SO - Even With End Of The Vogtle Saga Southern Co. Is A Hold

2023-06-25 22:23:00 ET

Summary

- Southern Company is a reliable utility company with a long track record of sales and EPS growth, leading to a reliable dividend.

- The company faces risks such as a high debt burden, increasing interest expenses, and inflation, which could limit dividend growth.

- The shares are currently unattractive due to their valuation, and it is recommended to hold unless the P/E ratio is around 16.

Introduction

As an investor in dividend growth stocks, I search for new investment opportunities in income-producing assets, mainly stocks. I try to add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The utility sector is interesting nowadays since it was used as a bond replacement for a very long time. Now that bonds are attractive again, some utility companies may see investors selling their stocks. Therefore, the dividend yield may become more attractive and offer long-term investors a decent entry point. In this article, I will analyze a utility company I own- Southern Company ( SO ).

I will analyze Southern Company using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

The Southern Company engages in the generation, transmission, and distribution of electricity. The company also develops, constructs, acquires, owns, and manages power generation assets, including renewable energy projects and sells electricity in the wholesale market, and distributes natural gas in Illinois, Georgia, Virginia, and Tennessee, as well as provides gas marketing services, gas distribution operations, and gas pipeline investments operations. In addition, it constructs, operates, and maintains 77,591 miles of natural gas pipelines and 14 storage facilities with a total capacity of 157 Bcf to provide natural gas to residential, commercial, and industrial customers.

Fundamentals

The revenues of Southern Company have increased by 72% over the last decade. It is a relatively fast growth for a utility, but yet still sums up to roughly 5% annually. The company grows sales as the population grows and people consume more energy. It is a regulated utility. Thus the tariff is controlled by the regulator. In the future, as seen on Seeking Alpha, the analyst consensus expects Southern Company to keep growing sales at an annual rate of ~ 1 % in the medium term.

The EPS (earnings per share) of Southern Company increased by 56% over the last decade. This is a slower growth rate compared to the growth in sales, even though the company improved its margins over the decade. The reason is that the company has issued shares and significantly diluted shareholders to fund its projects. Therefore, despite higher net income, a higher number of shares decreased the EPS. In the future, as seen on Seeking Alpha, the analyst consensus expects Southern Company to keep growing EPS at an annual rate of ~ 6 % in the medium term.

The dividend of Southern Company seems safe despite a payout ratio of 88% using GAAP EPS. The reason for that is that the non-GAAP payout ratio is 80%. While the second figure is also high, it is manageable for a utility company with a regional monopoly with predictive income. The dividend yield is attractive at almost 4%, and the company has a long track record of dividend increases for 21 years in a row.

Companies use buybacks in addition to dividends to return capital to shareholders. It supports EPS growth as it lowers the number of shares outstanding. As I mentioned in the paragraph about the EPS, the company dilutes its shareholders. The number of shares increased significantly by 25% over the past decade. The company had to issue shares to raise capital to fund projects and overruns such as the Vogtle project.

Valuation

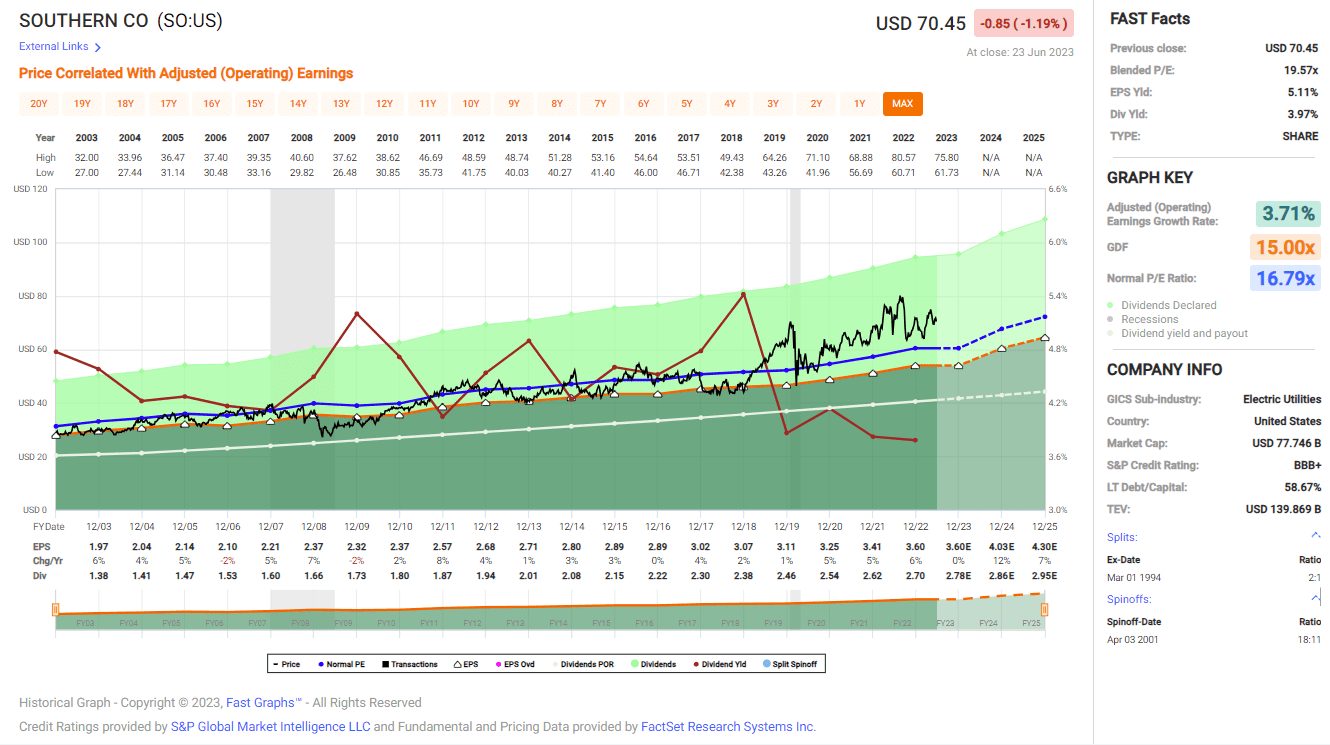

The P/E (price to earnings) ratio of Southern Company stands at almost 20 when using the forecasted EPS for 2023. This is an average valuation for the company over the last twelve months, as the price-to-earnings ratio climbs to 22 and then drops to 17. Paying 20 times earnings for a regulated utility with limited growth that manages to increase its EPS by 6% annually in the medium sound a bit expensive, especially when the interest rates are higher, and the risk-free interest is almost equal to the earnings yield of ~5%.

The graph below from Fast Graphs also implies that the shares of Southern Company are slightly overvalued. Over the last two decades, the average P/E ratio of the company was 17, and the current P/E ratio stands at 20. However, the earnings are growing at a faster pace compared to the company's history. EPS has grown at a 4% CAGR, and the current forecast is 6% CAGR. I believe it just fires some premium, yet the shares are still unattractive.

{kind=link}

Opportunities

The Vogtle Saga regarding the nuclear plant in Georgia is extremely close to its completion. Unit 3 has passed almost all the tests and is forecasted to be operational in July. Unit 4 is also progressing according to plan and will be in service by the end of the year or Q1 of 2024. This saga has cost the company billions of dollars, and investors paid for it by being diluted and having their EPS consumed by interest expenses. The bleed is about to stop, leaving the company with positive free cash flow for the first time since 2015.

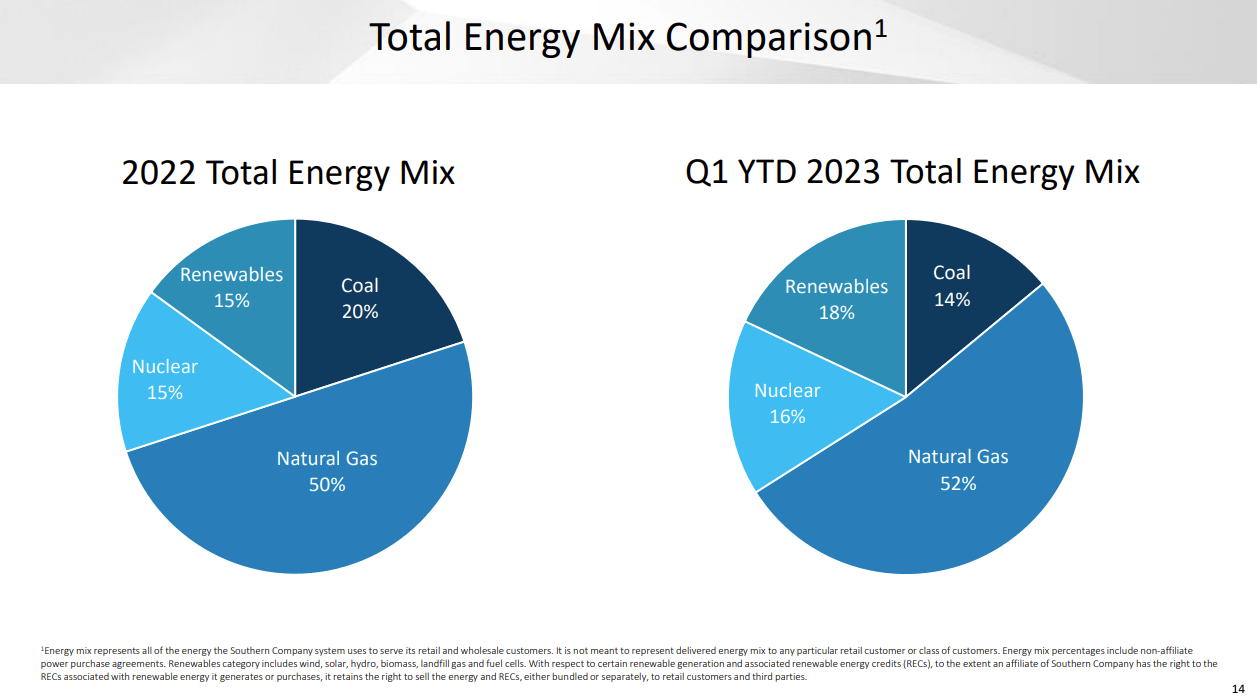

Another opportunity for Southern Company is its improved energy mix. The company is shifting its production from polluting fuels such as coal to less polluting fuels like natural gas and renewables. These investments benefit the company, as they help it become "greener," thus making it more favorable to regulators and consumers. More importantly, these investments justify rate increases from the regulators.

{kind=link}

Demographics and diversification are other growth opportunity. First, the company is active mainly in the southern part of the United States. This is a growing part demographically, mainly due to internal immigration. Moreover, the company will benefit from the shift towards electric vehicles, and its value proposition of natural gas and electricity will mean that it can grow its natural gas business with trucks and buses that use CNG (compressed natural gas) and its electricity business with electric cars.

Risks

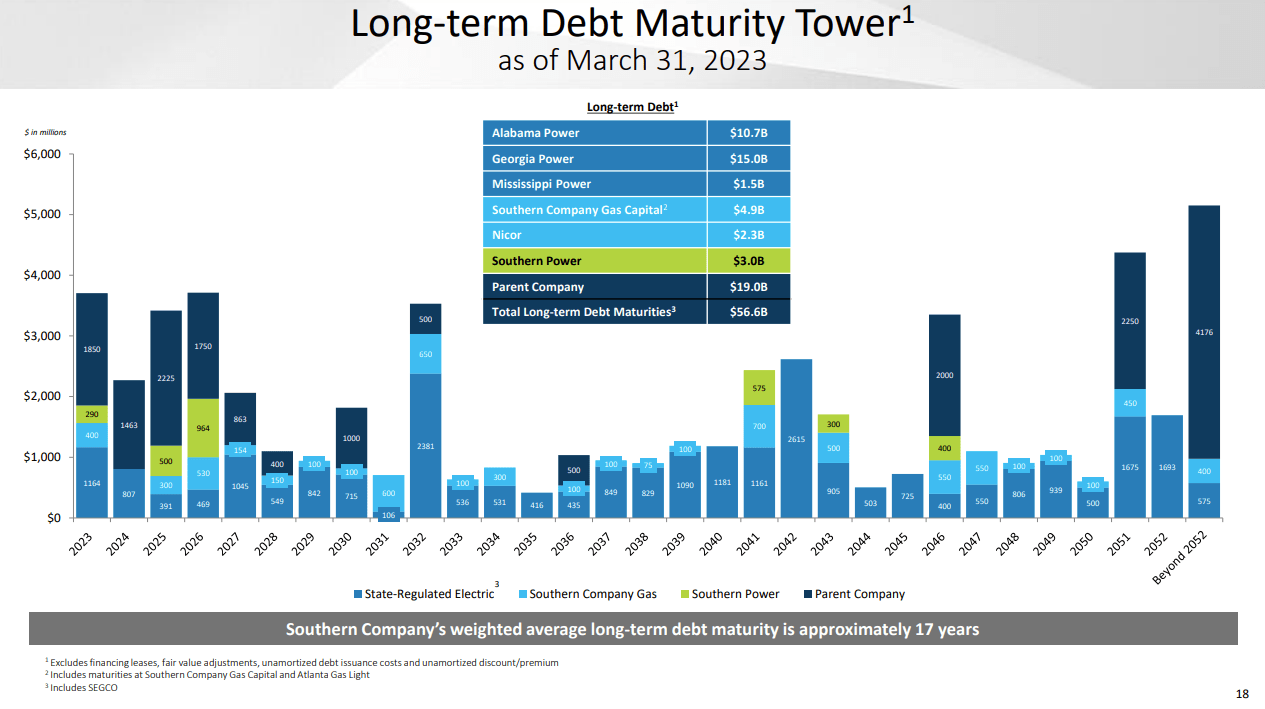

Debt load is a significant risk. A year ago, the total long-term debt was ~$52B, and now it is almost $57B, a 10% increase in just a year. The debt load limits the company's growth ability as the debt-to-EBITDA ratio reached 5.4. Therefore, the company has to grow by issuing more shares and diluting investors. The billions of dollars financed in the coming years will bear higher interest rates as rates are higher today.

{kind=link}

The margin of safety that Southern Company offers investors is extremely low. The shares are not overly expensive, but there is no significant margin of safety if the company doesn't execute well. At a P/E ratio of almost 20, the shares seem fully valued and even trading for a slight premium. This is especially true when we consider that interest rates have increased over the last two years, making it harder to justify such a small margin of safety.

Inflation is another risk for Southern Company, and it's a more profound risk for the company as it cannot quickly increase prices. Inflation makes it more expensive to generate electricity, yet unlike other sectors, utility companies need regulatory approval to raise prices. Regulators do not want to be seen helping firms raise prices during inflationary periods, so they may try to postpone it for as long as they can.

Conclusions

To conclude, Southern Company is a reliable utility company with a long track record of sales and EPS growth that led to a reliable dividend. The company is finally putting the Vogtle saga behind it, and it will be able to achieve free cash flow again. Moreover, the company will also enjoy the growth in the usage of electric vehicles and the demographic growth in the southern United States to increase its earnings.

However, the company is trading for a valuation that I believe is still unattractive. It sells for a premium when there are still risks to the investment thesis, mainly revolving around the extremely high burden of the debt and the increasing interest expense, which will limit dividend growth. While risk-free interest is around 5%, the shares are not attractive enough, and I believe it is a HOLD unless the P/E ratio is about 16.

For further details see:

Even With End Of The Vogtle Saga, Southern Co. Is A Hold