EB - Eventbrite: Outlook Just Got A Lot More Brighter After Q2 2023 Earnings

2023-08-17 05:18:28 ET

Summary

- Eventbrite reported strong 2Q23 earnings with revenue of $78.9 million, close to the high end of its guided range, and an adjusted EBITDA of $11.3 million.

- Management raised the FY23 revenue guidance and introduced a new monetization tool for event organizers, which I expect to enhance profitability and drive growth.

- The implementation of the new fee structure may cause disruptions and increased organizer churn, but it showcases the management's innovative approach to revenue generation.

Summary

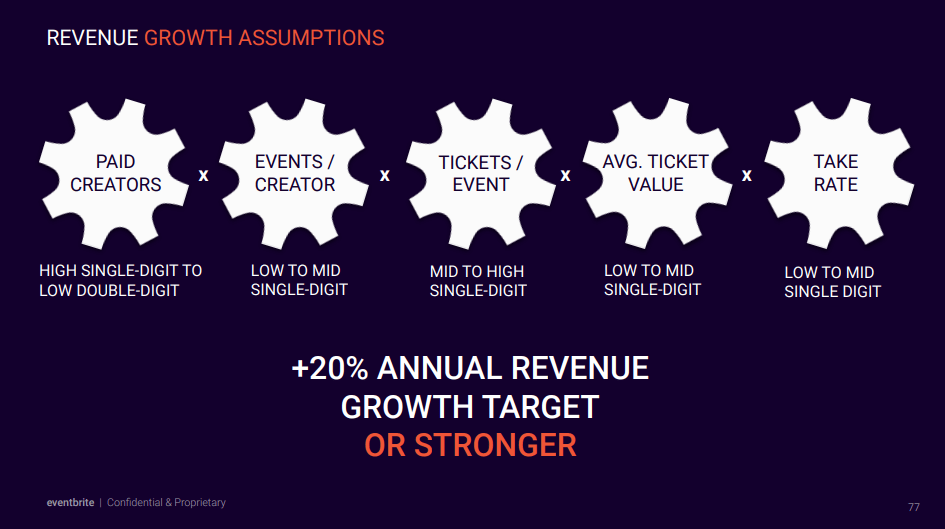

Eventbrite ( EB ) is a one-stop solution for: (1) Creators to manage events, ticketing, and marketing (2) End-consumers to discover events and purchase tickets. Generally serving small to mid-size events. Revenue and profits are mostly earned from fees earned through paid tickets. Readers may find my previous coverage via this link. My previous rating was a buy , as I believed EB's valuation was attractive at 2x forward revenue, and that performance thus far was encouraging for its future growth trajectory. I am reiterating my buy rating for EB as it continues to execute well and grow as planned. Moreover, I see the new monetization tool announced during the call as a catalyst that could drive growth in the near term, further supporting my view of EB’s 20% growth.

Financials / Valuation

EB reported its 2Q23 earnings results with revenue coming in at $78.9 million, close to the high end of its guided range, growing 19.5%. Adj. EBITDA came in at $11.3 million, implying a 14% margin. The strong results led to a revision in guidance, in which management raised the FY23 revenue guide. Specifically, management raised the low end of the FY23 revenue guide from $317 million to $330 million to $320 million to $330 million.

Based on my view of the business, EB should be able to grow revenue at 20% for the foreseeable future (based on management growth target listed during the investor day presentation in 2022), and the EBITDA margin should expand accordingly as well. When these happen, I expect the market to rerate the EB multiple back to its historical average of 3.6x forward revenue, translating to a share price of $20.

Based on author's own math

{kind=link}

Comments

EB's 2Q23 revenue was in line with consensus projections, but EB's adjusted EBITDA beat was a clear indication that it is headed in the right direction, producing more profits. Furthermore, the revision of FY23 guidance was clearly a positive takeaway from the earnings. Using the median of the FY23 revenue guide and the 3Q23 revenue guide ($79 million to $82 million), it suggests a possible sequential acceleration from 3Q23 to 4Q23, as mentioned above. Also noteworthy is that EB has increased what I believe to be a conservative FY23 adj EBITDA margin guide of 12%–13% from 10%. By all accounts, EB is performing admirably, as evidenced by growth in the 20% range and a marked increase in EBITDA margin (both sequentially and year over year). Assuming the same increase in EBITDA margin from 2Q22 to 2Q23, it implies an EBITDA margin of >13% in 3Q23.

In my opinion, EB will be able to maintain its 20% annual revenue growth and on-track expansion of EBITDA margins with the implementation of the new organizer fee. Starting in 2Q23, EB will roll out a new packaging framework that will provide creators, both free and paid, with access to all available features. This also includes the for-fee use of EB's marketing resources. Similar to the way fees are applied in different online marketplaces, the recently introduced fee for event organizers will be structured into two options , and the cost will change based on the quantity of tickets sold for each specific event. The Flex plan is a pay-as-you-go option with no minimum ticket requirement and a maximum fee of $49.99 per event. The Pro plan is a monthly subscription service with a starting price of $29 for up to 100 tickets per event and a maximum price of $159 for unlimited tickets per event, making it ideal for creators who plan multiple events per month.

These can be viewed as a "levy" for the use of EB's marketing tools, but they provide a substantial increase in profit over the previous free model. Given the easy comps (3Q22–2Q23 do not have this fee in place), I expect the impact to EB financials to be significant from an ARPU perspective, acting as a near-term catalyst to drive y/y growth acceleration from 3Q23–2Q24. What's more, I think this is a testament to the management's ability to creatively find ways to make money off of their offerings. Nonetheless, I recognize that implementing a new fee structure may cause disruptions, and I anticipate that this will manifest itself in increased organizer churn.

Overall, I really like the progress so far. However, one aspect that I am paying attention to is the bridge between EB’s adj. EBITDA and its GAAP EBITDA. GAAP EBITDA is still near zero at this point, and a large part of the gap is stock-based compensation [SBC]. As of 2Q23, SBC is still near 20% of revenue, which is insanely high. As such, I would recommend investors size their positions correctly, as the dilution impact is huge if SBC continues at this pace.

Risk & conclusion

I believe EB will be negatively impacted if any new entrants or existing players gain significant traction in the near future, even though competition is not yet as strong as EB at this time. If EB's SEO (organic search engine rankings) were to drop, it would likely increase the cost of traffic for a given growth rate, as the company relies heavily on these rankings.

Overall, EB 2Q23 earnings indicate a positive outlook, with strong revenue growth and improved EBITDA margins. The upward revision of FY23 guidance and the introduction of a new monetization tool for event organizers are noteworthy developments. I expect the new fee structure to enhance profitability and act as a catalyst for accelerated growth from 3Q23–2Q24. Despite potential disruptions and increased organizer churn, this strategic move showcases the management's innovative approach to revenue generation.

For further details see:

Eventbrite: Outlook Just Got A Lot More Brighter After Q2 2023 Earnings