JELD - Even After Surging Quanex Building Products Deserves Further Upside

2024-01-03 09:44:32 ET

Summary

- Quanex Building Products is a value investment opportunity with potential for additional upside due to its undervalued shares.

- The company has experienced mixed financial results, with a decline in revenue but an increase in operating cash flow and EBITDA.

- Despite uncertainties in the construction industry, Quanex Building Products is attractively priced compared to similar firms and has the potential for further growth.

One of the really great things about value investing is that, when you buy shares of a company that are drastically undervalued, you can experience tremendous upside and still the stock in question can warrant additional upside. Such is the case, in my opinion, when it comes to Quanex Building Products ( NX ). For those who are not aware, this enterprise focuses on the production and sale of components for OEMs in the building products market. Examples of products that it produces and sells include window and door components, kitchen and bath cabinet components, and more. It also produces solar panel sealants, trim moldings, vinyl decking, fencing, water retention barriers, and more.

Over the past year or so, this has not really been all that attractive a place to play in. A plunge and new orders and backlog associated with residential properties has proven to be a pain for pretty much any business that touches the home construction market. But as I have detailed in other articles, such as here and here , we are starting to see a nice recovery as evidenced by a surge in orders for new properties. Naturally, a firm like Quanex Building Products should benefit nicely. While financial results have been somewhat mixed as of late, the combination of shares being cheap and investors recognizing that the worst for the construction space is over, the picture for the company from a share price perspective has been fantastic. Since I rated the company a ‘buy’ back in September of 2022, shares have seen upside of 69.3%. That's more than double the 30.5% rise seen by the S&P 500. Even with that move higher, I would argue that additional upside is likely on the table. And because of that, I've decided to keep the company rated a ‘buy’ for now.

A great firm despite mixed results

In an ideal world, fundamentals for companies would improve year after year without exception. But in the real world, variability in results from one year to the next is common. Our prospect is actually a really great example of this. Consider revenue, for starters. In 2023, Quanex Building Products generated sales of $1.13 billion. That represents a decline of 7.4% compared to the $1.22 billion the company generated in 2022. While the enterprise experienced weakness across all three of its major operating segments, the biggest pain came from its North America cabinet division. Revenue of $215.4 million translated to a year over year decline of about 22% compared to the $275.7 million reported in 2022. About $10.8 million of the $60.3 million decline was driven by a reduction in prices that the company was able to pass on to its customers thanks to lower raw material costs. But $49.5 million of the drop was due to lower volume associated with soft market demand thanks to weakening consumer confidence.

{kind=link}

On the bottom line, the picture was most certainly mixed. Net profits actually went from $88.3 million in 2022 to $82.5 million last year. On the other hand, operating cash flow rose from $98 million to $147.1 million. If we adjust for changes in working capital, on the other hand, we would see that it remained flat at $134.8 million. Meanwhile, EBITDA for the business inched up from $152.5 million to $159.6 million. Any portion of this improvement seen was driven by a couple of factors. Even though selling, general, and administrative costs rose by 6% year over year and depreciation and amortization rose by 7%, the company reported a roughly 10% plunge in cost of sales do not only to lower volume, but also lower raw material costs and foreign currency fluctuations.

{kind=link}

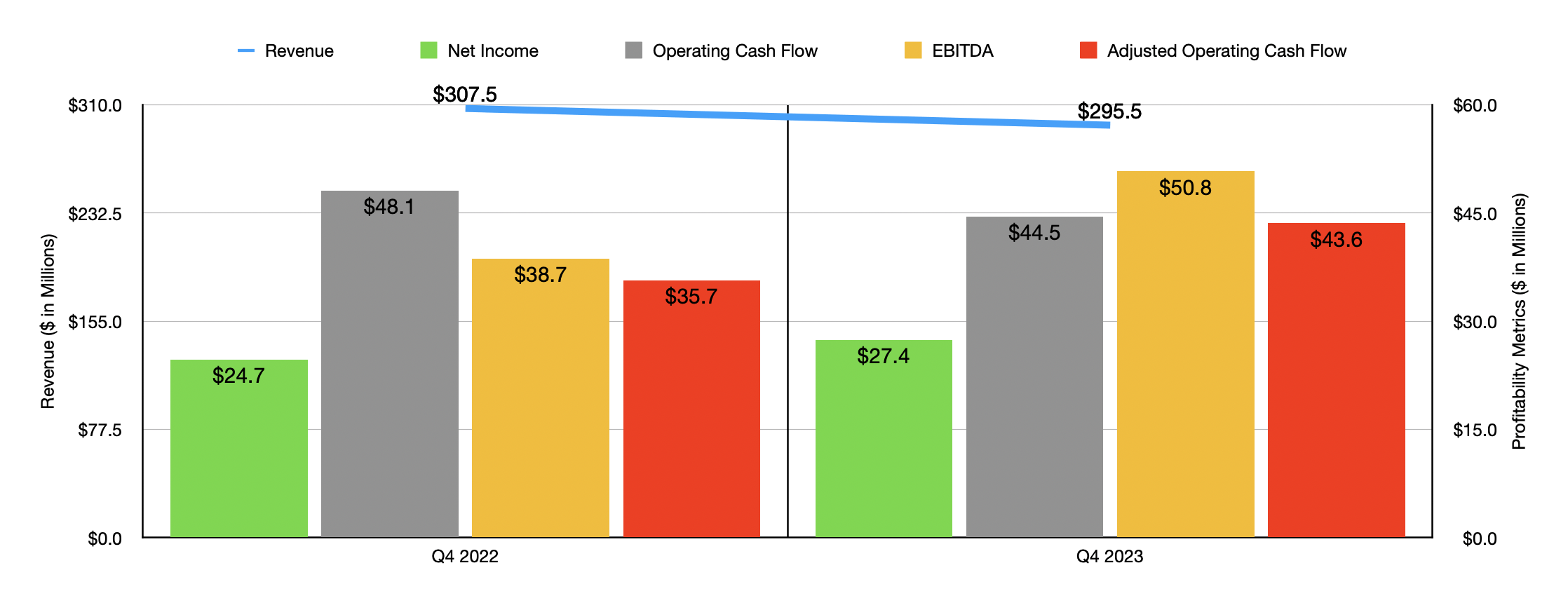

As you can see in the chart above, financial results for the final quarter of 2023, which were released on December 14th of last year, show that the mixed performance of the company has continued even to the present day. What is encouraging from this, however, is the bottom line. In addition to net profits coming in higher year after year in the final quarter, both adjusted operating cash flow and EBITDA are higher as well. As to whether or not this will continue, my own belief is that it will, but management has taken a more measured approach. The firm actually decided not to provide guidance for 2024 at this time. This is because they do think that the first half of the year might experience macroeconomic challenges, plus normal seasonal fluctuations are expected to weaken the company during that window of time. However, they do believe that demand will improve in the second half of the year thanks to a recovery in consumer confidence.

{kind=link}

This does, unfortunately, leave us a little empty handed. But the good news is that, even if financial performance matches with the company saw in 2022 or 2023, shares are attractively priced at this time. I say this because you can see the results as shown in the chart above for both years. Although the price to earnings multiple of the company could be cheaper, both of the cash flow metrics for each year look great. I then, as part of my analysis, compared the company to five similar firms as shown in the table below. On a price to earnings basis, only one of the five firms ended up being cheaper than our prospect. This number pops to four of the five if we use the price to operating cash flow approach. But when it comes to the EV to EBITDA approach, our target ended up being the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Quanex Building Products |

| 12.1 |

| 7.4 |

| 6.3 |

| Insteel Industries ( IIIN ) |

| 23.1 |

| 5.3 |

| 11.2 |

| JELD-WEN Holding ( JELD ) |

| 12.3 |

| 4.3 |

| 6.9 |

| American Woodmark Corp ( AMWD ) |

| 13.7 |

| 5.4 |

| 7.1 |

| PGT Innovations ( PGTI ) |

| 21.2 |

| 13.2 |

| 11.9 |

| Apogee Enterprises ( APOG ) |

| 11.3 |

| 6.5 |

| 6.8 |

Takeaway

As far as construction-oriented companies go, I definitely consider Quanex Building Products to be a solid prospect for investors to consider. In addition to shares being cheap on an absolute basis, they are also cheap relative to similar firms. Or at least that's the case using two of the three valuation metrics. Financial performance has been mixed. But we are seeing signs that the picture is beginning to improve steadily. Even if industry conditions flatline, I would argue that shares are cheap enough, both on an absolute basis and relative to similar firms, to warrant some additional upside from here. As such, I've decided to keep Quanex Building Products rated a ‘buy’ for now.

For further details see:

Even After Surging, Quanex Building Products Deserves Further Upside