer Embraer ( NYSE: ERJ ), which still maintains a controlling 76% stake. As of the time of writing this video Eve has a market cap of about $2.3 billion and an enterprise value of about $2 billion. Embraer currently has a market cap of ~$2.7 billion and an enterprise value of ~$3.1 billion. At today's stock price Embraer's stake in Eve is worth ~$1.75 billion. If you subtract the value of their Eve stake, Embraer’s stub enterprise value is just $1.35 billion. Thus, today Eve, which has generated zero revenue, is worth more than Embraer's entire traditional aircraft business which generated $4.5 billion of revenue last year. Clearly the market is pricing in a lot of growth for Eve. In my opinion this premium valuation is premature given that Eve is still years away from generating revenue, let alone profits.

The rest of this article will be split up into three sections. Firstly, we’ll look at why the market is so excited about the nascent eVTOL industry. Then we’ll look at Eve’s development timeline versus some of its key competitors. And finally we’ll look at how profitable Eve could potentially be at scale.

eVTOL Industry

An eVTOL is exactly what it sounds like, a fully electric aircraft that can take off and land vertically. There are a few advantages of eVTOL’s over traditional airplanes and helicopters. Firstly, if they use renewable electricity they can have zero carbon emissions. Secondly, they can be quieter than traditional kerosine-powered helicopters. And thirdly, their lack of an internal combustion engine should make them easier to maintain.

{kind=link}

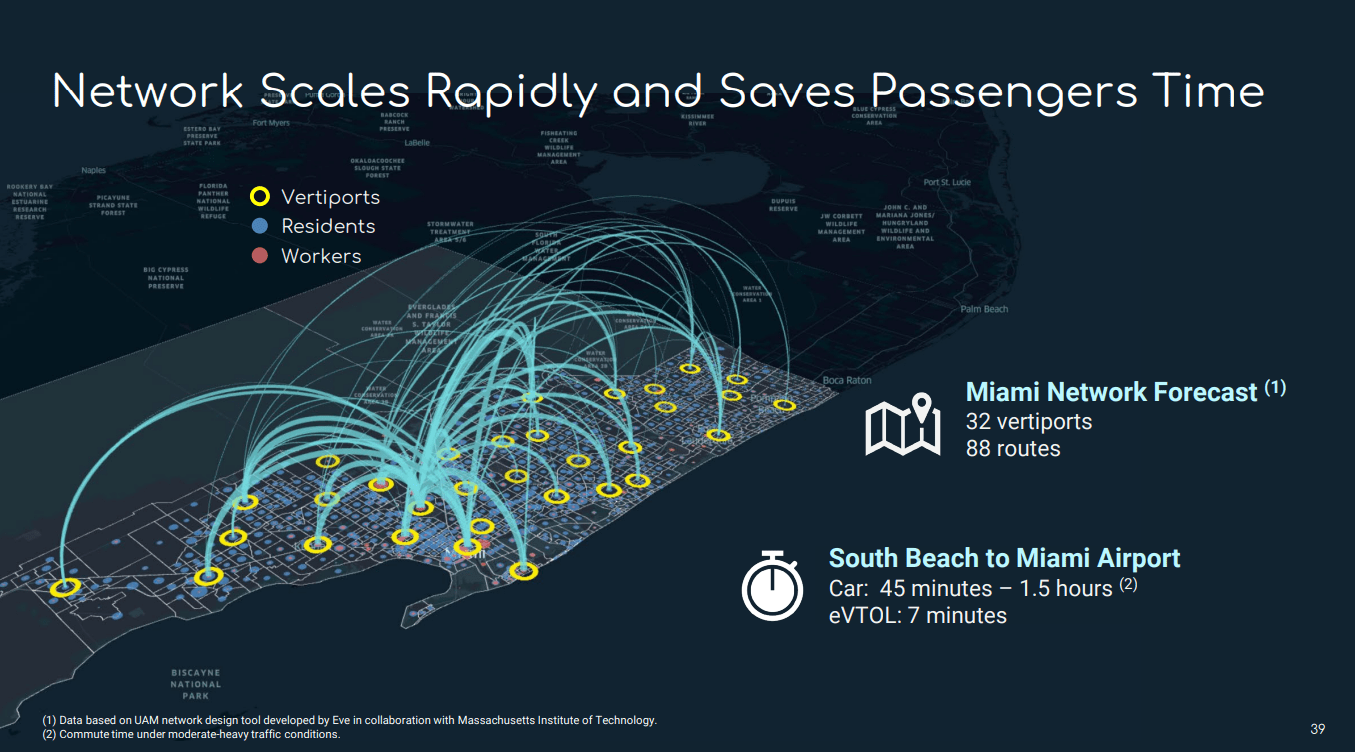

The main anticipated use case for eVTOL aircraft is urban passenger transport. For example, Eve envisages their aircraft being used to transport passengers from airports to city centers. They claim that their aircraft will be able to take passengers from the Miami International Airport to the center of the city in 7 minutes, a journey which would take about an hour by car.

{kind=link}

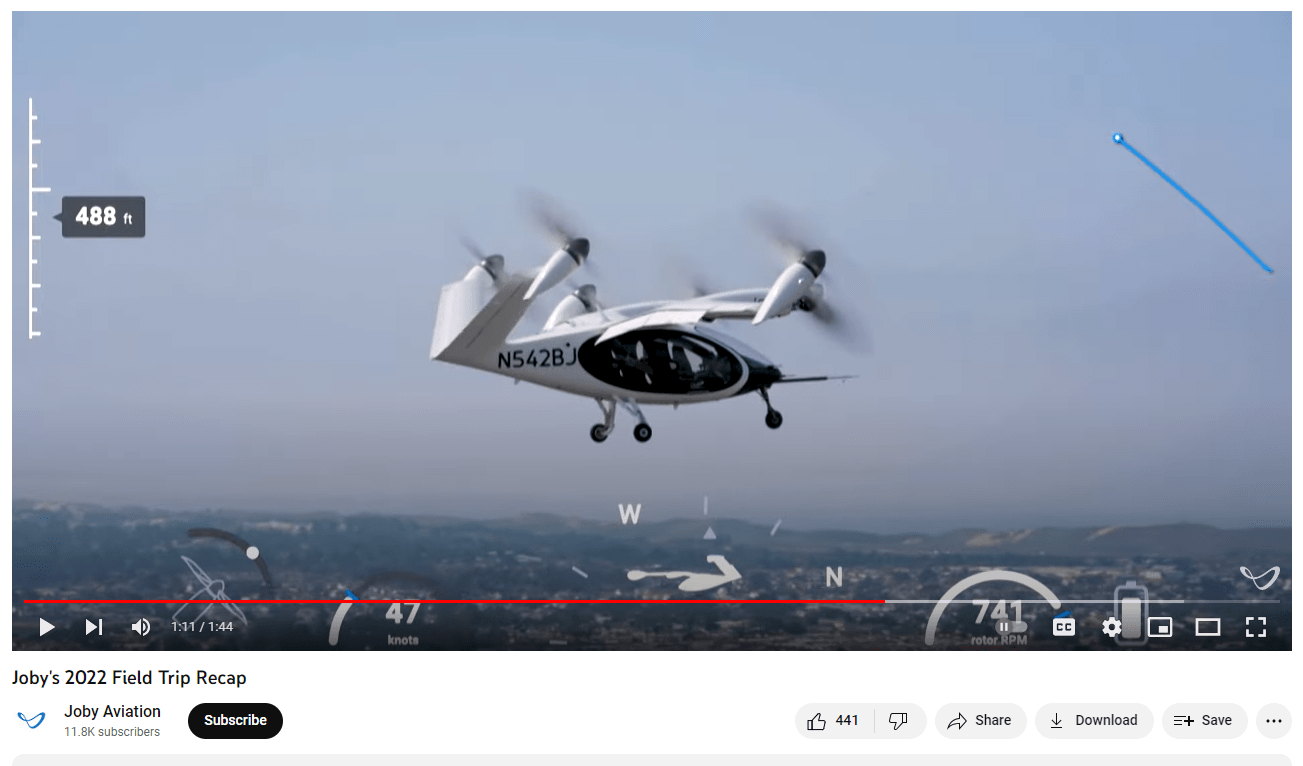

Currently there are no commercially operating eVTOLs in the US. This is because no eVTOL aircraft has yet received FAA approval for commercial flights. The company farthest along towards getting approval is California-based Joby Aviation ( NYSE: JOBY ) which received approval to begin test flights of its production eVTOL aircraft in June of 2023. Joby expects to receive approval for commercial operations in 2025.

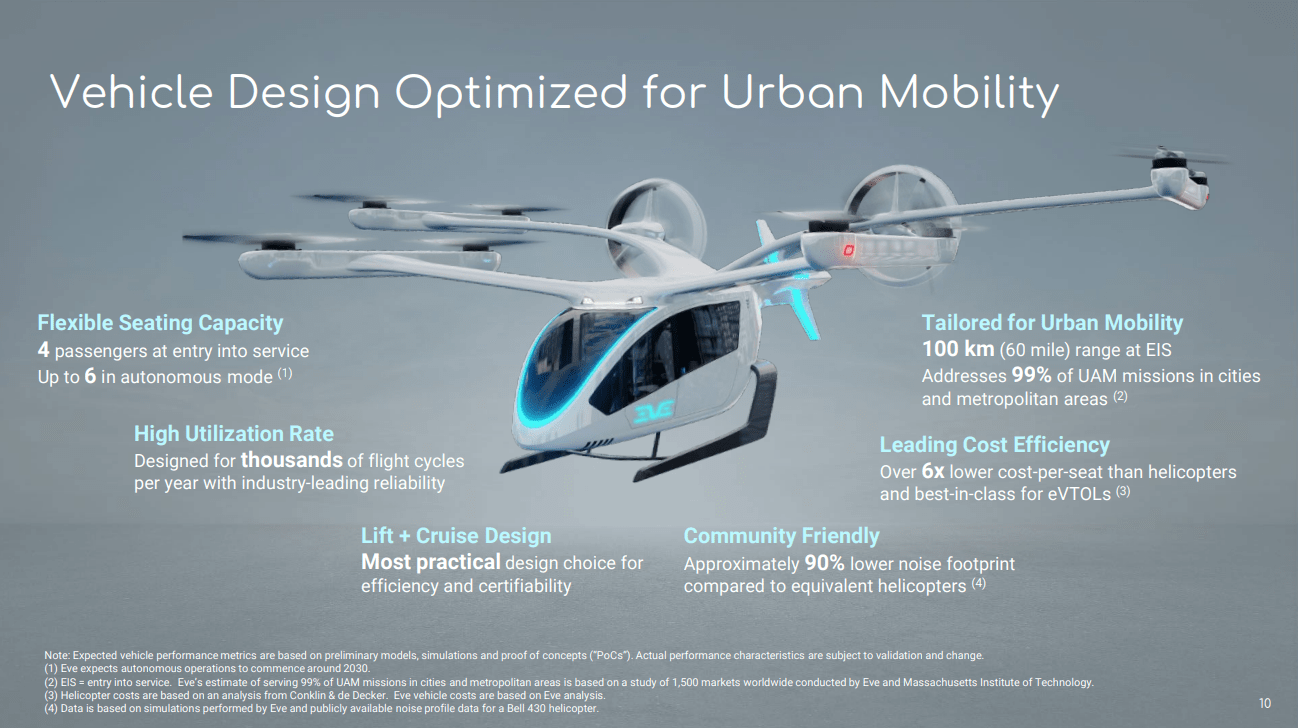

Eve is currently working on developing an eVTOL aircraft which will have a 60 mile range and the capacity to seat 4 passengers . There is a lot of interest for eVTOL aircraft across the aviation industry. Eve already has letters of intent for 2,850 aircraft worth $8.6 billion. This represents a purchase price of about $3 million per aircraft. Customers include airlines including United ( NASDAQ: UAL ) as well as helicopter operators like Blade .

Eve order backlog (Eve Air Mobility)

While the high customer interest is certainly a positive it’s important to note that these letters of intent are non-binding and the customers can cancel them at any time at no cost. And to fulfill any of these orders Eve first has to build the aircraft.

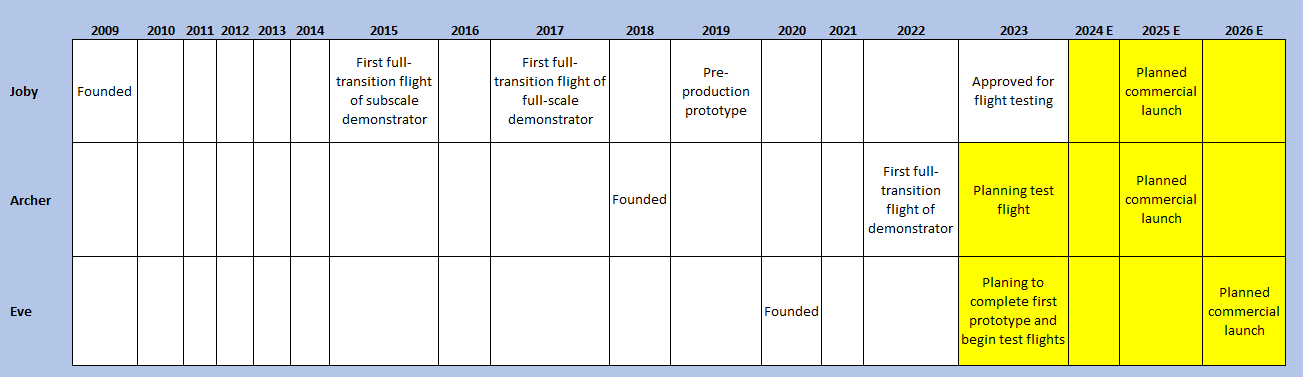

Development Timeline

Eve aims to assemble their first prototype in the second half of 2023, start test flights in 2024, and get certification to begin commercial operations in 2026 . While theoretically possible, I view this timeline as optimistic and at very high risk of delays. Let’s compare their development timeline with those of Joby Aviation ( NYSE: JOBY ) and Archer Aviation ( NYSE: ACHR ), which are Eve’s two largest publicly-traded competitors in the US. Joby and Archer plan to get certified and begin commercial operations in 2025. So Eve aims to be one year behind Joby and Archer. Now let’s look at the current aircraft from these three manufacturers.

This is what Joby’s aircraft looks like as of October 17th 2022:

{kind=link}

This is what Archer’s aircraft looks like as of December 20th 2021:

Archer eVTOL aircraft (Archer Aviation)

This is what Eve’s aircraft looks like as of May 11th 2023, the most recent image available:

{kind=link}

You don’t need a P.H.D. to see that both Joby and Archer are substantially ahead of Eve. Below I compiled the development timelines of the three manufacturers.

Development timelines (Eve Air Mobility, Joby Aviation, Archer Aviation, compiled by author)

{kind=link}

Of the three Joby is the only one that has been approved to begin test flights of its production prototype in 2023 . This comes 4 years after the successful flight of their full size pre-production prototype, 6 years after the first successful flight of their full-scale demonstrator, and 8 years after the first successful flight of their sub-scale demonstrator. They expect it will take another 2 years until they receive FAA approval to begin commercial operations in 2025 . Thus, in total they expect it to take 6 years (2019 to 2025) between completing the pre-production prototype and commercial launch. Not to mention the many years before that developing their demonstrator aircraft.

Archer completed the first successful flight of their demonstrator in 2022, 4 years after they were founded. In May of 2023 they finished assembly of their production prototype and aim to begin flight tests later this year. Flight tests have not yet been approved by the FAA. They also expect to launch commercial operations in 2025. If they make this target it would be 3 years in between when they demonstrated the first successful flight of their demonstrator and commercial launch. This is a far more optimistic timeline than Joby. It is also far more speculative as they have not yet received FAA approval to begin test flights of their production prototype.

Eve’s timeline is far more aggressive even than Archer’s. Eve doesn’t have a production prototype. They don't even have a demonstrator. Currently all they have is some propellers mounted on a truck. As of June 18th 2023 they still have not even chosen suppliers for critical components including flight-control systems, avionics, airframe and power-management systems. Yet they aim to have FAA approval for commercial launch in 2026! One reason Eve plans to go faster is because they’re skipping the demonstrator phase and going right to building the production prototype. While this can certainly save time it greatly increases the risk of unforeseen problems which could cause delays down the line. Eve has the advantage of their close relationship with Embraer which has substantial experience in getting airplanes approved. But Embraer has never before made an eVTOL. They have never even made a helicopter or any vertical take-off aircraft in the past. I personally view their timeline as way too optimistic.

It’s important to note that Joby is the only manufacturer with FAA approval to even begin test flights of a production prototype so their timeline is the most credible. I would put Eve’s current progress equivalent to where Joby was in 2015 when they flew their first subscale demonstrator, 10 years before their anticipated commercial launch in 2025. If anything this is being generous to Eve as they don’t even have a demonstrator. Let’s say that Embraer's expertise in traditional aviation allows them to double the speed of development to just 5 years. This would allow them to begin commercial operations in 2028.

Eve currently has ~$269 million of liquidity on their balance sheet. In the first half of 2023 they generated operating cash flows of negative $47 million. So let’s call the cash burn $100 million per year. If anything I would expect the cash burn to accelerate over time as they have to build out their assembly plants. But even at $100 million per year they will burn $500 million over the next 5 years. Thus, I expect they will need to raise additional capital before beginning commercial operations.

So let’s say in 2028 Eve finally launches commercial operations. How much will the business be worth then?

Unit Economics

The main expected use-case for eVTOL is passenger transport in urban areas. The most logical place to start is between airports and city centers. These routes have a high volume of passengers for a fixed trip. While this has never been done with eVTOL aircraft it has been attempted with traditional kerosine powered helicopters. In 2019 Uber ( NYSE: UBER ) launched UberCopter , a service that can take passengers from JFK International Airport to a fixed landing pad in lower Manhattan. Shortly after the program was launched, CNN sent a correspondent to test it out . The review was underwhelming. The ride cost $205, more than triple an Uber car ride which would have cost $61 and orders of magnitude more expensive than public transportation. The value proposition of the UberCopter is that the flight only takes 8 minutes, compared to 40 minutes for a car ride. However, CNN reported that the total trip length on the UberCopter was 55 minutes. So how did an 8 minute flight end up taking 55 minutes? It’s because they only have one specific drop-off point in lower Manhattan. Unless your destination happens to be within walking distance, you will have to take public transportation or a traditional Uber to your final destination. This defeats a lot of the purpose. While Uber has not disclosed the financial performance of UberCopter it was probably underwhelming. As of 2023, 4 years after the initial launch, UberCopter is still only operating in New York City . Had it been a resounding success I would expect them to have expanded to more cities.

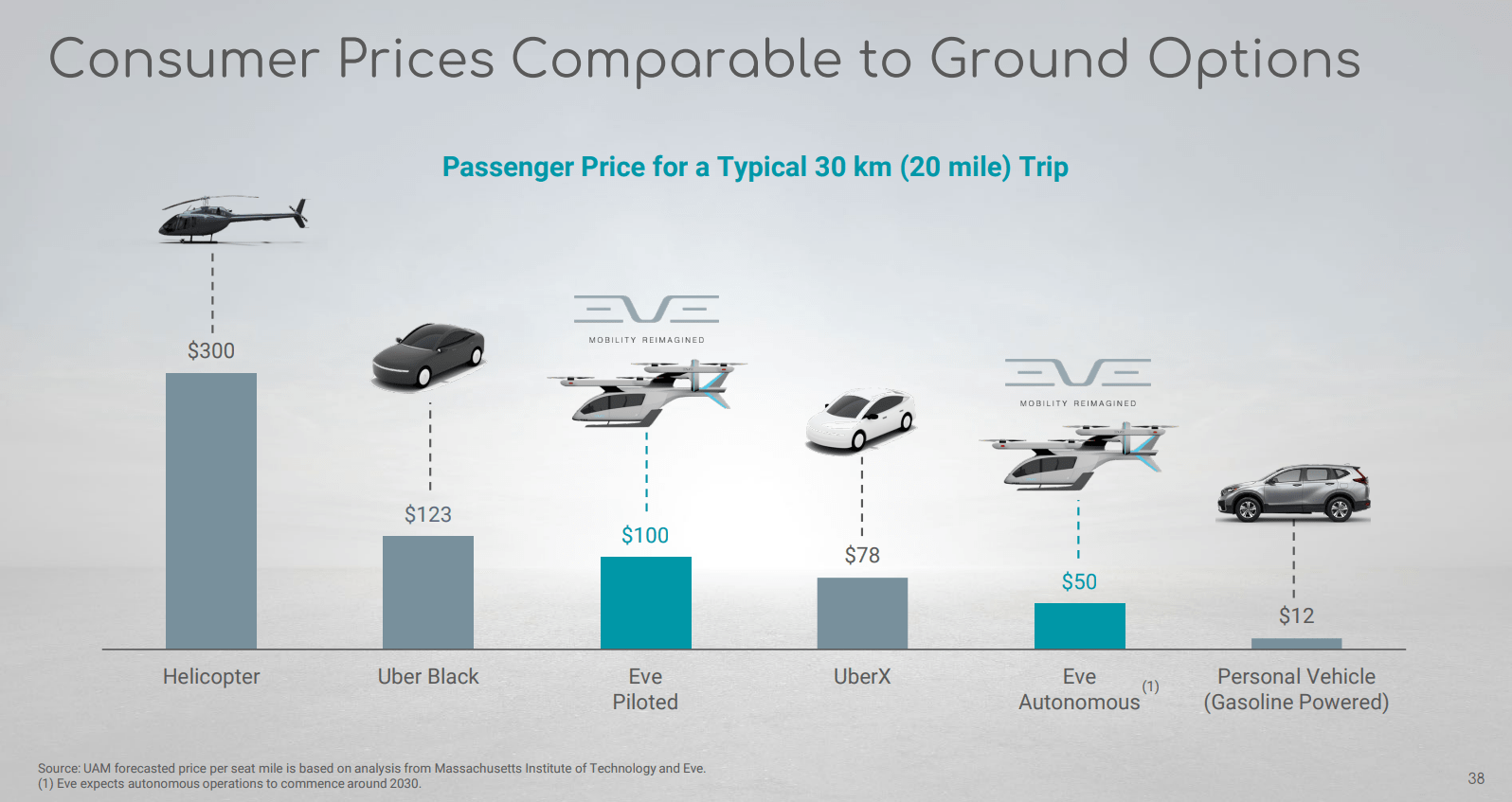

eVTOL’s will have the same problem because they too need a fixed landing pad. The only real advantage of the eVTOL over a traditional helicopter is that the eVTOL is simpler and cheaper to operate. eVTOL operators will attempt to outperform traditional helicopters by pricing their fares far lower. Eve expects a 20-mile ride, which is roughly the same distance between JFK and Manhattan, to be priced at $100, a little less than half of what UberCopter charges.

{kind=link}

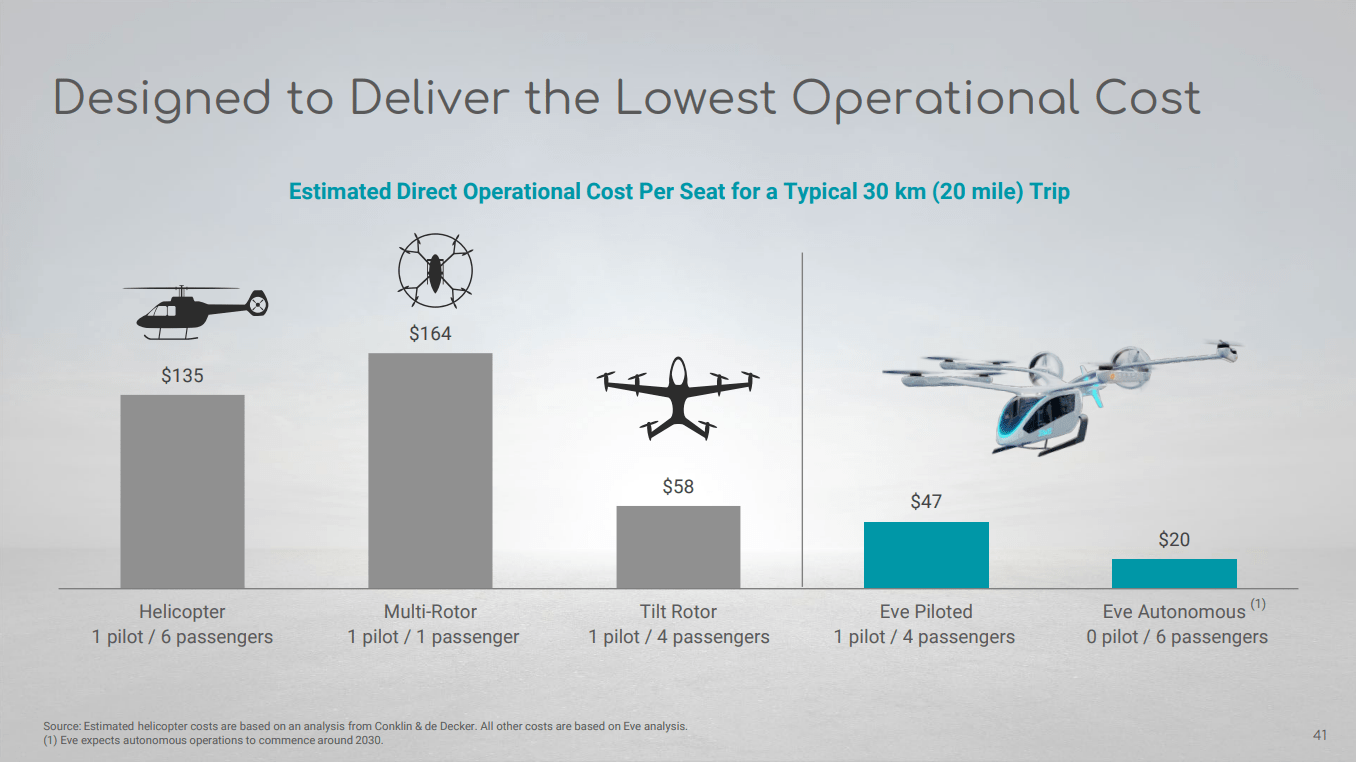

Eve expects the direct operating costs of their aircraft to be $47 per passenger, substantially cheaper than a traditional helicopter. They also expect to launch a fully autonomous aircraft by 2030. But this is so far in the future and so speculative that I’ll ignore it for our current analysis. $47 of direct costs is less than $100 of revenue. But the direct costs are not the only costs.

{kind=link}

There are a few issues. Firstly, the $205 UberCopter fight includes a traditional Uber ride from the landing spot to your final destination anywhere in Manhattan. So to be comparable we need to look at the price of the full trip, not just from JFK to the landing pad. The UberCopter lands at the Downtown Manhattan Heliport which is 7 miles and a 21 minute drive from Central Park. Assuming central Manhattan is where most people ultimately want to go, an UberX ride there would cost $22 based on current rates . Of course, you could use public transportation for much cheaper, but this would defeat a lot of the purpose. And we’re comparing it to an UberCopter ride which includes a last-leg Uber journey.

Heliport to Central Park (Google Maps)

So if the total trip is to cost the passenger $100, the eVTOL operator can only charge $78. Eve expects each aircraft will be able to fly 5,600 flights per year . To get so many passengers whoever operates the aircraft will have to utilize some type of network like Uber which will charge a commission. We don’t know what this commission will be because no such platform exists yet. Currently Uber charges a 20% commission on ride-hailing so let's assume this same rate. That will represent a $16 expense.

Next is the landing fee. The operator has to pay a landing / take-off fee both at the airport and at the heliport in Manhattan. The Manhattan heliport fee is $40 per person . I couldn’t find information on how much JFK charges for helicopter landing but I did find that the Miami International Airport charges a $24 landing fee per helicopter. With 4 passengers that’s $6 per passenger. Altogether that gets $46 per passenger in total landing / take-off fees.

Next is the direct operating cost. Eve says they expect $47 of direct operating cost per passenger. They don’t disclose what this includes but I assume it's little more than pilot salaries and electricity. The reason I believe this is they say the cost will only be $20 once they have fully autonomous aircraft. A large portion of that $20 will go to electricity and maintenance. So it’s inconceivable to me that landing fees are included. And again, for the purposes of this analysis we’re not considering fully autonomous aircraft.

The operator who buys the eVTOL aircraft from Eve needs to make a profit for it to be worth their while. Let’s assume a 10% cost of capital. The Eve aircraft itself has a list price of $3 million. But you also have to consider the cost of developing charging infrastructure. Super fast charging infrastructure does not yet exist at airports. We don't know how much this will cost to set up because eVTOLs are not in operations yet. The most analogous estimate I could find is a recent study from the University of Chicago which estimates it would cost $21 million to create a charging station for 100 electric semi-trucks, or $210,000 per truck. If anything the cost will be higher at an airport because of the limited available space. So let's assume $3.2 million of total capital costs knowing that this is probably an underestimate. At a 10% cost of capital the operator needs to make $320,000 of profit per year. Eve's aircraft will have a max capacity of 4 passengers per trip. But they will not always be full. According to the International Air Transport Association passenger aircraft generally achieve a passenger load factor of about 80% . If we assume the same for eVTOLs that translates to 17,920 passengers per year. Thus, the operator needs to make an $18 profit per passenger.

Next is depreciation. Commercial airplanes are typically depreciated over a useful life of 20 years according to a study by the International Air Transport Association . Let’s assume the aircraft and charging infrastructure have similar useful life spans. With straight-line depreciation that equates to 5% of the capital expenditure or $9 per passenger.

And finally the operator needs to cover their overhead costs and other miscellaneous expenses like insurance. Let’s assume corporate overhead is 10% of revenue, so another ~$8.

Estimated unit economics (Some data from Eve but mostly author assumptions)

Admittedly I used a lot of assumptions in the above calculations. But given that there is no commercially operating eVTOL business today this is unavoidable. If we run with my numbers, an eVTOL operator would need to charge $143 for the flight itself. Add $22 for the last leg Uber ride and you get $165, which is cheaper but not orders of magnitude cheaper than the UberCopter. And it's important to stress again that the eVTOL will still be slower than just taking an Uber car ride to your final destination in the vast majority of cases.

The core problem is that the only real advantage I see in eVTOL over traditional helicopters is the direct operating costs. But direct operating costs represent only a minority of total costs. Thus, I’m highly skeptical of some of the wildly optimistic projections we’ve seen like Morgan Stanley ( NYSE: MS ) predicting a $1.5 trillion urban air mobility market by 2040 .

Urban Traffic Management

In addition to developing eVTOL aircraft Eve is also working on an Urban Air Traffic Management (ATM) system. This is basically an air traffic control system but for eVTOL aircraft. This is in its early stages and they only just started conducting simulations this past May. Given my skepticism of the viability of the urban air mobility market as a whole I’m not terribly optimistic about this part of the business either. It’s also important to note that Eve is developing the Urban ATM system in partnership with its parent company Embraer. They signed a master services agreement where Eve will have to pay Embraer for the use of its intellectual property and other services. The exact terms of the master services agreement have not been disclosed. But to the extent that Eve’s Urban ATM generates revenue some unknown portion of it will ultimately go to the parent company.

Master Services Agreement with Embraer (Eve Air Mobility 2022 Form 10K)

{kind=link}

Competition

Notwithstanding my skepticisms about the core use case of urban air mobility there will be at least some demand for eVTOLs. At the very least some ultra high net worth individuals may want to buy them for their private yachts. But this market will likely be small and competition will be fierce. According to Electric VTOL News, there are over 350 companies developing over 600 different designs for eVTOLs. These competitors include Boeing ( NYSE: BA ) and Airbus ( OTC: EADSF ). There are also companies like Joby which is far closer to commercialization. With so many other options likely to come to the market before Eve there is a high risk that a large portion of their backlog will be cancelled. Remember, their $8.6 billion backlog consists entirely of non-binding letters of intent.

Verdict

It’s always hard to come up with a fair valuation for pre-revenue companies. But I think Eve’s current enterprise value of ~$2 billion is far too high given that it’s greater than the stub value of Embraer’s entire traditional airplane business.

I think there’s a big risk that competitors such as Joby may begin commercial operations and saturate the market before Eve achieves FAA certification. If this happens investors may lose confidence and Eve's ability to raise additional capital could be greatly impaired. Thus, in my opinion there’s a significant probability the company goes bankrupt before generating any revenue.

If Eve can execute on its extremely ambitious goal to complete and begin flight testing on its production prototype in 2024 I may change my bearish view. But I think this is unlikely to happen so I rate the stock a strong sell.

For further details see:

Eve Air Mobility: Way Too Early To Get Excited